China’s Minsky Moment?

-

John Mauldin

John Mauldin

- |

- March 22, 2014

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinA Front-Row Seat

The Bubble That Is China

China’s Minsky Moment?

The Bigger They Come…

Cafayate, South Africa, New York, Europe, and San Diego

In speeches and presentations since the end of last year, I have been saying that I think the biggest macro problem in the world today is China. China has run up a huge debt, and the payments are coming due. They seem to be proactive, but will it be enough? How much risk do they pose for the global system?

This week as I travel to Cafayate I have asked my young associate Worth Wray to write up his research and our conversations on China. Worth has lived in China; and with his (and my) access to people with their fingers on the pulse of China, he has come up with some valuable insights. The hard part for him was to keep it in a single letter. China is a such a huge topic that writing about it can easily yield a tome.

I am lucky to have enticed Worth to come to work with me. He is extraordinarily talented and insightful as an economist, has the boundless energy of youth (which means he seemingly doesn’t sleep), and spent the last five years deep in one of the best training grounds that a young analyst could have. He brings his own extensive Rolodex to our organization. In the not too distant future, we plan to start writing a joint letter on portfolio design and construction, translating the macro insights we have into real-world portfolios that can inform your own investing. Lots of I’s to dot and T’s to cross, but we are making progress.

I am delighted to be able to bring a talent like Worth to your attention. So let’s let him talk China to us and see where it takes us. [Note: as I do the final edits here in Cafayate, I see that Worth did an outstanding job of bringing the data together and making the story understandable. You want to take the time to read this!]

By Worth Wray

Before I teamed up with John last July, I worked as the portfolio strategist for an $18 billion money manager in Houston, TX that, among its other businesses, co-managed (with an elite team of investors from the university endowment world) one of the largest registered funds of funds in the United States.

For a bright-eyed kid from South Louisiana, it was a life-changing experience. I had a front-row seat for every investment decision in a multi-billion-dollar portfolio for almost five years; and along with my colleagues and mentors in Texas, North Carolina, New York, Shanghai, and Singapore, I had the chance to meet and interact with a long list of the most sought-after hedge fund, private equity, and venture capital teams. I often found myself in the same room with honest-to-god legends like Kyle Bass, John Paulson, JC Flowers, and Ken Griffin … and I forged lasting some friendships with their portfolio managers and analysts.

As you can imagine, the information flow was addictive. I spent thousands of hours poring over manager letters from six continents, doing my best to connect the global macro dots ahead of the markets and coming up with question after question for everyone who would return my calls. That experience plugged me in to an enduring network of truly independent thinkers, forced me to see the world from an entirely different perspective, and put me in an ideal position to figure out what it takes to navigate the unprecedented (not to say strange) investment challenges posed by a “Code Red” world.

Sometimes, combing through a mountain of manager letters felt like reading the newspaper years in advance. I remember watching with amazement as a free-thinking global macro investor named Mark Hart made a fortune for his investors by shorting US subprime mortgages and then shifted his focus to what he argued would be the next shoe to drop – a series of sovereign defaults across the Eurozone.

Mark explained how the launch of a common currency had allowed historically riskier borrowers like Portugal, Ireland, Italy, Spain, and France to issue sovereign debt for the same borrowing cost as Germany did… without any kind of fiscal union to justify the common rates. The resulting debt splurge led to a big increase in fiscal debts, drove an unwarranted rise in unit labor costs across the southern Eurozone, and essentially activated a ticking time bomb at the very foundations of the euro system. It seemed obvious that rates would eventually diverge to reflect the relative credit risks of the borrowers, but the market didn’t seem to care until it got very bad news from Athens. We all know what happened next.

Just as Mark and his team at Corriente Advisors had predicted, spreads blew out in Greece, then in Ireland, then in Portugal, then in Spain… and it now appears that Italy and France are veering toward a similar fate. When the euro crisis finally broke out, my colleagues and I were waiting for it, because Mark had already walked us through his playbook for a multi-act global debt drama.

