Ed D'Agostino: Hi, I'm Ed D'Agostino. Thanks for joining me for this Mauldin Economics presentation.

Let me start with a quick story to set the stage for our discussion today.

I grew up on a farm in rural Vermont back in the days when you could ride in the bed of a pickup truck, and I often did, and it provided an interesting perspective. Riding in the back of a truck bed, you can't see where you're going; you can only see where you've been. That tailgate perspective is how a lot of people are thinking about investing these days. They see the past, and they just assume that the future will look the same.

And sure, a sense of market history is important, but the bigger financial rewards, the bigger opportunities belong to the people who can look ahead and see the massive trends converging on the horizon. I think we’re in one of those periods today, where there’s massive change ahead. That’s what we’re going to cover.

This has led to the latest evolution of our thinking and research at Mauldin Economics, and I’m going to share that with you today. It’s the answer to the biggest question we’ve gotten from readers over the years.

I believe we are at an inflection point in the markets, in the country, and in the world as a whole. I believe we’re heading into a new investing environment, and it’s nothing like what most investors are used to.

After the great financial crisis, investors could simply buy the market and do great. You could buy a broad-based ETF of the S&P 500 like SPY, or do the same thing for the NASDAQ with the QQQ ETF, and just watch your money grow. You could even buy what they call the FANG stocks. Any one of these approaches worked, and now that's over. We're entering a new investing environment.

I recently sat down with Felix Zulauf. He's the former global strategist at UBS, and he's one of the most successful macro investors of our time. He thinks money managers and investors are in for a period of big swings in the market.

Here’s an excerpt from our conversation.

Felix Zulauf:

Last time we spoke, Ed, I said, this decade is the decade of the roller coasters, and I still believe that what money managers and investors will go through in coming years is unseen. We have not seen anything like that before with the big swings in magnitude on both sides of the market.

Ed D’Agostino: So, what can investors do to prepare? That’s what we’re going to talk about.

Now is not the time to invest broadly in the market as a whole or even in a concentrated handful of seven tech stocks. I’m going to present an alternative today, a way to invest strategically in opportunities that are being fueled by big unstoppable trends. We've been following these trends and others, and we've assembled them into investible themes.

Here's what we'll cover:

-

Three big trends that my team and I are focused on

-

Three takeaways or themes derived from these trends

-

Two specific investment ideas.

I'll share the companies with you, plus a description of one other investment idea that we're about to recommend. I've assembled a great team to help me produce this research, and they'll be joining me throughout this presentation to share some of their findings and insights.

The first trend is on everyone’s mind right now. I’m sure you could guess it—you’ve been hearing about it everywhere. It’s AI, and it’s real. Harvard Business Review estimates AI could add $13 trillion to the global economy over the next decade. McKinsey & Company estimates that generative AI could add 2.6 to $4.4 trillion a year in economic value. We are still in the early innings with AI. The opportunities for investors who get this right are big.

It is not too late to invest in AI. Sure, early profits have been made, and congratulations to you if you owned Nvidia back in late 2020. But understand that AI will reshape the economy, and most people are asking the wrong question: Will AI destroy millions of jobs? Our research shows something very, very different. I believe AI will be a net positive for almost everyone. It's going to affect almost every industry and eliminate jobs and tasks that are undesirable.

In many ways, this is the next Industrial Revolution. So, how do you invest? Well, you've got to be careful because the hype around AI right now is outrageous. A review of transcripts found roughly 2,500 mentions of AI during earning calls of S&P 500 companies in 2023. That's 10 times more than the previous year. That's hype.

How do you pinpoint the real investing opportunities? This is where our approach and research process really shines.

I was in mergers and acquisitions for many years, and I just loved it. You get exposure to all kinds of companies, managers, owners, and business cultures. To be successful in M&A, you must be able to analyze any type of company. And you have to work in segments of the economy where there's growth, even if it's not yet obvious. You have to look ahead, and that forces you to build a deep understanding of the macro landscape and economic trends.

That background has served me very well over the years—going deeper, asking lots of questions. That's why we develop themes to drive our research process. Themes are a way to bring several trends together into one investible framework. It's a way of thinking about the direction and impacts of all these various trends. Themes allow us to invest in and around major multiyear, multi-industry shifts in the economy.

