Every Central Bank for Itself

-

John Mauldin

John Mauldin

- |

- April 12, 2014

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinEvery Central Bank for Itself

The QE-Induced Bubble Boom in Emerging Markets

Anatomy of a “Balance of Payments” Crisis

The Taper Reveals What QE Was Hiding

Rajan Shows His Cards

What’s a Country to Do?

Amsterdam, Brussels, Geneva, and San Diego

“Everybody has a plan until they get punched in the face.”

– Mike Tyson

For the last 25 days I’ve been traveling in Argentina and South Africa, two countries whose economies can only be described as fragile, though for very different reasons. Emerging-market countries face a significantly different set of challenges than the developed world does. These challenges are compounded by the rather indifferent policies of developed-world central banks, which are (even if somewhat understandably) entirely self-centered. Argentina has brought its problems upon itself, but South Africa can somewhat justifiably express frustration at the developed world, which, as one emerging-market central bank leader suggests, is engaged in a covert currency war, one where the casualties are the result of unintended consequences. But the effects are nonetheless real if you’re an emerging-market country.

While I will write a little more about my experience in South Africa at the end of this letter, first I want to cover the entire emerging-market landscape to give us some context. Full and fair disclosure requires that I give a great deal of credit to my rather brilliant young associate, Worth Wray, who’s helped me pull together a great deal of this letter while I am on the road in a very busy speaking tour here in South Africa for Glacier, a local platform intermediary. They have afforded me the opportunity to meet with a significant number of financial industry participants and local businessman, at all levels of society. It has been a very serious learning experience for me. But more on that later; let’s think now about the problems facing emerging markets in general.

Before going into battle, every general has a plan, which immediately begins to change upon contact with the enemy. Everyone has a plan until they get hit… and emerging markets have already taken a couple of punches since May 2013, when Fed Chairman Ben Bernanke first signaled his intent to “taper” his quantitative easing program and thereby incrementally wean the markets off of their steady drip of easy money. It was not too long after that Ben also suggested that he was not responsible for the problems of emerging-market central banks – or any other central bank, for that matter.

As my friend Ben Hunt wrote back in late January, Chairman Bernanke turned a single data point into a line during his last months in office, when he decided to taper by exactly $10 billion per month. He established the trend, and now the markets are reacting as if the Fed's exit strategy has officially begun.

Whether the FOMC can actually turn the taper into a true exit strategy ultimately depends on how much longer households and businesses must deleverage and how sharply our old-age dependency ratio rises, but markets seem to believe this is the beginning of the end. For now, that’s what matters most.

Under Fed Chair Janet Yellen’s leadership, the Fed continues to send a clear message to the rest of the world: Now it really is every central bank for itself.

The QE-Induced Bubble Boom in Emerging Markets

By trying to shore up their rich-world economies with unconventional policies such as ultra-low rate targets, outright balance sheet expansion, and aggressive forward guidance, major central banks have distorted international real interest rate differentials and forced savers to seek out higher (and far riskier) returns for more than five years.

This initiative has fueled enormous overinvestment and capital misallocation – and not just in advanced economies like the United States.

As it turns out, the biggest QE-induced imbalances may be in emerging markets, where, even in the face of deteriorating fundamentals, accumulated capital inflows (excluding China) have nearly DOUBLED, from roughly $5 trillion in 2009 to nearly $10 trillion today. After such a dramatic rise in developed-world portfolio allocations and direct lending to emerging markets, developed-world investors now hold roughly one-third of all emerging-market stocks by market capitalization and also about one-third of all outstanding emerging-market bonds.

The Fed might as well have aimed its big bazooka right at the emerging world. That’s where a lot of the easy money ran blindly in search of more attractive real interest rates, bolstered by a broadly accepted growth story.

The conventional wisdom – a particularly powerful narrative that became commonplace in the media – suggested that emerging markets were, for the first time in a long time, less risky than developed markets, despite their having displayed much higher volatility throughout the past several decades.

