Inflation Reaches Unicorns

-

John Mauldin

John Mauldin

- |

- June 24, 2022

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin“Government has three primary functions. It should provide for military defense of the nation. It should enforce contracts between individuals. It should protect citizens from crimes against themselves or their property. When government—in pursuit of good intentions—tries to rearrange the economy, legislate morality, or help special interests, the cost comes in inefficiency, lack of motivation, and loss of freedom. Government should be a referee, not an active player.”

—Milton Friedman

“Don’t give me a low rate. Give me a true rate, and then I shall know how to keep my house in order.”

—Hjalmar Schacht, Reichsbank president, 1927

One reason today’s inflation has us all so concerned is we went a long time without any—or at least not much. That wasn’t normal. In the 1990s, a 3% annual Consumer Price Index reading was common and almost unremarkable. CPI approached 5% in 2005 and was briefly over 5% in 2008. But from 2012 until last year, 3% was a hard ceiling—to the point where Federal Reserve officials worried more about generating inflation than preventing it.

At the same time, many households faced constantly rising bills for healthcare, housing, and other essentials. The benchmarks certainly didn’t reflect common experience. But inflation was, if not actually low, at least lower than in the past. This is one reason the prospect of extended 5%, 8%, or higher inflation feels so dreadful. We’ve forgotten what it was like.

Post-2008 monetary policy unleashed deflationary forces no one anticipated. As often happens, well-intentioned plans had unintended side effects. Years of near-zero interest rates didn’t just produce stock and real estate booms. They also changed how businesses operate in ways that are now adding to our inflationary pain. The Fed and other central banks financialized markets and business to an extent that we are just now recognizing, distorting the economy in ways that will haunt us for years.

As you’ll see today, interest rates aren’t simply the price of borrowing money. They are also information, providing signals telling economic players what to do. Interest rates are in fact the price of time. Low interest rates don’t value time very much. Bad signals produce bad outcomes… and that’s where we are now.

This letter is actually in two parts. I’m going to describe a set of circumstances which are odd in and of themselves, and then we’ll begin to look at the reasons.

Unicorn Herd

Investors are naturally (and correctly) concerned about inflation and/or recession affecting the stock market. They’re usually thinking of the public stock market, which of course is quite important but it’s not the only stock market.

A growing number of large, well-known companies are choosing to stay private long past the point where they would once have gone public. It’s become common enough to have a term. They’re called “unicorns.”

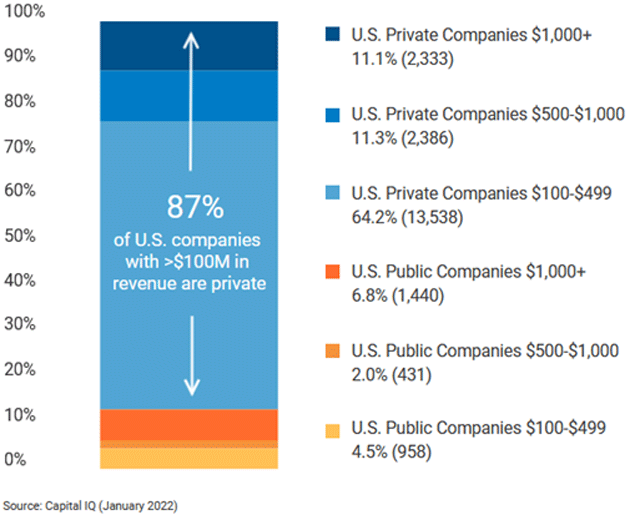

Here’s a number I bet will surprise you. As of January 2022, the US had 2,800 public companies with annual revenues over $100 million—and 18,000 private companies of that size.

Source: Hamilton Lane

Many of these companies have no plans to ever go public. They are family-owned or otherwise don’t need the hassles that go with an exchange listing. An IPO gives early shareholders an easier exit, but if they don’t need or want that liquidity, staying private is often more attractive.

Now, think about where a fast-growing private company gets its capital. The main source is by selling equity via private offerings to venture capital funds, institutional investors, or wealthy individuals, and (at later stages) to private equity funds.

From the investor or manager’s point of view, a portfolio of unicorns that might disrupt an industry is relatively more attractive when the alternative is a 2% corporate bond. This leads to a weird situation where companies go years not just without profits but sometimes without revenue, staying in business only because their VC investors believe a giant breakthrough is coming. Cash running low? Just do another round. The money will be there.

Now that model is breaking down—and it’s making inflation worse.

Disruption Plans Disrupted

With all that in mind, let’s look at a recent article from The Atlantic. It’s not economic analysis as such. The writer, Derek Thompson, simply observed some changes in his urban Millennial lifestyle—like $50 for an Uber ride that until recently cost much less—and wondered what was causing them.

In answering that question, I think he hit on something important. Here’s part of the story, with some of his key points in bold.

“With markets falling and interest rates rising, start-ups and money-losing tech companies are changing the way they do business. In a recent letter to employees, Uber’s CEO, Dara Khosrowshahi, said the firm needs to ‘make sure our unit economics work before we go big.’ That’s chief-executive speak for: We gave Derek a nice discount for a while, but the party’s over and now it costs $50 for him to get home.

