Time to Change Strategy

-

John Mauldin

John Mauldin

- |

- May 3, 2019

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinWe Have a Problem

No Solutions

Friends Don’t Let Friends Buy and Hold

Dallas, SIC, and Conversations

My recent letters described what I think the future will look like. I hasten to add, it isn’t what I think the future should look like or what I want to see. Almost the entire developed world has painted itself into a corner.

It won’t necessarily be terrible. I don’t expect another Great Depression or economic upheaval, but we will have to adapt our portfolios and lifestyles to this new reality. The good news is the changes will happen relatively slowly. We have time to adapt.

In war movies, it’s common for the dashing leader to make bold promises like, “We will never retreat!” ahead of a glorious victory. The assumption is that retreat is bad. But real-life military strategists say retreat can be the right move. When the odds are against you, better to save your ammunition for another time. Better yet, adopt a new strategy that gives you a better chance.

My last few letters may look like retreat, but I’m just recognizing reality. There is no plausible path to stopping the world’s debt overload, much less paying it off, without a serious and painful purge. If you know of such a path, please share it with me, but I haven’t seen one. So I foresee a tough decade ahead.

Summing up:

- Entitlement spending, interest on the debt, defense spending, and so forth will continue to produce trillion-dollar-plus deficits.

- No constituency is arguing to reform the entitlement system by reducing benefits. By the middle of the next decade, deficits will be in the $1.5 trillion range even under the CBO’s optimistic assumptions. While the numbers look marginally different elsewhere, the developed countries are all going the same direction: toward higher deficits.

- Following the next recession (and there is always one coming), the US deficit will be well north of $2 trillion and the total debt will quickly rise to $30 trillion. It will almost certainly be in the $40 trillion range before 2030. Unless interest rates drop significantly, simply paying the interest will consume much of the tax revenue. (Fortunately, I expect interest rates to drop significantly. Think Japan.)

- A growing body of academic literature and real-world experience suggests there is a point beyond which debt becomes a drag on growth. That means that the recovery after the next recession will be even slower than the last one. If, as I expect, the Federal Reserve and other central banks react with massive quantitative easing, it is entirely possible that the whole developed world will begin to look like Japan: slow nominal GDP growth, low interest rates that penalize savers, low inflation or even deflation, etc.

- In such an environment, normal equity index funds won’t produce the returns many have grown to expect.

- Public pension funds will get hammered in the bear market and many will have difficulty meeting their obligations. Governments will be forced to either cut benefits, raise taxes, or both. That is not going to make for a happy citizenry. It will play out in different manners all across the world, but the resulting frustration will be the same. And to put it very bluntly, “frustration” is inadequate to describe the result of underfunded pensions. Retirees made plans for their futures based upon receiving those pensions. And taxpayers likewise make plans.

- All of this will have significant investment implications, which we will visit below and in great detail in the coming weeks and months. But Japanification, to use a word, is going to make income and wealth inequality worse, not better.

This all being the case, the priority now isn’t whether to “retreat,” in the sense of changing your investment strategies, but how and to where, so you can pick up the fight later. Developing a strategy requires us to understand exactly what is happening and why. So I’m looking at the situation from different angles.

|

We Have a Problem

You have likely heard of “income inequality”—that wealthy people are making a larger share of our collective income. In one sense, it’s nothing new. Of course, the people with the highest incomes have more of the total. Math guarantees it.

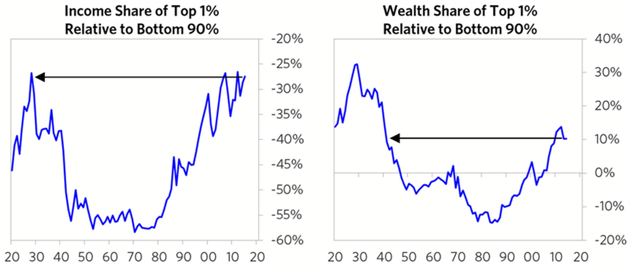

But it is true that the top’s share has grown in recent decades, as has the share of assets owned by the wealthiest. Ray Dalio of Bridgewater Associates has been writing about this for a few years now. Here’s a chart and quote from his latest article.

As shown below, the income gap is about as high as ever and the wealth gap is the highest since the late 1930s. Today, the wealth of the top 1% of the population is more than that of the bottom 90% of the population combined, which is the same sort of wealth gap that existed during the 1935-40 period (a period that brought in an era of great internal and external conflicts for most countries). Those in the top 40% now have on average more than 10 times as much wealth as those in the bottom 60%. That is up from six times in 1980.