How does this apply to AI? Well, AI is a huge trend, but our research suggests that the bigger theme arising out of the AI trend will be America’s next productivity boom. When you combine AI with automation, and with what I call a “clean slate approach” to integrating AI into every aspect of business, starting from scratch in many cases, you have a better framework for identifying investment opportunities. Many companies won’t get this right. It takes management buy-in. It takes an understanding of how AI systems work. It takes access to a lot of data in a format that AI can train on, it takes a big investment, and it might require outside assistance.

The select few companies that get these elements right will boost their productivity to a level not seen since the days of Henry Ford. AI is an important piece, but it's one piece of this multi-trend puzzle. You need all three elements present to get the full benefit of AI: AI, plus automation, plus a rethink of your business's operations and processes.

The US economy, in particular, is prime for AI. We have a labor shortage. Unemployment is below 4%. We have a demographic problem in our country—our workforce is aging. The average age of a US farmer today is 57 years old. And there's a skills mismatch. We have about 9.5 million job openings, and those jobs might never be filled because we don’t have enough people with those specific skills.

On top of all that, we have Silicon Valley, the number one tech development ecosystem in the world, bar none. When you add artificial intelligence to this mix, you have a really exciting opportunity for the economy because the very best companies, the best managers, they're going to combine all these trends. This process is only just beginning.

Very, very few public companies have integrated AI at the level that I'm talking about, which means most of the investment opportunities are still ahead of us. So how do we invest? Well, we've identified two types of companies.

First, there are adopters. Adopters are companies that adopt AI early and deeply across all their business activities. Then they add in automation—not just physical automation, but automation of processes so that they gain an edge in their industry. They expand their margins, and they take market share. The other type of company are facilitators. These are the businesses helping the large multinational companies successfully implement and integrate AI.

And our first investment idea for you today is a facilitator. This is a 42-year-old international technology consultancy with its own AI arm. It's a company that will give us exposure to one of the world's fastest-growing economies. And what do I really like about it? It's one of the few companies positioned to profit from both the US and China's efforts to decouple, which we'll get into later.

I've asked Kevin Brekke to join us to go into the specifics on this investment idea.

Kevin's been a managing editor and senior analyst at Mauldin Economics since our founding in 2012. He's our resident contrarian. He's an avid traveler. He's lived in both the US and Europe for many years, so he brings a very global perspective to macro analysis. In fact, I think Kevin's currently on a boat, so I appreciate him taking some time from what he probably thought was a vacation to join us today.

Here’s Kevin Brekke:

Our first portfolio recommendation, Infosys. Infosys is an international company. It's an IT and consultancy. It's based in India, and its location gives it several advantages that we like. It can have efficiency and cost advantages, and it also means that they can avail themselves of a very large and talented labor pool.

It is also a company that we deem a facilitator, so they come in and assist other companies to achieve their goals. And one way they're doing that is they have embraced artificial intelligence, the AI revolution, and they have developed their own in-house platform, and they have also developed over 150 preset models that their clients can choose from and adapt to their own goals.

Again, we're really excited about Infosys and what Infosys is doing now. We’re excited about the management team and the direction they're headed. We're also excited to have you on board here at Macro Advantage.

Ed D'Agostino: Thanks, Kevin.

Now let's move on to trend number two. America is experiencing a manufacturing renaissance right now. Last summer, US construction spending on manufacturing reached $198 billion on an annualized basis. That's a 66% increase from the prior year. It's the highest level since the Bureau of Economic Analysis started tracking the data in 1950. This is part of a much bigger theme called Reshoring. The US is bringing critical industries and production back to North America. There's a lot driving this trend: supply change, shipping disruptions, rising labor and transportation costs overseas, geopolitical tensions. Companies are awake to the benefits of reshoring, and they're taking action.

Here's a list of companies that have brought major aspects of their production back to the US. Apple, Caterpillar, 3M, Intel—even good old GE, a pioneer of outsourcing. They’re bringing back key manufacturing, production, and service operations that were previously offshored to other countries.

So for perspective, in 2022, job announcements from reshoring and foreign direct investment rose 53% over the previous year, according to the Reshoring Initiative. They were 6,000% higher than they were in 2010. This is a big, big shift away from past decades when globalization was the dominant trend in business. Bank of America reported that S&P 500 companies mentioned reshoring on first-quarter earnings calls 128% more often than the previous year. Kearney Consulting's 10th Annual Reshoring Index Report notes that companies are reportedly scrambling to find facilities in the US and Mexico.

