Renovating the Fed

-

John Mauldin

John Mauldin

- |

- December 2, 2017

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinNonmusical Chairs

Monetary Mismatch

Main Street on the Fed

Little Bits of Fed Trivia

Rich Yamarone, RIP

Earnings don’t move the overall market; it’s the Federal Reserve Board…. Focus on the central banks and focus on the movement of liquidity…. Most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.

– Stan Druckenmiller (hat tip Steve Blumenthal)

The Federal Reserve will soon have a new chair, assuming the Senate confirms Jerome Powell as Janet Yellen’s successor. Yellen’s departure will reduce the nominally seven-member Board of Governors to only three. That may or may not be a good thing, depending on some other events.

In fact, in talking with some of my Fed-watching friends, it appears the world’s most important central bank is about to experience some potentially profound changes – not just in personnel but more importantly in the kind of people who lead it. Those changes could, in turn, have some serious economic impacts; so it’s worth taking a deeper look.

First, let me remind you that early bird rates will expire soon for my Strategic Investment Conference, next March 6–9 in San Diego. We’ve received a great response even without announcing all the speakers yet – and I do have some more big names pending. Several people you don’t want to miss are trying to clear their schedules. You can wait to find out who they are, or you can register now and save yourself a few hundred bucks. It should be an easy choice. Everyone who comes always says that my conference is the best. Click here to learn more.

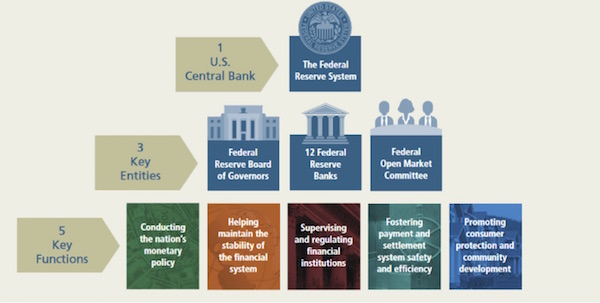

Before we get into the impending changes at the Fed, let’s quickly review how the organization works. For some of you this review will be too elementary, but even many sophisticated investment people really don’t have much understanding of the inner workings of the Fed.

The Federal Reserve System consists of the Federal Reserve Board of Governors, which is a federal agency, and twelve regional Federal Reserve Banks. The Fed banks are “owned” by the member commercial banks in their district, but the Board of Governors appoints one-third of their directors.

Source: Federal Reserve Board of Governors

The Board of Governors itself has seven members, all appointed by the US president to 14-year terms. The terms overlap, so by original design no one president should have too much influence on the board’s composition. However, nothing requires governors to serve their full terms, and many do not. That arrangement seems to have created a perfect storm of sorts, at least for President Trump: He may get to appoint as many as seven governors next year. Trump has the opportunity to seriously shake up the Fed – if he chooses to take it. Or he can stick with the usual choices. Here’s hoping he doesn’t.

When Trump took office, the Board of Governors had two vacancies and five members: Janet Yellen, Stanley Fischer, Lael Brainard, Jerome Powell, and Daniel Tarullo. Fischer and Tarullo both resigned this year. The Senate confirmed Randal Quarles as a board member and as vice-chair for supervision. So that leaves the membership at four as of now. Note that Quarles is not taking Stanley Fischer’s vice chairman of the Federal Reserve position. That nomination is still open. There is the possibility that a brand-name economist could take that position. Would John Taylor be willing to be vice chairman? Inquiring minds want to know.

The president chose not to renominate Yellen to another term as chair. She could have stayed on as a board member but has said she will retire when the Senate confirms Powell as the new chair. Powell is already on the board, so elevating him to chair doesn’t change the number of members.

Sidebar: Technically, the term of the Fed chair ends on February 3, after the January Federal Open Market Committee meeting the last two days of January. I am sure this is not always the case, but my recent memory says that the current chair shows up for the last meeting as a kind of swan song, and everybody engages in a Kumbaya lovefest, exclaiming over how wonderful their time together has been. I cannot even imagine that Powell will want to take control of that meeting, even if he is confirmed by then. As he definitely should be. He just seems to be too much of a gentleman to do that.

