2015 Five-Year Global Financial Forecast | Mauldin Economics

-

John Mauldin

John Mauldin

- |

- January 12, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinSeven Significant Events for the Next Five Years

Sayonara or Pour Me Some More Sake

Europe: A Ticking Time Bomb

China Enters a 12-Step Program for Debtaholics

Cincinnati, the Cayman Islands, Zurich, and Florida

Seven major trends are likely to produce an economic tsunami over the next five years, wreaking havoc but delivering opportunities to the savvy investor.

It is the time of the year for forecasts; but rather than do an annual forecast, which is as much a guessing game as anything else (and I am bad at guessing games), I’m going to do a five-year forecast to take us to the end of the decade, which I think may be useful for longer-term investors. We will focus on events and trends that I think have a high probability, and I’ll state what I think the probabilities are for my forecasts to actually happen. While I could provide several dozen items, I think there are seven major trends that are going to sweep over the globe and that as an investor you need to have on your radar screen. You will need to approach these trends with caution, but they will also provide significant opportunities.

There is a book in here somewhere, but I do not intend to write one today. In fact, my New Year’s resolution is to write shorter letters in 2015. Over the last decade and a half, the letter has tended to get longer. A little more here, a little more there, and pretty soon it just gets to be a bit too much to read in one sitting. That means I need to either be more concise, break up my topics into two sessions or, if further writing is necessary, post the additional work on the website for those interested.

So I’m writing today’s letter in that spirit. Each of the major topics we’ll be covering will show up in other letters over the next few months. I would appreciate your feedback and any links to articles and/or data points that you think I should know about regarding these topics.

But first, this is generally the most downloaded letter of the year. I want to invite new readers to become one of my 1 million closest friends by simply entering your email address here. You can follow my work throughout the year, absolutely free (and see how my prognostications are turning out). And if you’re a regular reader, why not send this to a few of your friends and suggest they join you? At the very least, Thoughts from the Frontline should make for some interesting conversations this year. Thanks. Now let’s get on with the forecasting.

Seven Significant Changes for the Next Five Years

Let’s look at what I think are six inexorable trends or waves that will each have a major impact in its own right but that when taken together will amount to a tsunami of change for the global economy.

1. Japan will continue its experiment with the most radical quantitative easing attempted by a major country in the history of the world… and the experiment is getting dangerous. The Bank of Japan is effectively exporting the island nation’s deflation to its trade competitors like Germany, China, and South Korea and inviting a currency war that could shake the world. I’ve been saying this for years now, but the story took a nasty turn on Halloween Day, when the Bank of Japan announced it was greatly expanding and changing the mix of its asset purchases. The results have been downright scary, and a major slide in the JPY/USD exchange rate is almost certain over the next five years. I give it a 90% probability. All this while the population of Japan shrinks before our very eyes.

2. Europe is headed for a crisis at least as severe as the Grexit scare was in 2012 – and for the resulting run-up in interest rates and a sovereign debt scare in the peripheral countries. After all these years of struggle, the structural flaws in the EMU’s design remain; and now major economies like Italy and France are headed for trouble. In the very near future we will finally know the answer to the question, “Is the euro a currency or an experiment?” The changes required to answer that question will be wrenching and horrifically expensive. There are no good answers, only difficult choices about who pays how much and to whom. Again, I see the deepening of the Eurozone crisis as a 90% probability.

3. China is approaching its day of reckoning as it tries to reduce its dependency on debt in its bid for growth, while creating a consumer society. The world is simply not prepared for China to experience an outright “hard landing” or recession, but I think there is a 70% probability that it will do so within the next five years. And the probability that China will suffer either a hard landing OR a long period of Japanese-style stagnation (in the event that the Chinese government is forced to absorb nonperforming loans to prevent a debt crisis) is over 95%. To be sure, it is still quite possible that the Chinese economy will be significantly larger in 2025 (ten years from now) than it is today, but realizing that potential largely depends on President Xi Jinping’s ability to accomplish an extremely difficult task: deleveraging the debt overhang that threatens the country’s MASSIVE financial system while rebalancing the national economy to a more sustainable growth model (either through either a vast expansion of China’s export market or the rapid development of “new economy” sectors like technology, services, and consumption; or both). This will not be the end of China, which I’m quite bullish on over the very long term, but such transitions are never easy. Even given this rather stark forecast, it is still likely (in my opinion) that the Chinese economy will be 20 to 25% bigger as 2020 opens than it is today; and every other major economy in the world (including the US) would be thrilled to have such growth. At the very least, though, China’s slowdown and rebalancing is going to put pressure on commodity exporters, which are generally emerging markets plus Australia, Canada, and Norway.