There's a direct correlation between the rise in geopolitical risks and the increase in corporate leaders talking about reshoring. Reshoring is going to upend global supply chains and reshape the global economy. It will allow companies to reimagine how they construct and operate a supply that will carry them forward into the next decade, and that's according to Omar Troncoso, who's a partner in Kearney's consumer and retail practice.

Reshoring is the best option for safeguarding our economy and our national security. And the key driver of reshoring isn't cost, it's resiliency. And it's not unique to the US by the way. China feels the same way. The need for resiliency is driving a global realignment of trade that will continue for years. And here's what most people get wrong about the reshoring trend.

Most people think COVID was the start of it, and it certainly was a contributor, but reshoring was underway well before COVID started, mainly because China's no longer a low-cost provider. For decades, ultra-cheap labor in China made up for the extra shipping costs, the time delays, the language barriers, political risks, the mountains of logistical hurdles.

Back when I was in business, we used to call it brain damage, right? You had to put up with a lot of brain damage because it was just so cheap to manufacture in China. It was worth it. Well, those savings are less compelling today because China's no longer a cheap labor leader.

The US government has placed a priority on reshoring with over $900 billion in incentives and investments. First is the CHIPS Act pushing over $50 billion into the domestic production of semiconductors. Then the Inflation Reduction Act that gives tax credits for onshore clean energy and manufacturing. It also includes $500 billion in private manufacturing investment. The Infrastructure Investment and Jobs Act earmarked funds for onshore energy supply chains. And finally, we have $75 billion worth of tariffs on solar panels, steel, aluminum, and washing machines even, and other goods from China.

So how do you invest? Well, there will be big winners and big losers from this trend. It's not as simple as investing in companies that are moving production back to the US because reshoring on its own isn't going to boost a stock price.

One loser that I mentioned last year were container shipping companies. So how do you pinpoint the real investing opportunities here? Well, I think this is where our research and our approach really shine.

It reminds me of a lesson I learned from one of my early mentors and friends. I'll call him EB to protect his privacy. But I met EB shortly after graduating from college. He owned the house that I was renting with a few friends back before I got married. He was a successful business person and an entrepreneur who retired early, and he started accumulating several investment properties, mainly just to keep himself busy, but also for the cashflow.

EB taught me one of my earliest lessons about building wealth. I saw what those rental properties did for him. So after getting married, instead of buying a single-family home like all of our friends were doing, my wife and I decided to buy a duplex. We lived in one side, we rented out the other, and we did so well that we ended up buying that single-family home just a few years later. But we held onto the duplex. Ten years later, we sold it and the profits paid for two of my three kids' college education.

By delaying the goal of owning a single-family house for just a few years, we made one of the best early investment decisions of our lives.

The lessons that I learned were have a plan, be patient, and investing early gives you an edge. That's why we develop themes. They're part of our plan, our process. We start with a top-down approach to investing, but then we add bottom-up analysis, good old-fashioned stock picking, but with fund-level research. And that's how we identify the investment opportunities that tie in with our themes.

We've identified our first investment idea based on reshoring, and I've asked my friend David Lutomski to walk us through the research and analysis that got us to this recommendation. David is our Macro team senior analyst. He's a level three CFA candidate. I hired him personally at Mauldin Economics years ago to join our analyst pool. And last year, I asked him to join me on the Macro team because I'm so impressed with his work. He takes our top-down approach, our themes, and then he adds his bottom-up company analysis... and he goes deep, which I really like.

David, thank you for joining us. Tell us about your way to invest in reshoring. I really like this idea. I mentioned before, global container shipping companies were going to be the big losers of reshoring. Well, this company is the other side of that coin.

Here’s David Lutomski:

Thank you, Ed, and thank you for the opportunity to be part of the Macro Advantage team. I'm very excited to be here.

We employ a top-down process, and we blend it with the fundamental process that's bottom up. The top-down process would be researching macroeconomic tailwinds that might benefit a company, and that is really epitomized in our themes. They're also a big part of the service. Then we blend that with the fundamental research, which is the bottom-up research. This is where we get into the income statement, the balance sheet, cashflow statements, and some valuation work, which we'll get to a little later on.

With that, let's get started with the top down. And this chart is extremely important. It jumped out to me and our team.

