Gross Domestic Problems

-

John Mauldin

John Mauldin

- |

- January 27, 2018

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinFictitious Wall Street villain Gordon Gekko famously declared, “Greed is good.” I think actual Wall Street titans would mostly disagree. They would change one word. Instead of “greed,” they would say, “Growth is good.” That is Wall Street’s real mantra. Growth is the magic elixir we all need.

Getty Images

The question, if we define growth as good, is how do we measure it? Presently we use gross domestic product, or GDP. But GDP is showing its age in the 21st century. The measure was actually invented in the late 1930s when President Roosevelt needed some way to prove that his policies were working. And at 85 years old, the old formula may be nearing time for retirement.

The only way for Roosevelt to show that his policies were working was to put government spending inside the GDP number. There was vicious fighting among economists over whether he should be allowed to do so. Many economists even argued that military spending should not be included in GDP because it didn’t produce anything. And it’s true that overreliance on GDP has often sent policymakers and business owners in wrong directions. We need a better yardstick.

First, we must next decide what, specifically, a newly formulated GDP should measure and how – and that’s a thornier question than you might think. Today we’ll wrestle with that question and with some of the implications of changing how we measure growth.

These are exactly the types of pressing questions we will be attempting to answer at my upcoming Strategic Investment Conference. By “we,” I mean the hand-selected, A-list cast of economic, investment, and geopolitical powerhouses who will speak, and the audience that will respond to them. And for SIC 2018 we really do have an all-star group, including “bond king” Jeffrey Gundlach, hedge fund titan John Burbank, renowned historian Niall Ferguson, and some 20 more brilliant minds. At SIC you will get their latest and best thinking. Better yet, SIC is small enough that you can usually find the speakers in the hallway or after hours and interact with them.

In addition, there are a couple of hundred “core” SIC attendees who come every year. They represent a remarkable range of talent, experience, and wisdom. Some of them really ought to be on the stage. Instead, they’ll be sitting with you, and you’ll find them friendly and ready to swap ideas. We’ve seen countless business relationships form at SIC, and many more will happen this year. I hope you’ll join us, March 6–9, in San Diego.

Now, let’s see how we can fix the GDP problem, starting with where we are right now.

Getty Images

Brian Wesbury, chief economist at First Trust Advisors, has been calling our present recovery phase a “plow horse economy” for several years. It’s not fast or impressive, but it’s not stopping, either. He’s been mostly right, too.

Last week Brian said that the horse is now breaking free.

We’ve called the slow, plodding economic recovery from mid-2009 through early 2017 a Plow Horse. It wasn’t a thoroughbred, but it wasn’t going to keel over and die either. Growth trudged along at a sluggish – but steady – 2.1% average annual rate.

Thanks to improved policy out of Washington, the Plow Horse has picked up its gait. Under new management, real GDP grew at a 3.1% annualized rate in the second quarter of 2017 and 3.2% in the third quarter. There were two straight quarters of 3%+ growth in 2013 and 2014, but then growth petered out. Now, it looks like Q4 clocked in at a 3.3% annual rate, which would make it the first time we’ve had three straight quarters of 3%+ growth since 2004-5.

That was Monday. On Friday the Commerce Department released its first 4Q GDP estimate at 2.6%. The estimate will likely change, but for now it looks like Brian was a tad bit optimistic about Q4. But you should read his outlook anyway, because he breaks his estimate down to the components of GDP to show how he arrived at 3.3%.

The GDP formula is C + G + I + NX, where

C = Consumer spending

G = Government spending

I = Private investment

NX = Net exports.

Net exports is exports minus imports, so it’s a negative number for a country like the US that runs a trade deficit.

To get GDP, you just estimate the change in each component, weight it by the appropriate amount, and add the components together.