Source: Ray Dalio

Dalio thinks it is significant that inequality, at least by these measures, is now in the same area it was in the Great Depression. It plunged in the postwar years and began rising again in the 1980s.

I suspect, if we had data going back a few centuries, we would see that those 30 or so years between 1950 and 1980 were actually the statistical aberration. Mass prosperity hasn’t been the historic norm. It certainly wasn’t that in the 1800s and the Gilded Age. Nor was it so in Europe.

Some people see this inequality as somehow unfair. I think it is more complex than that. It depends on how those with wealth became so. There’s a big difference between (a) despots who use political authority to enrich themselves and their friends, (b) monopolists who thrive by taking choice away from consumers instead of adding to it, and (c) entrepreneurs who grow wealthy by selling useful products to willing consumers.

(Incidentally, Dalio does a good job describing the problem, but I think he lays the blame at the wrong doorstep. His proposed solutions leave a lot to be desired. I will discuss this at length in a forthcoming letter.)

The problems begin when people perceive the wealthy are getting rich at the expense of others. And, it’s hard to escape that conclusion when the data say the top tier is keeping a bigger share of the pie, even if the pie is growing. Especially when your piece of the pie is not growing nearly as fast as those of the top. The relative distance becomes even more stark.

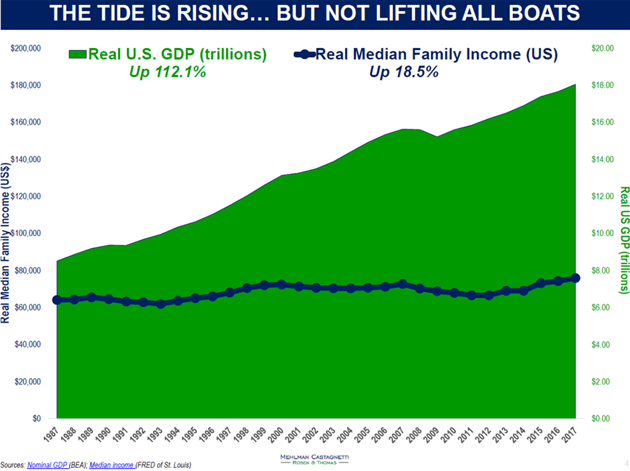

Let’s review some charts from my friend Bruce Mehlman’s latest fascinating slide deck. (He has much more that you can and definitely should view here.)

Source: Bruce Mehlman

If you take GDP as a proxy for national income, it’s been growing far faster than median family income, even adjusted for inflation. The wider that gap gets, the more people feel like they are being left behind.

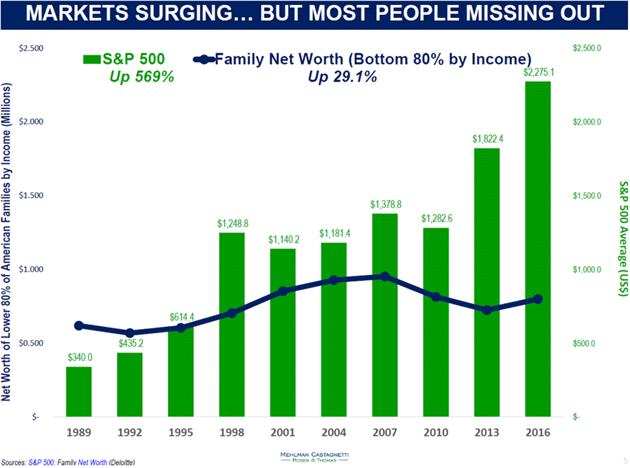

Here’s another one comparing stock market growth with family net worth. This isn’t really surprising since we know the top quintile owns most of the stocks. The lower 80% see little direct benefit. But the magnitude of the disparity is still remarkable.

Source: Bruce Mehlman

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

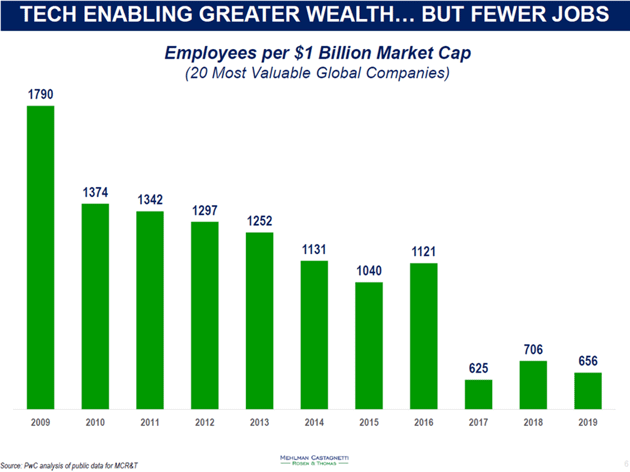

One reason income may be unequal is that talent is increasingly unequal, too. Or at least, the willingness of businesses to buy talent. Here’s a chart showing the most valuable companies have been getting that way with a smaller headcount.