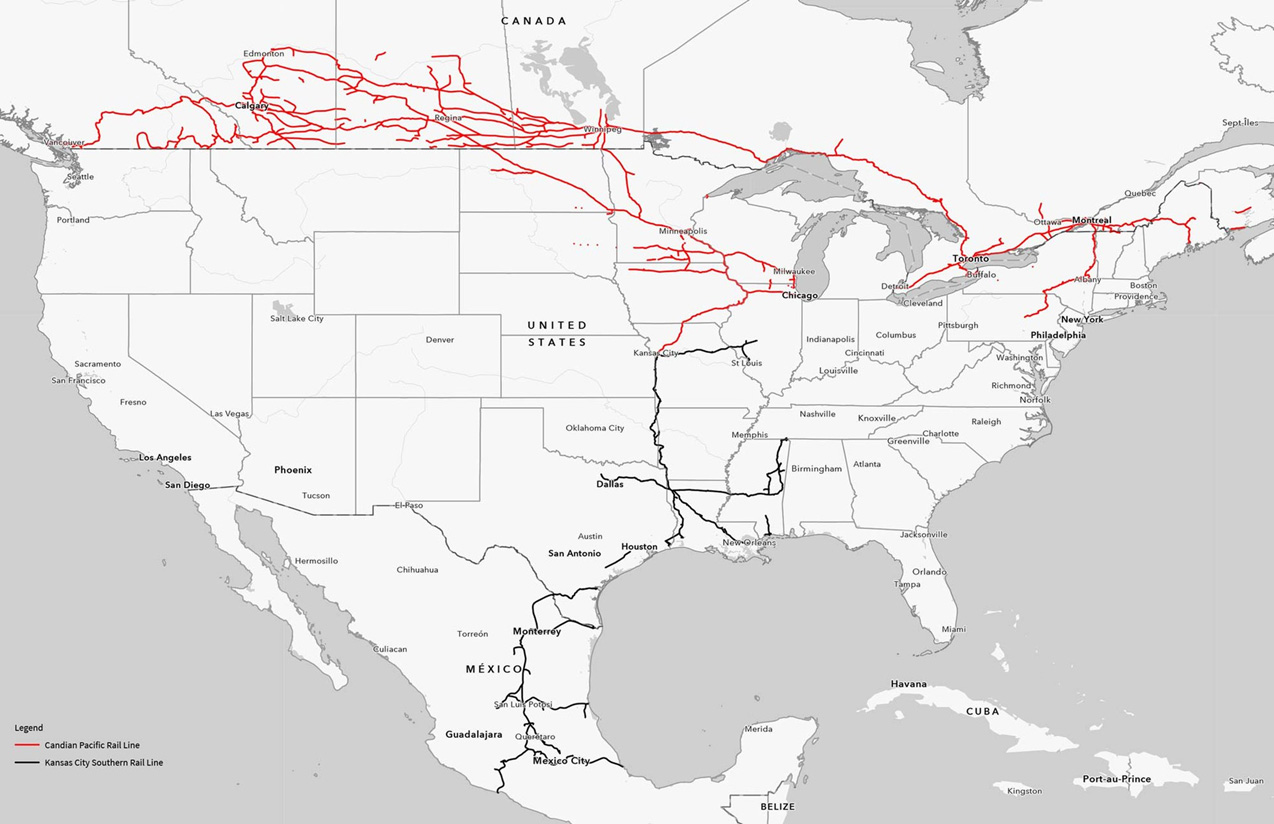

Canadian Pacific Kansas City Southern Rail Lines Run from Canada to Mexico

There are six Class 1 railroads that operate in Canada and the United States. You have Union Pacific and Burlington Northern Santa Fe, which is a Berkshire company, that operate primarily on the West Coast. You have CSX and Norfolk Southern that operate primarily on the East Coast. You have Canadian National, which operates in Canada. And then as of April 2023, when Canadian Pacific completed the merger with Kansas City Southern, they're now the only Class 1 railroad that has tracks in Canada, America, and Mexico, which is a huge advantage for us as investors. And that's something we're about to delve into.