Instead of blowing up in spectacular fashion, the Eurozone crisis has taken far longer to resolve than a lot of investors and economists expected (Mark, John, and myself included); but the euro’s survival thus far has been largely the result of extensive Realpolitik and an increasingly hollow narrative from Mario Draghi and the ECB laying claim to the wherewithal to “do whatever it takes” to preserve the single-currency system. Meanwhile, as Corriente understood, the likelihood of major defaults across the Eurozone rises every day that the ECB does the bare minimum to resist France’s and Italy’s slide toward deflation. It’s not over until the fat lady sings.

The point I am trying to make is that Mark saw the fundamental imbalances behind the global financial crisis in time to launch a dedicated fund in 2006, and he saw the root causes of the ongoing European debt crisis in time to launch a dedicated fund in 2007… precisely because he thinks of the global economy as one interconnected system peppered with a series of unstable and still unresolved debt bubbles. Mark is one of the most forward-thinking investors I have ever met and one of the best in recent decades at spotting the big imbalances that spell T-R-O-U-B-L-E.

I can’t tell you if he will be right about the next phase of the global debt drama. Predicting the actions and reactions of elected and unelected officials is next to impossible in a Code Red world, but some people have an eye for fundamental imbalances. And since Mark has been largely right in identifying the major debt bubbles that have plagued the world since 2007, John and I can’t comfortably ignore his warning.

As Carmen Reinhart and Kenneth Rogoff argued in their still-authoritative history of financial boom and bust over the past eight hundred years, “When an accident is waiting to happen, it eventually does. When countries become too deeply indebted, they are headed for trouble. When debt-fueled asset price explosions seem too good to be true, they probably are.”

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Following his prescient calls on the subprime debacle and the European debt crisis, Mark identified in 2010 another source of instability that he warned could shake the global economy. And it took me by surprise. He warned that China was in the “late stages of an enormous credit bubble,” and he projected that the economic fallout when that bubble burst could be “as extraordinary as China’s economic outperformance over the last decade.”

To my knowledge, Mark Hart and his team at Corriente were the first of many global macro managers to anticipate a hard landing in the People’s Republic of China. Mark argued that the Middle Kingdom would land very hard indeed, popping speculative bubbles in the property and stock markets, sending foreign capital flying out the door, and triggering a rapid collapse in the renminbi … and even if the Chinese government could manage its economy away from a deflationary bust, they would be forced to devalue the renminbi to do so. In other words, Mark saw a much lower renminbi under almost every outcome.

It was a mind-blowing concept to me that the main driver of global growth (at the time) could not only implode but even drag the rest of the world down with it.

I can’t share the original Corriente China presentation with you for legal reasons, but here are a few public notes published by the Telegraph’s Louise Armistead after she attended one of Mark’s presentations in November 2010. These may look like obvious observations today, the sort you can find plastered all across the internet, but very few people were actually paying attention four years ago. And the data has only gotten worse since 2010 as rampant credit growth and insidious shadow lending have continued to fuel greater and greater capital misallocation.

In the presentation, which amounts to a devastating attack on the prevailing belief that China is an engine for growth, the financier argues that ‘inappropriately low interest rates and an artificially suppressed exchange rate’ have created dangerous bubbles in sectors including:

Raw materials: Corriente says China has consumed just 65pc of the cement it has produced in the past five years, after exports. The country is currently outputting more steel than the next seven largest producers combined – it now has 200m tons of excess capacity, more that the EU and Japan's total production so far this year.

Property construction: Corriente reckons there is currently an excess of 3.3bn square meters of floor space in the country – yet 200m square metres of new space is being constructed each year.