4. All of the above will tend to be bullish for the dollar, which will make dollar-denominated debt in emerging-market countries more difficult to pay back. And given the amount of debt that has been created in the last few years, it is likely that we’ll see a series of crises in emerging-market countries, along with an uncomfortably high level of risk of setting off an LTCM-style global financial shock. My colleague Worth Wray spoke about this new era of volatile FX flows and growing risk of capital flight from emerging markets at my Strategic Investor Conference last May, and he has continued to remind us of those risks in recent months (“A Scary Story for Emerging Markets” and “Why the World Needs the US Economy to Struggle”). Now that Russia has tumbled into a full-fledged currency crisis with serious signs of contagion, Worth’s prediction is already playing out, and I would assign an 80 to 90% probability that it will continue to do so, as a function of (1) the rising US dollar and a reversal in cross-border capital flows, (2) falling commodity prices, or (3) both. This massive wave is going to create a lot of opportunities for courageous investors who are ready to surf when countries are cheap.

5. I do not believe that the secular bear market in the United States that I began to describe in 1999 has ended. Secular bull markets simply do not begin from valuations like those we have today. Either we began a secular bull market in 2009, or we have one more major correction in front of us. Obviously, I think it is the latter. It has been some time since I’ve discussed the difference between secular bull and bear markets and cyclical bull and bear markets, and I will briefly touch on the topic today and go into much more detail in later letters. For US-focused investors, this is of major importance. The secular bear is not something to be scared of but simply something to be played. It also offers a great deal of opportunity. If I am right, then the next major leg down will bring on the end of the secular bear and the beginning of a very long-term secular bull. We will all get to be geniuses in the 2020s and perhaps even before the last half of this decade runs out. Won’t that be fun? Let’s call the end of the secular bear a 90% probability in five years and move on.

6. Finally, the voters of the United States are going to have to make a decision about the direction they want to take the country. We can either opt for growth, which will mean a new tax and regulatory regime, or we can double down on the current direction and become Europe and Japan. I’ve traveled to both Europe and Japan, and they’re both pleasant-enough places to live, but I wouldn’t want to be a citizen of either Japan or the Eurozone for the rest of this decade. (I particularly love Italy, but it is beginning to resemble a basket case, with last year’s optimistic drive for reforms seemingly stalled.)

However, I would rather live and work and invest in a high-growth country, with opportunities all around me, a country where we reduce income inequality by increasing wealth and opportunities at the lower end of the income scale instead of trying to legislate parity by increasing taxes and imposing government-mandated wealth redistribution, which slows growth and squelches opportunity for everyone.

A restructuring of the US tax and regulatory regime does not mean a capitulation to the wealthy, big banks, or big business. Properly conceived and constructed, it will allow the renewal of the middle class and result in higher income for all. Sadly, it is not clear to me that either the Republican or Democratic parties are up to the task of making the difficult political decisions necessary. They each have constituencies that tend to opt for the status quo. But I see hope on both sides of the political spectrum that change is possible. The course they set will give us an idea where we will want to focus our portfolios in the decade of the ’20s. It is a 100% probability that we will have to make a decision. It is less than 50% that we will make the right one – or at least the one that I think is the right one.

7. We have entered the Age of Transformation. We’re going to see the development of new technologies that will simply astound us – from increasingly capable robots and other applications of AI to huge breakthroughs in biotechnology. The winners are going to be those who identified the truly transformational technologies early on in their development and invested wisely. While riskier (potentially far riskier) than most of your investments should be, a basket of new-technology stocks should be considered for the growth part of your portfolio. I see the Age of Transformation as a 100% probability.

Just for the record, I also see a continuation of the global deflationary environment and a slowing of the velocity of money until we have some type of resolution concerning sovereign debt. Central banks will continue to try to solve the “crises” I mentioned above with monetary policy, but monetary policy will simply not be enough to stem the tide. Central banks can paddle as hard as they like into the waves of change, but they cannot reverse their powerful flow.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Now, let’s look further at each of the waves that are forming into a potential tsunami.