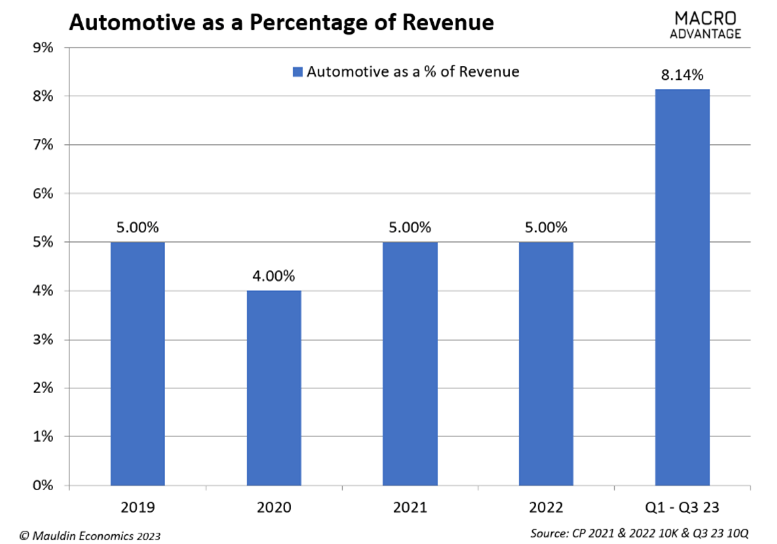

There are a lot of examples we could pick from, but the first one we picked was automotive. Automotive manufacturing has moved to Mexico. You can see in the chart below, this is the percentage of revenue from Canadian Pacific that was from the automotive segment. And you can see from 2019 to 2022, it hovers around 5% with 2020 being the exception because of COVID, which was a wacky year.

But you can look at the first nine months for 2023, and you see that automotive revenue as a percentage of revenue is up over 8%. And I believe, and I think our team believes, that this is reshoring in action. This is some proof in the pudding, and we see that here.

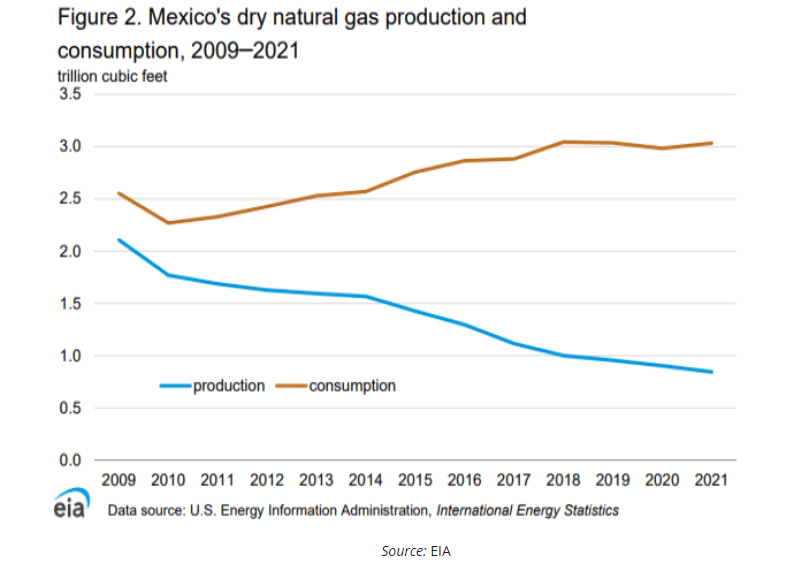

The second part to automotive manufacturing in Mexico is that these manufacturing facilities require enormous amounts of energy. The company we’re in, Canadian Pacific Kansas City, will be the company that delivers energy to Mexico to produce and manufacture these cars.

If you look here at this chart, you can see the orange line is consumption and the blue line is production. So, there's a shortfall. Canadian Pacific now has tracks from Alberta, Canada all the way down to Houston, which is where a lot of oil and gas get refined, and then down into Mexico, which can use it to manufacture cars. Then the cars can be distributed through Mexico, or sent back up into the United States and Canada.

So Canadian Pacific is servicing two very important industries just to create automobiles. And that's just one example. There are a ton of others.