That’s easy enough, but the calculation ignores whether those are the right components and how to define them. The result is a lot of potential distortion. For example, very little happens to GDP if you do your own housekeeping. You consume some cleaning products, but your labor doesn’t count, no matter how long you scrub. But the labor does count toward GDP if you hire someone and pay that person to do the exact same work while you take a nap. The hired labor “produced” something of value, and you did not.

To an economist, a barrel of oil selling for $100 has the exact same effect on GDP as two barrels of oil selling at $50. Silly, but that’s the way the accounting works.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Looking deeper, we realize that GDP is a historical artifact from an industrial economy that doesn’t really exist anymore, at least in the US. GDP worked well in the post-World War II era when the US economy thrived by making material goods: trucks, cars, machinery, appliances, airplanes, houses, and skyscrapers, etc. Output is easy to measure for such goods, as are the kinds of inputs required to produce them, mainly large factories and raw materials.

Today’s economy isn’t like that. Technically, manufacturing is still 35% of GDP, but fewer than 9% of US workers are actually involved in that manufacturing. We are producing more stuff than ever, but we are doing it with far fewer people. And now we produce huge quantities of largely intangible goods: computer software, movies, music, and so on. Those products are easy to copy and hard to track. The productive capacity often exists inside some smart human’s brain. How do you measure that?

Think also of how much more productive technology has made us. That’s hard to measure, too. Imagine it’s 1975 and you want to know what GDP growth was in 1972. Unless you happen to be an economist who keeps such figures handy, you get in your car and drive to the library. You consult a card catalog, note the Dewey Decimal classifications of a number of promising volumes, then set off to search the shelves for them. When you chance on something, you thumb back and forth through it to find the statistic you want. Then you head back home and resume typing your research paper on a typewriter – perhaps you even have an IBM Selectric!

To get that number now, of course, you whip out your smartphone, type “us gdp 1972” into a search window and voila! I just did this, and it literally took me less than five seconds.

Getty Images

Or consider travel. Remember the spiral-bound map books that covered major cities? In Dallas the company that made them was called Mapsco. If your job involved going to unfamiliar places, you had to have one, and they were expensive. And you had to buy a new one at least every few years. Now your phone can get you anywhere you want to go, not just in your hometown but the world over.

We could list thousands of little tasks that used to take hours but now require only seconds. Add up all that time saved, then scale it over hundreds of millions of workers. The impact on productivity is mind-boggling. Does it show up in GDP? Not really. It may even reduce GDP, since we no longer consume as much fuel, printing, and library space, etc. I grew up in the printing business, and I would often print prospectuses. They were incredibly expensive and time-consuming to produce. Today a prospectus is a PDF file. Going back to the old ways might improve the economic numbers, but would it help the economy? No way. Yet we measure economic growth as if it would. That’s a problem.

