A Big Swirling Italian Mess

-

John Mauldin

John Mauldin

- |

- December 2, 2016

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinExtend & Pretend, Italian-Style

An Ungovernable Mess

Strange Brew

It’s Not Just Italy

Washington DC, New York, Atlanta, and Florida

“Move to Italy. They know about living in debt: They don’t care.”

– John Lydon

“Italians were eating with a knife and fork when the French were still eating each other.”

– Mario Batali

Italians are headed to the polls this Sunday (and thus this letter is reaching you a little earlier than usual) – but no one is quite sure what is on the ballot. On the surface, the voters are considering whether to approve constitutional reforms that should make the government operate more effectively (or not, depending on your point of view). But many people think the real question is whether the current government should stay in power and whether Italy should remain yoked to the Eurozone.

Coming up with an answer isn’t necessarily helpful when you can’t even agree on the question. However Italians vote, it may take some time to figure out exactly what the result means to Italy, the Eurozone, the EU, and the global economy. I am fairly confident that the ultimate outcome won’t be good, no matter what they choose. The problems are deeper than simple structural reform can cure.

Before we wade into the weeds on this topic, please understand, I love Italy. I love the culture, the people, the food, the beautiful art and architecture, and the heritage the country has bestowed on all of Western civilization. Some of the best moments of my life happened in Italy. I wish nothing but joy to the country and all its people. But politically and economically, Italy is an ungovernable mess heading straight for a Greek-style banking and debt crisis – but with an Italian flare.

Viewed from a historical perspective, this prospect shouldn’t surprise anyone. The territory we now call Italy was a shifting collection of smaller city-states for centuries. They came together as a Republic only after World War II, so they still have some issues to sort out. Creating a stable banking system is high on the list. But Italy can’t have that until it has a stable political system, which has been elusive: Italy has had 65 different governments in the postwar era. They last just over a year, on average.

As I’ve said several times in this election year, I try not to write about politics, since this newsletter is about economics and investing. Unfortunately, drawing a sharp line between them grows harder every day. And in Italy it is impossible. The economy and markets increasingly depend on electoral politics, geopolitics, and politically charged policy decisions. That’s just a fact of life now, one I suspect Italians will have to accept for many years to come.

Now, it’s true that economic forces usually prevail over politicians in the long run. How long is that? I’d say a generation – twenty years or more. But political forces are very important if we’re trying to forecast the next twelve months or the next five years. Ignoring them is not an option.

It’s not just Italy, either. Political, economic, and social changes are afoot almost everywhere in the world. As an investor, what are you to do when all of these inputs are crash-landing on your portfolio?

A couple of years back, we here at Mauldin Economics saw this serious period of change coming. That’s why I started VIP, a bundle of our best publications wrapped up in one neat, heavily discounted bow. It covers all the bases and is designed to help your portfolio survive and thrive in these trying times. It’s available now until December 13.

Extend & Pretend, Italian-Style

I’ll cut to my conclusion: There is a high degree of probability (approaching 90%, I’d say) that Italy will experience a severe banking crisis in the next few quarters. Perhaps they can stave off the problem for a year, but something will have to be done about the banks. We’ll go into that later in the letter, since the plight of the banking system is the root cause of all the country’s other problems. Without a banking crisis, Italy would still be the political mess it has been for 65 years, but the banking mess turns the political mess into an economic mess.

There is a significant chance Italy will decide to leave the Eurozone and/or the European Union in the next year or so. Is it likely? No, but we’ve seen less likely things happen recently. Just the discussion of the possibility could be destabilizing to markets that already have enough worries.

If we are lucky, Italy will decide quickly what to do and then do it in a planned, orderly fashion. That would, however, go against everything we know about Italy from experience.