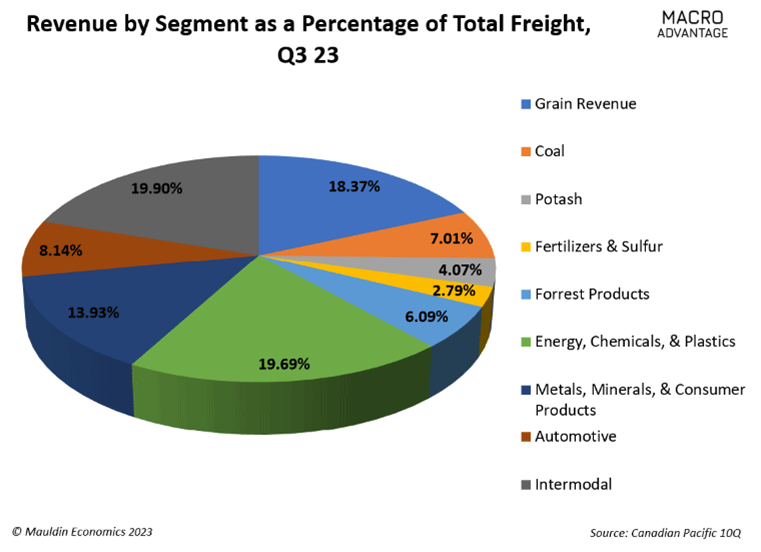

That brings us to one of my favorite pie charts. As you can see, all the industries Canadian Pacific services are very, very important. They're integral to the economy and to supply chains.

Automotive revenue is a little over 8%. The energy, chemicals, and plastics segment is about a fifth of their revenue. So that’s very important. And that ties together the top-down analysis since we think Canadian Pacific will fit and fulfill all these needs.

From there, we move to the bottom-up analysis. This is where we look at the financial statements, the income statement, the balance sheet, and the cashflow statement. And then we wrap it up with a little bit of valuation at the end. For Canadian Pacific, the fundamentals make sense, the price is right, and you’re getting paid about 70 to 80 basis points of yield via dividend. So, from all that, we think, wow, it seems like a great recommendation. So, we recommended it.

This is also where some portfolio management comes into play. For Canadian Pacific, we have a full position size in mind that we want to reach, but initially, we only recommended a third of that. We're going to use some portfolio management and kind of monitor the markets, so we can dollar-cost average and eventually build up to that full position.

In essence, you're getting that top-down analysis, the fundamentals, and then some portfolio management on the back end. That ties all this together for a recommendation that we really, really believe in, and we hope that when you read the recommendation, you do too, and are able to follow along.

With that, Ed, thank you for the opportunity to present and to be a part of the Macro Advantage team. I'm excited to be here, and I'm excited for you all to come on this journey with us. Thank you very much.

Ed D'Agostino: We've covered a lot of ground so far, so thank you for staying with me.

We've gone over two of our three top themes, and this seems like a good time to just take a step back and tell you more about the changes that are happening here at Mauldin Economics.

A big part of what we try to do at Mauldin Economics is to help people filter what's important. We try and show all sides of an issue, but in a way that's efficient for you. We want our work to serve as a touchstone where we can help you find information that you can invest in. And a question we often hear from you, our readers and viewers, and a top comment coming out of our Strategic Investment Conference every year is something like, “That was amazing. Thank you. But how do I invest?” That's the biggest unanswered question that we've had since we started Mauldin Economics.

How can you take the macro—the big picture, the cycles, the trends, the Great Reset that John's been writing about, or my themes like Reshoring and AI, all these big topics that we cover—how can you invest in these trends in a way that makes sense? Well, that's the next chapter or the evolution, if you will, of Mauldin Economics, and it's what we've been working towards for the past several years. We're launching a new type of research service, it's called Macro Advantage, and in many ways, it’s the fulfillment of my and John’s vision for Mauldin Economics.

I sat down with John a couple of weeks ago to talk about this. Here’s what he had to say.

John Mauldin: Ed, that’s just one of the reasons why I’m pretty enthusiastic about what you’re doing. We’ve been talking macro. We’ve been trying to figure out how it fits in, and how we can help our readers. And what you’ve been doing, the team you’ve been pulling together is kind of a culmination of... what, next year will be my 25th year of writing this letter, which has had a macro theme. But now we’re collaborating together. We’re working together to pull this into a framework that becomes more useful.

My letter has been self-limiting because I was a broker-dealer, an investment advisor. I had limits on what I could say and do. I mean, I just had limits about what I could say to buy or sell or anything like that. You don’t have those limits. Our business structure is completely different now. So you’re allowed to come in and say, “Let’s take this work, not just John’s work, but all of this data that we get together, and let’s put it into an actionable work.” I think that’s going to be a really exciting culmination of what I’ve been looking for, for a very long time.

