The US Dollar and the Cone of Uncertainty

-

John Mauldin

John Mauldin

- |

- December 22, 2014

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinThe Beginning of a US Dollar Bull Market

There Has Been No Deleveraging

The Biggest Consequence of a Rising US Dollar

The Fourth Arrow

Adding China into the Mix

A Dangerous Illusion

Cincinnati, the Cayman Islands, Zurich, and Florida

Currently we have an international monetary non-system. Nobody has to follow any rules. Everybody does what they consider is in their own short-term best interest. The real difficulty is: What is in their short-term interest – for example, following ultra-easy monetary policy – could well backfire somewhere. It might be not in their long-term best interest. And as the easy monetary policy influences the exchange rates, it influences other countries. Almost every country in the world is in easing mode, following the Fed, and we have absolutely no idea how it will end up. We are in absolutely unchartered territory here.

– William S. White, former Chief Economist, Bank for International Settlements, in an interview for Finanz und Wirtschaft

I visualize this process [of forecasting the future] as mapping a cone of uncertainty, a tool I use to delineate possibilities that extend out from a particular moment or event. The forecaster’s job is to define the cone in a manner that helps the decision maker exercise strategic judgment. Many factors go into delineating the cone of uncertainty, but the most important is defining its breadth, which is a measure of overall uncertainty.

Drawing a cone too narrowly is worse than drawing it too broadly. A broad cone leaves you with a lot of uncertainty, but uncertainty is a friend, for its bedfellow is opportunity – as any good underwriter knows. The cone can be narrowed in subsequent refinements. Indeed, good forecasting is always an iterative process. Defining the cone broadly at the start maximizes your capacity to generate hypotheses about outcomes and eventual responses. A cone that is too narrow, by contrast, leaves you open to avoidable unpleasant surprises. Worse, it may cause you to miss the most important opportunities on your horizon.

– Paul Saffo, technology forecaster

Saffo borrows the term “cone of uncertainty” from weather forecasting. While you may not be familiar with the concept, you see it in use every time there is a hurricane forecast. The further away you get from where the hurricane actually is at the moment, the wider the “cone” predicting its possible paths.

For the past two letters we’ve been looking at the global scene and trying to figure out which issues will help us outline scenarios for 2015. We finish the series today by looking at the impact of the dollar bull market on the probabilities for various 2015 developments.

Let me say at the outset that I think a global currency war (kicked off by Japan last year and just now heating up) and a rising bull market in the US dollar are the big macroeconomic drivers not just for 2015 but for the next four to five years. I think all future economic outcomes pivot along with these two major forces – they are the lever and fulcrum, so to speak. As we look at all possible futures, as we map our own cones of uncertainty, it is certainly true that that our assessment could change with the emergence of important new trends at the outer fringes of the cone; but I believe (and have believed for some time) that we need to organize our forecasts around the currency war and the dollar bull market.

(Let me note that even though this letter is much shorter than usual in terms of actual words, for which readers may be grateful, it will print longer, as there are an unusually large number of charts.)

Before we jump into the letter, let me quickly suggest that you save the date for the Strategic Investment Conference next spring, April 30–May 2. We already have commitments from Ian Bremmer, Mohamed El-Erian, Niall Ferguson, Louis Gave, Jeff Gundlach, Lacy Hunt, Larry Meyer, Michael Pettis, David Rosenberg, and Grant Williams, and are close to finalizing an additional 4-5 headliners, which I expect to be able to announce in a few weeks. In short, the usual over-the-top group of speakers that I am somehow able persuade to show up in San Diego. Altegris Investments will have the web page up for you to register within a few weeks, and I really hope to see you there. I think this will be our best conference ever. Now let’s think about the dollar and its impact on macroeconomics.

The Beginning of a US Dollar Bull Market

Currencies are not supposed to have large movements in short spans of time and certainly not violent moves such as we have recently seen with the Russian ruble. Relatively stable currencies – ones that make moves measured in single digits over multiple years – are what you want to see for stable trade and world GDP growth. Violent moves like the ruble’s signal that something is seriously wrong, so wrong that it may well precipitate a deep recession. You very seldom if ever see a similarly rapid upward move in a currency. (Off the top of my head, I can’t think of one, but surely somewhere in history… and if I said “never,” I would probably be corrected by my astute readers.)