Source: Bruce Mehlman

Mehlman cites technology as the explanation for this, and I agree that’s a significant part of it. But so are other things, like the increasing number of sectors where a small number of companies, whose existence is enabled by financial engineering and monetary policy, dominate their respective markets.

My good friend Ben Hunt of Epsilon Theory notes that the S&P 500 companies have the highest earnings relative to sales in history.

Source: Ben Hunt

Quoting Ben:

This is a 30-year chart of total S&P 500 earnings divided by total S&P 500 sales. It’s how many pennies of earnings S&P 500 companies get from a dollar of sales… earnings margin, essentially, at a high level of aggregation. So at the lows of 1991, $1 in sales generated a bit more than $0.03 in earnings for the S&P 500. Today in 2019, we are at an all-time high of a bit more than $0.11 in earnings from $1 in sales.

It’s a marvelously steady progression up and to the right, temporarily marred by a recession here and there, but really quite awe-inspiring in its consistency. Yay, capitalism!

Ben goes on to say many people think that is because of technology. He argues it is the financialization of our economy and the Fed’s loose policies. I agree 100%. If you think they haven’t changed the rules since the 1980s and 1990s, you aren’t paying attention, boys and girls!

Work-saving technology isn’t bad. In the past, it freed our bodies from dangerous, exhausting toil, and now it’s freeing our minds from mental drudgery. We can adjust. The problem is that it is hitting us so fast. Farming went from manual labor to automation over several generations. Now we’re traveling an equal distance in only a few years, resulting in millions of unemployed humans.

As unhappy as all this is making people now, imagine how it will be when recession hits. And then couple that with an ever-increasing explosion of new technologies that reduce demand for many types of labor (like automated driving).

No Solutions

Some degree of unhappiness and discontent is part of the human condition. It’s what drives us to improve our lives. We accept challenges as long as we think we have a fair chance at overcoming them.

Many Americans no longer believe they have that chance. That’s partly because they have higher expectations—possibly too high. But right or wrong, the perception is there. It affects behavior and, more to the point, it affects what people expect from the government. When they perceive less ability to reach the next level on their own, they look to Washington for help.

I noted last week that almost no one really wants to cut government spending. Even the so-called fiscal conservatives mostly nibble around the edges, reducing budget growth here and there. Bill Clinton was wrong when he said “the era of big government is over” in 1996. It’s bigger than ever and growing faster than ever. Whether you like it or not, that is a fact.

Government revenue is not growing faster than ever, which means rising debt even in today’s relative prosperity.

Again, whether you like this or not is irrelevant. It’s happening. I see no way out. Raising taxes on the wealthy won’t get us even close to a balanced budget, even at confiscatory levels. Raising taxes on the middle class won’t happen in a recession. The only tax system with a shot at actually paying for current spending (even without adding the new programs some Democrats want) is a “VAT” or value-added tax, and it is anathema in both parties.

No matter how I look at this, I keep coming back to gigantic deficits that the Federal Reserve will have to monetize in some fashion—probably something like the previous QE rounds but on a vastly larger scale. And thus my belief it will launch an era of Japan-like deflation and economic doldrums.

If you think this is impossible or I’m being too pessimistic, please, please tell me why I’m wrong. Show me where we can get the necessary tax revenue without severely impacting the economy. Show me how we can cut benefits without getting massive pushback from politicians. And please, show me how we get off the path we are on. And tell me what scenario you think is more plausible. I don’t see one. I really don’t.

Friends Don’t Let Friends Buy and Hold

You probably read my letters because they help inform your investing strategy. If so, then let me say this loud and clear: your strategy probably needs to change. The methods that worked well recently won’t cut it in the new era I think we will enter soon.

At the risk of repeating myself for the 20th time, bear markets like last December that are not accompanied by recessions have V-shaped recoveries. Bear markets that happen in the context of a recession have long recoveries. The next one, because of the massive debt that will be increasing at an astounding rate, is likely to see an even slower recovery.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Friends don’t let friends buy and hold. At a minimum, you need some type of hedging program on your equity portfolios. Using a simple 200-day moving average to signal the time for going to cash, while not the best, will help protect you from the worst of a massive bear market.