Ed D’Agostino: The purpose of this briefing today is to share with you some of our top investing ideas, but also to introduce you to our new research service, but it’s not a sales pitch. Look, if you’re with me so far and you like what you hear, then please take a minute to learn about Macro Advantage.

Learn More about Macro Advantage

You can click here and a new window will open up with a special charter invitation for everyone who’s watching today as a thank you. Like I said, it should open up in another window so you can keep watching the rest of this presentation. I hope you take a minute to check it out. But regardless, let’s get back to our themes.

We’ve discussed AI. We’ve discussed Reshoring. That brings us to the third big trend that we’re following. We’re living in an increasingly multipolar world. There’s an obvious split forming in the world between East and West, and the examples are pretty striking. The Wall Street Journal reported just recently, China has passed Japan to become the number one auto exporter in the world.

This is a tectonic shift for a huge global industry, yet no one in the US would know by looking on the street. I mean, when’s the last time you saw a Chinese-made car? If you’re in Europe, it’s a different story, but in the US, we never would’ve known. Much of China’s exports, by the way, are going to Russia. The Chinese automaker BYD recently overtook Tesla as the world’s top electric vehicle seller. This is a major shift for most of us.

Since World War II, we first lived in a world with two superpowers, the US and Russia. Then the wall came down in Germany in 1989. The US, at that point, became the world’s undisputed heavyweight. In the early 2000s, we saw the rise of China with its economic power on full display after the United States’ great financial crisis. China’s surge in investing demand pulled the US and the entire world out of a global recession. It was very powerful.

But geopolitics is always in play. Nations are constantly rising and falling. What makes today unique is that many countries share a broad desire to be less dependent on the United States and the US dollar. The US is also bumping up against limitations on the number of conflicts it can handle both financially and diplomatically. This is leading more nations to take aggressive actions in their self-interests. They feel there’s less chance of US intervention. Venezuela is a good example of this. COVID accelerated the derailing of global trade in a way that made nations more aware of their dependencies, but also their strengths. Now, many are leveraging those strengths to gain regional influence or power or wealth.

I mentioned Felix Zulauf earlier. Well, he and I discussed the shift from a unipolar to a multipolar world, and here’s what he had to say.

Felix Zulauf: Usually, geopolitics or politics does not affect the market for very long. If something happens, it’s a short-term affair. However, if geopolitics or politics change the secular trend of the economic framework, then it affects markets. And I think that’s what we are seeing. The unipolar world order that has been very US-centric with the US as a major hegemon, that is over. That’s gone.

Ed D’Agostino: I agree.

Felix Zulauf: And we have now a transition period, which I would call disorder, and the world has to find a new order, which will likely be a multipolar order. If we cannot achieve that through diplomacy, we have to go through wars. And when the top dog is weakened or considered to be weakened, you have all sorts of conflicts popping up to the surface: Armenia, Serbia, Guyana, Gaza, what have you. And I think this will continue because the BRICS are considering the US as weak, and the US is not in a strong position. I quote, again, a famous historian who said, “The US needs another 10 years to be ready for war.” So the US is not ready for war, and that creates risks, much higher risks than we assume. So this makes for a very volatile world, very volatile markets. And what the biggest assets investors should have is an open mind and flexibility because the moves will be quite dramatic.

Ed D’Agostino: Today, you often hear the argument that the world is, again, dominated by two superpowers with China on the rise and the US in decline. I take a slightly different view. The US might get a lot wrong, but it remains the world’s leader in nearly every sector that matters: militarily, economically, even fiscally.

Culturally, we’re the tastemakers for most of the world. Our culture is emulated and envied. We can be energy independent, agriculturally independent, and we occupy an enviable geographic position in the world. We’re protected by huge oceans on two sides and friendly neighbors on the top and bottom.

You’ll note that most of our themes have a common thread that runs through them, and that’s American exceptionalism. We’re seeing it in the economy today: incredibly low unemployment, solid GDP growth, inflation dropping quickly. We are ahead of the entire world in terms of the pandemic recovery. There’s a lot of reasons to be bullish on the US right now, and this brings me to one of the big takeaways of the multipolar world idea.

As the East and West pull apart, America needs to become more resilient. Energy is one area of importance. We’re able to generate much of our own energy needs, but our friends in Europe are starved for resources. They may need our help with oil and gas. On top of that, there’s a push to generate more carbon-free energy. Like John says, “No one wants to see the air they breathe.”