Property prices: The average price-to-rent ratio of China's eight key cities is 39.4 times – this figure was 22.8 times in America just before its housing crisis. Corriente argues: “Lacking alternative investment options, Chinese corporates, households and government entities have invested excess liquidity in the property markets, driving home prices to unsustainable levels.” The result is that the property is out of reach for the majority of ordinary Chinese.

Banking: As with the credit crisis in the West, the banks’ exposure to the infrastructure credit bubbles isn’t obvious because the debt is held in Local Investment Companies – shell entities which borrow from Chinese banks and invest in fixed assets. Mr Hart reckons that ‘bad loans will equal 98pc of total bank equity if LIC-owned, non-cashflow-producing assets are recognised as non-performing.’

The result is that, rather than being the ‘key engine for global growth’, China is an ‘enormous tail-risk’.

(Louise Armistead, The Telegraph, “Hedge fund manager Mark Hart bets on China as the next ‘enormous credit bubble’ to burst.” Nov. 29, 2010)

The markets may damn well prove Mark right, along with a host of other managers who either jumped on his bandwagon or reached the same conclusions independently; but it seemed downright crazy in 2010 to think that the main driver of global growth could abruptly become its biggest threat within a few short years.

On a personal note, I obsessed over China’s culture, economy, and political system for years in college and then witnessed the country’s transformation firsthand during my time at Shanghai’s Fudan University in the summer of 2007. Then and later, I marveled at China’s strength relative to the developed world and the seemingly invincible central government’s ability to keep the economy chugging along with credit growth and fixed investment while it hoped for the return of its developed-world customers then mired in the Great Recession.

It wasn’t what I wanted to hear … but I had to accept that Mark could be right. He had clearly identified a major imbalance which has continued to worsen over the last few years, and now we are just waiting for the next shoe to drop.

Four years later, Chinese production is slowing in the shadow of a massive credit bubble and in the face of aggressive reforms.

Disappointing investment returns are revealing broad-based capital misallocation; property prices are cooling (relative to other countries); and commodity stockpiles are mounting.

With China’s new policy of allowing defaults (historically, China’s default rate has been 0%), there is a real risk that follow-on events could spin out of control, raising nonperforming loan ratios and sparking a panic as bank capital is significantly eroded.

In the meantime, the renminbi is trading down, most likely due to an intentional effort by the People’s Bank of China to aid in the slow unwinding of leveraged trade finance.

Now the signs of a Chinese slowdown (and thus a global one, as the world is geared to 8% Chinese growth) are clear, and people around the world are meeting uncertainty with emotion. With that in mind, let’s dig into the data that really matters and try to get to the heart of China’s dilemma.

“China is like an elephant riding a bicycle. If it slows down, it could fall off, and then the earth might quake.” – James Kynge, China Shakes the World

After 30 years of sustained economic growth topping 8% and a successful bank cleanup in 2000, the People’s Republic was well on its way to blowing through the “middle income trap” and transitioning to a more advanced consumption-based economy. But then in 2008 the banking crisis in the United States abruptly ushered in a painful era of balance sheet repair across the developed world and delivered a demand shock to emerging markets. Rather than allow the Chinese economy to fall into recession at such an inconvenient time, the Party leadership sprang into action to stimulate demand with its largest fiscal deficit in more than 60 years and to mobilize bank lending with historically low interest rates and enormous liquidity injections.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

As you can see in the charts above, China’s total debt-to-GDP (including estimates for shadow banks) grew by roughly 20% per year, from just under 150% in 2008 to nearly than 210% at the end of 2012 … and continued rising in 2013. Even more ominous, corporate debt has soared from 92% in 2008 to 150% today against the expectation that China’s government would always backstop defaults. That makes Chinese corporates the most highly levered in the world and more than twice as levered as US corporates, just as corporate defaults are happening for the very first time in more than 60 years.