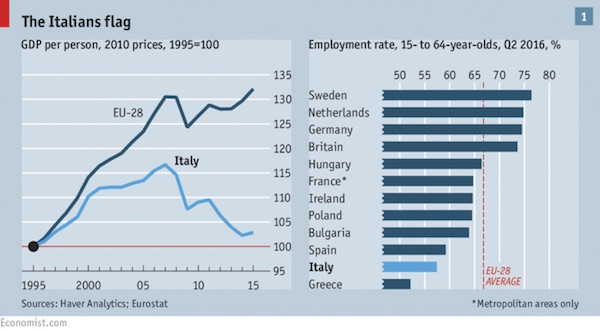

Italian citizens haven’t had much fun the past decade, judging from their GDP. You can see in the left side of the chart below that GDP per person has lagged the EU since 1995. Worse, it kept falling after 2009 even as Italy’s neighbors recovered.

This performance stands in stark contrast to Italy’s pre-euro experience. Even though Italy constantly revalued the lira, that revaluation process allowed Italy to grow its GDP in real terms as fast as Germany did for decades. Notice in the graph above that the real dropoff in Italian economic performance began shortly after the introduction of the euro in 1999.

Italy was one of the economic miracles of the ’60s and ’70s. The northern part of Italy was a production powerhouse. The region was strong in the design and manufacturing of all manner of products across a whole host of industries. Even banking was strong. You need to know that Italy is the eighth-largest economy in the world and has issued the third-largest amount of sovereign bonds. This is not a minor country we are talking about. And that mountain of sovereign bonds is really the avalanche-in-waiting that an Italian banking crisis will send tumbling down on the rest of the world, because a large percentage of those bonds are outside of Italy, sitting on the books of banks and central banks.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The bar chart on the right above shows the employment rate for people ages 15–64 in various European countries. Italy is second worst on the list, with only Greece having fewer working-age jobholders. That tells you all you need to know about why there is political turmoil and pushback from Italian voters.

Note, incidentally, which countries are on top of the pile: Sweden, the Netherlands, Germany, and the UK. The geo-economic split in Europe isn’t imaginary. The northern tier is in better shape than the southern by almost any measure. France and Ireland are the north’s employment laggards, but they are still far better off than Spain, Italy, and Greece.

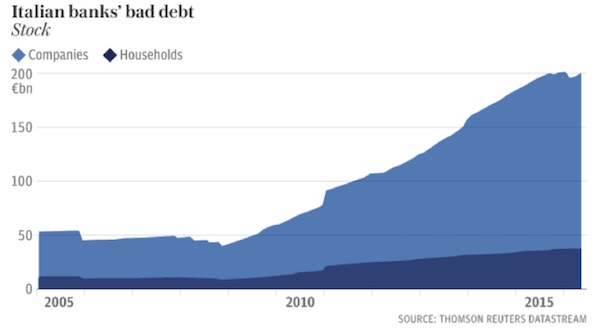

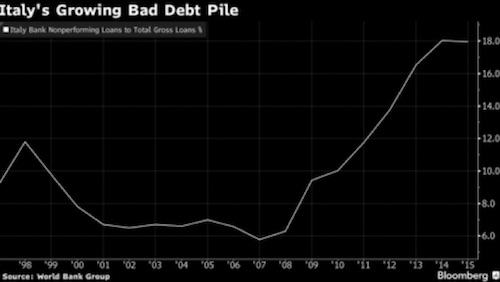

Eighteen percent of the total loans made by Italian banks are now considered to be nonperforming. Nonperforming loans occur everywhere, of course, but not to this level. On an aggregated basis, the Italian banking system has less than 50% of the capital it would require to cover the bad debts. Estimates are that Italian banks may need €40 billion just to remain solvent. The banking situation gets even worse, as we will see.

Italy is problematic for many of the same reasons that Greece, Spain, and Portugal are. Bank customers in these southern-tier Eurozone states borrowed to buy goods from the wealthier north, mainly from Germany; and then the economic growth they anticipated failed to occur. The purchased goods have mostly been consumed, so there is no collateral to recover. Many loans look like near-total losses.