Sayonara or Pour Me Some More Sake

Some four or five years ago I started saying that Japan is a bug in search of a windshield. Let’s see if I can summarize the problems and opportunities in a few paragraphs. Essentially, Japan began its lost decades (in 1990) with 30% government debt-to-GDP and is now at 250% (or thereabouts), and the number keeps growing. Well over 90% of government debt is owned by the Japanese themselves, and that number too keeps rising. Nominal GDP is roughly where it was 25 years ago. Growth has been nonexistent. Their massive Keynesian experiment has been a failure, at least as regards its the ability to create growth.

Without getting into the weeds of the actual numbers (which we will do in subsequent letters), the Bank of Japan is currently purchasing the majority of all new Japanese debt that is traded; and some days it is the market in 10-year bonds: no one else does any buying or selling. Japanese pension funds are now rotating out their massive overexposure to Japanese bonds and into Japanese as well as international stocks. We are talking huge cash flows, which is particularly bullish for equities in the developed markets as well as Japan.

If interest rates were to rise by a mere 2%, it would take anywhere from 80 to 100% of all Japanese tax revenues simply to pay the interest on the Godzillaesque Japanese debt. This is not a working business model, as the Japanese are running roughly a 5 to 7% deficit this year, even as interest rates fall due to BOJ purchases. The Japanese government simply cannot allow interest rates to rise, or it would face an economic catastrophe of the first order. Therefore my simplistic conclusion is that it won’t. But since the only way you can control interest rates and a rapidly growing bond market is to ensure adequate purchases and demand, and since the only real demand in the country is from the Bank of Japan, the BoJ will continue its radical experiment in quantitative easing. We are talking about a level that is two to three times (in relative terms) the magnitude of recent quantitative easing of the United States. And that is today. I think there is better than a 50% probability that the Japanese will be forced to increase that level of QE, as inflation will prove to be a mirage they chase for the rest of the decade.

They are going to continue monetizing their debt until enough Japanese government debt is on the books of the Bank of Japan that they can afford to allow interest rates to rise. That will be when they get their fiscal deficit under control and are actually running a surplus that could handle a rise in the remaining debt in the public market. Right now their plan is to have a balanced budget by 2020. Any time a politician tells you that the plan is to balance the budget in six years, what he’s really saying is, “I don’t want to take any more heat than I’m already taking today.” In Abe’s defense, he did raise taxes last year, which caused an immediate recession; but he went ahead with the taxes, although he has postponed the next increase until 2017. But QE, Japanese-style, will not end until the Japanese have their budget under control and can allow interest rates to rise. Point: they might stop QE short-term for the purposes of screwing around with the currency markets, but they will be forced to resume.

One of the basic rules of markets is that you can control the quantity of something or the price of something but not both. The Japanese are increasing the quantity of money in the markets, and therefore the value of that money is dropping. The Japanese yen is already down 50% from its highs of just a few years ago. Some would point out that Japan has not disappeared, so why is this a bad thing?

If you are a Japanese consumer, you have seen your disposable income fall as your food and energy costs have risen. Which is why there has not been an explosion of consumer spending or any appreciable inflation so far, though both were part and parcel of the plan of Abenomics. Japan desperately needs to see nominal GDP growth in the 3% to 4% range, but it is nowhere close. Since the deficit is higher than 3% to 4% and will likely to remain so for the next few years, total government debt-to-GDP is rising every year. Wrong direction.

While the Japanese government can occasionally back-slap the currency markets with the odd policy correction, long-term they have no choice but to continue to monetize the debt. Not to do so would be to accept a deflationary collapse, something that I think everyone pretty much agrees must be avoided. The time for Japan to make good choices was 15 to 20 years ago, when they should have avoided increasing their debt toward the level where they find it today. Today they have no good choices. They simply have a choice between Disaster A and Disaster B. They have chosen Disaster B, which is to devalue their currency. If I were in their shoes, I would make the same choice. Home team rules and all that.

How low will the yen go? I have said 200 to the dollar, but in reality that is just a guess based on my back-of-the-napkin calculation of how much I think they will need to monetize. I have some very smart friends who think 140 is probably the final number. I have other very smart friends who think 300 is the final number, because they think the government of Japan will lose control over the markets. The reality is that none of us know, as this experiment has never before been tried in the history of the world.

Will Japanese consumers (read voters) accept ¥200 to the dollar over the next 10 years? We will see, but I honestly see no choice for them. If I were Japanese, I would be buying gold and assets not denominated in yen and getting my money into the dollar or other foreign currencies. I will touch on this in later letters, but there is so much opportunity here. Japan provided my single biggest personal source of returns in 2014. Go Abe and Kuroda.

