Don’t Count Out Copper Yet

-

Ed D'Agostino

Ed D'Agostino

- |

- August 6, 2024

- |

- Comments

Ed D'Agostino

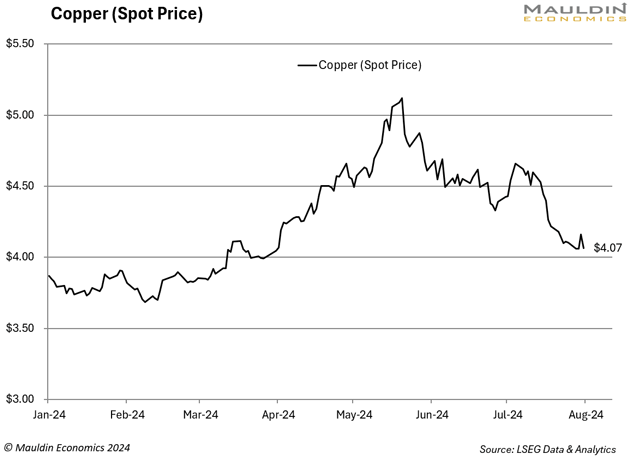

Ed D'AgostinoCopper prices have pulled back since peaking in May at $5.12, but the long-term bull case for copper remains strong.

Much of the copper story comes down to electricity. Copper is essential to meeting electricity demand, which is expected to grow 13% here in the US by 2030 (though my hunch is this is an underestimate). The IEA anticipates electricity consumption for artificial intelligence, data centers, and crypto alone doubling by 2026.

Just this morning, the US Department of Energy announced a new $2.2 billion investment in the US power grid. Worldwide, grid capacity will need to double by 2050 to meet increased electricity demand. This will require an additional 427 million metric tons of copper. Even in China, where the economy has cooled considerably, electricity demand is still expected to jump 5.1% this year.

This will all drive copper demand, as will electric vehicles (EVs), both in the US and in fast-growing emerging markets like India. EVs use up to 4X more copper than gas-powered cars, and hybrids use around twice as much. Then there’s the copper needed for manufacturing and construction… copper supports nearly every segment of the economy.

All told, the IEA sees global copper demand increasing twentyfold by 2040. Where will all this copper come from?

|

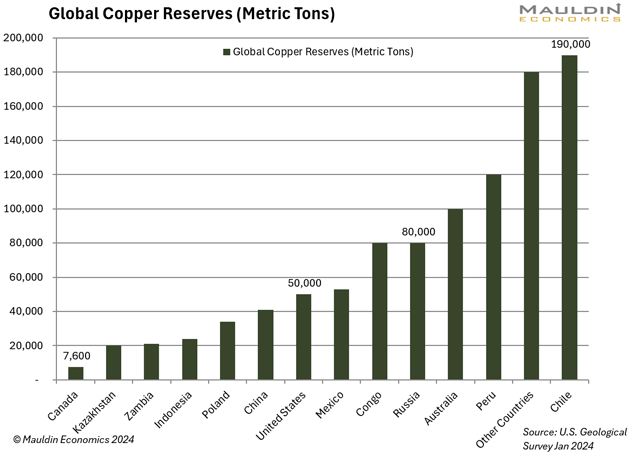

Around 65% of identified copper sits in the ground in five countries: Chile, Australia, Peru, Mexico, and the US. Chile has the greatest copper reserves, followed by Peru.

Last year the US produced an estimated 1.1 million tons of copper, or 11% less than it had in 2022, with around 70% of that coming from Arizona.

Globally, copper miners have ramped up production every year for the past 20 years. And not long ago, analysts thought a supply deficit was years away. Those forecasts quickly changed last November, when Panama ordered First Quantum Minerals Ltd. to halt operations at the Cobre Panama mine, which accounted for 1.5% of global production in 2023. This coincided with strike-driven interruptions at the Las Bambas mine in Peru, which normally produces roughly 2% of the global copper supply.

Copper production in Chile ended up sinking to a 15-year low last year, while output at the world’s largest copper mine dropped 8.4% to a 25-year low.

Now the consensus is that a copper supply deficit could happen this year. Looking ahead, the IEA says existing copper mines, as well as those being developed, will only be able to meet 80% of copper demand by 2030. Goldman Sachs projects a 5Mt deficit by then.

Miners like Rio Tinto, BHP Group, and Southern Copper are all working on new projects. But opening a new mine is a slow and cumbersome process. Two weeks ago, I noted that it takes around 16 years to bring a nuclear power plant online in the US, but that’s a breeze compared to the two decades it can take to get a new copper mine up and running.

Planning for this is imperative to improving economic resiliency. There is a national security component to the copper story, too, since it’s used in munitions, the tactical EVs the US Army plans to incorporate, and other military applications. There’s a reason China, which imports 60% of globally traded copper, has been boosting its stockpile.

The Democratic Republic of Congo (DRC) moved ahead of Peru to become the second-largest copper producing nation in 2023. Notably, all the leading producers there, save for Glencore, are Chinese companies: CMOC Group, China Minmetals, Zijin Mining Group, Jinchuan Group International Resources.

This makes it all the more concerning that copper does not show up on the unclassified list of the National Defense Stockpile. As the world continues to electrify and become increasingly multipolar, China, Russia, and other nations in their spheres of influence (including the DRC), may hoard and dominate access to critical commodities like copper. The US and its allies should be building up their own caches, too.

The recent market volatility underscores the need for caution. The best way to play this may not be miners, but other pick-and-shovel-type opportunities, of which there are many. We are eyeing one that we plan to add to the Macro Advantage portfolio soon. More details on how to join us here.

|

Thanks for reading.

Ed D’Agostino

Publisher & COO

Tags

Suggested Reading...

|

|