Double Debt Problem

-

John Mauldin

John Mauldin

- |

- November 23, 2018

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinUnderstated Problem

Endless Guarantees

Comorbid Crises

Houston, Puerto Rico, Cleveland, and Boca Raton

The selloff in GE is not an isolated event. More investment grade credits to follow. The slide and collapse in investment grade debt has begun… (and later) Don’t be fooled by bond prices holding up, because trading volumes are down. There are fewer bids in the market, and the dispersion of bids is wider. It is time to jog—not walk—to the exits of credit and liquidity risk.

- Scott Minerd, Guggenheim Partners Chief Investment Officer

From a 50,000-feet viewpoint, we're probably in a global debt bubble…Global debt to GDP is at an all-time high…This is going to be a very challenging time for policymakers moving forward.

- Paul Tudor Jones at the Greenwich Economic Forum in Connecticut, November 15, 2018

Last week, I talked about Ray Dalio’s new book on debt cycles. He describes how debt is inherently cyclical, because it enables more spending now that must be offset by less spending later.

Ray’s book helped me refine my description of The Great Reset. It’s a critical refinement, too. After reading the book, I realized it is entirely possible we will have another debt crisis before what I think of as The Great Reset. I firmly believe the latter is still coming, but there may be another “mere” credit crisis beforehand.

Understated Problem

In last week’s letter, we began reviewing Ray’s book called Principles for Navigating Big Debt Crises in which he examines those debt cycles and what we can do about them. The book is a must-read resource for anybody who wants to understand the economic and financial world we are living in and what increasingly looks like another debt crisis around the corner. I read it on my recent trip to Frankfurt, and I highly recommend you do the same. (That link is for Amazon, but you can also get a free PDF copy here. I read it on my Kindle so I could highlight and save notes.)

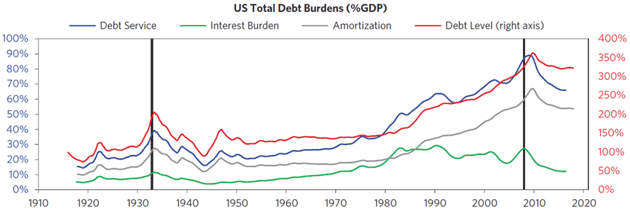

I referred to the section I bolded below, promising a deeper dive, which we will do today. I’ve included some preceding text and chart for context.

The chart below shows the debt and debt service burden (both principal and interest) in the US since 1910. You will note how the interest payments remain flat or go down even when the debt goes up, so that the rise in debt service costs is not as great as the rise in debt. That is because the central bank (in this case, the Federal Reserve) lowers interest rates to keep the debt-financed expansion going until they can’t do it any more (because the interest rate hits 0 percent). When that happens, the deleveraging begins.

While the chart gives a good general picture, I should make clear that it is inadequate in two respects: 1) it doesn’t convey the differences between the various entities that make up these total numbers, which are very important to understand, and 2) it just shows what is called debt, so it doesn’t reflect liabilities such as pension and health care obligations, which are much larger. Having this more granular perspective is very important in gauging a country’s vulnerabilities, though for the most part such issues are beyond the scope of this book.

Source: Ray Dalio

Close to the beginning of the book, Ray tells us that his debt cycle descriptions are just that: a description of past debt cycles. He excludes government liabilities like pensions and healthcare that, which while not technically “debt,” look and act just like it to those who are planning on it. People assume those payments will appear. If they don’t, then some sort of deleveraging, default, or liquidation process must occur. It will be painful to everyone.

Ray clearly knows about the government debt problem but compartmentalizes for the sake of analysis. The book looks specifically at private-sector debt and how it interacts with the economic cycle. Government debt is a different problem with different characteristics. But as we all know, it’s still debt, as most of us think of debt: an obligation that must be paid in the future... and it is definitely still a problem.

The fact that government pensions and obligations are not on the balance sheet doesn’t change the fact that millions of people around the world expect to get them. Those future payments are part of their retirement planning, every bit as much as a 401(k) or other savings. For most people, at least in the United States, it is almost all their retirement planning. Without those payments already-bleak retirement prospects would look even worse. So it’s hard to overstate their importance.

Endless Guarantees

Let’s review how big this problem is.

The US government on-budget deficit was $100.5 billion in October. It was $63.2 billion in the same month a year earlier. There are always revenue timing issues comparing any previous months, but that’s the wrong direction. I see little hope it will reverse. There is no appetite in Congress or the public for lower spending. Nor will we see the kind of tax-policy changes that would generate more revenue. (I still think my VAT idea is the best answer, but I’m way out on a limb there.)