The euro is not a currency; it is an experiment. It will not be a currency until France has a true crisis in which the European Union has to decide whether to keep the euro and create a fiscal union or to dissolve into competing currency environments that will allow for adjustments among different countries. Either path will be horrifically expensive. Quite simply, the monetary policies that are suitable for what I call the FANG countries (Finland, Austria, the Netherlands, and Germany) are not the same as those needed by the peripheral countries. I am tempted to make some pun about the FANG countries having Europe by the throat, but I will resist (at least for now).

There is a growing recognition in Europe that they need some sort of quantitative easing, but this is opposed tooth and nail by the FANG countries. Mario Draghi has promised for several years to do “whatever it takes,” but the markets are beginning to believe that he is long on rhetoric and short on the wherewithal to pull it off. The European Central Bank (ECB) is controlled by a complex voting system. You have the five larger countries sharing four votes (on a rotating basis), the other 12 countries sharing seven votes (again on a rotating basis), and six appointed board members who are, as best I can determine, parceled among various countries, but the usual suspects seem to have secured permanent board positions.

If it came down to a vote, Signor Draghi could probably win; but he would not have a consensus, and the ECB is nothing if not a consensus-driven machine. This lack of unanimity is a problem, as a number of ECB voting members are essentially no more than city states. Luxembourg, Malta, and Cyprus are all marvelous places, but they each have fewer than one million citizens. Five other countries in the euro currency area have fewer than ten million (and several just two million). I am hard-pressed to believe that Germany would feel comfortable with the idea that countries that have less population than a decent-sized German state or even a city should have a controlling say in monetary policy.

If Draghi cannot bring the Germans along on some type of quantitative easing program, he will lose all credibility in the markets. I can’t see him hanging around for very long if he fails. Every day he stayed after that critical juncture would further damage his chances of doing anything else going forward. I think it is more likely he would leave and take the job as Italian president and try to solve the mess Italy is in. That might be easier, but only marginally.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

If Draghi gets his way on QE (I would take the “over” on this bet), the euro is then likely to weaken, and the crisis may be postponed for a few years. If he doesn’t, it is entirely possible that the euro will strengthen even as the Eurozone economy weakens, and that interest rates in countries with outsized government debt and economic problems will see their interest rates begin to rise. Now throw into the mix the Greek election on Jan. 25, which is likely to give control of the government to a party that wants to significantly devalue (or completely do away with) the Greek debt, and you heighten volatility. The simple fact of the matter is that the Greeks have 175% debt-to-GDP; and as I said four years ago when the problem was said to be “solved,” the Eurozone’s bailout of Greece merely kicked the can down the road to the day when the Greeks would end up defaulting on even more debt. It now seems we have come to the end of that particular road. The Germans and the French say that if the Greeks don’t want to pay they can leave the euro. The Greeks rightly point out that physically, mathematically, they can’t pay – but they don’t want to leave the euro. Try and figure this one out. It’s not an economic decision; it’s a political decision. Predicting what politicians will do, especially in Europe, is particularly problematic.

I want to thank Paul Krugman for calling to everyone’s attention in his recent New York Times column my contention that France will be every bit the problem that Greece is. Of course, he said that in the context of pointing out that France is now borrowing long-term money at 0.8% and that (at least so far) I have been wrong. “Where is the French time bomb?” he asks. My reply is that it is still there, ticking away quietly in the background. If you have a neo-Keynesian ear, you can’t hear it. I hope he will be equally diligent in drawing attention to the outcome of my call in four or five years. Actually, I hope that I am wrong about France. The world will be better off if I am: France matters.

Sidebar: Paul (may I call you Paul?), you also called me an inflationista. I truly must object. If anything, I am a deflationista, since I have banged my deflation drum for well over a decade and a half. I was aggressively recommending long US bonds in the ’90s. I actually agree with you that those who thought QE in the US would cause hyperinflation and the demise of the dollar were missing the point. I have produced numerous columns explaining all that. It still doesn’t mean the latest QE was a good idea or accomplished anything useful over the long term.