Over the last few centuries, as the world moved away from the gold standard and gold-backed currencies, the valuations of fiat currencies began fluctuating, sometimes wildly, over time. Currency wars following the onset of the Great Depression certainly contributed to the length of the downturn. After World War II, the financial leaders of the nations of the world came together and created a monetary system called Bretton Woods, named after the mountain resort in New Hampshire where it was created. Basically it was an anchored dollar system, where the dollar was convertible into gold and the rest of the world used the dollar for their reserves and generally pegged their currencies to it. The linchpin of the deal was the understanding that the US dollar would remain a stable currency.

We didn’t live up to that deal, printing too much money during the Vietnam War; and the nations of the world, led by France, began to ask to convert their dollars into gold. Since that would have drained the gold out of the United States, Nixon closed the “gold window.” We won’t get into the argument about the propriety of his move here.

The chart below shows the US Dollar Index (the DXY, which is heavily weighted to a comparison with the euro) since 1967. Prior to 1967 the dollar was generally stable. As the value of the dollar began to slide in 1970 – a troubling development if you were holding dollars in Europe – the world began to wonder if perhaps the United States was taking advantage of its position. Note that after the closing of the gold window in ’73 the dollar continued to fall but with greater volatility. This was mostly due to the Federal Reserve’s allowing inflation and printing money.

Then Paul Volcker came along and began to raise interest rates, and a major dollar rally ensued. The dollar doubled in value in less than five years. As interest rates came down from nosebleed highs in the late ’80s, the US dollar fell back to its original level and more or less drifted sideways for the next 10 years before once again climbing to 120. Then, in the early’00s, low rates and easy money took their toll, and the dollar fell to an all-time low in the middle of the credit crisis and has traded around the “80 handle” for the last six years. This is in spite of the Fed’s undertaking massive quantitative easing and flooding the world with dollars, which you would think would put downward pressure on the dollar. That is generally what happens when a central bank floods the world with its currency. Certainly, it is what is happening in Japan, and it is what we expect to happen in the Eurozone.

Something is different about the dollar, then. That difference can be explained mostly by the fact that the US dollar is the world’s reserve currency and the demand for dollars for global trade, which is growing at a rate the world has never seen, is stronger than ever. If the Federal Reserve had not entered into a policy of massive quantitative easing, it is entirely possible that we would have seen the dollar rise significantly over the last five years rather than languishing as it has.

Now that quantitative easing is finally done and the Federal Reserve is thinking about raising interest rates at a slow drip back to something that looks normal (possibly, maybe, perhaps, conceivably – we aren’t in any hurry and you may need to be patient for a considerable period of time and anyway everything is data-dependent), the coiled spring that is the dollar may be set free.

And since we are in background mode, we need to understand that there are many ways to measure the strength of the dollar. As I mentioned, in the standard US Dollar Index (the DXY), significant weight is given to the euro. To more accurately reflect the strength of the dollar relative to other world currencies, the Federal Reserve created the trade-weighted US dollar index (for more about it see here and here), which includes a bigger collection of currencies than the US Dollar Index.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The composition of the US Dollar Index (DXY) is

- Euro (EUR), 57.6%

- Japanese yen (JPY), 13.6%

- Pound sterling (GBP), 11.9%

- Canadian dollar (CAD), 9.1%

- Swedish krona (SEK), 4.2%

- Swiss franc (CHF), 3.6%

Thus a fall in the euro, as we’ve seen recently, changes the valuation of the index more than it might another index like the Bloomberg Dollar Index (BBDXY), which is composed of a broader basket, including emerging-market currencies, with less emphasis on EUR/USD:

- Euro (EUR), 31.4%

- Japanese yen (JPY), 19.1%

- Mexican peso (MXN), 9.6%

- Pound sterling (GBP), 9.5%

- Australian dollar (AUD), 6.2%

- Canadian dollar (CAD), 11.5%

- Swiss franc (CHF), 4.2%

- Brazilian real (BRL), 2.2%

- Korean won (KRW), 3.3%

- Offshore Chinese yuan (CNH), 3.0%

Note in the chart below that at times one index is stronger than the other. This is primarily a reflection of the strength or weakness of the euro and the fact that the Bloomberg Dollar Index contains a much higher proportion of emerging-market currencies.