As a general rule, people believed emerging markets had much lower levels of government debt, much stronger prospects for consumption-led growth, and far more favorable demographics. (They overlooked the fact that crises in the 1980s and 1990s still limited EM borrowing limits until 2009 and ignored the fact that EM consumption is a derivative of demand and investment from the developed world.)

Instead of holding traditional safe-haven bonds like US treasuries or German bunds, some strategists (who shall not be named) even suggested that emerging-market government bonds could be the new safe haven in the event of major sovereign debt crises in the developed world. And better yet, it was suggested that denominating these investments in local currencies would provide extra returns over time as EM currencies appreciated against their developed-market peers.

Sadly, the conventional wisdom about emerging markets and their currencies was dead wrong. Herd money (typically momentum-based, yield-chasing investors) usually chases growth that has already happened and almost always overstays its welcome. This is the same disappointing boom/bust dynamic that happened in Latin America in the early 1980s and Southeast Asia in the mid-1990s. And this time, it seems the spillover from extreme monetary accommodation in advanced countries has allowed public and private borrowers to leverage well past their natural carrying capacity.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Anatomy of a “Balance of Payments” Crisis

The lesson is always the same, and it is hard to avoid. Economic miracles are almost always too good to be true. Whether we’re talking about the Italian miracle of the ’50s, the Latin American miracle of the ’80s, the Asian Tiger miracles of the ’90s, or the housing boom in the developed world (the US, Ireland, Spain, et al.) in the ’00s, they all have two things in common: construction (building booms, etc.) and excessive leverage. As a quick aside, does that remind you of anything happening in China these days? Just saying…

Broad-based, debt-fueled overinvestment may appear to kick economic growth into overdrive for a while; but eventually disappointing returns and consequent selling lead to investment losses, defaults, and banking panics. And in cases where foreign capital seeking strong growth in already highly valued assets drives the investment boom, the miracle often ends with capital flight and currency collapse.

Economists call that dynamic of inflow-induced booms followed by outflow-induced currency crises a “balance of payments cycle,” and it tends to occur in three distinct phases.

In the first phase, an economic boom attracts foreign capital, which generally flows toward productive uses and reaps attractive returns from an appreciating currency and rising asset prices. In turn, those profits fuel a self-reinforcing cycle of foreign capital inflows, rising asset prices, and a strengthening currency.

In the second phase, the allure of promising recent returns morphs into a growth story and attracts ever-stronger capital inflows – even as the boom begins to fade and the strong currency starts to drag on competitiveness. Capital piles into unproductive uses and fuels overinvestment, overconsumption, or both; so that ever more inefficient economic growth increasingly depends on foreign capital inflows. Eventually, the system becomes so unstable that anything from signs of weak earnings growth to an unanticipated rate hike somewhere else in the world can trigger a shift in sentiment and precipitous capital flight.

In the third and final phase, capital flight drives a self-reinforcing cycle of falling asset prices, deteriorating fundamentals, and currency depreciation… which invites more even more capital flight. If this stage is allowed to play out naturally, the currency can fall well below the level required to regain competitiveness, sparking run-away inflation and wrecking the economy as asset prices crash.

(To those of you who’ve been reading me for a while, this may sound suspiciously similar to the Minsky cycle we often use to describe the leverage process. If you caught that, you get extra credit.)

In order to avoid that worst-case scenario, central bankers often choose to spend their FX reserves or to substantially raise domestic interest rates to defend the currency. Although it comes at great cost to domestic growth, this kind of intervention often helps to stem the outflows… but it cannot correct the core imbalances. The same destructive cycle of capital flight, falling asset prices, falling growth, and currency depreciation can restart without warning and trigger – even years after a close call – an outright currency collapse if the central bank runs out of policy tools.