By another measure, China has accounted for more than $15 trillion of the $30 trillion in worldwide credit growth over the last five years, bringing Chinese bank assets to roughly $24 trillion (2.5x Chinese GDP) and prompting London Telegraph columnist Ambrose Evans-Pritchard to tweet John and me a short message: “China riding tail of $24 trillion credit tiger. Tiger will eat Maoists.” And to that, I would respond that I hope the tiger doesn’t find its way to France. (You can follow John and Worth on Twitter at @JohnFMauldin and @WorthWray.)

Looking further into the debt problem, China is steadily incurring more and more credit for less and less growth – suggesting that the newer debt is less productive because it is being put to unproductive uses – as you can see in Chart 2 above. That explains why many analysts believe China’s official reported nonperforming loan ratio of 1% is more like 11% – or more than 20% of GDP.

Furthermore, China’s incremental capital/output ratio rose from 2.5x in 2007 to almost 5.5x in 2012. That means it takes more than twice as much debt to generate a given improvement in growth as it did before the debt binge began; and as an aside, the interest burden on China’s total debt, at 9.2%, is higher than in the US in 1929 and near the peak interest burden in 2008. Moreover, debt-service costs in China are more than double the total interest burden seen at any time in the last 100 years of US history.

China’s massive debt build-up since 2008 looks like the perfect recipe for a particularly destructive banking crisis; but as George Soros explains, “There are some eerie resemblances with the financial conditions that prevailed in the US in the years preceding the crash of 2008. But there is a significant difference, too. In the US, financial markets tend to dominate politics; in China, the state owns the banks and the bulk of the economy, and the Communist Party controls the state-owned enterprises.”

It will be a difficult balancing act, but China’s ruling elite doesn’t appear to be in denial about its debt problem, as we have come to expect from the United States and the Japan of old. In fact, it seems the new government under President Xi Jinping is intent on popping the domestic debt bubble and allowing widespread defaults rather than continuing to leverage the system into an unmanageable crisis or a Japanese-style stagnation. The trouble is, their efforts may be too little too late to manage a gradual deleveraging from a massive debt bubble. They are about to perform a dive off the high board that has never been attempted, with the whole world watching.

Among the various reforms set forth in last November’s Communist Party Third Plenum, ranging from financial liberalization to a crackdown on corruption and pollution, the greatest challenge will be gradually deleveraging the Chinese economy without throwing growth into a tailspin. Wei Yao and Claire Huang at Societe Generale argue that the Chinese government must approach the deleveraging process in three steps:

The first step is to stall credit growth – especially the growth of risky lending – so that overall leverage rises at a slower pace. In order to achieve this, Beijing has to stick to stringent monetary policy. The market has got a bitter taste of this. Since the beginning of the year, the People’s Bank of China (PBoC) and financial regulators have issued a slew of policy-tightening measures on local government off-budget borrowing, cross-border arbitrage flows, bank WMPs and the interbank bond market. These measures were intended to limit the supply of easy liquidity – mostly from the interbank market – for speculative uses and risky shadow bank lending. In early June, interbank liquidity conditions started to tense up as these measures took effect. The PBoC at first adopted a surprisingly tough stance and held off on liquidity injections, which resulted in unprecedented interest rates spikes. We would agree that this approach lacks elegance and the central bank could have been more communicative, but it was a strong signal that policymakers disapproved of all the risky lending behaviour plaguing the system. This is nonetheless a difficult stance to maintain when economic growth slows, given that credit growth has been used as a policy tool by the Chinese government to stabilize short-term economic growth.

The second step is to keep rolling over (a majority of) bad debt. This may be a necessary evil. If stalling credit growth caps the upside on economic growth, rolling bad debt should limit the downside, at least in the near term. The purpose is to avoid sparking a series of corporate bankruptcies, and economic growth can also do its part in deleveraging. Particularly in the case of infrastructure debt, keeping existing projects going can help manufacturers’ supply glut from going wider, and some projects, once completed, may eventually generate cash flow.

In addition, an improving global economy is likely to invite a return of export demand.

