The End of Monetary Policy

-

John Mauldin

John Mauldin

- |

- September 28, 2014

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinThe End of Monetary Policy

Let’s Look at the Numbers

Where’s my GDP?

Demographics, Debt, Bond Bubbles, and Currency Wars

That Pesky Budget Thing

A Multitude of Sins

Not with a Bang But a Whimper

Washington DC, Chicago, Athens (Texas), and Boston

We are the hollow men

We are the stuffed men

Leaning together

Headpiece filled with straw. Alas!

Our dried voices, when

We whisper together

Are quiet and meaningless

As wind in dry grass

Or rats’ feet over broken glass

In our dry cellar…

This is the way the world ends

This is the way the world ends

This is the way the world ends

Not with a bang but a whimper.

– T. S. Eliot, “The Hollow Men”

What we may be witnessing is not just the end of the Cold War, or the passing of a particular period of postwar history, but the end of history as such: that is, the end point of mankind’s ideological evolution and the universalization of Western liberal democracy as the final form of human government. This is not to say that there will no longer be events to fill the pages of Foreign Affairs' yearly summaries of international relations, for the victory of liberalism has occurred primarily in the realm of ideas or consciousness and is as yet incomplete in the real or material world. But there are powerful reasons for believing that it is the ideal that will govern the material world in the long run.

– Francis Fukuyama, The End of History and the Last Man

Francis Fukuyama created all sorts of controversy when he declared “the end of history” in 1989 (and again in 1992 in the book cited above). That book won general applause, and unlike many other academics he has gone on to produce similarly thoughtful work. A review of his latest book, Political Order and Political Decay: From the Industrial Revolution to the Globalisation of Democracy, appeared just yesterday in The Economist. It’s the second volume in a two-volume tour de force on “political order.”

I was struck by the closing paragraphs of the review:

Mr. Fukuyama argues that the political institutions that allowed the United States to become a successful modern democracy are beginning to decay. The division of powers has always created a potential for gridlock. But two big changes have turned potential into reality: political parties are polarised along ideological lines and powerful interest groups exercise a veto over policies they dislike. America has degenerated into a “vetocracy”. It is almost incapable of addressing many of its serious problems, from illegal immigration to stagnating living standards; it may even be degenerating into what Mr. Fukuyama calls a “neopatrimonial” society in which dynasties control blocks of votes and political insiders trade power for favours.

Mr. Fukuyama’s central message in this long book is as depressing as the central message in “The End of History” was inspiring. Slowly at first but then with gathering momentum political decay can take away the great advantages that political order has delivered: a stable, prosperous and harmonious society.

While I am somewhat more hopeful than Professor Fukuyama is about the future of our political process (I see the rise of a refreshing new kind of libertarianism, especially among our youth, in both conservative and liberal circles, as a potential game changer), I am concerned about what I think will be the increasing impotence of monetary policy in a world where the political class has not wisely used the time that monetary policy has bought them to correct the problems of debt and market-restricting policies. They have avoided making the difficult political decisions that would set the stage for the next few decades of powerful growth.

So while the title of this letter, “The End of Monetary Policy,” is purposely provocative, the longer and more appropriate title would be “The End of Effective and Productive Monetary Policy.” My concern is not that we will move into an era of no monetary policy, but that monetary policy will become increasingly ineffective, so that we will have to solve our social and physical problems in a much less friendly economic environment.

In today’s Thoughts from the Frontline, let’s explore the limits of monetary policy and think about the evolution and then the endgame of economic history. Not the end of monetary policy per se, but its emasculation.

Asset classes all over the developed world have responded positively to lower interest rates and successive rounds of quantitative easing from the major central banks. To the current generation it all seems so easy. All we have to do is ensure permanently low rates and a continual supply of new money, and everything works like a charm. Stock and real estate prices go up; new private equity and credit deals abound; and corporations get loans at low rates with ridiculously easy terms. Subprime borrowers have access to credit for a cornucopia of products.