The recent flurry of IPO filings by “unicorn” companies like WeWork ought to be ringing alarm bells. The venture capital investors who financed these businesses thus far are ready to exit. They’re doing so because they think the risk-reward equation is as favorable as it will ever be. Possibly they’re wrong, but I don’t think so.

We have reached the “distribution” stage, when insiders and professional investors become net sellers while the small investors who missed most of the bull market finally jump in. History says it won’t end well for the latter group.

As the economy weakens into recession and public markets retreat, I think we’ll see two strategic trends.

First, active management will return to prominence as investors realize prices can move in both directions. The RIAs, mutual funds managers, and hedge funds that have managed to hold on through the lean years (and many didn’t) will draw assets once again. That doesn’t mean they will succeed, performance-wise, but they’ll get a chance to try.

Second, and possibly more important, the best opportunities will leave the public markets entirely. We already see this unfolding as the number of listed companies declines, mainly at the expense of small caps. There is just no reason for most successful companies to accept the hassles and expense of an exchange listing. They can raise all the capital they need from that small number of investors in whom most of the wealth is now concentrated.

This will, unfortunately, aggravate the inequality frustrations. Our regulatory structure keeps most private investments off limits to the average investor, or even above-average net worth investors. So even if you manage to accumulate some capital, you may not have the much better options for investing it than those with a few million dollars and more. The government has rigged the markets against small investors in the name of protecting them.

That doesn’t mean investment success will be impossible. You’ll have opportunities, but you may have to hunt for them and act quickly when you find them. That’s what active managers do, and not just in stocks and bonds. I foresee many opportunities in real estate as well. There are going to be amazing opportunities in new technologies. Like smart generals, sometimes we have to retreat from the unwinnable battle and develop a different plan. That’s what I am doing.

We’ll go deeper into this subject at my conference in Dallas, which is now less than two weeks away. I can’t wait. You can hear and/or see most of it with a Virtual Pass. I truly don’t know of a better educational opportunity for investors than either directly attending the Strategic Investment Conference or getting your Virtual Pass. Please note that for people like me, who prefer to learn by reading and not listening, all of the speeches will be transcribed for the Virtual Pass. And attendees automatically get them. The conference is May 13–16 and there are usually a few spots that open from people having to cancel at the last minute. If you can make it, you probably should. I look forward to seeing you there.

Dallas, SIC, and Conversations

Shane and I will head for Dallas next Wednesday, taking care of some local business and meeting friends (and hopefully getting to watch the new Avengers movie) and then turn our complete focus to the conference. Surprisingly, my travel calendar after that is fairly sparse for the early summer, with a few potential spots here and there.

I was in Washington, DC this week where I did a video interview with my friend Neil Howe. We discussed a wide variety of subjects, including what the last half of the Fourth Turning will look like. He foresees a great deal of political angst. There is the real potential for the same kind of political stresses that gave us Franklin Roosevelt almost 90 years ago. For some of you, that is a scary thought, and others will say “about time.”

I then had the privilege of spending some time with good friend Newt Gingrich and some of his staff. We drove to a bookstore in Virginia for a book signing and then he took two of us to a hole-in-the-wall Italian restaurant near his home. He quizzed me for some time on my view of the economy and its interplay with society, and in return, I got to ask a few questions as well. Newt has some of the best stories. As does Neil Howe. I have been with them together, and it is a priceless moment. Just for the record, I also met with those of a different political and economic philosophy. I do so all the time.

One of the greatest investment risks is a lack of imagination, in that we can’t imagine what could actually go wrong with our main investment thesis. As Mark Twain supposedly said, “It ain't what you don't know that gets you into trouble. It's what you know for sure that just ain't so.”

Michael Lewis’s book The Big Short opens with this similar quote, from Leo Tolstoy:

The most difficult subjects can be explained to the most slow-witted man if he has not formed any idea of them already; but the simplest thing cannot be made clear to the most intelligent man if he is firmly persuaded that he knows already, without a shadow of a doubt, what is laid before him.

I spend a great deal of time trying to determine if what I already “know for a fact” is actually the case. That is especially true when I’m developing a new thesis that makes me uncomfortable. But if the facts change, what else can we do but evolve with them?

And on that note, let me wish you a great week! Find a friend or two and swap a few stories. It will make your life better.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Your trying to see the way forward analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.