The third step is to start NPL disposals bit by bit. Many companies in China are probably unable to even support interest payments on their debt. If the financial system were to keep all of them alive, the percentage of financial resources that goes into the efficient part of the economy would only decline. This is essentially the lesson we can learn from Japan’s lost decades – the economy struggled to grow due to the large number of zombie companies in the system. Therefore, China needs to let bad projects fail and failing companies disappear to make space for efficient ones.

(Wei Yao & Claire Huang, “Asian Themes: Deflating China’s credit bubbles.” Societe Generale; September 19, 2013)

If President Xi Jinping, his Politburo comrades, and the People’s Bank of China can work together to slow credit growth, roll over the majority of bad debts, and gradually start disposing of the worst nonperforming loans, they may have a small, but not hopeless, chance of avoiding the difficult choice between a forceful deleveraging and footing the bill to backstop defaults and/or bank failures that could pile up toward 20% of GDP. That increasingly likely scenario would seriously disrupt real GDP growth along with China’s annual budget.

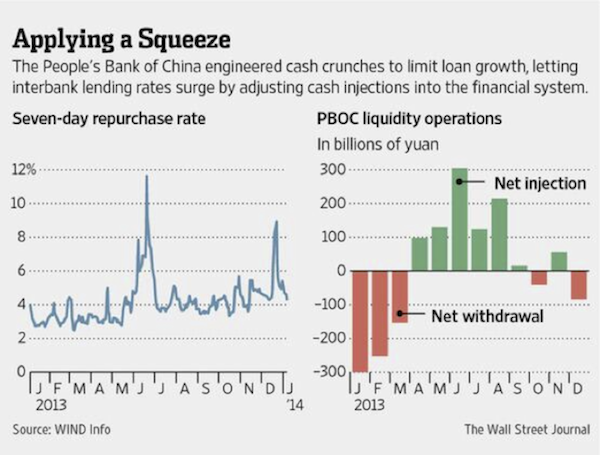

Trouble is, the People’s Bank of China has allowed some pretty wicked cash crunches over the past year. Some say it was an intentional move to discipline the shadow banking system. That scenario scares the hell out of me, because that kind of behavior suggests the Chinese are playing a dangerous game – and not just with their own economy. Interbank rates do not normally bounce from 2% to 12% in a healthy economy.

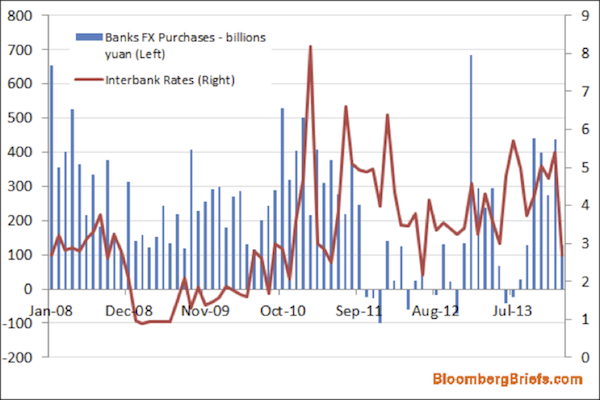

In the chart below from Bloomberg, it appears that fluctuations in FX flows may explain a lot of the easing and tightening happening in the interbank market. I suspect this is a clear sign that the PBoC may already be losing control.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

For all practical purposes, with China’s corporate debt above 150% and total debt above 210%, history suggests that China’s Minsky Moment is quickly approaching. Investors should prepare for the inevitable demand shocks and fall in global growth regardless of the specific outcome. The Chinese government may have the assets to backstop a truly horrific crisis and maintain slow growth in the 2-3% range; but then again, Mark Hart may have the final word.

