Change Squared

-

John Mauldin

John Mauldin

- |

- March 4, 2022

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin“How did you go bankrupt? Two ways. Gradually, then suddenly.”

- Ernest Hemingway, The Sun Also Rises

Change usually comes slowly. But every now and then, events like Pearl Harbor, September 11th, and COVID-19 come out of nowhere and change everything.

We can look at those in hindsight (which is 20/20) and often see some clues were there. People just didn’t notice them. Change occurred gradually, then suddenly.

One of my recurring themes in recent years has been the accelerating pace of change, what I call “The Age of Transformation.” These world-changers used to come along only every decade or so. Now? You don’t have to look back far. It was just over two years ago we learned about a deadly virus that would, within weeks, reorganize daily life and entire economies in ways few could imagine, with profound consequences.

Now, with the COVID books still not closed, we have another world-changer. Vladimir Putin’s invasion of Ukraine really shouldn’t have surprised us. We saw his Crimea takeover in 2014. We knew his grand vision of a great empire, his desire for buffer zones around Russia. Maybe wishful thinking obscured reality. Regardless, it’s clear now. Everything changed again in the last week.

And the change is not just a war. The very fabric of globalization and the concept of property has changed.

Now, we have change on top of change. Call it “Change Squared,” with the already-giant COVID changes multiplied by a new geopolitical and global economic order unfolding before our eyes. There’s no going back from this. Whatever lies ahead will be profoundly different from what any of us know. Illusions have been shattered, assumptions exposed, paradigms exploded.

The near future will bring nothing but uncertainty. But in a way, that may be a good thing. It gives us a chance to change our mindsets. We need to let go of what we “know” and get ready for what is coming, whatever it may be.

Today we’ll start what I’m sure will be a series of letters on Change2. I’ve said for some time the 2020s would be a turbulent period leading to a much better 2030s. I still believe that. I also believe the events we’re watching right now will define what that new order will be.

We’ll begin with the most immediate consequences: the economic sanctions other countries are imposing on Russia. I believe they are a necessary response and certainly preferable to a military one. But they bring risks and unintended side effects that may cause problems, possibly soon.

Inflation Complications

Before all this erupted, inflation and the associated policy responses were our primary macroeconomic concerns. The Federal Reserve was (and still is) preparing to tighten financial conditions, hoping to dampen inflation without pushing the economy into inflation. (I keep thinking of the old comedy line, “Slowly I turned, step by step, inch by…”) Many of us were skeptical they could engineer such a “soft landing.”

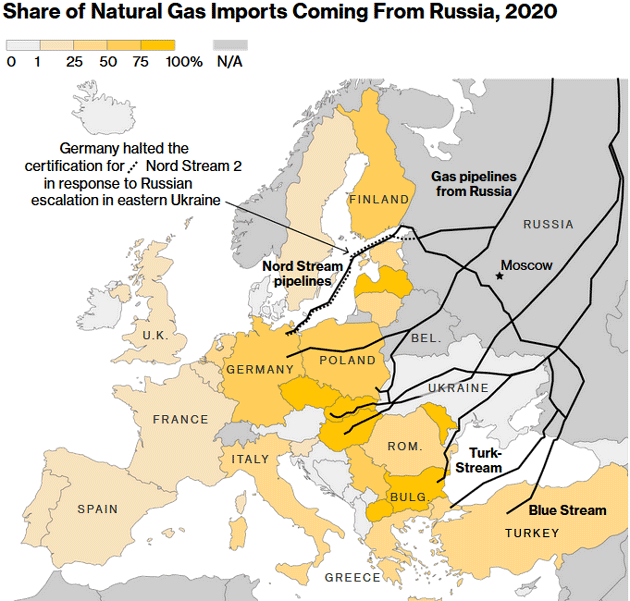

This picture is now a lot murkier. One of the world’s top oil exporters, and Europe’s top natural gas supplier, has created substantial doubt it can/will continue exporting at current volumes. This is already showing in energy prices, even though the flows are just starting to be interrupted. Energy is a not-insignificant contributor to the inflation the Fed seeks to fight, so higher prices don’t help. And they could go higher still.