This week the president nominated economist Marvin Goodfriend to one of the vacant Board of Governors seats. Goodfriend is controversial, as we’ll see in a minute, so getting him through the Senate could take some time. I’m guessing it will be March or even later before he’s confirmed. But the flip side is, he is Trump’s pick. So somebody should tell the Senate to go ahead and do its job and don’t leave the Fed with just three Board of Governors members by the middle of February. And then somebody should tell Trump to get busy nominating at least two more members.

Barring that outcome, sometime in January or by February 3, the Board of Governors will drop to only three members: Powell, Brainard, and Quarles. There’s an outside chance it could drop to two, since Quarles holds a partial term that ends January 31, 2018. His nomination to stay beyond that date is pending before the Senate. Presumably the Senate will act in time, but you never know with that bunch – they have a lot on their plates. But they have already have approved Quarles once, so his approval should be a perfunctory act.

How does a seven-member board operate with four vacancies? Is that even a quorum? Well, yes, technically it is. Back in 2003 the Board of Governors amended its rules to stipulate that a simple majority of the current membership constitutes a quorum. With three Senate-confirmed governors, any two can meet and make decisions. This amendment was created in reaction to 9/11, when the governors realized that bad things can happen and that people in leadership positions need to be able to make decisions.

But simply making decisions is not the same as making the right decisions. In talking to former governors I’ve met over the years, I’ve gathered that they divide the workload so various issues can get the board-level attention they need. That division of labor gets harder when there are fewer governors. The result may be either poor decisions or long delays in getting anything done.

And just for the record, the Federal Reserve does a lot more than just set interest rates. Its tasks include bank regulation, actually moving currency around, dealing with local banking issues, handling cash transfers between banks, and so much more. And in a changing world, on-the-ground conditions often change, so that every now and then somebody actually has to make a decision. And sometimes the rules require a board-level decision. But when you get down to just a few board members, scheduling gets tough, which is why you need the full seven board members.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

So it’s best for everyone that the board get its full complement back. Yet President Trump – who could have nominated two governors the day he took office and two more replacements this year – has had only Randal Quarles confirmed and has simply promoted Powell, who was already there.

Marvin Goodfriend will take one of the other three vacancies, leaving two open seats once Yellen retires (more on Goodfriend below). By filling those positions, Trump will put his stamp on the Federal Reserve Board. What an amazing opportunity – if he will seize it. Carpe diem!

Among other things, the missing governors could have an impact on monetary policy. Here again, I must explain the Fed’s Byzantine organizational scheme.

Monetary policy – interest rates and the like – issues from the Federal Open Market Committee. The FOMC comprises:

• All seven Board of Governors members

• The president of the New York Federal Reserve Bank

• Four of the other 11 Fed Bank presidents, who rotate through one-year terms.

So on this committee of 12, the politically appointed governors have seven votes, outweighing the five privately appointed bank presidents – except when there aren’t seven governors, as is the case now and probably will be well into 2018, at least.

Source: Federal Reserve Board of Governors

In practice, this voting edge rarely matters because Fed chairs work hard to build consensus on the FOMC. They don’t like dissenting votes. I can’t recall any situation where the Board of Governors and the bank presidents seriously disagreed, although there has been the odd dissent here and there. But it could happen. And if it happens in 2018, the bank presidents will have the upper hand.

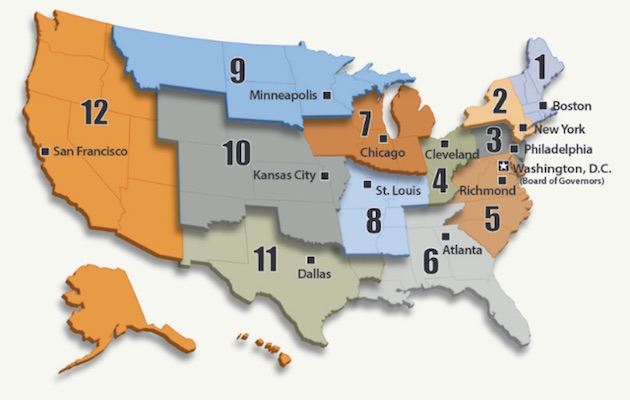

Just to make the situation even murkier, two of the five bank presidents who will be on FOMC in 2018 are currently unknown. New York Fed President William Dudley will be leaving by mid-year. The other four will be the Atlanta, Cleveland, Richmond, and San Francisco presidents; and the Richmond post is presently vacant.