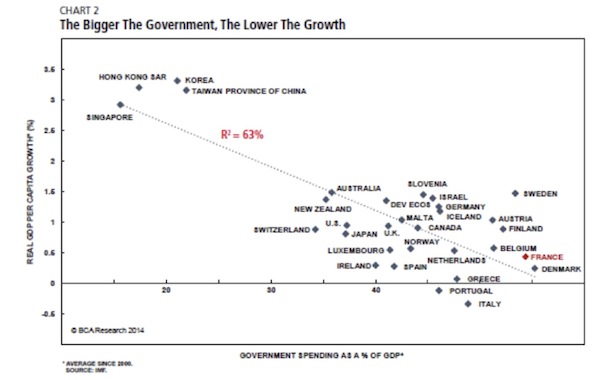

You might have arrived at the inflationista label because I am a debtophobe – I see many of the world’s ills as caused by too much debt, held by governments that are too large relative to the size of their economies. A graphic depiction of my concern can be seen in the following chart, from a recent Bank Credit Analyst report, which shows that the larger government spending is as a percentage of GDP, the lower growth is per capita. Japan grows more slowly than Europe, which grows more slowly than the US; and it seems to me there is a direct relationship to the amount of debt in the system. To pretend that too-high levels of government debt do not affect growth is simply not mathematically reasonable. Thus my concern.

While Spain, Italy, and the other peripheral countries all have growth concerns, I think the linchpin to the entire eurosystem is France. In the chart above, we find France in the lower right. France is ranked 62nd globally in terms of competitiveness, some ways behind Albania. The reforms being proposed in France are simply tinkering around the margins. The absolute best the country can hope for this year is about 1% GDP growth, but it seems more likely that it will slip back into a triple-dip recession. Without a credible ECB quantitative easing program to help keep interest rates low, when French interest rates begin to rise, they may do so slowly at first; and then they may do so all at once. Then France will indeed look like Greece. Will Germany then finally allow a QE program to shore up their most necessary partner in the European Union? Can they do so without requiring some kind of fiscal union? This all suggests to me a period of great volatility and slow growth.

The French dilemma is further exacerbated by the growing strength of Marine Le Pen and her National Front Party. Under the guise of “economic patriotism” (whatever the hell that is), they are openly protectionist and believe “protectionism makes the state stronger.” They believe in large government. If Marine Le Pen is the answer, France is asking the wrong question. But given the recent tragic events in Paris, it is the answer they may get. Note this paragraph from a recent Telegraph column:

[Marine Le Pen] objects to all forms of globalisation, including free trade and immigration, and has toned down the fascist rhetoric, making her party more palatable to disillusioned centrists. The regional elections in March will give us an early clue to any shift in opinion. What is certain is that unless the mainstream political establishment finds a way of regaining the initiative on law and order as well as the economy, it is no longer inconceivable – though still unlikely – that she could one day win an election. This would be catastrophic, not just for the business community and for investors, but also for everybody else in France, in Europe and around the world.

(I am as saddened and outraged as anyone about the Paris bombings. My deepest sympathies to all the family members and to the country. The Muslim world needs to be party to a serious conversation about what it means to be part of a global civilization. To that end, I was encouraged by a recent speech by Egyptian President Abdel Fattah Al Sisi at Al-Azhar University in Cairo, the very heart of Islamic learning (excerpted here – subscription needed), in which he forcefully called into question the acceptance of violence and terror by Muslim clerics. We need to see more of this from politicians and clerics in the Muslim world. Quite simply, the Western world does not understand the apparent condoning of beheadings, kidnapping of teenage girls, rape, and killing of those who do not “believe correctly” – violence supposedly perpetrated in the name of their religion. Where are the fatwas against terrorism? I am sure that Al Sisi took such a stand at some risk, as have others. I read in Time magazine a most thoughtful response to the Charlie Hebdo shootings by Kareem Abdul-Jabbar (yes, the same gentleman who scored the most points in NBA history), and I commend it to you.)

Given that the potential crisis in Europe is controlled by political decisions in Germany, there is no real way to develop a timeline, but I sincerely doubt that the next Eurozone crisis can be postponed for five years. We will go into more details in future letters.

China Enters a 12-Step Program for Debtaholics

China’s massive GDP growth has been fueled by equally gargantuan growth in debt. Much of that debt is not on the official books, but when you look at all of the debt guarantees the government has in place, it is easy to come to a reckoning which suggests that Chinese government debt-to-GDP in China is already well above 200% and could be considerably higher. Given the nature of their socialist market economy, something that has no true analog in Western economic history, and the fact that official Chinese data are simply made-up numbers, we are left to our own devices in trying to figure out what is really happening.