Europe is highly dependent on Russia for natural gas, which, despite dreams of converting to all-renewable energy, is still economically critical. And not just for power generation—gas is important for manufacturing and agriculture (i.e., fertilizer production) as well.

Source: Bloomberg

This vulnerability may be one reason Putin didn’t expect the resistance European leaders are showing. But the vulnerability goes both ways: Russia needs the hard currency it gets from energy exports. That trade has been carved out of the sanctions imposed so far. Whether it will remain that way is anyone’s guess.

If circumstances interrupt these flows, what can Europe do? It could fill some of the shortfall with liquified natural gas from the US and the Middle East. But there’s not a great deal of surplus on the market, nor is it easy to ramp up production quickly.

It’s also not clear the energy industry wants to produce more. They’re tired of getting burned in the boom-bust cycle. Just this week, Chevron CEO Mike Wirth told shareholders the company is sticking with previous modest production increases. Of course, the industry could change its plans and certainly will if prices get high enough and stay there. But that’s unlikely to make a difference to this year’s inflation.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The sanctions greatly complicate the Fed’s next steps. Higher energy prices make inflation worse, adding to their task, but may also reduce economic activity (which is already weakening) and make the Fed overshoot. Meanwhile, increased global demand for US dollars is pushing real Treasury yields even lower, which, if it persists, means the Fed will have to raise nominal rates even more to achieve the same effect.

The risk of a Fed policy error was already high. Now it’s considerably higher, complicated even further by the fact that no one knows what’s next—in either the territorial war or the economic war. The Fed has to find a very narrow path between tightening too much and not enough. I’m not at all confident they can do it.

Neon Signs

The war also aggravates another preexisting problem: snarled supply chains and shipping delays. I was frankly amazed by the speed and unanimity with which countries slapped all kinds of sanctions on Russia. Necessary? Yes, but the side effects are already showing. In this connected world economy, interruptions anywhere quickly become interruptions everywhere.

We already see it in energy. The sanctions on Russia excluded energy shipments and the related transactions. As it’s turning out, that doesn’t matter. Tanker lines are either raising their rates to move oil and gas out of Russia or declining completely. That’s a rational business choice, given the risk of further sanctions or of having your ship impounded. Plus, the insurers, banks, and others who facilitate shipping have to comply with the sanctions. It will take some time as countries draw down reserves and cargos already in transit reach their destinations, but shortages seem inevitable.

Nor is it just energy. The major container shipping lines are also pulling out of Russia, which will affect Western exporters. Russia brings in large amounts of manufactured goods. That’s all stopping. An IKEA store opened in Moscow to great fanfare. Russian consumers could get modern goods like anywhere else. Except that store is now shut down. Apple Pay and credit cards no longer work.

President Biden keeps saying the sanctions are designed to not hurt American businesses. I’m sure the administration is doing what it can, but there’s just no way to order such massive, open-ended interventions and not cause collateral damage.

At the same time, some of this is outside US control. A small example: Ukraine produces about 70% of the world’s neon gas exports. While neon signs are now mostly antiques, it is a crucial component in semiconductor production. That kind of neon gas has to be refined to ultra-high purity. Two-thirds of it comes from a single factory in Odesa, Ukraine. Furthermore, the kind of ships that can carry that gas aren’t super common and could become even less so if someone gets trigger-happy in the Black Sea.

If those neon shipments should stop, analysts say global chipmakers probably have about eight weeks’ supply on hand. Then what? The industry is just now starting to recover from COVID-driven disruptions, which in turn affected production at a long list of downstream companies, especially automakers.