My good friend and fishing buddy Bob Eisenbeis of Cumberland Advisors, a former Fed economist, pointed out in a recent analysis that once Yellen leaves, the Board of Governors will have only one doctorate-holding economist, Lael Brainard (who will quite likely be leaving the board within a year – see below). Marvin Goodfriend will be another when he is confirmed. I’ve discussed Goodfriend before. He was a featured speaker at the Fed’s Jackson Hole summer retreat last year, where he explained why he thinks negative interest rates are the best thing since sliced bread. I beg to differ, and I suspect some senators will disagree, too. Goodfriend’s confirmation hearing will be must-see TV for Fed watchers. I think rather than watching the live version on C-SPAN, which could drag on for hours as Senators try to grandstand, I will just wait for the YouTube highlights. But I actually will watch that highlight reel.

To be fair, Goodfriend is often cited as a conservative economist. I am not sure how that squares with his open support of negative interest rates. Bob Eisenbeis also just penned a piece on Marvin Goodfriend. There is no question Marvin is qualified. Here’s Bob:

He [Goodfriend] brings a lot to the table. First, he is a first-rate economist with a truly international reputation. He has held visiting, consulting, and evaluative positions at numerous central banks and international organizations including the Riksbank (Sweden), Bank of Japan, De Nederlandsche Bank (Amsterdam), Bank of India, Norges Bank (Norway), Swiss National Bank, ECB, Saudi Arabian Monetary Agency, and IMF, just to name a few. Additionally, he has been actively involved with the Federal Reserve System itself since joining the faculty at Carnegie Mellon in 2005 and has been a member of the Shadow Open Market Committee. So he knows central banking and the workings, culture, and staffs of the Board of Governors and the Federal Reserve system more generally; and he has participated in policy evaluations of the performance of several non-US central banks.

Second, his academic credentials are extensive. He has published in the best journals in both the areas of monetary policy and international trade. He has served on the editorial boards of most of the major economics journals and is a research associate at the National Bureau of Economic Research.

Third, when it comes to policy, he understands the models employed. During Marvin’s long tenure at the Richmond Fed, the policy positions taken by then President Broaddus evidenced a concern by both men for inflation and keeping it low. This belief is also reflected in some of Marvin’s writings and transcends his time at the Richmond Fed. However, as was noted in a recent WSJ article summarizing his likely approach to policy, there are also times when one must also be concerned about deflation and how policy might best be conducted in a world where interest rates are zero or perhaps even negative. For example, Marvin proposed policy options for dealing with the so-called “zero lower bound” problem in 2000, long before it became a real issue in the wake of the financial crisis.

Back to the FOMC. The Atlanta, Cleveland, and San Francisco banks all have economists at the helm. Eisenbeis thinks the New York and Richmond Fed Banks will appoint economists as well. So we are setting up a situation where the 2018 FOMC will be split along two axes: governors/bank presidents and economists/non-economists. (Truly sidebar trivia: Axes is the only word in English that can be the plural of three different singular noun forms: ax, axe, and axis.)

How does that two-way split matter? As I have mentioned before, the economics profession hasn’t exactly covered itself in glory in the wake of the financial crisis. I wrote a deep-dive letter on that topic last January, called “Post-Real Economics.” Read it again if you’re interested. Briefly, I think academic economists have become too enamored of their models, which fail to account for the modern economy’s vast complexity and the often-irrational decisions people make.

I would much prefer to have the Federal Reserve System led by experienced business leaders and others with more practical experience in the economy the Fed helps manage. I think we would all be better off.

You know who agrees? The Fed’s founders. Section 10 of the Federal Reserve Act of 1913 tells the US president what kind of people to put on the Board of Governors:

In selecting the members of the Board, not more than one of whom shall be selected from any one Federal Reserve district, the President shall have due regard to a fair representation of the financial, agricultural, industrial, and commercial interests, and geographical divisions of the country.