So the takeaway here is that, when we say “the dollar is strong,” we are really talking about its strength relative to particular groupings of currencies. It’s a generalization. If an index included the Russian ruble or the Argentine peso, then the dollar would even be “stronger” as measured by that index.

There Has Been No Deleveraging

In general, nature keeps a balance in a given ecosystem. There is a continual adjustment between the number of predators and the number of prey, but over time the system tends toward balance.

Just as nature has a way of forcing balance in the order of things, basic accounting (math is its own force of nature) has a way of forcing balance in currency flows and valuations. Quantitative easing and the developing currency war have created a great imbalance in the global economic order. The process of rebalancing the world monetary system is somewhat chaotic and crisis-prone in the best of times. Now, the massive amount of debt, both public and private, that has been created in the past decade is making that process even more chaotic.

It is usual in a crisis like the Great Recession that there is a resolution in the amount of outstanding debt, through a process called deleveraging. The process can take many forms, but in the past it has almost always meant that at the culmination of the process there is less debt. However, in recent months I’ve highlighted papers demonstrating that this time around there has been no deleveraging. Central banks and governments simply did not allow it to happen. That means we have pushed the inevitable process of deleveraging into the future. Debt cannot grow to the sky – at some point it has to be dealt with.

Four years ago in Endgame and in speeches since, I’ve been proclaiming that the dollar is going to get stronger than anyone can possibly imagine. I was saying this even as the yen and the euro were strengthening at times against the dollar. Those who have been proclaiming the destruction of the dollar are just seeing one small part of the equation: quantitative easing. There is a far larger and more complicated process going on in the world, and the rebalancing that is underway is going to mean that the dollar will increase in value against most currencies, and against some currencies by a great deal.

The Biggest Consequence of a Rising US Dollar

The beginning of a bull market in the dollar has multiple consequences, many of them not benign. Let’s start with the BIG one, the USD breakout and unwind of the USD-funded carry trade.

The yen and euro are dropping fast as the USD strengthens. As of today, the EUR/USD is below 1.23, while the USD/JPY has climbed to nearly 120. This is a function of central bank policy divergence… which in turn is a function of economic divergence among the major developed economies… which in turn is a function of debt divergence in those various economies. Total debt-to-GDP is approximately 334% in US, 460% in the Eurozone, and 655% in Japan, according to Lacy Hunt’s latest note.

With such divergence comes the major macro risk that the US Dollar Index (DXY) is breaking out in a big way. To anyone who believes in technical analysis (and skeptics should keep in mind that a lot of macro and currency traders DO), it looks like the USD is ready to break out of a 29-year downtrend that began with the Plaza Accord way back September 1985. The reversal of a trend that has been in place for that long is going to catch a number of people offsides. Unfortunately in investment and economics, you get more than a five-yard penalty for being offsides on a trend this big.

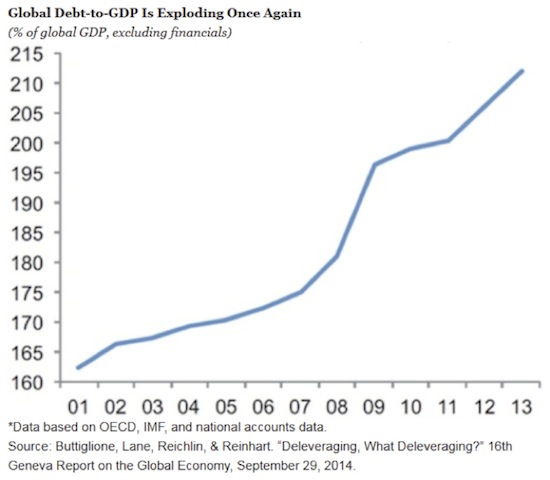

We are now going to look at a number of charts in rapid-fire fashion. As noted above, the dollar bull trend is exacerbated by debt. Global debt-to-GDP has been rising over the past several years.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

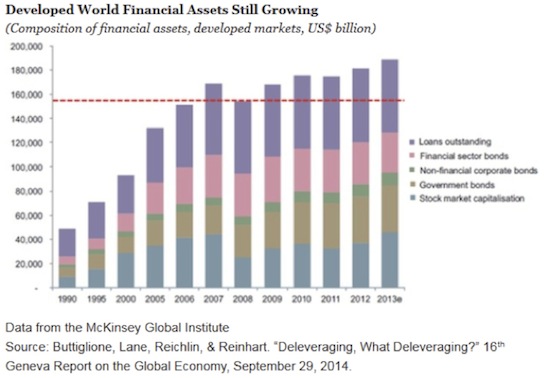

The pool of developed-world financial assets is still growing, after a minor decrease in 2008. Again, there has been no deleveraging.