The Taper Reveals What QE Was Hiding

That worst case is the looming risk for many emerging markets today, particularly in the externally leveraged “Fragile Five”: Brazil, India, Turkey, Indonesia, and South Africa (where I am as I finish this letter). Together they account for more than $3.3 trillion of the total $10 trillion of developed-country assets currently invested in emerging markets. Not only have those countries amassed a disproportionate share of total inflows to emerging markets, each has its own insidious combination of structural and political obstacles to long-term growth. And their own central banks are seriously constrained in the run-up to national elections between now and October 2014.

After a brief reprieve from taper-induced capital flight, the most externally leveraged emerging economies have had some time to breathe easy; but the crisis is far from over. This one, as all such booms and busts do, will end in tears.

Although countries like India and Indonesia have taken positive steps toward reducing their external imbalances, real reforms take time; and balance-of-payments episodes will recur until the core imbalances have been resolved.

A sudden rise in real interest rates abroad – which could arise purely from a miscue in FOMC forward guidance – could slam a long list of emerging markets simply by reducing the real risk premium over “safe” assets. Even a 200-basis-point move in US rates could create a strong incentive for less productive capital in compromised or overvalued markets to rush for the exits in headlong capital flight.

It may sound like an extreme case, but even a moderate rise in real interest rates abroad would be enough to trigger disorderly and destructive currency adjustments across the emerging world.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

A little over two months ago, I argued that Reserve Bank of India Governor Raghuram Rajan was stepping forward as the unofficial spokesman for an entire group of emerging-market central bankers struggling to manage what he calls “capital-flow-induced fragility.”

(I spent several days on a speaking tour with Rajan, and he is a very serious academic and critical thinker. As a central banker, he will be a force to be reckoned with. I wonder how often that marvelously sly sense of humor that I saw will be allowed to come out during the crisis that is brewing in India. I haven’t seen much of it in his last interviews and speeches. This is a man who understands the seriousness of his situation.)

Developed-market observers like to criticize emerging-market policymakers first for complaining about excessive capital inflows into their economies and then for throwing a “tantrum” when supposedly unwanted flows slow or start to reverse… but Rajan took that tendency to task in a January 30, 2014, interview with Bloomberg’s Vivek Law. (You can watch Governor Rajan’s January appeal to rich-world investors here. Even if you have already seen it several times, I encourage you to watch it again… and this time play close attention to his body language.)

In the real world, Rajan explained, FX volatility can be downright traumatic for emerging markets.

We complain when it goes out for the same reason when it goes in. It distorts our economies. And the money coming in made it more difficult for us to do the adjustment which would lead to sustainable growth and prepare for the money going out.

You see, the nostrum amongst economists here is "Let the prices adjust and things will be fine. Let the exchange rate move; let the money flow out; and you will figure it out. That is often a reasonable prescription for an economy that has its fundamentals, as well as its institutions, well-anchored. But when those aren't anchored, what happens is the volatility feeds on itself. Exchange rates fall. Stop loss limits are hit. More selling takes place. Then some firms get into difficulty because they have unhedged exposures. Government budgets get hit because they're not hedged against currency fluctuations. There are also second- and third-round effects which happen in a country which is not as advanced or industrialized.

This week Governor Rajan upped the ante by presenting an explosive and controversial paper at the Brookings Institution – literally right in front of former Fed Chairman Ben Bernanke – entitled, “Competitive Monetary Easing: Is it yesterday once more?” (Please note that this is the same Ben Bernanke who basically told emerging-market central banks that the US was not responsible for their problems, not all that long ago when he was chairman of the Fed. This was the central banker’s equivalent of saying, “Go pound sand!”)

In his paper and oral presentation, Rajan worries openly about the consequences for the rest of the world as advanced-economy interest rates start to normalize. His comments offer us critical insights into the coming climax and resolution of the global debt drama (emphasis mine).

Ultra accommodative monetary policy [in advanced economies] created enormously powerful incentive distortions whose consequences are typically understood only after the fact. The consequences of exit, however, are not just to be felt domestically, they could be experienced internationally.