Does that kind of “fair representation of the financial, agricultural, industrial and commercial” sectors exist on the present board? No. Jerome Powell, an attorney and a former private equity manager, will be the first non-economist chair in decades. I think that’s positive, though of course we’ll have to wait and see how his term unfolds.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Still, the Board of Governors doesn’t have, and possibly never has had, fair representation of nonfinancial private-sector businesses. “Main Street” has the Fed’s ear only indirectly, filtered through the regional banks and their Beige Book impressions.

If President Trump chooses to exercise his options, he can make history by actually following the law and giving the Board of Governors the kind of diversity its founders said it ought to have. His predecessors in both parties failed to do so. Maybe Trump will do better. We can only hope.

• Technically, the president is supposed to appoint someone from a community bank, which means someone with senior experience from bank with under $10 billion in assets.

• Rumor has it that Dr. Lael Brainard will hang around at least until the midterm elections next year to see which way the political winds blow. If it looks like her friend Senator Elizabeth Warren might become president in 2020, then she is a serious candidate for Secretary of the Treasury. If the Republicans somehow have a good election (and at this point who knows, since they seem to be forming up a circular firing squad), then she may go ahead and leave.

• There will be at least one dissenting vote, if not several, at the December meeting over raising rates in the coming year. While the FOMC has signaled that short-term rates will be raised at the December meeting, there are a few regional presidents who are concerned.

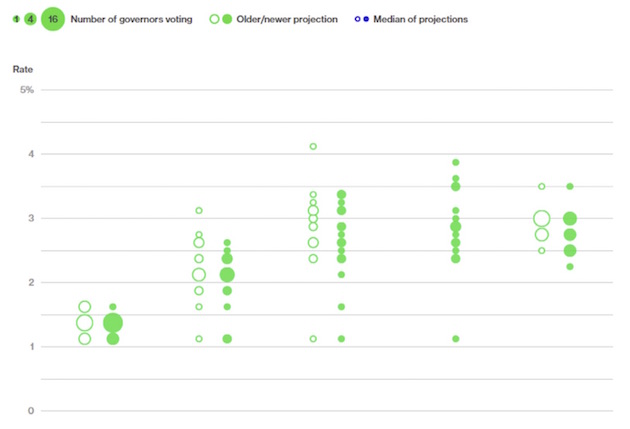

• There seems to be a drumbeat for much more aggressive raising of interest rates next year. The “dot plot” from the FOMC shows they expect to raise rates at least three and possibly four times.

Source: Federal Reserve Board of Governors

Goldman Sachs is now saying four raises. There seems to be this feeling that because the US economy has grown over 3% for the last two quarters (which is a great thing) and because unemployment is low, wage inflation is just around the corner. Nearly every current member of the FOMC (and much of the Fed staff) are slavish adherents to the Phillips curve, which says that wage inflation will increase when there is low unemployment. We will see about the future members, but economists and analysts that I respect are pointing out that with four more rate hikes we could easily see an inverted yield curve, perhaps in the first part of 2018, which typically signals a recession within 12 months. Just saying…

On the inflation issue, my friend Peter Boockvar recently had this to say:

The Fed’s favorite inflation gauge, the PCE index, rose .1% at the headline level in October and .2% at the core m/o/m and 1.6% and 1.4% y/o/y respectively. All were about in line with expectations, while the core rate, however, was revised up by one tenth in September. Higher energy prices helped to drive the headline gain y/o/y but was down m/o/m after the spike in the two prior months while durable goods prices fell again. Services inflation remained steady, rising by 2.2% y/o/y.

The average of the core and headline inflation numbers is 1.5%. That is not exactly rip-roaring inflation. Of course, the inflation the average person sees is in the cost of health care and housing – you know, things they actually purchase. And to quote my friend Doug Kass from last night:

We truly live in a parallel universe inhabited and controlled by passive investing products (ETFs) and strategies (risk parity and volatility trending), which have been delivering a virtuous cycle as their inflows continue to overwhelm the markets and are conditioned to buying every dip.

When interest rates rise and central banks pull back (or an unexpected event occurs), the virtuous cycle could be halted by outflows from ETFs and from these machine-dominated algos.

Despite protestations on our site and elsewhere, the recent market leg higher has only partially been influenced by the corporate profit and economic backdrop. As I have documented, this has been a valuation-driven and not an earnings-driven market buoyed by inflows into the aforementioned products and strategies coupled with excess central bank liquidity.