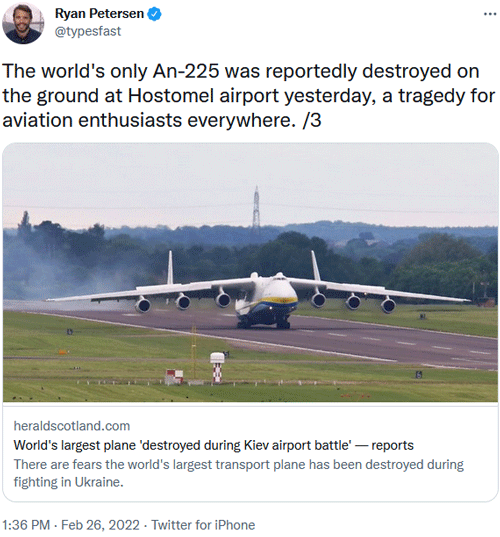

There’s more. Suppose you have some large object to transport by air—bigger than a 747 can carry. Heavy industrial users do it all the time, using giant Antonov cargo jets which are made in Ukraine. The largest, the An-225—a one-of-a-kind monster—was destroyed at Hostomel airport outside Kyiv during a recent attack. The company’s fleet of somewhat less-giant An-124 planes mostly survived, but they depend on Ukrainian facilities for maintenance and spare parts. So those planes are unavailable or will be soon.

Source: Ryan Petersen

Are there a lot of these giant objects to move? No, but they’re important. The inability to deliver one of them can shut down an entire multi-billion-dollar project, killing thousands of jobs.

And here’s the most disturbing part: The path forward is unknown. Ending the war might not end the sanctions. The sanctions could even get tighter. The permutations are endless, and that makes international business planning highly risky, if not impossible.

Closer to home, I suspect within weeks, we’ll start noticing even more shortages, seemingly random but often connected to this war. Long before then, we’ll be paying higher prices for fuel and all kinds of petroleum-derived products. Then those prices will start feeding through to other things.

The more I think about this, the more it starts to resemble the 1970s OPEC oil embargo and the associated conflicts and instability. We know what harm that did to a far less globalized economy. We also know how the Fed (eventually and belatedly) responded. If you don’t remember that time, I can assure you, it wasn’t fun.

But wait, there’s more.

|

From Our Partners: Turn your 401k into Real. Physical. Gold. "Inflation proof" your retirement with the timeless power of gold. It's easy and secure. Tax-free or tax-deferred. |

Plumbing Problems

Earlier this week, I saw a journalist on Twitter noting it’s never a good sign when he has to write about financial system plumbing—things like counterparty risk, debt covenants, and the like. It’s a good analogy. Plumbing (the kind with water in it) is something we use every day with no second thought. It’s there, it works, it makes life better… until it doesn’t. Then life quickly gets uncomfortable.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

In the grand scheme of things, Russia is a relatively small economy—comparable to Italy (smaller than Texas). But its key position as a top energy supplier makes the country more important than its size would imply. The economic sanctions will affect Russia but also others. And there, it gets tricky because we really don’t know where all the connections are.

For example, suppose you are a European bank with loans to Russians. Will you get your next loan payment? How? And if you don’t get it, then what? Keep in mind banks are highly leveraged even in normal circumstances. Even a few bad loans can put them on shaky ground. We may not know if it’s a problem until the loans get a few months behind. But if this drags on, write-downs are inevitable.

That’s really the small-potatoes part, though. The US and others have done something almost no one anticipated by freezing Russia’s central bank reserves. Some $300 billion is on deposit in Western institutions. Russia is now unable to access it, which is why the ruble is collapsing.

The resulting instability in a highly leveraged complex system will have negative effects. For one, now no one knows who they can trust. Your counterparty may look like it has a fortress-like balance sheet. But if some of it falls in the sanctions’ crosshairs, it could evaporate overnight. Trading institutions will handle this by demanding more and better collateral. Where will the collateral come from? It all gets messy very fast.

This new knowledge that a central bank’s reserves are subject to freeze will give leaders a good reason not to hold their reserves too far from home. China was already moving on a number of fronts to build alternatives to the dollar-based financial system. Xi will no doubt accelerate those plans now.

We don’t know where all this will lead, and that’s really the problem. It’s all coming out of nowhere, with decisions made hastily and without due regard to the inevitable side effects.

The New World Disorder

For decades, I have dismissed projections of the dollar’s end as the world’s reserve currency. I have to confess: today, I’m less sanguine. I don’t think it will happen within a few years but over a decade? I hinted at it above, but the massive changes from the sanctions are far more profound than “merely” disrupting the Russian economy.