To adapt an old saying: If you owe the bank a million dollars, the bank owns you. If you owe the bank $100 million, you own the bank. Writing off a massive loan as a loss will render the bank insolvent, so instead it goes into “extend and pretend” mode, allowing endless payment delays on the flimsiest premises, hoping against hope that you will win the lottery and resume paying your loan. That’s what is happening in Italy and indeed throughout Europe. It happened in the US during our housing crisis. The chart below shows Italy’s pile of nonperforming loans in terms of its percentage of GDP. To put the bad debt in context for US readers, our banks would have to have nonperforming loans of $3.8 trillion to be this badly off. That total would dwarf any problems from the 2008 subprime crisis. (But wait, there’s more.)

Eventually, even the bank has to admit that its delinquent borrowers aren’t going to mend their ways and become creditworthy. Then what? Where do you find the needed bank capital? You go looking for a bailout. That is the current situation in Italy. The country’s largest banks need fresh capital. Where to get it?

Banca Monte dei Paschi di Siena, the world’s oldest bank, one of Italy’s largest, and possibly its most troubled, is trying to raise €5 billion in new capital with a three-part plan: convert subordinated bonds to equity, sell new equity via private placement to institutions, and promote a new public equity offering. None of the three is going well. You know a bank is in trouble when its stock drops 84% in less than a year and still no one sees a bargain.

Unicredit, which is even larger than Monte dei Paschi, intends to raise €13 billion early next year. Prospects for success range from slim to none. Time is running out, too, as depositors pull out their money and decline to deposit more. And we haven’t even talked about the multiple lawsuits facing these banks, for which they have set aside only a fraction of the potential judgments.

Some of those judgments will arise from an unsavory practice engaged in by certain banks that have sold bank-issued bonds to customers who thought they were depositing money into a bank account. Now the bonds have lost value and may lose even more, potentially 100%, if EU rules prevail and Italy has to bail-in bondholders before using public funds for a bailout.

This is not just a problem with Monte dei Paschi. There is roughly €240 billion of this type of bank debt scattered around Italy. Bank customers looking for yield were told that this was a safe way to get it. You trusted your local bank, right? Except now these loyal customers are first in line to lose all of their investment if their bank hits the wall. And that’s just what most of them are in danger of doing. I’ll have more to say on the practicality of taking what amounts to 12% of GDP from mom-and-pop customers. The equivalent in the US would be $2.2 trillion. Think about average middle-class Americans losing 2.2 trillion dollars, and then think about what kind of political pushback there would be. We’ll get to that pushback thing in a moment…

All these issues are part and parcel of Italy’s political dysfunction. Economic weakness flows out of a sclerotic, multi-layered government that finds it very easy to spend money and very hard to do anything else. The result is a bureaucracy that stifles commerce and massive government debt that retards economic growth. Weak, chaotic governance is a prime reason Italy has such high unemployment. Bailing out the banks will add to the debt – but the alternatives to saving them may be even worse.

Italy’s debt problem is not recent. When the Italians joined the euro they were able to enjoy low interest rates at both the national and personal level, so they ran up their debts. The problem is that the country can no longer devalue its way out of the problem. It is running a massive, and I mean truly massive, trade deficit with Germany and the rest of Europe.

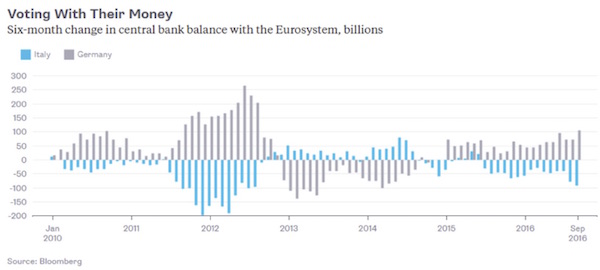

And bank deposits and capital are simply flying out of Italy as we speak. We measure this by something called TARGET2 balances. Essentially, Italy’s TARGET2 balance is the money leaving Italy and going to other countries within the euro system. I should note that the chart below depicts the latest data but does not include the whisper numbers we are hearing that would make the chart look even worse. Remember, the US elections and the other political upsets have happened since the ECB published this chart in September. And the euro is falling out of bed.