What was Paul Volcker really thinking by raising interest rates and punishing the economy with two successive recessions? Why didn’t he just print money and drop rates even further? Oh wait, he was dealing with the highest inflation our country had seen in the last century, and the problem is that his predecessor had been printing money, keeping rates too low, and allowing inflation to run out of control. Kind of like what we have now, except we’re missing the inflation.

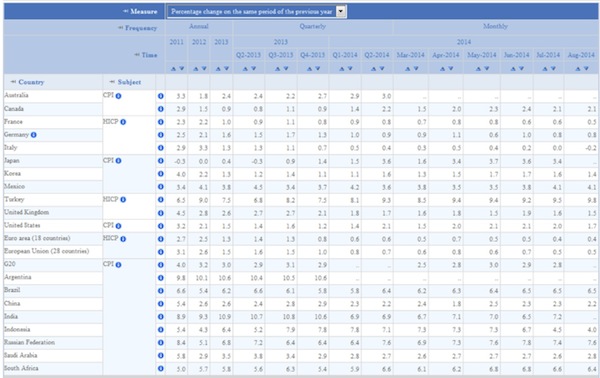

The Organization for Economic Cooperation and Development has a marvelous website full of all sorts of useful information. Let’s start by looking at inflation around the world. This table is rather dense and is offered only to give you a taste of what’s available.

What we find out is that inflation is strikingly, almost shockingly, low. It certainly seems so to those of us who came of age in the ’60s and ’70s and who now, in the fullness of time, are watching aghast as stupendous amounts of various currencies are fabricated out of thin air. Seriously, if I had suggested to you back in 2007 that central bank balance sheets would expand by $7-8 trillion in the next half-decade but that inflation would be averaging less than 2%, you would have laughed in my face.

Let’s take a quick world tour. France has inflation of 0.5%; Italy’s is -0.2% (as in deflation); the euro area on the whole has 0.4% inflation; the United Kingdom (which still includes Scotland) is at an amazingly low 1.5% for the latest month, down from 4.5% in 2011; China with its huge debt bubble has 2.2% inflation; Mexico, which has been synonymous with high inflation for decades, is only running in the 4% range. And so on. Looking at the list of the major economies of the world, including the BRICS and other large emerging markets, there is not one country with double-digit inflation (with the exception of Argentina, and Argentina is always an exception – their data lies, too, because inflation is 3-4 times what they publish.) Even India, at least since Rajan assumed control of the Reserve Bank of India, has watched its inflation rate steadily drop.

Japan is the anomaly. The imposition of Abenomics has seemingly engineered an inflation rate of 3.4%, finally overcoming deflation. Or has it? What you find is that inflation magically appeared in March of this year when a 3% hike in the consumption tax was introduced. When government decrees that prices will go up 3%, then voilà, like magic, you get 3% inflation. Take out the 3% tax, and inflation is running about 1% in the midst of one of the most massive monetary expansions ever seen. And there is reason to suspect that a considerable part of that 1% is actually due to the ongoing currency devaluation. The yen closed just shy of 110 yesterday, up from less than 80 two years ago.

I should also point out that, one year from now, this 3% inflation may disappear into yesteryear’s statistics. The new tax will already be factored into all current and future prices, and inflation will go back to its normal low levels in Japan.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Inflation in the US is running less than 2% (latest month is 1.7%) as the Fed pulls the plug on QE. As I’ve been writing for … my gods, has it really been two decades?! – the overall trend is deflationary for a host of reasons. That trend will change someday, but it will be with us for a while.