Federal debt has grown with little complaint (except from a few of us curmudgeons) because it was mostly painless over the last decade. Interest rates and inflation were historically low, and the Federal Reserve was buying Treasury bonds by the truckload. Those helpful factors are now changing. Last year, interest on the federal debt was $263 billion, or 1.4% of GDP. The Congressional Budget Office expects it will rise to $915 billion by 2028, or 3.1% of GDP.

Let’s stop right there for a minute. You can review the CBO’s budget outlook here. The interesting numbers start about page 43, and then the actual projected deficits at page 84. The total projected 2028 deficit (on and off budget) is $1.5 trillion. Take that number with a grain of salt; they were only projecting the total debt for this year (2018) to increase $779 billion, when it actually rose $1.2 trillion including off-budget items. The CBO also assumes no recessions, wars, or other crises in the next 10 years.

And yet they still project, even with optimistic assumptions, that interest on the debt will overtake defense spending plus other “discretionary” expenses. It is quite likely that fiscal 2019 will see a $1.5 trillion deficit (assuming no recession), and that if (when) we have a recession, total debt will increase at least $2 trillion a year. Considering that we are already at $23 trillion of total debt, it is very likely that by the mid-2020s we will have $30 trillion worth of debt and already see that $915 billion interest expense they were projecting for the end of the decade.

And that’s not all. Look back at my June 29, 2018 “Unfunded Promises” letter for some staggering numbers on the various non-debt obligations that our political heroes have placed on “We the People” beyond Social Security and Medicare. They’ve made lots of other guarantees, explicitly or not.

For example, consider the Pension Benefit Guaranty Corporation, which stands behind thousands of private defined-benefit retirement plans. The plans pay premiums but not enough to cover the number of failures we could see in a severe recession and debt crisis, much less the Great Reset.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

If we learned anything from 2008, it is this: Congress will open the national wallet in a crisis, even if it means creating new guarantees out of thin air. They did it with TARP, the Troubled Asset Relief Program. No such program was anywhere on the radar until the big banks wobbled. If, say, some large state pension plans can’t meet their obligations, will Congress face similar pressure to fund the gap? You bet it will, and I have little doubt what will happen.

Now, if you are a Keynesian you might think that’s ok. The government is supposed to stimulate the economy through troubled times. But Lord Keynes also advised us to run surpluses in growth periods, so we could afford the stimulus. We haven’t, except briefly two decades ago. So even if the Keynesian path works, we are already way off of it.

As bad as all this is, however, I think Ray Dalio is right to analyze it separately from the more “normal” debt crises. That was the most important revelation for me in reading his book. We have two different problems that may or may not overlap.

Comorbid Crises

Physicians have an unpleasant-sounding term called “comorbidity.” It is as bad as it sounds. It is when two separate health conditions affect a patient simultaneously. They might be related but are medically distinct problems. Heart disease and diabetes often go together, for example. Evaluating them separately is important in making treatment decisions.

Such is the case with our debt disease.

- We have a big problem with private-sector debt, with many overleveraged corporations likely to default if the economy weakens.

- We have another big problem in government debt and unfunded liabilities, with politicians making commitments the taxpayers can’t keep.

Both problems are serious. To some degree they overlap, because the government draws its funding (whether taxes or borrowing) from the same population and wealth pool as private borrowers. But they are distinct problems we should analyze separately.

There may be at least a little bit of good news in this. Since these are distinct problems, maybe they won’t explode at the same time. That would make each one more manageable.

We saw this in 2008, in fact. Subprime mortgages and related derivatives led to contagion in commercial paper. As terrible and frightening as it was, the Federal Reserve was there as a backstop. So was the US Treasury. We had a lot to worry about, but I don’t recall anyone seriously thinking the government would collapse. (Whether it did the right things is a different question.)

Will the same happen next time? We should all hope so. I’m skeptical because federal debt is now roughly twice as big a percentage of GDP as it was in 2008. The Fed’s balance sheet is considerably larger, too. They have less room to maneuver, but maybe they’ll find some new tools.

Nevertheless, at some point the government will hit a debt wall and probably drag private debt down, too. That will lead to what I think of as actually the Great Reset. But we could have one (or more) smaller debt crises first.

The Great Reset will occur when global government debt grows so large that merely rolling it over becomes a problem. It will crowd out private lending, forcing interest rates higher, which is definitely not good for economic growth. Or else the government resorts to “unusual actions.” In either case, a private debt crisis at the same time could be really painful…

At some point, the private market will just not be able to fund such massive debt increases. Then we’ll have a “crisis” and the government will resort to “unusual actions.” Like Congress authorizing the Federal Reserve to buy Treasury debt.