Perhaps most vulnerable to the increased risk-taking in this integrated world are countries across the border. When monetary policy in large countries is unconventionally accommodative, capital flows into recipient countries tend to increase local leverage; this is not just due to the direct effect of cross-border banking flows, but also the indirect effect, as the appreciating exchange rate and rising asset prices, especially in real estate, make it seem that borrowers have more equity than they really have…

Recipient countries should adjust, of course, but credit and flows mask the magnitude and timing of needed adjustment. For instance, higher collections from property taxes on new houses, sales taxes on new sales, capital gains taxes on financial asset sales, and income taxes on a more prosperous financial sector may all suggest that a country’s fiscal house is in order, even while low risk premia on sovereign debt add to the sense of calm. At the same time, an appreciating nominal exchange rate may also keep down inflation. The difficulty of distinguishing the cyclical from the structural is exacerbated in some emerging markets where policy commitment is weaker, and the willingness to succumb to the siren calls of populist policy greater…

Ideally, recipient countries would wish for stable capital inflows, and not flows pushed in by unconventional policy…. But when source countries move to exit unconventional policies, some recipient countries are leveraged, imbalanced, and vulnerable to capital outflows.

Given that investment managers anticipate the consequences of the future policy path, even a measured pace of exit may cause severe market turbulence and collateral damage. Indeed the more transparent and well-communicated the exit is, the more certain the foreign investment managers may be of changed conditions, and the more rapid their exit from risky positions.

So, Rajan is clearly lining out a framework for understanding the QE-induced bubble boom and the balance of payments crises that could follow in overexposed countries.

Unconventional monetary policy pushes far more capital into emerging markets than would naturally flow there in a normalized rate environment, and the easy money tends to lull elected officials into inaction.

Following the classic balance-of-payments boom/bust cycle, capital overflows appear to boost growth for a while as leverage grows and policymakers have an increasingly difficult time distinguishing between cyclical and structural forces in the economic data – making it virtually impossible to intervene at the appropriate time. The bubble builds up until the “source country” decides to exit its unconventional policies, wrecking asset prices globally and damaging overexposed “recipient countries.”

The problem for emerging markets is that there are no conventional tools for blocking this kind of knock-out punch… except for much-reviled exchange rate interventions and capital controls.

Considering the available options, it is very clear that Rajan intends to do whatever it takes to defend the Indian rupee; but he would obviously like to avoid trade sanctions in the process. That’s why he argues so forcefully that emerging markets find themselves pushed up against a new kind of constraint equivalent to the zero bound.

Emerging economies have to work to reduce vulnerabilities in their economies, to get to the point where, like Australia, they can allow exchange rate flexibility to do much of the adjustment for them to capital inflows. But the needed institutions take time to develop. In the meantime, the difficulty for emerging markets in absorbing large amounts of capital quickly and in a stable way should be seen as a constraint, much like the zero lower bound, rather than something that can be altered quickly.

Expanding on that argument, Governor Rajan argues that there are essentially two kind of unconventional policy: “policies that hold rates at near zero for long” and “balance sheet policies such as quantitative easing or exchange intervention, that involve altering central bank balance sheets in order to affect certain market prices.”

In other words, Rajan is arguing that quantitative easing, which aims to lower real rates at the zero bound, is essentially identical to exchange-rate intervention, which aims to explicitly target an exchange rate to maintain or regain competiveness. And that “our attitudes towards [either approach] should be conditioned by the size of their spillover effects rather than by any innate legitimacy of either form of intervention.”

For better or worse, Governor Rajan is clearly broadcasting his intent to employ explicit exchange-rate intervention (probably some form of currency peg) or outright capital controls to protect the Indian rupee.

I think a lot of emerging-market central banks will follow suit, and harder currency pegs will follow. Otherwise, as Rajan says,

The lesson some emerging markets will take away from the recent episode of turmoil is (1) don’t expand domestic demand and run large deficits, (2) maintain a competitive exchange rate, and (3) build up large reserves, because when trouble comes, you are on your own.