To the credit of the Chinese leadership, they recognize the problem. They are attempting to do something that no country (to my knowledge) has done before, and that is to let the air out of their debt bubble in a controlled manner before it bursts, while simultaneously rebalancing the national economy toward a more sustainable growth path (which dramatically increases the chances of the bubble’s bursting). When the true nature and magnitude of China’s dilemma is properly understood, it is quite easy for Homo economicus occidentalis to predict disaster. However, Western economists would also have said what China has done over the last three decades wasn’t possible to do the way they have done it, so perhaps we should refrain from saying that what they’re attempting to do now is impossible.

What I will say is that I don’t think it is likely that they can transition from a debt-fueled economy to a consumer-driven one without suffering a serious slowdown at minimum. The odds are clearly in favor of a sharp, hard landing or else a Japanese-style stagnation in the coming years – but miracles are always possible.

Whether or not the official data will ever acknowledge the severity of China’s adjustment is beside the point. Even if Xi Jinping and the State Council manage to guide the economy through to a successful rebalancing without an economic collapse, it’s still likely that China will shake the world. Chinese purchases of a variety of commodities are going to decline and in some cases collapse outright, as commodity-intensive “old China” sectors such as infrastructure, real estate, and mining give way to commodity-light “new China” sectors like technology, services, and consumption. Despite the fact that this slowdown is already in progress, most commodity-exporting countries and businesses are still not prepared for such an eventuality.

It would be nice if Prime Minister Modi could get the bureaucracy of India under control in short order and India could take over as the commodity-buying growth engine of the world, but that is simply not realistic. While Modi may eventually succeed, it is not going to be an overnight process. Thus we are left to assume that there is going to be a significant adjustment in world growth.

China is a mystery to most investors, but it is central to an understanding of the global economy. My colleague Worth Wray and I are wrapping up an anthology on China, with contributions from some of the true experts on China from around the world. Our plan is to publish the book electronically on Amazon, iTunes, and Barnes & Noble for a relatively low price. Hopefully it will be out in February.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

If I’m going to keep my New Year’s resolution, I need to close here. We will take up the remaining components of our tsunami next week, and maybe even dip our toes into a more typical annual forecast, or at least those elements of one that I have some clue about.

Cincinnati, the Cayman Islands, Zurich, and Florida

I see Cincinnati, Grand Cayman, Zurich, and Florida on my schedule. I will be in Cincinnati on the 13th for the CFA forecasting dinner. Then in February it’s on to the Caymans. It has been awhile since I was in the Cayman Islands, and this time I’ll take a short hop over to Little Cayman to visit my friend Raoul Pal for a few days. A brilliant macroeconomist and trader, Raoul has now based himself in Little Cayman, although he frequently flies to visit clients. He is also a partner with Grant Williams in Real Vision Television, a fascinating new take on internet investment TV. In March I’ll be in Zurich (and maybe some other parts of Europe) and then hop the pond back to Orlando. I know I have to get to NYC as well in that period.

I should note that my friend Jack Rivkin has been on a roll in his economic and political blog. Jack is a deep thinker of enormous breadth and is one of the most thought-provoking investment professionals I know. I always look forward to spending time with him. He recently did his own list of potential economic surprises, called “What to Expect in 2015 and Beyond.” It’s designed to get you thinking about the risks and opportunities in 2015 from a different perspective and to give you a peek at some potential tail risks. It’s not long, and you’ll find it well worth your time.

After my final look-through, I really must give myself a C in keeping this letter shorter. I hope I am more successful with my other New Year’s resolutions, which involve losing that last bit of fat and reading more books. I would also say that I want to travel less, but my travel schedule seems to be subject to the tyranny of business demands and not to my personal whims.

I also intend to add this year to my culinary repertoire. I have never been able to make a decent piecrust. In fact, my efforts can only be described as boring and pasty. I was recently invited to what turned out to be a long, pleasant dinner at the home of Dr. Peter Raphael, a local celebrity surgeon; and as it turns out, master chef is his true calling. He created an exquisite brie cheese appetizer with multiple layers of filo dough and other delightful fillings. I think the same process, though very time-consuming and perhaps needing a surgeon’s hands, would create the ultimate pie crust. I’m also open to any old family recipes that may be in your possession. Man cannot live by economics alone.

It’s time to hit the send button. I truly hope that together we can make 2015 the best year ever. There are lots of changes coming at Mauldin Economics that I hope will make a difference for the better in your life.

Your more excited than ever about the future analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.