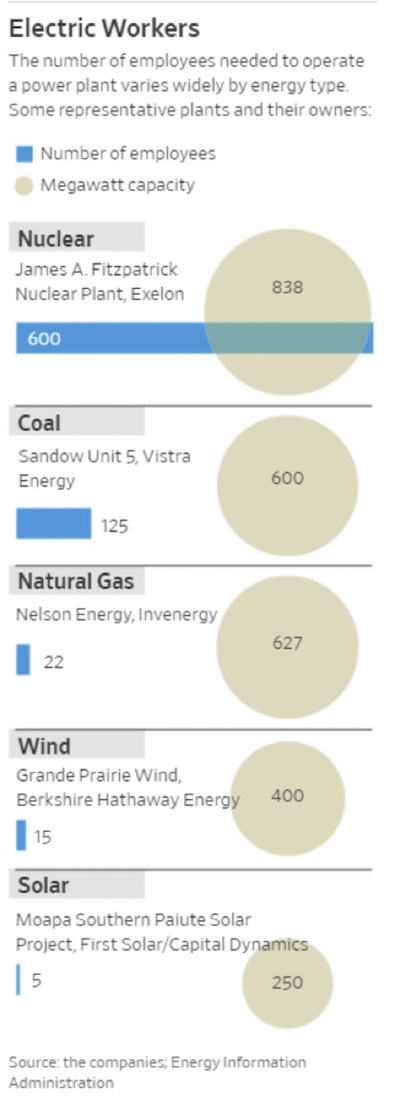

Our antiquated methods matter to employment, too. I saw in a recent Wall Street Journal report the reduction in labor needed to operate a power plant as we move from nuclear or coal to natural gas or wind or solar. One company that is shutting down its coal plant and laying off 430 workers will be opening a solar plant in West Texas that will be one of the largest solar facilities in the country, operated by two workers, who may actually be part-time. Put that in your future-of-work pipe and smoke it.

Coal power accounted for 39% of US electricity production in 2014, 33% in 2015, and 30.4% in 2016. There are 1308 coal-powered plants in the US. Assume 125 workers per plant. That’s 163,500 workers. Now cut that number by at least 80% if the plants all shift to natural gas, which they will over time. That’s a loss of 130,800 workers. And that’s assuming that they all go to natural gas and don’t go to wind or solar. This is going to happen in the next 10 to 15 years. My math could be off here or there, but not by an order of magnitude.

We are now producing vastly more energy with far fewer workers than we did in GDP’s heyday. That’s a labor problem for sure, but it’s also a growth measurement problem. We desperately need a better method.

Getty Images

I could go on at length about the problems with GDP, but I’ve done that before. Read “GDP: A Brief But Affectionate History” and “Weapons of Economic Misdirection” for the gory details.

A key question: Is GDP completely outmoded, or does it just miss some things? If the latter, then maybe it just needs some tweaking instead of total replacement. The wickedly brilliant Diane Coyle, a University of Manchester economist, has been working on this issue for years. She proposed in a recent paper with Benjamin Mitra-Kahn a series of incremental changes that should help: better measurement of intangible goods, an adjustment based on income distribution, and some other relatively simple changes.

Distribution effects are a problem whenever we look at GDP per capita, as we commonly do when we compare nations. Almost everywhere, income is far more concentrated at the top than it used to be, but the effect varies a lot depending on where you are. It is entirely possible, indeed it is likely in some places, for per capita GDP to rise sharply while most of the population sees no change in its living standards or economic health. An adjustment to compensate for this inequity is an excellent idea.

That point brings up a thornier problem, though. In whatever way we measure it, is “growth” the right thing to watch? Does it really tell us what we think it does? We look at GDP growth and assume a country that has it is prospering. We think everyone who lives there must be thrilled. Often, they have little reason to be.

The assumption works in the other direction, too. If GDP is flat or falling, we see a recession and react accordingly. That is particularly the case with political leaders and central bankers, who then introduce policies to solve the perceived problem. These policies can be damaging if the problem is less serious than central bankers think it is. This may be happening in the US right now.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We’re asking GDP to do something it can’t. What we want is a benchmark of economic progress. Are a country and its people generally better off economically than they were last year or five years ago? If so, by how much? Then we can start to know which policies might help and which might hinder progress. Business owners would be able to make better decisions, and ultimately everyone should feel the benefits.

The problem is, measuring concepts like income inequality may differently skew the witches’ brew that is GDP. The only part of the economy that is really subject to serious increases in productivity is manufacturing; and, as noted above, manufacturing involves less than 9% of the workforce. It is hard to get increased productivity out of service workers. Now, you can use technology to replace them, but that hardly improves their situation, even if it does increase the production of gross domestic stuff per dollar spent.