That’s not crazy. The Bank of Japan is doing it right now. The BOJ has well over 140% of Japanese GDP on its balance sheet. It is now, like the Swiss National Bank and the ECB, buying equities and private debt in order to push money into the economy, with seemingly no consequences.

And so maybe that’s what the US will do. But once politicians and voters realize they can tap the central banks, will there be any motive to balance the budget? Maybe not, unless monetizing the debt creates yet another crisis.

One of the debt crises that Dalio describes in detail is the German Weimar Republic and the hyperinflation of that period. Germany was monetizing the government debt that they assumed from World War I. I’d like to ask Dalio whether he chose that particular debt crisis as a warning about what happens when governments play around with printing money.

It is very difficult to predict the path The Great Reset will take. We can’t know what the political environment will be as technology begins to eat into the employment rate. Will increasing productivity reduce consumer prices or will inflation rise? If it’s the latter, will the Fed react by raising rates and trigger a Volcker-style recession? Will Congress order the Fed to monetize the debt? Like I said, 2008 clearly showed that Congress and the executive branch will do almost anything in the midst of a panic to avoid accepting pain.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

But in economic jargon, that yawning government debt chasm will have to be “rationalized.” Retirees and others receiving government benefits will expect to keep receiving them. There is no political will to reduce those benefits. The money will be found; the question is where? Hint: not under the sofa cushions.

When you begin to “wargame” the problem, the options are both limited and severe. Japan’s experience of Japan, even though it is apples and oranges to the US and Europe, will be so enticing. Just authorize the central bank to print money. When the world’s two main currencies begin to monetize debt at a significant rate—more than the small percentage of GDP that occurred in 2008–2009—and when that world is in a global recession, which is by definition deflationary, what will the consequences be?

The answer is we don’t really know. We only have economic theory as a guide, and we know how theory works in a crisis. I will admit that I have trouble imagining that whatever happens will be less than painful, no matter which theory you adhere to.

Dealing with too much debt, even debt of the “merely” promised kind, always involves some kind of pain to someone, and more likely to everyone, leaving nobody happy.

But that’s a story for another letter. To be continued…

Houston, Puerto Rico, Cleveland, and Boca Raton

I have a quick last-minute trip to Houston for one night next week, then back to Dallas for more meetings. Shane and I will be going to Puerto Rico in early December, then to Cleveland for a complete checkup with Dr. Mike Roizen at the Cleveland Clinic along with my friends Mike West and Pat Cox. I can envision some very interesting dinners. Then in late January, I go to Boca Raton to speak at an investment conference.

Quick anecdote from my time in Frankfurt. I spoke for fund manager Lupus Alpha to approximately 250 pension fund managers, representing most of Germany’s retirement monies. I asked for a show of hands on whether they liked being part of the European Union. Almost everyone raised their hands. I then asked if they thought participating in the euro was a good thing. Probably 80% raised their hands. When asked who doesn’t like the euro, maybe 10% of the hands went up.

Then the money question. I asked if they would be willing to take Italy’s debt and all the debt of every eurozone member and put it on the European Central Bank balance sheet, with caveats about controlling national budgets. Fewer than 20% of the hands went up.

I then engaged the audience further, saying, the last two questions were essentially the same. If you want to keep the euro, you’ll have to do something about the imbalances between the countries and debts. No monetary union in history has ever survived without becoming a fiscal union as well. Even reminding them that failure to do this might cause the euro to break up and bring back the Deutschmark didn’t seem to change many opinions. I reminded them that a Deutschmark would mean a serious recession/depression in Germany as it would raise the price of all German exports by at least 50%. Mercedes and BMWs are expensive enough for Germany’s customers, let alone at a 50% price hike.

This audience should have easily accepted the argument for putting all European debt on the ECB balance sheet. Imagine if I asked the typical German voter, especially those in rural areas. That tells me Europe could have a bumpier future than I thought.

My mind is still reeling with the implications of that impromptu survey. That’s going to be a letter someday. I invite comments from my European counterparts about what they think of that process in their own countries.

It’s time to hit the send button. I hope your Thanksgiving week was as great as mine, as I had all my kids over and many of my grandkids. I made prime rib, mushrooms, and all the fixings, accompanied by smoked turkey… and I even made a banana nut cake. (He does macroeconomics and bakes too!)

I always enjoy the season as it is a good time to get together with friends. And I always enjoy spending time with you in this letter. Thanks for taking the time to be with me.

Your really thinking about the future analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.