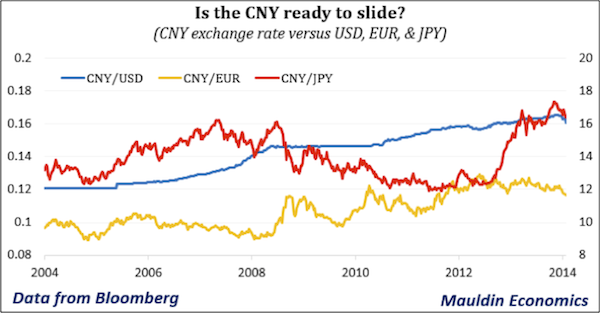

Four years on, the denouement has clearly taken longer to arrive than Mark expected, but he is still in the market with his Corriente China Opportunities Fund. And he is still betting big against the yuan, which continues to surprise and slide.

With so much of the market expecting one-way appreciation in the RMB/USD – despite a crescendo of warnings of currency volatility from the PBoC – such moves represent a big surprise and may simply be the first steps down.

China’s government finds itself on the exact opposite side of the carry trade now, and it appears they have a lot to gain by unwinding it – on the order of $200 billion for every 10% devaluation in the CNY/USD. It’s essentially a way to join the currency war and boost exports without appearing to circumvent the free market.

Contrary to what many onlookers believe, the People’s Bank of China and China’s top leadership are probably not willing and possibly not able to defend the currency while also supporting growth in a deleveraging economy. They will have to make a choice, and frankly, they already have an incentive to let the renminbi fall as they attempt to put the right reforms in place to support long-term growth – or face a deflationary nightmare in the uncomfortably near future.

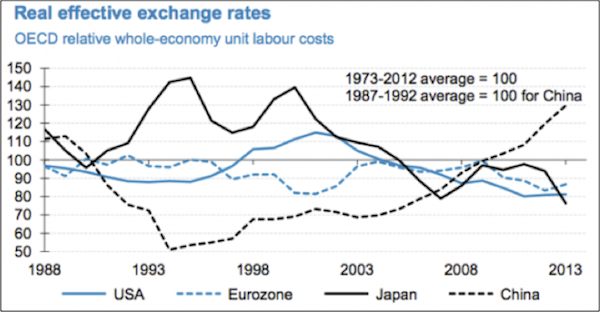

Not many people realize that China has lost a great deal of competitiveness as its real effective exchange rate has risen in recent years.

Source: OECD

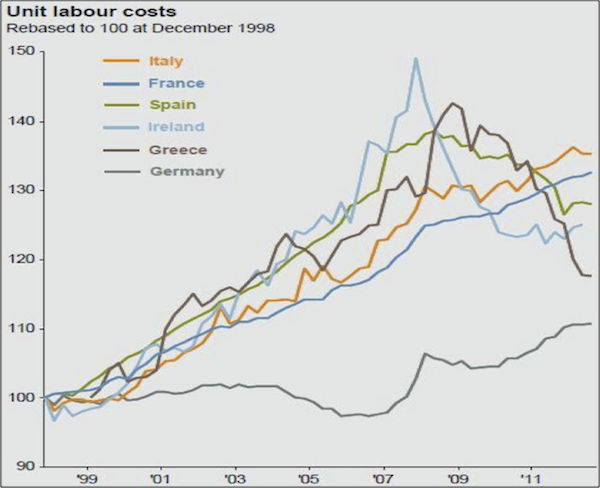

This is the same kind of dynamic that made Ireland, Spain, Greece, Italy, France, and others so uncompetitive relative to Germany in the easy-money years leading up to the euro crisis.

Source: JPMorgan, “Guide to the Markets”

After years of complaints from politicians around the world to let their currency float, the Chinese can allow just that to happen. A 10%, or 20%, or even 50% fall in the renminbi would take pressure off potential problems involving levered trade finance, boost China’s competitiveness, and pad government accounts at a critical time for China’s industrial transition. (Remember, the average currency devaluation in the Asian financial crisis of 1997-1998 was an even greater 60%.)