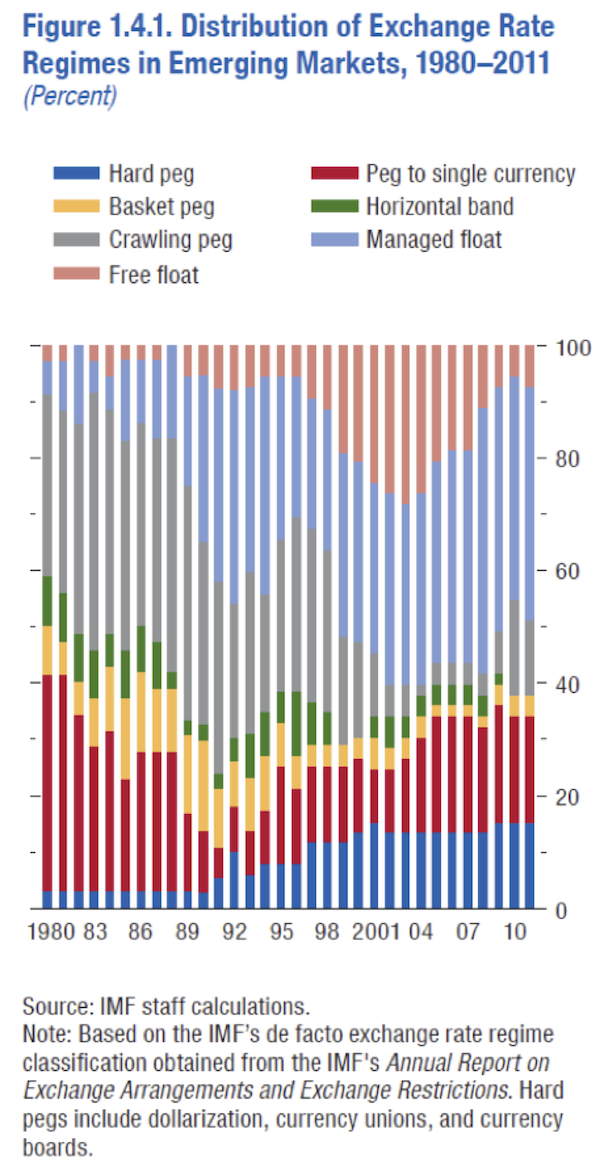

Notice in the chart below that the currency exchange-rate regimes for countries change all the time. I would expect that volatility to increase in the next few years as emerging markets respond to what is in effect a developed-market currency war, currently led by Japan, though I expect it to heat up everywhere within a few years.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

One of the significant differences I’ve noticed this time in South Africa is just how remarkably cheap (for the traveler) everything seems to be that has no, or very little, international component in its makeup – things like food and wine. The rand has depreciated significantly since I was last here; and while that is good for tourists, it is hard on the locals. I had more than a few South African financial industry participants tell me they wished they could come to our conference in San Diego but that the rand had fallen too much to make it affordable. I joked about how I feel the same about travel in Europe, but that was hollow consolation.

I spoke some eight times in four days here, plus media interviews, and at each of the venues there was a considerable question-and-answer period. The most difficult questions centered around how South Africa should respond to the actions of the developed-world central banks and especially the US Federal Reserve and what South Africa should do to improve its own current situation? These difficulties are compounded by the fact that a general election will be held here in less than a month. The ruling party, the African National Congress, is beset by serious charges of corruption and an economy that is clearly not hitting on all cylinders, yet it appears the ANC will still get at least 60% of the vote.

South Africans are quite passionate about their country and their desire to see it do better. They genuinely wanted to hear some answers from me, but that didn’t make coming up with them any easier.