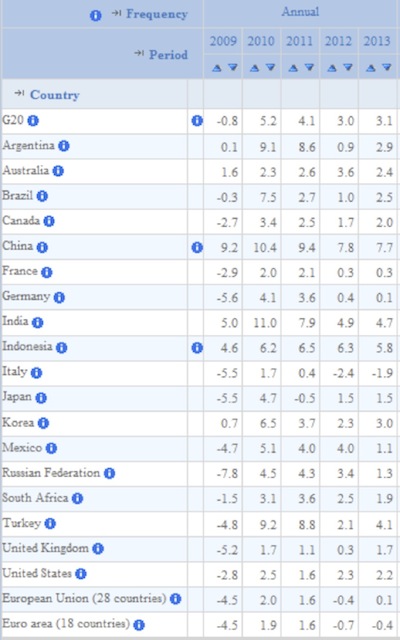

Gross domestic product around the developed world ranges anywhere from subdued to anemic to outright recessionary:

The G-20 itself is growing at an almost respectable 3%, but when you look at the developed world’s portion of that statistic, the picture gets much worse. The European Union grew at 0.1% last year and is barely on target to beat that this year. The euro area is flat to down. The United Kingdom and the United States are at 1.7% and 2.2% respectively. Japan is in recession. France is literally at 0% for the year and is likely to enter recession by the end of the year. Italy remains mired in recession. Powerhouse Germany was in recession during the second quarter.

Let’s put those stats in context. We have seen the most massive monetary stimulation of the last 200 years in the developed world, and growth can be best described as faltering. Without the totally serendipitous shale oil revolution in the United States, growth here would be about 1%, or not much ahead of where Europe is today.

Demographics, Debt, Bond Bubbles, and Currency Wars

Look at the rest of the economic ecology. Demographics are decidedly deflationary. Every country in the developed world is getting older, and with each year there are fewer people in the working cohort to support those in retirement. Government debt is massive and rising in almost every country. In Japan and many countries of Europe it is approaching true bubble status. Anybody who thinks the current corporate junk bond market is sustainable is smoking funny-smelling cigarettes. (The song from my youth “Don’t Bogart That Joint” pops to mind. But I digrass.)

We are seeing the beginnings of an outright global currency war that I expect to ensue in earnest in 2015. My co-author Jonathan Tepper and I outlined in both Endgame and Code Red what we still believe to be the future. The Japanese are clearly in the process of weakening their currency. This is just the beginning. The yen is going to be weakening 10 to 15% a year for a very long time. I truly expect to see the yen at 200 to the dollar somewhere near the end of the decade.

ECB head Mario Draghi is committed to weakening the euro. The reigning economic philosophy has it that weakening your currency will boost exports and thus growth. And Europe desperately needs growth. Absent QE4 from the Fed, the euro is going to continue to weaken against the dollar. Emerging-market countries will be alarmed at the increasing strength of the dollar and other developed world currencies against their currencies and will try to fight back by weakening their own money. This is what Greg Weldon described back in 2001 as the Competitive Devaluation Raceway, which back then described the competition among emerging markets to maintain the devaluation of their currencies against the dollar.

Today, with Europe and Japan gunning their engines, which have considerable horsepower left, it is a very competitive race indeed – and one with far-reaching political implications for each country. As I have written in past letters, it is now every central banker for him- or herself.

Developed governments around the world are running deficits. France will be close to a 4% deficit this year, with no improvement in sight. Germany is running a small deficit. Japan has a mind-boggling 8% deficit, which they keep talking about dealing with, but nothing ever actually happens. How is this possible with a debt of 250% of GDP? Any European country with such a debt structure would be in a state of collapse. The US is at 5.8% and the United Kingdom at 5.3%, while Spain is still at 5.5%.