What’s an Italian investor to do? Think about it. You’re worried about the banking system; you think there is likely to be a failed referendum; and you don’t know what will happen. You move your money to Germany:

So what is this weekend’s referendum supposedly about? Matteo Renzi, the prime minister, seeks to overhaul Italy’s political system with constitutional reforms. Presently, the national government has a bicameral parliament. Unlike in other countries, Italy’s two chambers are co-equal, and very little can happen unless they agree – which is apparently rare. This setup lets the bureaucracy run wild.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Renzi’s reform plan would reduce the senate from 315 elected members to 95 who would be chosen by regional assemblies and mayors, and five more senators who would be appointed by the president. The senate would lose most of its ability to block bills. The plan would also pull back certain powers the national government had given to some regions. The current system practically guarantees that no serious reforms can be passed, and Renzi is gambling his political future on changing that system.

When I was last in Italy, Renzi had been in power for just a few months. I and a friend met with their central bank and some of the politicians in Renzi’s leadership. They were all absolutely convinced that Renzi would be able to reform Italy. These were true believers.

Renzi correctly concluded that without the reforms Italy would be ungovernable, so he called for the referendum at what he thought was a propitious time – but then postponed it to the point where it now looks as though success may have slipped out of reach.

Separately, Renzi already pushed through another set of electoral reforms called the Italicum. It is complex, but the important feature of it is that it will enable a party that gets less than a majority of votes, and possibly a lot less, to get bonus seats in parliament and end up with firm control. Party leaders will have tremendous power under this system. Note that this measure was pushed through with the consent of both of the leading center-right and center-left parties in an effort to make sure that the growing minority parties couldn’t band together and form a government. Oops. It is now no longer certain that one of those “minority” parties (like the Five-Star Movement) wouldn’t be the leading vote getter. Certainly, such a party wouldn’t win a majority of votes, but it might succeed in fracturing the Italian political system even further.

Renzi worked his way up from the bottom of this ungovernable political heap to the top. He rose quickly in the party leadership, was elected mayor of Florence, and was appointed (not elected) prime minister in 2014, at the tender age of 39. To me, he appears intent on either making his mark on the government very quickly or just leaving government completely. He has staked his reputation on the reform bill by promising to resign if voters don’t approve it.

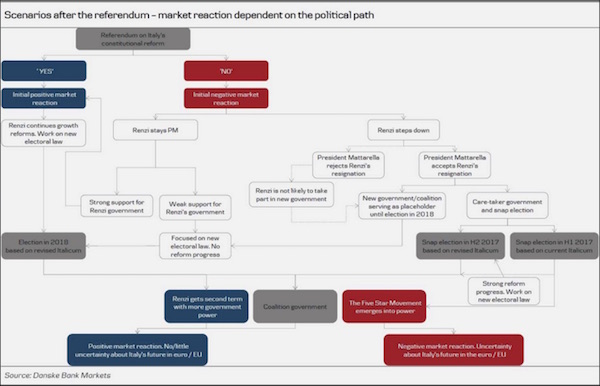

I’m not sure whether it was planned this way or Renzi made a mistake, but opposition parties have framed the reform vote as a vote on Renzi’s leadership. Renzi himself turned it into a tool others can use to remove him from power. It may well turn out that way, but the possibilities are myriad. This flow chart from Danskebank outlines the possible paths (larger version here).

The red boxes represent possibilities markets would likely see as negative. If the reforms fail, Renzi may or may not keep his promise to resign; the president may or may not accept his resignation; and new elections may or may not immediately follow. But elections are likely by 2018 at latest. The danger, at least as some perceive it, is that the populist Five Star Movement could take power after all this shakes out.

A spaghetti-like flowchart that took into account the reality of the banking crisis would make the above chart look appealingly simple. That’s because the choices that will be forced upon whoever is governing Italy will actually be much more difficult than this seemingly Byzantine flowchart indicates.