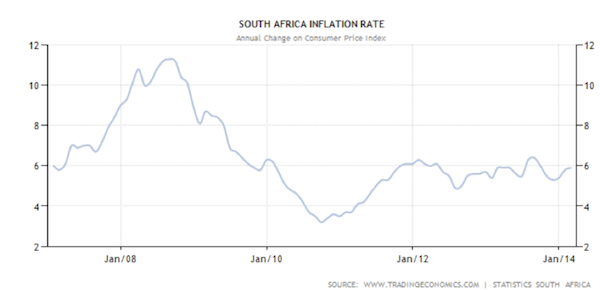

The problem is that there is not much South Africa can do about the policies of central banks other than their own. As I described above, it truly is every central bank for itself. But the South African central bank has local problems that compound its problems. Unemployment is roughly where it was 4-5 years ago, at 24%. Inflation is high and seemingly rising, and the rand is weakening (see chart below).

The South African inflation rate has been relatively stable the last few years at around 6%, after rising to almost 11% in late 2008 and dropping to well below 4% in late 2010.

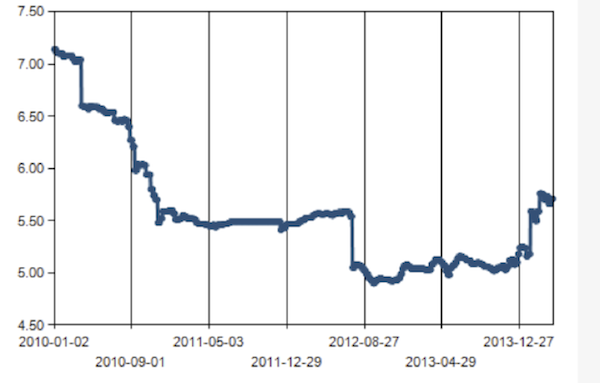

Treasury bill yields are somewhat lower than the current inflation rate, just as they are in much of the world. But clearly the central bank felt it needed to raise rates in a world where the rand was suffering.

From my friends at moneyweb.com, based here in South Africa:

Record low interest rates in the U.S., Europe, and Japan, along with the U.S. Federal Reserve’s multi-trillion dollar quantitative easing programs, caused $4 trillion of speculative “hot money” to flow into emerging market investments over the last several years. A global carry trade arose in which investors borrowed cheaply from the U.S. and Japan, invested the funds in high-yielding emerging market assets, and earned the interest rate differential or spread. Soaring demand for emerging market investments led to a bond bubble and ultra-low borrowing costs, which resulted in government-driven infrastructure booms, dangerously rapid credit growth, and property bubbles in countless developing nations across the globe.

The emerging markets bond bubble helped to push South Africa’s 10-year government bond yield down to a record low of 5.77 percent after the global financial crisis:

South Africa’s external debt now totals $136.6 billion or 38.2 percent of the country’s GDP – the highest level since the mid-1980s – due in large part to the emerging markets bond bubble that boosted foreign demand for the country’s bonds. South Africa’s external debt-to-GDP ratio was 25.1 percent just five years ago. $60.6 billion of South Africa’s external debt is denominated in foreign currencies, which exposes borrowers to the risk of rising debt burdens if the South African rand currency depreciates significantly, such as the currency’s 15 percent decline against the U.S. dollar in the past year. To make matters worse, over 150 percent worth of South Africa’s foreign exchange reserves are required to roll over its external debt that matures in 2014.

Unsecured loans, or consumer and small business loans that are not backed by assets, are the fastest growing segment of South Africa’s credit market and are essentially the country’s own version of subprime loans. Unsecured loans have grown at a 30 percent annual compounded rate since their introduction in 2007, when the National Credit Act was signed into law. Unsecured lending has become popular with banks because they are able to charge up to 31 annual interest rates, making these riskier loans far more profitable than mortgage and car loans in the low interest rate environment of the past half-decade. The unsecured credit bubble is estimated to have boosted South Africa’s GDP by 219 billion rand or U.S. $20.45 billion from 2009 to mid-2013.