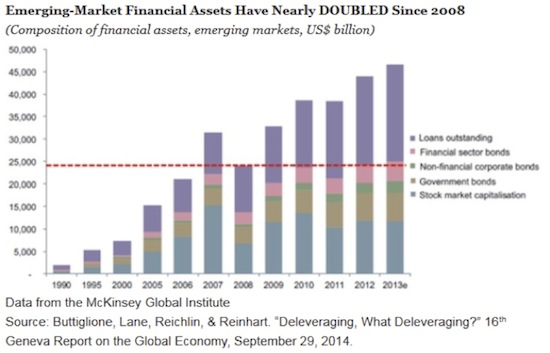

Even though debt and financial assets have been growing in the developed world, the real explosion in debt and financial assets has occurred in emerging markets, where the unwarranted flow of easy money has fueled a borrowing bonanza on the back of a massive USD-funded carry trade.

These QE-induced capital flows have kept EM sovereign borrowing costs low and enabled years of elevated emerging-market sovereign debt issuance, even as many of those markets displayed profound signs of structural weakness. I’m seeing estimates for the USD-funded carry trade around the world ranging from $3 TRILLION to $9 TRILLION. Raoul Pal believes it is roughly $5T, with nearly $3T of that going directly into China. (Other estimates for China suggest a somewhat lower number, but whatever it is, it is massive.)

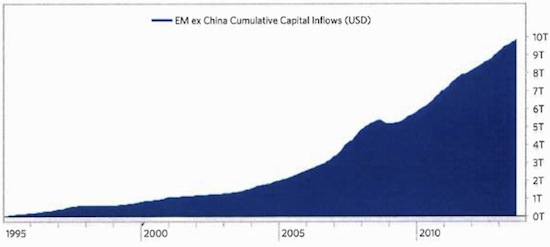

Earlier this year, Bridgewater argued that total portfolio flows into emerging markets had doubled between 2008 and early 2014, from $5T to $10T.

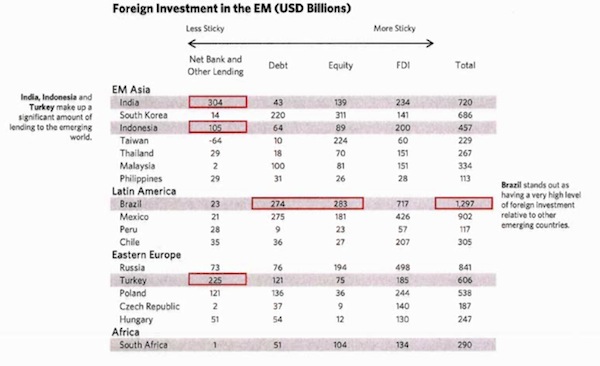

Their study gave us some very specific data on flows into the larger EMs.

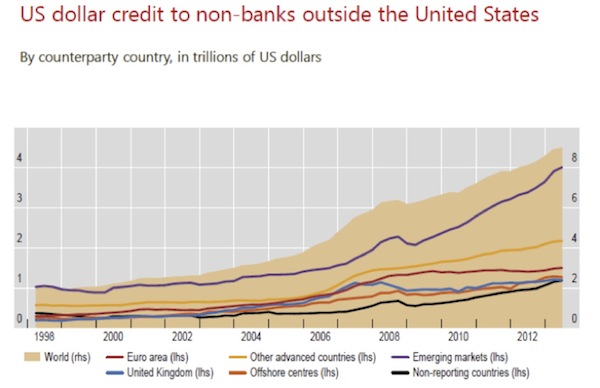

The following slide from Hyun Song Shin, head of research for the Bank for International Settlements, estimates that total USD-denominated credit to non-banks outside the United States is more than $9T.