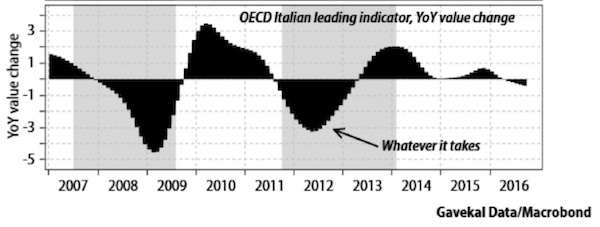

Let’s get to those choices. Italy has a €1.9 trillion GDP. The country’s debt-to-GDP ratio is already 136% and rising, since the economy is shrinking as the debt is rising. And it is very possible that Italy is slipping back into recession. This chart from Gavekal shows that the leading indicators for Italy are once again in negative territory.

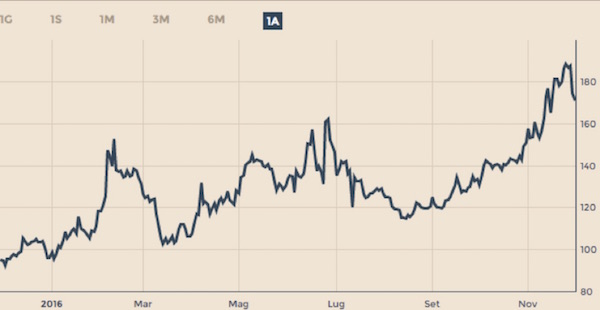

The year-over-year yield spread of the Italian 10-year bond versus the German 10-year has turned negative for the first time in five years. But even worse for Italy, Italian 10-year bond yields have hit a recent high and threaten to climb even higher:

The entire Italian system is being propped up by the European Central Bank’s (ECB) buying of Italy’s bonds as part of its overall quantitative easing project. There is a significant revolt involving many members of the ECB who want to scale back if not all together halt the QE program. That would remove the prop from Italian bonds, and their yields would soar back to the 6 to 7% range.

French and German banks that own Italian bonds are already down tens of billions of euros on the interest-rate move since September. Removal of QE support would be devastating to banks that are already under pressure. Germany’s banks own €83 billion worth of Italian bonds.

Italy is going to have to find at least €40 billion of private capital to refund its banks. Getting approval for that program through the dysfunctional Italian system is going to be a problem. That means the banks will probably need an ECB bailout. And by the way, that €40 billion is chump change compared to the €240 billion of Italian bank bonds that have been sold and that would be at risk. Now we’re beginning to talk about real money. A bailout might add another 15% of debt onto Italy’s already mountainous accumulation. Further, while €40 billion might fix the problem as it stands today, one thing we know about nonperforming loans in times of crisis is that they typically don’t perform any better as time passes. So while a bailout could “fix” the problem today, it could also come right back and bite them again a few years from now. (Think Greece.)

Further, if Italy were to approach the ECB for €40 billion to stabilize its funds, it would essentially have to apply to the European Stability Mechanism in the same process that Greece went through, subjecting the nation to all kinds of controls and tax increases, etc., from Brussels. I just don’t see the Italians, after having watched Greece go down, agreeing to anything like that. Renzi might be able to look Merkel and the rest of Europe in the eye and simply tell the Italian central bank to fund the debt and to get the money from the ECB and dare the ECB not to write the check. That would be the end of the euro project, and everybody knows it.

But could another Italian government led by a renegade populist get away with such a thing? Another story entirely…

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Enter the Five-Star Movement, which is a strange brew. Americans may want to think of it as an alliance between Donald Trump and Bernie Sanders voters. It is anti-immigration, anti-bank, pro-labor, environmentalist, and unfriendly to foreign alliances like the Eurozone and European Union. Its leader is former comedian Beppo Grillo, who cannot himself serve in parliament due to some legal difficulties he encountered decades ago, but who has tremendous influence nonetheless. Five-Star has said that it will hold a referendum on the euro and the EU if it comes to power, though it would be a nonbinding referendum unless they could somehow change the Italian constitution.