How do we reduce pollution while simultaneously creating even more baseload power to keep our ever-growing AI and cloud computer centers fed with electricity, not to mention the demand that’s going to come from all the electric cars that are coming? Demand for electricity in the US is only going up. There’s only one answer to this problem that works at scale, and that’s nuclear energy.

So how do you invest? Well, backing up a little bit. It’s very hard to invest in geopolitical events. Usually, they have fleeting impacts on the markets, but where geopolitics matters is in determining trends. The development of a multipolar world is absolutely an investible trend. It will help you find areas outside of the US for investment. It will help you stay out of bad investment situations overseas, and it will help you source domestic opportunities that are going to benefit from trends. Areas outside of the US that we’re currently looking at right now include India and Japan. But as I mentioned earlier, when it comes to American resiliency, energy is important, very important.

Our team is wrapping up research on what will be our first recommendation under this Multipolar World theme. It’s a small cap. Its market cap is just under $1 billion, so that makes it a bit of a speculation. So, if you’re going to invest in it, I’d ask you to size your investment accordingly. But this is a company that ties into all the themes we’ve discussed today. It’s an investment in American resiliency, AI, reshoring, and the multipolar world. This company is on the cutting edge of energy, and as the US builds the next generation of nuclear power plants, small modular reactors or SMRs, this company will be a key supplier. Now because of its size, we’ll be releasing our research on this company exclusively to Macro Advantage readers next week.

You’ve just gotten a primer on what Macro Advantage is all about. My goal with this service is to give you a framework for understanding and profiting from big economic and market changes that are just getting underway. And if you’re still with me, my guess is you’re likely interested in what you’ve heard, and that’s great. I hope you join us. We’ve put together a special charter membership offer for you. You can see it by clicking here.

You know, I’ve been fortunate. For the past decade, I’ve spoken several times a week with John Mauldin, Olivier Garret, and Jared Dillian, and the interactions that I’ve had have been some of the most rewarding, informative, and interesting professional experiences of my career, and I suspect they’d say the same. I’ve learned from the interactions with each of them, and part of what I’m hoping to create with Macro Advantage is a community of investors: a community where we’re able to interact with each other and for you to interact with our team, including me. In effect, spreading out the power of interactive exchanges like I enjoy at Mauldin Economics.

I’ve asked Ann Pringle to talk a little bit about the community that we’re building. Ann’s our director of communications. She has a background in the legal profession. She has a law degree. She provides research support for our themes, and she’s our managing editor, which means she turns our wonky jargon into something we hope you want to read.

Ann, tell us a little bit about the online community that we’re building, and thanks for doing this.

Ann Pringle: Thanks, Ed. I’m happy to be back working with you, David, and Kevin again as part of the Macro Team.

Yes, as you mentioned, we have big plans to build a thriving Macro Advantage community. We want it to feel like a virtual clubhouse where members can come in, ask questions, share ideas, and connect with both us and with other members of the Macro Advantage community.

Macro Advantage members can access all our research, updates, and official communications in the community space, including our themes and portfolio recommendations. And we’re planning to regularly host special events like AMA sessions where Ed, David, Kevin, and I will jump in and answer your questions in real time. We already have one of those on the books for later this month, so that's something we're all really looking forward to.

Before I sign off, I want to say that we wouldn't be here without our members’ support and involvement, and we are truly grateful for each and every one of you. I look forward to seeing you all inside Macro Advantage community.

Ed D'Agostino: Ann, thank you.

One final thought. I recently had a great conversation with a viewer of mine, a gentleman who watches my interview series, Global Macro Update. He's a retired US Coast Guard rear admiral, and he went on to become the Homeland Security advisor to the president. So I'm pretty flattered that he watches me.

But he brought up an acronym that I'd never heard of before during our conversation. He said we're living in an increasingly VUCA world. VUCA stands for volatility, uncertainty, complexity, and ambiguity. These are all qualities that make a situation difficult to analyze, plan for, or respond to, and that's really what Macro Advantage is all about—giving you a framework and tools to make better sense of this VUCA world, so you can invest with more confidence as we transition into this new investing regime.

Thank you so much for spending so much of your time with me today. I hope you found it helpful, and I hope you'll join us in the new Macro Advantage community. I really appreciate all your support. Thanks for watching and take care.