Why I’ll Never Use a High-Yield Savings Account

-

Kelly Green

Kelly Green

- |

- July 26, 2023

- |

- Comments

Kelly Green

Kelly GreenI went into the bank a few days ago and was talking to the teller about putting my nephews as named beneficiaries on my accounts. This is important to me because I have a house listed for sale, and I anticipate putting the proceeds in there for at least the short term.

Her face lit up as she started telling me that a banker could help me go over my options because a high-yield savings account would be the best option for me. As I don’t have the money yet, it was easy to dodge out of the sales pitch.

High-interest-rate savings accounts don’t interest me.

Why? Because I can do better with dividend stocks.

Just Look at Yield Shark’s Average Current Yield

According to Bankrate.com, I can get a high-yield savings account with interest of around 4.5%. I only looked at accounts with no minimum balance since I can get started investing in the Yield Shark portfolio with as little as $14.

That $14 stock has a yield of 5.4%. One of our open positions trades at just $18.35 and yields 9.13%. This is on preferred shares of a company with a $600 million market cap… not a speculative startup. The average current yield of the Yield Shark open portfolio is 6.6%.

That’s based on if you bought one share of each of the 18 positions marked “buy” today. Our lowest yield is 4.1%, and the highest comes in at 11.3%.

But What About the Uncertainty?

I’m not saying just go out and start grabbing dividend stocks because they have yields over 4.5%. Dividends are up to the discretion of the management of a company. At any point, a company could see its dividend slashed or cut completely.

We do occasionally utilize preferred stocks and exchange-traded bonds to offset this risk, but even then, the risk is never 0%.

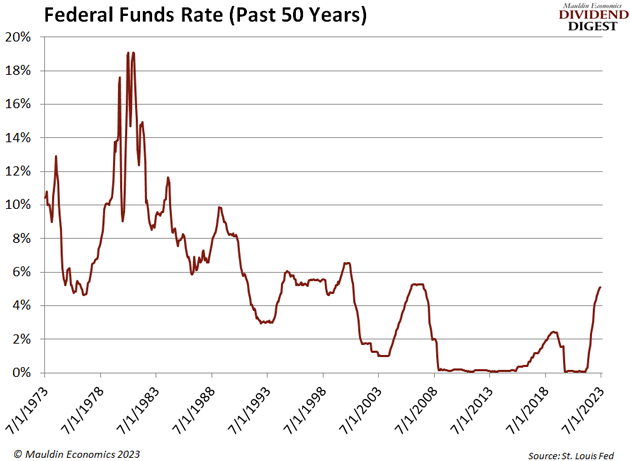

I don’t believe that the 4.5% on a high-yield savings account is any safer in the long term. Rates on savings accounts are variable. These rates are loosely linked to the Fed funds rate, but they’re mostly impacted by competitive pressures from other institutions.

Yes, we’ve seen the Fed funds rate increase over the past few years. But we can’t forget the 10 years it was essentially 0.

I’ve got some guesses where the peak will be this go-round, but I don’t want to stake my yield on guesswork and the whims of government officials.

Instead, I’m going to stick with the power of dividends for both my short- and long-term investments.

Timeline Matters

When I get any money, I divide it into three baskets:

-

Bills

-

Spending

Like what you're reading?

Get this free newsletter in your inbox every Wednesday! Read our privacy policy here.

-

Investment

That investment money is further divided into income generation and wealth building. These correspond with the Yield Shark portfolio designations of Current Yield and Bedrock Income.

For my income-generation money, 4.5% is simply not enough yield.

For my wealth-building money, being at the mercy of the Fed funds rate is not ideal. (I may be biased due to the zero-interest-rate environment I’ve experienced throughout most of my adult life.)

Instead, I look for companies with proven track records of increasing their dividends and solid businesses to continue doing so for many years to come.

I’ve given Dividend Digest readers some of my favorite ways to profit from dividends. Enterprise Products Partners (EPD) is still one of my favorite Bedrock holdings. And its 7.3% current yield makes it a great alternative to a high-yield savings account for both short-term and long-term investors.

My Yield Shark readers earned $3.76 per share from this position. And their effective yield is 8.4%.

So, if you want to be among the first to receive all my recommendations, make sure you’re on the Yield Shark list. The latest issue just came out yesterday, so you’ll be able to get into our new position right away.

For more income, now and in the future,

Kelly Green