Like U.S. subprime lenders from 2002 to 2006, South Africa’s unsecured lenders target working class borrowers who have limited financial literacy, which has contributed to the country’s growing household and personal debt problem. A 2012/2013 report from the National Credit Regulator showed that South Africa’s 20 million citizens carried an alarming 1.44 trillion rand or U.S. $140 billion worth of personal debt – equivalent to 36.4 percent of the GDP. In addition, household debt now accounts for three-quarters of South Africans’ disposable incomes.

What’s a central bank to do when faced with such a situation? There is very little else it can do other than try to mitigate the damage if there are significant currency outflows. The rest – the heavy lifting – will have to be done by the government. Which is somewhat problematical, given that the government under current president Zuma has essentially done very little for the last five years.

Seven years ago I wrote a very optimistic piece about South Africa called Out Of Africa. Many of the reasons for that optimism remain, including the basic spirit and willingness of South Africans to work and the significant financial-community expertise that is available.

But the similarities between then and now end there. Now the South African equity markets are rather fully valued. And the government, which I had hoped would cut through the red tape hindering business, has in fact added to it. Admittedly, there have been some positive changes, and an encouraging document outlining a decade-long economic plan has been developed, but there has been no implementation whatsoever.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The policy recommendations I outlined to Zuma in our meetings a number of years ago remain the same. The country must be structured for higher exports and the production that makes them possible. This will require significant labor reform or at least the introduction of commercial business loans with labor-law terms that will allow foreign direct investment to feel comfortable in coming to South Africa.

South Africa must realize that it’s competing with every other country in the world when it seeks foreign direct investment. And with regard to manufacturing for the African continent, while the scope of the competition might narrow to other countries in Africa, the competitive principle remains the same.

One of the remarkable things I notice as I travel around the world is the business acumen of the South African diaspora. South African expatriates always seem to be running businesses and conducting entrepreneurial activities. Their skills are highly sought after.

Those same entrepreneurial skills and desires are found in abundance in South Africa, and that, not gold or platinum or diamonds, is the greatest resource of this country. A restructuring of the rules surrounding the formation of businesses would unleash a South African renaissance in less time than you might think, given the predatory activities of major central bankers fighting currency wars.

Free-trade zones, a completely revamped education system that is freely available and teaches skills based upon needs of the future rather than upon academic training suited to the past, and a thorough cleansing of the climate of corruption in the country would also help. This last real problem requires the creation of institutions free from the manipulation of the ruling government that can tackle the problems of corruption. The rule of law must be upheld. Political corruption and crony capitalism must both be done away with, root and branch. (And that goes double for the United States!)

On a personal note, South Africa remains one of my very favorite countries to visit. I find the people friendly and engaging; the scenery varies from exotic to breathtakingly beautiful (Cape Town gets my vote for most beautiful city in the world); and the culture is most pleasant. I have high hopes for the country and hope to be invited back often. Perhaps after this upcoming election the leadership will find the courage to take on the entrenched powers and move the country forward.

Amsterdam, Brussels, Geneva, and San Diego

I will be flying back to Dallas via London in a few hours. It is a long trip, and I must admit that after 25 days on the road I will be glad to be home. I will try to limit travel for a little over two weeks before heading to Europe on another speaking tour. I will be in Amsterdam, then Brussels, and on to Geneva. Then I am back home for a few days before hopping over to San Diego for my Strategic Investment Conference, where you really should join me! And at some point in the next few weeks, I have to begin making plans to return to Italy for the first few weeks of June.

I think that rather than making my normal personal comments, I will just go ahead and hit the send button, as I need to shower and check out of the hotel and make my way to the airport. In addition to trying to work through my once-again massive backlog of emails, I think I will take the opportunity on this flight to round up a little science fiction on my iPad. After the last few weeks I need a little break. Have a great week. I look forward to your comments and thank you for taking the time to make me part of your life.

Your ready to relax and enjoy the plane ride analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.