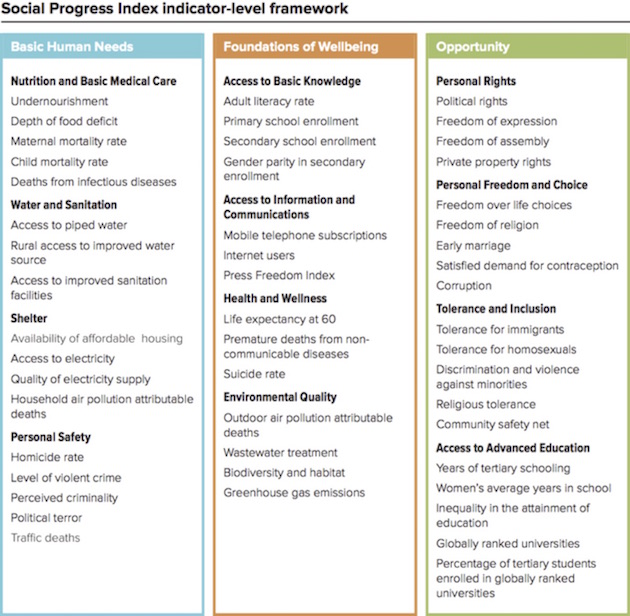

People have proposed such measures. In 2013 the Skoll World Forum launched the Social Progress Index, defined as “the capacity of a society to meet the basic human needs of its citizens, establish the building blocks that allow citizens and communities to enhance and sustain the quality of their lives, and create the conditions for all individuals to reach their full potential.”

Some of those indicators could be hard to pin down. I don’t see how you put a number on “religious tolerance,” or “tolerance for homosexuals,” for instance. But the creators of the index are on the right track in that they are attempting to measure well-being. I am not certain how widely accepted such a measure would be, but it’s a start.

Another effort appeared in a 2010 book by economists Joseph Stiglitz, Amartya Sen, and Jean-Paul Fitoussi, called Mismeasuring Our Lives: Why GDP Doesn’t Add Up. Their suggestion is to continue using GDP but add other data points to clarify it. They would use things like life expectancy, debt levels, educational achievement, and other social progress metrics.

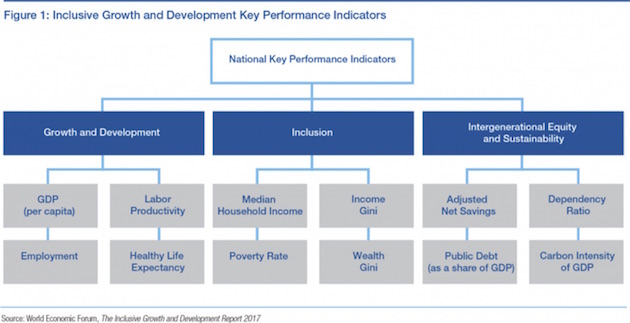

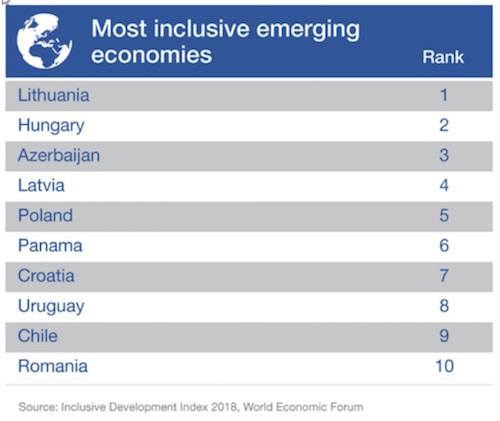

The World Economic Forum, which had its annual shindig in Davos last week, took another stab at this problem with its “Inclusive Development Index.” It too supplements GDP with other progress indicators.

The WEF paper says GDP is fine as a top-level measure, but growth is a means to an end, namely better living standards. Only by looking at those living standards can we know if GDP growth is accomplishing what it should.

By WEF standards, the “most inclusive” advanced economies are mostly European. The US and Canada are not in the top 10. The most inclusive emerging economies list is more interesting. Azerbaijan? Really?