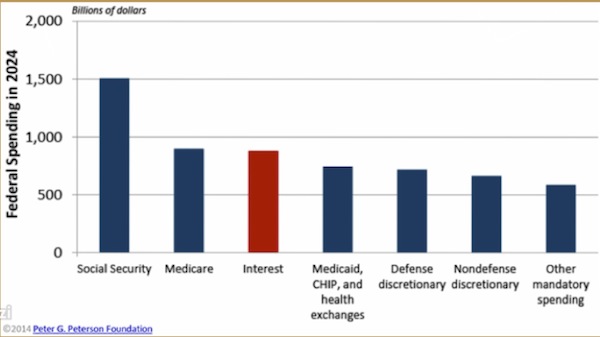

Let’s focus on the US. Everyone knows that the US has an entitlement-driven spending problem, but very few people I talk with understand the true nature of the situation, which is actually quite dire, looming up ahead of us. In less than 10 years, at current debt projection growth rates, the third-largest expenditure of the United States government will be interest expense. The other three largest categories are all entitlement programs. Discretionary spending, whether for defense or anything else, is becoming an ever-smaller part of the budget. Social Security, Medicare, and Medicaid now command nearly two-thirds of the national budget and rising. Ironically, polls suggest that 80% of Americans are concerned about the rising deficit and debt, but 69% oppose Medicare cutbacks, and 78% oppose Medicaid cutbacks.

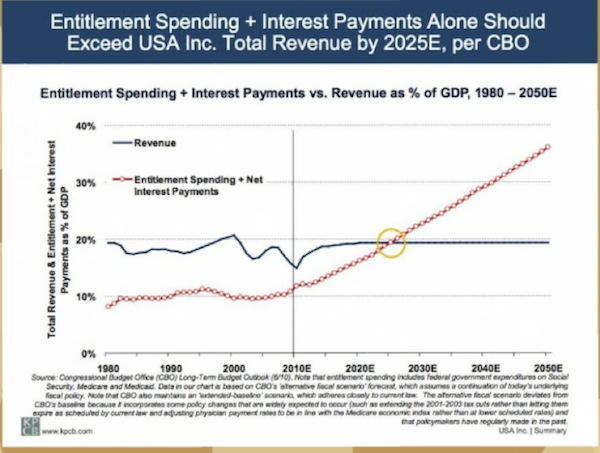

At some point in the middle of the next decade, entitlement spending plus interest payments will be more than the total revenue of the government. The deficit that we are currently experiencing will explode. The following chart is what will happen if nothing changes. But this chart also cannot happen, because the bond market and the economy will simply implode before it does.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Monetary policy has been able to mask a multitude of our government’s fiscal sins. My worry for the economy is what will happen when Band-Aid monetary policy can no longer forestall the hemorrhaging of the US economy. Long before we get to 2024 we will have a crisis. In past years, I have expected the problems to come to a head sooner rather than later, but I have come to realize that the US economy can absorb a great deal of punishment. But it cannot absorb the outcomes depicted in those last two charts. Something will have to give.

And these projections assume there will be no recession within the next 10 years. How likely is that? What happens when the US has to deal with its imbalances at the same time Europe and Japan must deal with theirs? These problems are not resolvable by monetary policy.

Right now the markets move on every utterance from Janet Yellen, Mario Draghi, and their central bank friends. Central banking dominates the economic narrative. But what happens to the power of central banks to move markets when the fiscal imperative overcomes the central bank narrative?

Sometime this decade (which at my age seems to be passing mind-numbingly quickly) we are going to face a situation where monetary policy no longer works. Optimistically speaking, interest rates may be in the 2% range by the end of 2016, assuming the Fed starts to raise rates the middle of next year and raises by 25 basis points per meeting. If we were to enter a recession with rates already low, what would dropping rates to the zero bound again really do? What kind of confidence would that tactic actually inspire? And gods forbid we find ourselves in a recession or a period of slow growth prior to that time. Will the Fed under Janet Yellen raise interest rates if growth sputters at less than 2%?

An even scarier scenario is what will happen if we don’t deal with our fiscal issues. You can’t solve a yawning deficit with monetary policy.

Further, at some point the velocity of money is going to reverse, and monetary policy will have to be far more restrained. The only reason, and I mean only, that we’ve been able to get away with such a massively easy monetary policy is that the velocity of money has been dropping consistently for the last 10 years. The velocity of money is at its lowest level since the end of World War II, but it is altogether possible that it will slow further to Great Depression levels.