Every country in the world now realizes its reserves and assets in foreign banks are subject to seizure if they don’t play “by the rules.” I’m not arguing that’s bad; I am suggesting it’s new. It is basic multiplayer game theory (John Nash’s A Beautiful Mind): When you change the rules of the game, the players change how they play the game.

Now the rules say that your assets can be seized. Even if you have no intention of ever breaking the rules, you would be foolish not to notice that the rules have changed, especially if you are China. China in particular—and many other countries in general—will try to do more business in their own currency rather than go from currency A to US dollars to currency B.

In the short term, that’s going to be difficult. Over the long term? Large countries like India or Indonesia that do a lot of local trade? Not every export or import, but certainly some.

I think we will slowly move from having a dominant reserve currency to a somewhat dominant reserve currency and many alternatives. That means less demand for the dollar, which will weaken the dollar, which won’t help in the battle against inflation.

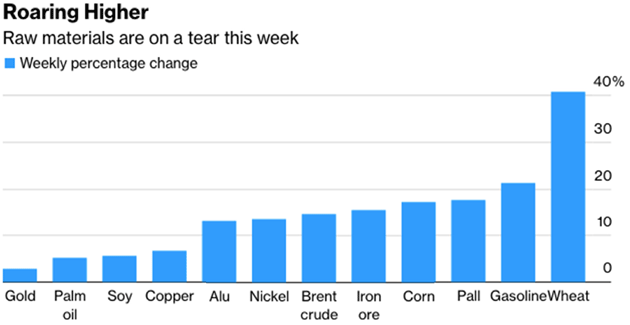

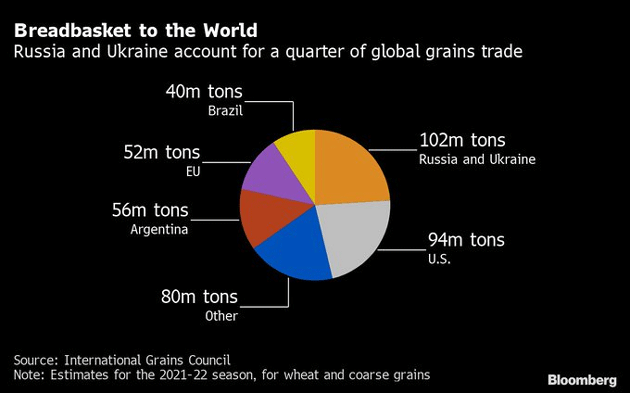

Further, the supply chain risks for critical goods like food and energy are going to change the way we trade. An Estonian ship was sunk in the Black Sea. Doesn’t matter what caused it. Try and get insurance on a ship going into the Black Sea, with up to 25% of some agricultural products like wheat coming from Ukraine and Russia. Corn has to be planted in Ukraine in the next 30 to 60 days. You want to bet it will happen? Egypt gets up to 80% of its wheat from Ukraine. Wheat is up 40% this week. Wheat futures have been “limit up” for four days. We don’t know what the price will settle at, except it will be the highest ever. See charts below.

Source: Bloomberg

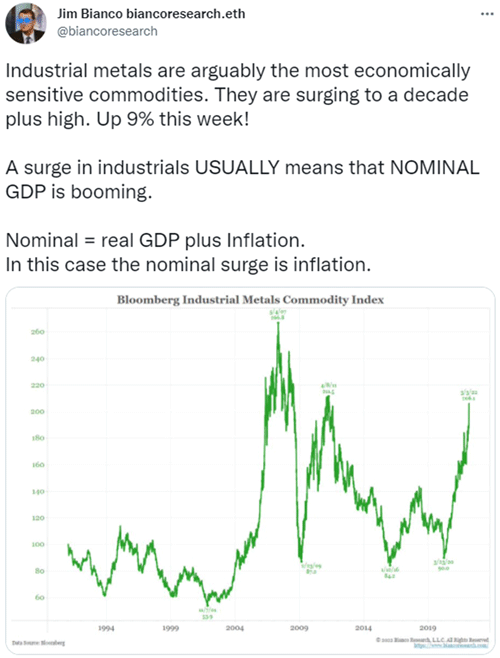

It’s not just agricultural commodities. Industrial metals of all types are rising significantly. Here is a tweet from my friend Jim Bianco.