Lithuania leads the list, and from what I’ve heard, it probably deserves to do so. (We have employees in Lithuania, and they are excellent and productive workers, as are our Eastern European staff. We are truly a worldwide virtual company.) The other countries on the list look like a strange mix at first but make more sense after some thought. Several live in the shadow of much larger neighbors, so maybe they are more willing to innovate. This list would be a good starting point if you have money to deploy in emerging markets.

That’s a good thought: Countries that are growing in a fair, sustainable way should attract investment. Often they don’t, because investors want quick profits. Look at the move by corporations to increase the number of temporary workers and contract workers so that they are not so much paying for employees as paying money for actual production, without having to cover a lot of the extra benefits that normally go along with traditional employment.

This is a particular complaint that I hear from the friends of my kids, especially the Millennials. They need to hold two part-time jobs in order to make ends meet, and generally those are not jobs that pay a great deal. The gig economy is not all that it’s cracked up to be. The drive by senior management to create short-term profits and to see employees as liabilities rather than as partners in the business process will create a great backlash in coming years.

I’m going to stop here because the next section of the letter would be at least as long as this letter is so far. But let me tease you for next week. I think I’m getting ready to start talking about the probability of a recession before the 2020 election cycle. I see structural problems, monetary policy errors, and a tax cut that is not going to produce the results that the Reagan tax cuts did. M2 money is not even growing at 2%. The savings rate is the lowest it has been for 70 years except for one quarter in 2005; and even though consumer spending was strong last quarter, it came from much-reduced savings and borrowing, much of it on credit cards as a result of the two hurricanes and other disasters and longer-term challenges.

So while on the surface 4.4% nominal GDP growth and 2.6% real growth look pretty good, when you really begin to inspect the engine of growth, you find less under the hood. The velocity of money keeps falling. Our demographics mean that we are not adding workers, and the latest immigration proposal would reduce the number of immigrants and potential workers. And while I am all for allowing the so-called Dreamers to be allowed to stay in this country – the only home country they have known – we do need to be a lot more strategic about allowing potential workers into this country.

After all, GDP is simply the number of workers times productivity. With the number of workers tailing off and with productivity as weak as it has been, the sugar high that the economy has been on is going to wear off. Let me hasten to say, I don’t think nearly enough credit has been given to Trump for changes in the regulatory environment. It’s not merely the reduced number of regulations, it’s the attitude of the regulators that I keep hearing businessmen talk about. Given that I am in highly regulated businesses, I hope to enjoy that new environment sooner rather than later.

I will be in Sonoma with my friends at Peak Capital in late February, and then of course I’ll head to San Diego for my conference. I’ll arrive a few days early and maybe stay an extra day just to relax from the adrenaline rush.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

My travel seems to have slowed down somewhat, as more people have been coming in my direction lately, keeping me from having to get on the road. And that is a good thing.

Being in and out of the cold in Boston last week – even though I was dressed for the weather – must have weakened my immune system, and then I sat in the plane across the aisle from somebody who was coughing his lungs out. But whatever the reason, I have had a serious head cold that is finally starting to get somewhat better. Last night was the first decent night’s sleep I’ve had. But I shouldn’t complain, as I rarely get sick. And at least I haven’t had a run-in yet with this season’s flu, which I am told is really devastating.

I’m spending a great deal of time on the phone, talking with speakers who will join us at the Strategic Investment Conference, going over details and getting a heads-up on where they are going with their presentations. I am actually shuffling the speaking order around in order to make things flow better. Planning this conference is my personal art form, and from the response I get, it seems I do a reasonably good job. But it helps to have an incredible team. Shannon Staton is the primary reason it all comes together. We are looking to add one or two more speakers and panel members that I think would be strategic, but with the conference just six weeks away, we are really having to lock things in.

Let me wish you a great week, and I think I will make myself some nighttime TheraFlu, which seems to help, and then began to wind down for the weekend.

Your worried about Federal Reserve monetary policy errors analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.