I think that looking at the Five-Star Movement in the context of our old left-right political thinking is to miss the point. The Movement is more about the Unprotected versus the Protected, more about those who have been left out as their incomes have been hollowed out over the last 15 years and their lifestyles negatively impacted. There is a growing frustration with Italy’s “elitist” leaders. Every minor politician, many even at the local level, gets a personal chauffeured car. I remember writing once that there were tens of thousands of such cars and chauffeurs.

The Trump victory here boosted stock prices, much to the relief of many; but it also drove interest rates higher and bond prices lower. Would a Trump-Sanders unity ticket (I know, just try to imagine it) have had the same effect? I don’t think so. It would have driven stocks down along with bonds, because it would deliver both higher spending and higher taxes.

Something even worse would happen to Italy under Five Star control. No more of Renzi’s gentle coaxing to get around EU and ECB bailout rules. Italy would ignore the rules, raise taxes to bail out the banks, and then leave the Eurozone and restore the lira as the national currency.

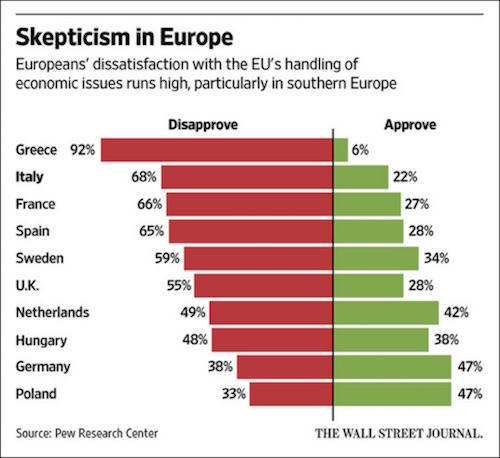

None of this would be easy or painless for Italians, of course; but I’m not sure that would stop them. It has not escaped their notice that waving the fiscal white flag didn’t seem to earn Greece any support from the EU’s top management. Greece gave up a great deal of sovereignty and feels it got little debt help in return. That’s how you get poll results like this:

As you can see from the above chart, big majorities disapprove of EU economic policies in much of Europe, but Greece is by far the unhappiest with Brussels. Italy is next, with France and Spain not far behind. The UK, where people are angry enough to have voted themselves out of the EU, looks even-tempered in comparison. That suggests to me that if you offered these other countries a chance to ditch the EU and reassured them that they wouldn’t cause the sky to fall, there are some that might take the leap.

Recall a couple of years ago, when Greece was in focus. Many of us said the EU might succeed at intimidating tiny Greece, but that Italy was a much bigger, more aggressive fish to fry. I’ve long thought this day would come. I speculated about it in a book I wrote five years ago. Now that day is here, though not in the precise form I expected. (It never quite works out that way.) The revolt against the elites has gained momentum shockingly fast. As recently as April of this year, Renzi (and those around him with whom I talked) apparently thought he could push through a reform program without much difficulty. And he may yet prove right… But polls taken two weeks ago suggest rather formidable opposition. (Note that Italy does not allow polls to be made public less than two weeks prior to an election.) The whisper numbers don’t seem to be suggesting a positive outcome for referendum, either.

After the vote is when it gets interesting. Whether the vote is yes or no, and whether or not Renzi decides to leave if it’s no, the problems remain. Just for the record, if I were Renzi and I got a no vote, I would do as I promised and depart – not because it’s important that he keep his promise, but because Italy will be ungovernable. It would be better for him not to be blamed for the ensuing crisis, so that he could possibly return to power at some point to have another try at fixing Italy’s troubles.

The EU has other problems, too. This weekend also features the rerun of Austria’s presidential election. It pits Green Alternative Party candidate Alexander Van der Bellen against Norbert Hofer of the far-right Freedom Party. Hofer is a fervent EU skeptic and immigration restrictionist. At 45, he is also much younger than the 72-year-old Van der Bellen. The two already faced off once this year. Hofer narrowly lost but was successful in getting the courts to look into the election process. They found significant evidence of fraud and ordered new elections.

