Mailbag Question: What Do You Think of This Medicine Cabinet Powerhouse?

-

Kelly Green

Kelly Green

- |

- May 29, 2024

- |

- Comments

Kelly Green

Kelly GreenIt’s been a while since we looked at the mailbag. This is partly because we now have our online community. There, you can comment on an article or ask questions in the chat area. This allows me and other members to respond in real time.

I like to reply to simpler questions there. When I need to do a little digging, it inspires me to do a write up here in Dividend Digest or in a weekly Yield Shark update.

Today, I wanted to answer a question that has been waiting for space in our publishing schedule.

Gregory asked me, “Is KVUE a dividend stock on your watchlist? I’d be interested to hear your thoughts on it.” So, let’s take a look.

Kenvue Inc. (KVUE) is the parent company of many of the most iconic brands in your medicine cabinet.

Source: Kenvue

Kenvue (pronounced ken-view) collects $15.4 billion in annual sales. That makes it the world’s largest consumer health company by revenue.

And its current yield is over 4%!

The company is the outcome of the biggest shake-up at Johnson & Johnson (JNJ) in its 137-year history. JNJ decided to focus on its main business in pharma and medtech. Its household products were then spun off as a new company.

The spin off was completed in May 2023 to form Kenvue. Since then, JNJ has lowered its stake in the new company. JNJ announced it will sell its remaining 9.5% stake in Kenvue earlier this month.

Gregory knew this stock was on my radar.

I love having consumer staples in my portfolio. Especially companies with brands that are recognized and trusted. And that’s the case here. These companies make great candidates for the Bedrock Income part of any portfolio. That’s where we’re looking for companies we could hold for years or maybe even decades to come. Plus, Kenvue comes with royalty status.

The Chance to Keep Royalty Status

Even though Kenvue has been a company for only one year, it’s considered both a Dividend Aristocrat and a Dividend King. If you’re new to these terms, they are designations given to solid long-term dividend payers that meet certain requirements.

To be considered a Dividend Aristocrat, a company must:

-

Increase its dividend for the past 25 consecutive years,

-

Be a member of the S&P 500

-

Have a market capitalization of at least $3 billion

Like what you're reading?

Get this free newsletter in your inbox every Wednesday! Read our privacy policy here.

-

Maintain average daily trading volume of $5 million for three months before acceptance

To earn the Dividend King title requires just one thing: the company has raised its dividend for the past 50 years.

Both JNJ and Kenvue will remain in the S&P 500 Dividend Index until the next rebalancing. The index wants to see indications from both companies of a consistent dividend paying policy. For the next 2 years, the index will combine the dividends of the two companies to determine eligibility. After that, each company must raise its dividend individually to retain its status.

A great example of this is the Abbott Labs (ABT) spin off of AbbVie (ABBV) in 2012. Over a decade later, these two companies are holding their own as both Aristocrats and Kings. We experienced the flipside of this with 3M (MMM) and Solventum (SOLV), who did not meet the requirements and are now excluded from the list.

|

Could Kenvue Be a Good Bedrock Holding?

We know the companies separated so each could focus on its core business. Kenvue said it’s committed to its transition as a new company with three clear strategies for 2024:

-

Reach more consumers

-

Free up resources to invest in its brands for continued growth

-

Foster a culture of performance and impact

The ability to unlock growth potential is the uncertainty right now.

For the first quarter, Kenvue saw net sales of $3.9 billion, up 1.1% year over year. This was driven by momentum in its Self Care and Essential Health segments, but partially offset by underperformance in Skin Health and Beauty. That’s not too shabby, but I’d like to see annual sales growth closer to 2%—and consistent 2-4% growth would be excellent.

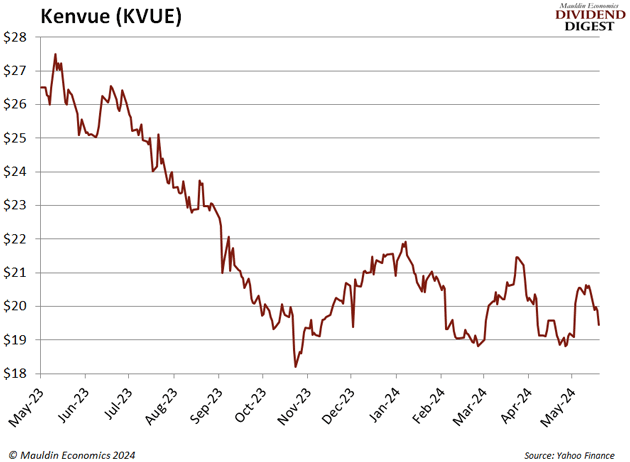

The market seems to agree with me and is not quite convinced on the outlook for KVUE. Shares have pretty much just slid lower since the spin off last year.

However, we have to note the current impressive 4% yield is a result of that share movement. Remember, when the share price falls and the dividend stays the same, the yield goes up. Uncertainty being built into the share price is the simple reason the yield is so high.

So, if you’re willing to take a gamble, this could be the time to buy. When my concerns above are remedied, the market will catch on and we can expect to see a yield between 3-3.5% or even less, much more in line with a core consumer staple stock.

Am I ready to say Kenvue would make a great addition to your income portfolio? No. Should it be on your watchlist? Absolutely.

It has a powerhouse of brands that consumers will continue to buy. If the company can successfully complete its strategic goals, sales of its brands should grow steadily year after year.

Like what you're reading?

Get this free newsletter in your inbox every Wednesday! Read our privacy policy here.

|

For more income, now and in the future,

Kelly Green