“For the past decade, people like me—youngish, urbanish, professionalish—got a sweetheart deal from Uber, the Uber-for-X clones, and that whole mosaic of urban amenities in travel, delivery, food, and retail that vaguely pretended to be tech companies. Almost each time you or I ordered a pizza or hailed a taxi, the company behind that app lost money. In effect, these start-ups, backed by venture capital, were paying us, the consumers, to buy their products.

“It was as if Silicon Valley had made a secret pact to subsidize the lifestyles of urban Millennials. As I pointed out three years ago, if you woke up on a Casper mattress, worked out with a Peloton, Ubered to a WeWork, ordered on DoorDash for lunch, took a Lyft home, and ordered dinner through Postmates only to realize your partner had already started on a Blue Apron meal, your household had, in one day, interacted with eight unprofitable companies that collectively lost about $15 billion in one year.

“These start-ups weren’t nonprofits, charities, or state-run socialist enterprises. Eventually, they had to do a capitalism and turn a profit. But for years, it made a strange kind of sense for them to not be profitable. With interest rates near zero, many investors were eager to put their money into long-shot bets. If they could get in on the ground floor of the next Amazon, it would be the one-in-a-million bet that covered every other loss. So they encouraged start-up founders to expand aggressively, even if that meant losing a ton of money on new consumers to grow their total user base…

“This arrangement is tailor-made for a low-rate environment, in which investors are attracted to long-term growth more than short-term profit. As long as money was cheap and Silicon Valley told itself the next world-conquering consumer-tech firm was one funding round away, the best way for a start-up to make money from venture capitalists was to lose money acquiring a gazillion customers.

“I call this arrangement the Millennial Consumer Subsidy. Now the subsidy is ending. Rising interest rates turned off the spigot for money-losing start-ups, which, combined with energy inflation and rising wages for low-income workers, has forced Uber, Lyft, and all the rest to make their services more expensive.”

We talk about companies raising prices to preserve their profit margins against inflation. That’s certainly happening, but a whole other universe of companies lack profits in the first place. Some are quite large, too. Many are privately held. We don’t see their quarterly reports—but I’ll bet the last quarter or two had even bigger losses than usual.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Low interest rates enabled this but weren’t the only factor. It was low interest rates accompanied by an investor belief that enough cash and patience would produce the same kind of disruptive, exponential growth that made Jeff Bezos so fantastically wealthy. They all want the returns like a $10,000 investment in an Amazon IPO would now be worth (drum roll) ~$20 million. And if you put $1,000,000 in an early private round? I think the term is gajillions. Thus, the allure of chasing the next unicorn.

It really happens that way in a few rare cases. More commonly, though, these ultra-patient investors shielded their startup companies from normal market forces that tell management whether its plans are working or not. Often, they didn’t work, at least not at the subsidized prices they dangled to consumers whom they hoped to hook for life.

The stories were alluring. Taxis used to be super expensive; surely technology could deliver a better solution. Uber and Lyft seemed to be the answers. But now, having started to travel again, I can tell you the old-fashioned, regulated yellow cabs are often less expensive than the higher fares the app-based services now charge, if not as comfortable.

In other words, what we see as “inflation” often represents not higher prices, but the end of artificially low prices. Or, put differently, it’s not so much price inflation as price rationalization. These businesses are finally having to charge enough to cover their costs, which comes as a shock to customers.

The market will sort this out eventually. Companies that can turn a profit offering things consumers want at prices consumers can pay will survive. But the winnowing process won’t be fun.

That means, as we watch a bear market on Wall Street, a less visible bear market will be unfolding in Silicon Valley, and in the boardrooms of institutions who invested in venture capital funds. We won’t see the full story, but we’ll see the effects. The companies will cut costs with lower wages and/or layoffs. Some will default on debt payments or even go bankrupt, leaving those starry-eyed shareholders holding only an empty bag.

Animal Spirits

Something similar happened in the energy business a few years ago. A combination of low interest rates, regulatory changes, and new technology enabled low-cost production from previously unprofitable shale oil and gas deposits. Crude oil prices were mostly above $80 for almost five years (2010‒2014) with production costs less than half that level. The seemingly forever profits encouraged oil companies to leverage their production at friendly banks.

The resulting handsome profits drew in new players and a lot of new production which, combined with Saudi Arabia defending its market share, drove prices sharply lower. The US economy had a rough stretch in 2015‒2016 as the boom unraveled. It wasn’t technically a recession, but sure felt like one in energy-producing regions.

The old commodity saying, “High prices are the solution to high prices” has a corollary: Low prices are the solution to low prices, too. The years following 2015 gave little incentive to invest in new production. Then when crude oil dropped nearly to zero (and briefly below zero) in the COVID panic, the industry had a kind of near-death experience. I imagine some executives saw their careers flash before their eyes. This raised the threshold for making capital investments even further. The religion of ESG and the pressure on institutions not to lend to oil companies is quite real, driving up the cost of new capital investments.