The original election was rather interesting in that the major parties were all beaten by the Freedom Party and Green Alternative Party, but no party picked up a majority. So there was a runoff. Hofer was considered such a radical that every other party supported the Greens and were evidently quite willing to stuff ballot boxes in order to ensure a win. Shades of Chicago. And even then, Hofer lost by only about 1/10 of a percent. We’ll see how it goes this time. The original election took place before the UK’s Brexit vote or Trump’s nomination and subsequent election, so I have to think Austria’s populist right will be more energized this time. Hofer is not promising to hold a referendum on the euro or to leave the EU, but he definitely does not support Austria’s current EU status.

Speaking of immigration, events in Turkey play a part in all this political turmoil, too. Recall that Turkey and the EU had a deal by which the EU would consider Turkey’s membership in exchange for Turkey’s stopping the flow of Mideast refugees into Europe. That was before the July coup attempt against Turkish President Recep Erdogan. His mass arrests and media crackdown make it very hard for the EU to even consider Turkish membership now. Erdogan is again threatening to open the refugee faucet. That threat will likely help rightwing populist movements gain more support across the EU.

This weekend will give us some key information. I do not expect to wake up Monday morning and find that the EU has broken apart. But if Renzi’s referendum fails and Hofer wins in Austria, it will be safe to say that 2017 will be a pivotal year for Europe. The UK will keep moving along the Brexit path; Marine Le Pen will have a real shot at taking power in France; and Italy’s government could fall into Five Star’s control. Angela Merkel will be up for re-election in Germany and will likely win, but she could be forced into concessions we haven’t seen her make in the past.

As the late-night commercials used to say, “But wait, there’s more!” As all this is going on, Europe will be glancing nervously both east and west. To the east, Vladimir Putin will be looking for ways to stay in power as energy prices remain soft. To the west, President Trump will be pushing NATO members to boost defense spending – unless they want the US to fold up its umbrella. And most of those countries have zero room in their budgets for defense if they want to maintain spending levels on social welfare programs. Italy spends less than 1% on defense, and many other countries spend much less. Germany spends only a bit over 1%. (Just for the record, Canada is a member of NATO, and it spends exactly 1%.)

NATO membership only partially overlaps with the EU. One big difference: Turkey is a key NATO ally but only a wannabe EU member. That’s going to mean some delicate negotiations between Ankara, Brussels, and other European capitals.

The investment consequences of all this are very much up in the air. The worst-case scenario is a Eurozone breakup and the collapse of the EU free-trade area. Or both could shrink as Italy and perhaps others leave.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

As I think about Italy, one point nags at me. Trends all over the globe point away from centralized power. We don’t see much in the way of new economic or military alliances among nations. The trend is the opposite, as we see in the UK vote to exit the EU, Trump wanting tough negotiations on trade, and the Trans-Pacific Partnership falling apart. We also see regions within nations trying to claw back authority from their national governments.

What Renzi wants to do in Italy runs counter to this trend. He wants to make Italy’s national government stronger – and arguably with good reason. But he’s swimming against the current, and that suggests he may not make it. Even if he does win the reform package, implementation will be tough as opponents fight him every step of the way. The Five Star Movement will not go away if the referendum succeeds. They’ll still be there and could find other paths to power.

The conclusion I keep coming back to is this: Borders are back in style. We spent the last few decades dismantling them, making them permeable or inapplicable to various categories of people and goods. I think we may look back and see 2016 as the year in which those trends reversed. Nations are again raising border defenses against both immigrants and trade.

Tearing down the borders took decades, of course. They won’t all go back up right away. Some borders will be more open than others. Nonetheless, I think we are in the early stages of the formation of a different world power structure. How it differs will make a difference to your investments.

Today’s globalized corporations see borders and governments as inconveniences, distractions they can avoid simply by going somewhere else. I’m not sure that strategy will work much longer. If it begins to fail them, we will have to completely rethink valuations in many different markets.

Note well that all of the above is true even if no one launches overt trade wars, as Trump has threatened against China. Tariffs have almost disappeared as a factor, anyway. I don’t see them coming back.