Source: Jim Bianco

This week has shown us that governments will weaponize the financial system to achieve their purposes. In this case, it is a good purpose, and when we have to rationalize debt (what I call “The Great Reset”), it will be just as necessary because otherwise, the entire system will collapse. I think we have seen a clear demonstration of what “unthinkable” might be.

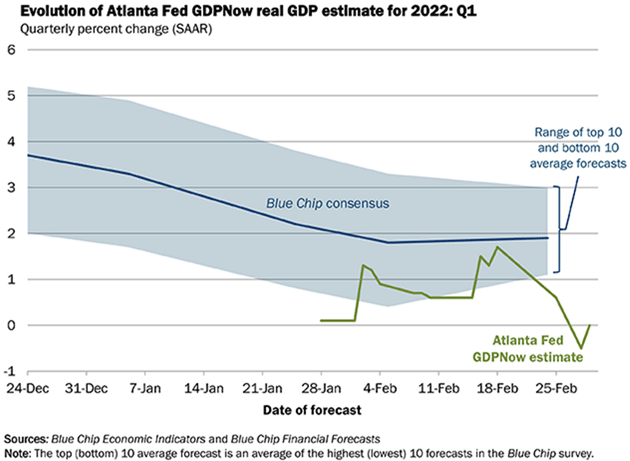

The US Economy Is Slowing Down

The Atlanta Fed’s real GDP model for the first quarter now shows 0% growth.

The yield curve is flattening. The difference between 2-year and 10-year yields is now less than 0.3 percentage points. Yields are essentially already flat at the long end of the curve. The Fed is going to tighten into a slowing economy, notwithstanding Friday’s monster employment number.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We will go into this in another letter, but I think inflation will be harder to bring down than seemingly anyone at the Fed now believes. At best, inflation will still be over 3% at yearend. I won’t be surprised to see 4% because of the screwy way we figure housing inflation. The Fed is going to be under massive pressure. I don’t think they or anyone else knows what they will do. It spells even more market volatility.

Laying Siege to a City

A final note. It seems the Russian strategy is to lay siege to a city, pretty much destroy it, and then set up a military government without really destroying the Ukrainian resistance. Now I am not a military strategist, but it seems to me if you have taken a city and are now surrounded by angry people who are receiving weapons from abroad and can disrupt your supply chains, I’m not certain that’s a good strategy. I guess we will see over the next few weeks and months. But the tragedy and destruction in Ukraine are heartbreaking and totally mind numbing.

My best geopolitical sources say there’s really no “offramp” in this situation, just more escalation. I am told that our Defense Department and State Department take the threat of nuclear weapons seriously. That doesn’t help me sleep well at night.

RIP, Dr. Gary North

Long-time readers and friends know I got my start in the investment industry as the marketing partner with Dr. Gary North at the American Bureau of Economic Research back in 1981. I stayed with him until the late 80s. He introduced me to Austrian economics, and I became friends with scores of other writers.

Sadly, Gary succumbed to a prolonged battle with prostate cancer last week. While we disagreed on many fundamental things, we maintained our friendship over the years, with him often making comments on my writing, pro and con, but always lively.

Many years ago, Gary (along with Mark Skousen) took me to the Austrian Alps, where we spent three hours with Friedrich Hayek at the end of his life, interviewing him on the beginnings of the Austrian movement in Vienna. Fascinating. There are just so many Gary North stories.

I learned so much from him, but what I really learned was how to write. Gary wrote over 50 books, literally typing with one finger, and was one of the greatest storytellers I have ever met. Knowing him was a master class on how to write, how to make your words flow, and help your readers learn.

Rest in peace.

It is time to hit the send button. It has been a tumultuous week. I am sure that many of you are glued to Twitter and news feeds, trying to understand how this all plays out. That has made me more active on Twitter, where I hope you will follow me. Have a great week!

Your thinking about how things will change analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.