Meanwhile, I continue to pound home that each day that goes by we get closer to a much wider monetary tightening next year – $420 billion to be sucked out by the Fed and about $500 billion less in the way of buying from the European Central Bank. I would note for timing purposes that one trillion dollars of reduced liquidity in 2018 is beginning in just four weeks.

I echo those sentiments. I keep asking, “Where’s the fire?” The obsession with potential inflation when we are not even close to their so-called 2% inflation target is lost on me. I simply do not understand the urgency to raise rates and contract the monetary supply at the same time. Why not do one and then the other? This is another form of QE, only this time it is Quantitative Experiment. They simply have no idea what’s going to happen when they pull that much money out of the money supply at the same time they are raising rates.

As my friend Lacy Hunt pointed out in a conversation today, given the extensive debt in the country, there is less room for tightening monetary policy than many on the FOMC and Fed staff think there is. There is also less of a tendency for inflation to actually become a problem.

I mean, I would actually welcome a little wage inflation. I think it would be good for the country. But economists are too stuck on their models and aggregates and are not breaking down the difference between the working class, the service class, and the professional class. The professional class has pricing power. The working class and especially the service class do not have pricing power. The number of people sitting on the sidelines rather than looking for work understates an “unemployment rate” that counts only those who are actively looking for work but can’t find it.

With market valuations stretched everywhere, with a full-blown bull market mentality in almost everything (dear gods, when strippers in Australia are trading Bitcoin and yakking about it on social media, we are reminded of Joe Kennedy’s shoeshine boy touting his investing moves in 1929), and with the prospect of virtually no liquidity if there were to be a selloff in the high-yield markets in either Europe or the US, I think it makes sense to be a bit cautious.

The time to have been raising rates was back in 2013 and going forward. However, Ben Bernanke wanted to pump up asset prices of all kinds – and he took full credit for the bull market in stocks and housing and for the other effects of low rates. The fact that savers and retirees were the ones to pay the price for his quantitative easing and bull market seems to be lost on him and much of the rest of the Fed. And now the Fed feels that taking all that away will have no effect on the markets? And with exactly zero evidence or a model or two to demonstrate that it is so? I mean, we have never been here before.

You want to know why people are fed up and angry with the elites? They feel they have no control over their lives and that there are a few people who seemingly run the system for the sole benefit of the rich. Sadly, there is more truth to that conclusion than I would like to think.

The world lost one of the really good guys and great economists last week. Rich Yamerone, a name that is familiar to longtime readers, as I often quoted him (and teasingly calling him Darth Vader, a moniker that he picked up on). As his last professional gig, he was a longtime senior economist at Bloomberg. He created the Orange Book for Bloomberg Intelligence, had a prodigious travel schedule that took him to colleges and universities all over the country to talk to students, and was a regular guest at the dinners I call together when I am in New York City. His sense of humor was legendary and was always welcome.

He was playing ice hockey on Thanksgiving with his friends and suffered a heart attack and died shortly thereafter. He died a young man, at 55. Rich was a true Renaissance man. He sang opera and played the guitar; he was a pilot, a fly fisherman, and a ranked athlete. But more than that, he knew every economic statistic in existence and every detail about that statistic. He literally wrote the book, which he updated several times, on economic statistics.

My favorite statistic that he would quote at me concerned women’s clothing sales. His point was that the wife is the CFO of the family, and when there is extra money she goes out and spends it. If money is tight, she doesn’t. You could actually see the correlations with US consumer spending.

Our mutual friend Barry Ritholtz wrote a tribute column, and he quoted what others were saying about Rich at the end. Mike McKee and Tom Keen at Bloomberg did a tribute to him here.

Source: Bloomberg

He will be missed by many of us in the economics profession, and there will be a hole in the fishing group next year in Maine and at our New York dinners. Rest in peace, my friend. We just didn’t have enough time, did we? We were all so lucky to know you.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Somehow, after writing that, I really don’t feel like adding any more personal comments. So I think I will just hit the send button and wish you a great week!

Your thinking the words “Here’s to fallen comrades” are appropriate analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.