Washington DC, New York, Atlanta, and Florida

Next week I will make my way to Washington DC and New York for a series of meetings and a special Friends of Fermentation celebration with Art Cashin and the group, and then I’ll steam on down to Atlanta for a Galectin Therapeutics board meeting. After the Galectin meeting I'll be home for the holidays, and then I’ll be at the Inside ETFs Conference in Hollywood, Florida, January 22–25. If you are in the industry and coming to that conference, make a point to meet with me. I will be making some big announcements at the conference. Then I'll be at the Orlando Money Show February 8–11 at the Omni in Orlando. Registration is free.

The last several letters have elicited more responses from readers than any other letters in my last 17 years of writing Thoughts from the Frontline. I've made a point to read every one of them – the pleasant and the not so pleasant to read. One of the things that happens when you write an investment and economics letter is that you get readers from all political persuasions. That has become abundantly clear to me the last few weeks!

The conversations I've had over the years and especially recently have helped to keep me centered, and I certainly appreciate your feedback. The quality of my readers is never more apparent than in their responses and comments to my letters.

Christmas approaches, and some of my kids were over, putting up the tree and decorating it. I will admit that I like to see them do it and appreciate their efforts. I don't particularly like to do all the Christmas preparations myself, so it’s good that several of my kids actually really enjoy putting up a tree and decorating the house. It didn't hurt that they made banana nut bread. The smell drifted throughout the house, and the Cowboys actually held on to win a game that was a real stretch for them. Given that the Dallas Mavericks are going to make a serious run at having the worst record in basketball, maybe the Cowboys will add a little balance to the year.

I have been a season ticket holder to the Mavericks for about 34 years, starting at the very top row in the corner when tickets were (I believe) two dollars a game, which was about all we could afford at the time. My seats are much better now, but I've learned that the team really has to get fairly bad in order to get the draft picks that let it claw its way back to the top. The only exception to that rule seems to be San Antonio. But when a star like Kevin Durant decides to leave a contender like Oklahoma City to go play for already dominant Golden State in pursuit of a ring, the odds get badly stacked. There was no way that KD would come to Dallas for any kind of money – there wasn't a ring to be had here. It's not that Mark Cuban isn’t trying. He has been shuffling players in and out for several years, trying to come up with the right mix. Now, maybe we can get lucky in the draft and get another Dirk Nowitzki and start the building process all over. That run was fun.

I will readily admit to being more of a fair-weather Cowboys fan. It’s a lot more fun to watch them when they’re on a winning streak. I just never could work up much of a football appetite during the Tony Romo years. God bless him, I know he tried, but you just never had the feeling that lightning might strike any moment, the way you did when Staubach or Aikman were taking the snaps. Now we have a rookie quarterback who looks like he might become the real deal. He has people in Dallas salivating over how good he could be in three or four years with some experience under his belt. And that powerful offensive line we have is young, and they have contracts that will keep them here for another 4–5 years.

And that’s the lighter side of things – I was really trying to stay away from commenting on the recent choices by the President-elect for various cabinet positions. I know that many of them are controversial, but my Marine son-in-law (who was one of the first combat troops into both Fallujah and Ramallah) is ecstatic about James Mattis. Google what some of those who served under him and with him say about him. The man has a 7,000-book library and supposedly has read every book. Those around him say that he is sophisticated and knowledgeable on a wide range of topics. He is that rare breed, a warrior-intellectual who inspires men to follow him anywhere. I guess all you can say is “Semper Fi!”

You have heard me say several times this year in Thoughts from the Frontline that to succeed in what I call the “Decade of Disruption,” we all need to diversify trading strategies, not just assets. Our VIP service is designed to help you do exactly that.

A one-year subscription will save you 63% and a two-year subscription a full 74%. You should look into becoming a VIP – but remember, we will close the doors to new members on December 13 and won’t reopen for at least another six months. Look here for more details.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

It's time to hit the send button. It won't be long until I’ll be walking past Rockefeller Center to look at the tree and the ice skaters. The 10-day forecast says it will actually be winter there, so it will feel like Christmas. You have a great week!

Your focused on Europe now analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.

{kind=link}