If, hypothetically (because the real world doesn’t work like this), oil prices had simply held steady around $80 for the last decade, we might be in an entirely different world now. Oil producers would be making a nice profit, supplies would be adequate, and the present inflation would be much less severe. The boom-bust cycle doesn’t let it happen that way, though.

This leaves energy companies in the opposite position of those VC investors described above. They won’t invest in long-term growth because they’re not confident there will be any. They see both governments and consumers increasingly favoring renewable energy, environmental regulations making fossil fuel production more expensive, and higher interest rates raising the cost of the capital that would let them overcome the other obstacles.

On top of that, the very real possibility of a global recession cratering fuel demand in the next year or two, thereby rendering any new capital investments unprofitable, gives energy producers every incentive to extract as much cash as they can, now. That happens to be what their investors want, too.

But in both cases, the result for consumers is higher prices. We will pay more for the services that VCs had been subsidizing, and we will pay more for the fuel the energy industry will produce only in quantities where it takes little to no risk.

That’s the common thread: Low interest rates created a distorted market which led to problems which ended in risk aversion. The animal spirits that have long let the technology and energy industries deliver innovative, cost-effective products are disappearing. Well, maybe not disappearing but going into hibernation. I see little reason to expect change anytime soon.

That means the higher prices—and the inflation they are fueling—probably aren’t going anywhere.

The Price of Time

My friend Rob Arnott introduced me to Edward Chancellor with a glowing review of his new forthcoming book, The Price of Time: The Real Story of Interest. We exchanged emails and I asked for a PDF copy of the book which he graciously sent.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I am partway through the first few chapters, but I can say the book is magisterial in its scope. He describes the reasons for the current distortion of the markets and why wealth and income disparity were so pronounced in the last 20 years. He lays blame on the Federal Reserve and central banks around the world distorting the markets with low interest rates. You’ll want to buy this book and get it the first day available.

With permission, here are a few quotes. From the introduction:

“In the year of Bastiat’s death, a final pamphlet appeared. In ‘What Is Seen and What Is Not Seen’ Bastiat tells the parable of a merchant, Jacques Bonhomme, whose shop window is broken by his careless son. Neighbors thought that it wasn’t all bad news. At least repairing the window provided employment for the glazier, who could spend the money on food and other sundries. But Jacques Bonhomme now had less money to spend, says Bastiat. Here, Bastiat is urging readers to consider the broad consequences of any economic action, not just its effect on a particular beneficiary:

“In the sphere of economics, a habit, an institution, or a law engenders not just one effect but a series of effects. Of these effects only the first is immediate; it is revealed simultaneously with its cause; it is seen. The others merely occur successively; they are not seen; we are lucky if we foresee them. The entire difference between a bad and a good Economist is apparent here. A bad one relies on the visible effect, while the good one takes account of both the effect one can see and of those one must foresee.

“The bad economist, says Bastiat, pursues a small current benefit that is followed by a large disadvantage in the future, while the good economist pursues a large benefit in the future at the risk of suffering a small disadvantage in the near term. The American journalist Henry Hazlitt elaborated on Bastiat’s Parable of the Broken Window in his bestselling book Economics in One Lesson (1946). Like Bastiat, Hazlitt lamented the ‘…persistent tendency of men to see only the immediate effects of any given policy, or its effects on only a special group, and to neglect to inquire what the long-run effects of that policy will be not only on the special group but on all groups. It is the fallacy of overlooking secondary consequences.’

“Hazlitt criticized the ‘new’ economics of his day which, he believed, considered only the short-term effects of policies on special groups and ignored the long-term effects on the whole community. He attacked what he called the ‘fetish’ of full employment. Schumpeter’s idea of ‘creative destruction’ must be allowed to operate unhindered, Hazlitt wrote, as it was as important for the health of an economy that dying industries be allowed to die as it was for growing industries to be allowed to grow. Hazlitt compared the price system in a competitive economy to the automatic regulator on a steam engine. Any attempt to prevent prices from falling would only keep inefficient producers in business. The supply and demand for capital are equalized by interest rates, Hazlitt maintained. Yet a ‘psychopathic fear of “excessive” interest rates’ induced governments to pursue cheap money policies. Easy money, wrote Hazlitt, ‘…creates economic distortions . . . it tends to encourage highly speculative ventures that cannot continue except under the artificial conditions that have given birth to them. On the supply side, the artificial reduction of interest rates discourages normal thrift, saving, and investment. It reduces the accumulation of capital. It slows down that increase in productivity, that ‘economic growth’ that ‘progressives’ profess to be so eager to promote.’”

We will re-visit this next week. This low/zero interest rate distortion has been the true source of financialization, preventing Schumpeter’s needed creative destruction. New companies don’t get to provide better services at lower prices when artificially low interest rates keep older, sclerotic companies alive on life support.

Life in Paradise

Not much happening here until mid-July when my twins and their daughters and husbands get here for a few days, other than lunches and dinners with friends.

I am spending my time reading a lot, especially about energy. I am increasingly convinced that between the government and the religion of ESG and the determination of the big oil producers not to bring about another 2015 and return money to their investors that prices are going to remain relatively buoyant.

Time to hit the send button. Enjoy your weekend and follow me on Twitter.

Your angry about monetary policy manipulation analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.