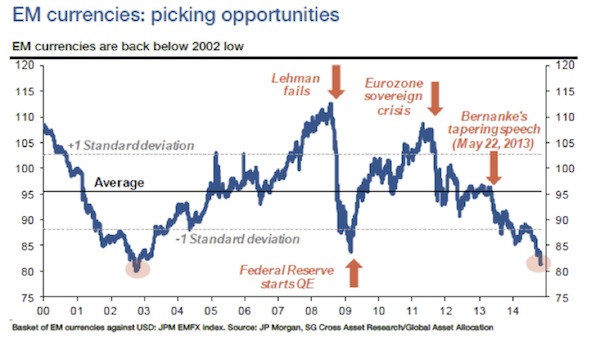

What I’m getting at here is that a reversal in flows from a forceful unwind in USD capital flows could have disastrous effects on emerging markets... and there are a number of ways the unwind could blow back on the USA and other developed markets in coming quarters. The crazy thing is that EM currencies as a group have already given back more than 10 years of gains… and their losses can get a LOT worse.

Companies and governments in emerging markets have borrowed in dollars because of the ultralow interest rates available, but they earn the money to pay those loans back in local currencies. If the local currency is dropping significantly faster than the dollar, then no matter how profitable a business is, it is sinking deeper into debt with every tick up in the dollar. That’s what happened in 1998, and it’s happening again today.

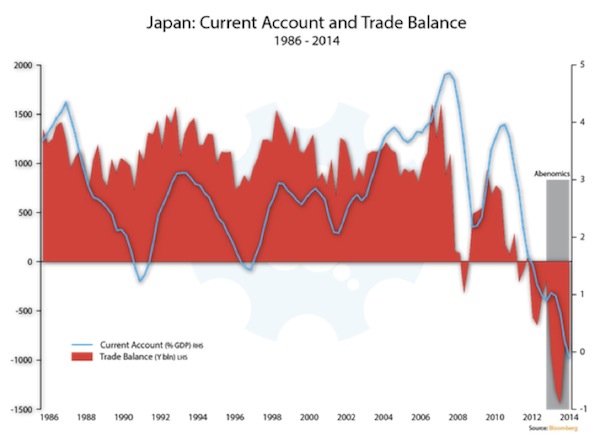

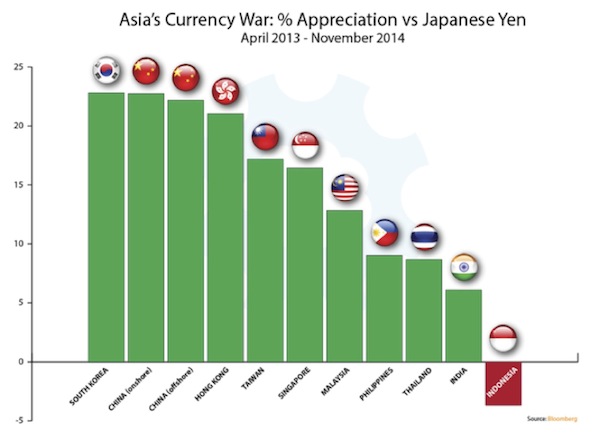

Moving on in our survey of the world, we see the Japanese yen continuing to fall as the Bank of Japan engages in the most massive experiment in quantitative easing the world has ever seen. And they are doing it at the time when Japan’s current account and trade balance are both deeply negative.

These three realities combined mean that the yen is going to fall much further. The fourth, unstated, poison-tipped arrow of Abenomics is the launching of a major currency war, the consequences of which are now starting to be felt, as we can see in the next chart.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The potential for policy mistakes or monetary crises on the part of other Asian nations is very real and very troubling. We could see a country lose control of its currency as it tries to respond to Japan, and it is not altogether unlikely that at some point Japan itself will lose control, which would bring about a whole different set of problems and crises. Meanwhile, the US dollar’s rise will go on creating further problems for dollar-denominated debt in emerging markets, including China, which may decide that it needs to respond by devaluing the renminbi.

China’s investment boom is cooling; its competitiveness is eroding; and markets may already be pricing in a renminbi devaluation. China’s boom was largely a result of foreign direct investment and a massive increase in debt in a short period of time. Even though bank lending has grown substantially, the real growth in debt in recent years came through an explosion in non-bank loan funding. China has created a shadow banking system that is staggering in size.