When the velocity of money begins to once again rise – and in the fullness of time it always does – we are going to face the nemesis of inflation. Monetary policy during periods of inflation is far more constrained. Quantitative easing will not be the order of the day.

For Keynesians, we are in the Golden Age of Monetary Policy. It can’t get any better than this: free money and low rates and no consequences (at least no consequences that can be seen by the public). This will end, as it always does…

Will we see the end of monetary policy? No, policy will just be constrained. The current era of easy monetary policy will not end (in the words of T.S. Eliot) with a bang but a whimper. Janet or Mario will walk to the podium and say the same words they do today, and the markets will not respond. Central banks will lose control of the narrative, and we will have to figure out what to do in a world where profits and productivity are once again more important than quantitative easing and monetary policy.

You need to be thinking about how you will react and how you want to protect your portfolios in such a circumstance. Even if that volatility is years off, “war-gaming” how you will respond is an important exercise. Because it will happen, unless Congress and the White House decide to resolve the fiscal crisis before it happens. Calculate the odds on that happening and then decide whether you need to have a plan.

Unless you think the bond market will continue to finance the US government through endless deficits (as so far has happened in Japan), then you need to start to contemplate the end of effective monetary policy. I would note that, even in Japan, monetary policy has not been effective in restarting an economy. It is a quirk of Japan’s social structure that the Japanese have devoted almost their entire net savings to government bonds. As the savings rate there is getting ready to turn negative, we are going to see a very different economic result. Japan with the yen at 200 and an even older society will look a great deal different than the country does today.

Current market levels of volatility and complacency should be seen as temporary. Plan accordingly.

Washington DC, Chicago, Athens (Texas), and Boston

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I am in Washington DC as you read this. I have a few meetings set up, as well as a speaking engagement, and then I’ll return home to meet with my business partners at Mauldin Economics later in the week. In the middle of October I will go to Chicago for a speech, fly back to a meeting with Kyle Bass and his friends at the Barefoot Ranch in Athens, Texas, and then fly out to Boston to spend the weekend with Niall Ferguson and some of his friends. I am sure I will be happily surfing mental stimulus overload that week.

Next weekend (October 4) is my 65th birthday. I had originally thought I would do a rather low-key event with family; but my staff, family, and friends have different plans. I’m not really supposed to know what’s going on and don’t really have much of an idea as I am not allowed around planning sessions, but it sounds like fun.

I am walking on legs that feel like Jell-O, as it was “legs day” yesterday, working out with The Beast. My regular workout partner couldn’t make it, so he was able to focus on exhausting me to the maximum extent possible. I’ve never been all that athletic. As a kid, for the most part I was not allowed to participate in PE due to some physical limitations (which fortunately went away as I grew older).

I became a true geek. Not that that is all bad: it has served me rather well later in life. Geeks rule. It wasn’t until I was in my mid-40s that I began to go to the gym on more than a haphazard basis. And I must confess that I was a typical male in that I focused on my upper body as opposed to my legs and abdominals. That oversight is catching up with me now. The Beast is forcing me to devote more time to my legs and core. Much better for me as I approach the latter half of my 60s, but it’s painful to realize the cost of my negligence.

In the last five or six years my travel has reduced my gym time, or at least that’s my excuse. For whatever reason, my travel has been reduced for the last two months, so I’m getting much more time in the gym, and my workouts are more well-rounded. I typically try to do at least another 30 minutes of cardio after our training sessions, even if the session was based around cardio. Except on leg days. There’s nothing left for extra walking or cycling after leg days.

I share this because I want you to understand that working out is just as important as your investment strategy. I fully intend to be going strong for a very long time. But that doesn’t happen (at least as easily) if you lose your legs. As much as I hate leg days, I probably need those workouts more than any others.

It’s time to hit the send button. I hear kids and grandkids gathering in the next room. That’s something else that is just as important as investment strategy. You have a great week.

Your thinking about how to profit from the coming crisis analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.