American, European, and Japanese politicians will have a hard time making the case for a downward-trending RMB as long as it floats freely. And honestly, the flip side will be difficult to defend. Although many economists believe that China’s abundant reserves, near 50% of GDP, will be enough to stem the tide in the event of capital flight, I don’t believe they are looking at the right data. In light of clearly wasted spending and widespread capital misallocation, GDP is artificially inflated … not to mention that a substantial portion of Chinese reserves may have already been locked up in loans to foreign borrowers.

M2 is a far better proxy for the capital that can rush out of an economy without warning … and Chinese M2 is now nearly twice the size of GDP. Since outstanding reserves cover less than 35% of M2, capital outflows place more pressure on the currency than most people realize. I wholeheartedly believe the renminbi will fall further over time, albeit with some serious volatility.

Over the last 50 years, every investment boom coupled with excessive credit growth has ended in a hard landing, from the Latin American debt crisis of the 1980s, to Japan in 1989, East Asia in 1997, and the United States after both the late-1990s internet bubble and the mid-2000s housing bubble.

The lesson is always the same, and it is hard to avoid. Economic miracles are almost always too good to be true. Broad-based, debt-fueled overinvestment (misallocation of capital) may appear to kick economic growth into overdrive for a while; but eventually disappointing returns and consequent selling lead to investment losses, defaults, and banking panics. And in the cases where foreign capital seeking strong growth in already highly valued assets drives the investment boom, the miracle often ends with capital flight and currency collapse.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

John and I talk about China constantly and always reach the same conclusion. We really have no way of knowing whether the country will suffer a modest slowdown or a hard landing, but we both agree with George Soros that “The major uncertainty facing the world today is not the euro but the future direction of China.”

To be clear, China doesn’t have to experience a deep recession in order to disrupt global growth. A slowdown to 2-3% real GDP growth and a corresponding decline in China’s import demand could fire demand shocks across emerging Asian economies like India and Indonesia, commodity producers like Australia and South Africa, and even deteriorating economies in the Eurozone like France and Italy.

The investor’s dilemma is that there is really no way to know what is happening in China today, much less what will happen tomorrow. The primary data is flawed at best, manipulated at worst, and there seem to be a lot of inconsistencies when we compare official data to more concrete measures of economic activity.

Even China’s new premier, Li Keqiang, believes China’s GDP numbers are “man-made” and therefore unreliable, according to a US diplomatic cable released by WikiLeaks in 2010. For what it’s worth, that same cable suggests the premier is more interested in measurements like electricity consumption (officially expected to rise by 7% in 2014), rail cargo volumes (officially expected to rise by 2% in 2014), and bank loans (officially expected to stall in 2014) ... which are all showing potential signs of fatigue.

From an investment perspective, China’s predicament can teach us one valuable lesson. The most important risks are often the ones you cannot easily anticipate, and thorough diversification may be your only defense. As the Chinese say, “Precaution averts perils.”

__________

John here. I think Worth did a good job of outlining the issues. I might add that I think a Chinese slowdown and possible move up the manufacturing value chain would be particularly disruptive to Germany at a time when the Eurozone might be under pressure from a deteriorating France. As Shakespeare once wrote, “When sorrows come, they come not single spies, but in battalions.” I see the situation in China as the domino that could topple and trigger another global crisis. Let us hope that they can find a path through a very difficult economic landscape. This way be dragons indeed!

For the record, I have been consistently saying for several years that when the Chinese allow their currency to float it will get weaker, perhaps materially so, not stronger, for a period of time. When they recently widened the bands, the renminbi did indeed weaken, and it seems to have been allowed to do so to teach those who were relentlessly trying to push the currency higher a hard lesson. When currencies float, they can move two ways. I believe the Japanese yen is on a very long and volatile ride to 200 to the dollar, but it will test the patience and resolve of all who try to trade it. The same resolve will be needed for trading the Renminbi. China is going to be a rough ride for anyone who thinks they can actually figure it out in advance.

Cafayate, South Africa, New York, Europe, and San Diego

I am in Cafayate, Argentina, which is in the northernmost province. While still in the tropics, it is at 5,500 feet, so the weather is almost perfect year-round and especially at this time of year. Some of the best wine grapes in Argentina grow here. Sunday or Monday we leave for Bill Bonner’s hacienda at almost 10,000 feet, up some of the roughest tracks I have ever been on, but the arrival is worth the adventure. At least this year we rented an appropriate vehicle for the drive. I don’t quite want to admit that I might not have chosen well the last time (since I didn’t know what lay in store for me), but I will suggest that you not buy a used rental car that comes out of Argentina. Getting towed out of rivers and sand dunes was challenging. And the roads were so rough and rocky that I drove on a flat tire for a few miles, since I couldn’t tell the difference in road feel, and the tire was shredded beyond recognition.

A week from Monday I head back to Dallas – for eight hours – before I take off for 12 days in South Africa. That will mean three straight nights in airplanes, a first for me. I will need that vacation resort, with lots of massages and hydrotherapy, to unwind me. I’m going to try something new this trip and post a few pictures and comments to Twitter. Follow me if you like. After South Africa I’m back home for like a day before I have to run up to New York to do some videos. Then it’s back home for a few weeks (or so it appears) before I head to Amsterdam, Brussels, and Geneva. I’ll come home for a few days and then head to San Diego for our Strategic Investment Conference – one of my real highlights of the year. And then I’ll be home for more than two whole weeks before heading to Tuscany for a few weeks of vacation. Whew. I will be ready to relax at the end of all that travel.

As I settled into my seat on the flight to Buenos Aires, who should sit down next to me but Kyle Bass, who was on a trip further south in Argentina to scope out what he sees as real opportunity. I should remind readers that Kyle and I will be doing a webinar on Monday, March 31, at 10 Central, sponsored by my partners at Altegris Investments. It is limited to qualified US investors. You can go to www.mauldincircle.com and sign up, and someone from Altegris will call and make sure you get an invitation. I hate to limit it, but that is the rule. (In the regard, I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA and SIPC. And read the risk disclosures!)

And as you know, Jack Rivkin, one of the most savvy and got-it-together writers and investors I know, recently assumed the position of CIO at Altegris. What you may not know is that Jack has started posting Altegris updates on investments, economic factors, market conditions, etc., which can be found here. These are interesting reads, with timely information – most notably Jack’s urgent focus on the need for an unconstrained approach to fixed-income. You should check this out now … and periodically going forward.

I am finally at the Grace Hotel in Cafayate, which has just opened, and I am delighted with my room and its panoramic view of the vineyards and majestic red mountains in the background. On the way here Olivier Garret and I stopped at a natural amphitheater in the canyon that towered some 700-800 feet high. There was a local musician over to the side, and I encouraged him to give us a song. He strummed a few chords and then in a lilting tenor voice sang us a local folk tune that should be performed on a national stage. The natural acoustics amplified it better than a thousand Bose speakers. It was amazing. Then he put down his guitar and picked up his flute. The sound was surreal, like the finest surround sound I have ever heard but stepped up a magnitude. I stopped, closed my eyes, and just took in the moment. Anywhere else, maybe, and he was just another flute player. But here he was a god. Maybe he should stay and avoid that big-city stage. It was the best 100 pesos I will spend this trip. Which, if he doesn’t spend it soon, won’t buy much, with Argentina’s raging inflation. But that was a problem for another day. In the moment there was just the magical connection through the music.

It is time to hit the send button. They say some 100 people are enjoying themselves while waiting for me down at poolside, and so I really need to go. And tomorrow there is a gym, spa, and a good book awaiting me. Have a great week!

Your already relaxing in Argentina analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.