There have been a number of studies on the relationship between the rapidity of growth of debt and subsequent financial crises. Even if we look to a broad sample of 48 instances over the last 50 years where total social finance expanded by as little as 30% over five years (less than half the magnitude of China’s credit explosion), history suggests there is still a 50% chance of a banking crisis or an abrupt fall in growth during the post-boom period. My point is that there is a clear relationship between the intensity of a credit boom and the subsequent adjustment (downward) in GDP growth rate. There are no cases in modern history where an economy has managed to avoid a banking crisis or outright bust after experiencing rapid lending growth anything like China’s ongoing credit boom.

The world is simply not prepared for a major China slowdown, let alone a hard landing. And gods forbid that the Chinese have a problem at the same time that Europe slides back into crisis.

The big question is, what happens next in China? Personally, I think it will be very difficult to avoid a real fall in the Chinese growth rate in the next 3-5 years. The reforms required to rebalance China to a more sustainable growth model will be very painful, and there is a real chance they could bring on a banking panic in the short term; but without those reforms, China literally has no chance. The Chinese Dragon is attempting a very intricate and delicate dance. The world needs China to succeed, but we must recognize that a Chinese hard landing is very much within our cone of uncertainty.

I want to close this letter with a quote from William White, who recently did an interview with Finanz und Wirtschaft, perhaps the leading business and economics newspaper in Switzerland. White is the highly regarded former chief economist of the Bank for International Settlements. Longtime readers may recall that I have quoted him at length over the years, as his writing is some of the most thought-provoking in the economics world.

The interview focused on the decision by the Swiss National Bank to go to negative interest rates on January 22, 2015. Not coincidentally, the European Central Bank will be meeting that day to decide whether or not to implement its own quantitative easing program. The Swiss are quite concerned about the massive capital inflows that are pushing their currency to very uncomfortable levels. In a highly unusual move, they are going to start charging banks for the privilege of holding Swiss currency accounts.

For the Swiss to enact such a move means that they must be convinced that the ECB is actually going to do something on January 22. Technically, it is against the rules for the ECB to buy sovereign debt, and the Germans are adamantly opposed. But my highly connected friend Kiron Sarkar asks:

What if the ECB does introduce a QE programme, involving the purchase of EZ government debt, though only on the basis that the relevant countries meet pre-agreed targets? You have provided a massive incentive to introduce structural reforms, dealt with the German's/Bundesbank objections, and those countries that play ball will benefit from lower interest rates and a weaker euro. On the other hand, if EZ countries do not cooperate, yields on their bonds will blow out massively – just the right stick to wield. It's the classic carrot and stick approach. Too fanciful? Well, maybe, but...

I guarantee you just such a solution is being talked about. We will see what actually gets implemented. Now let’s turn to the conclusion of White’s interview (emphasis mine):

The SNB has to follow the ECB in its monetary policy. Is it not dangerous when the monetary policy of one country affects another?

Currently we have an international monetary non-system. Nobody has to follow any rules. Everybody does what they consider is in their own short-term best interest. The real difficulty is: What is in their short-term interest – for example, following ultra-easy monetary policy – could well backfire somewhere [else]. It might be not in their long-term best interest. And as the easy monetary policy influences the exchange rates, it influences other countries. Almost every country in the world is in easing mode, following the Fed, and we have absolutely no idea how it will end up. We are in absolutely unchartered territory here. This worries me the most. The Swiss National Bank has been doing well in what it was forced to do by this international monetary non-system. The Swiss have to do the best they can, because that is what everybody else is doing.

What are the risks of this non-system?

There is no automatic adjustment of current account deficits and surpluses, they can get totally out of hand. There are effects from big countries to little ones, like Switzerland. The system is dangerously unanchored. It is every man for himself. And we do not know what the long-term consequences of this will be. And if countries get in serious trouble, think of the Russians at the moment, there is nobody at the center of the system who has the responsibility of providing liquidity to people who desperately need it. If we have a number of small countries or one big country which run into trouble, the resources of the International Monetary Fund to deal with this are very limited. The idea that all countries act in their own individual interest, that you just let the exchange rate float and the whole system will be fine: This all is a dangerous illusion.

My associate Worth Wray will join us next week, presenting his forecast for 2015, which will concentrate on the emerging markets and China. I will return after the first of the year with my own 2015 forecast – there is much to ponder over the next couple of weeks.

Cincinnati, the Cayman Islands, Zurich, and Florida

I am home for the rest of the month, but the calendar for next year is beginning to fill up. I see Cincinnati, Grand Cayman, Zurich, and Florida on my schedule. It has been awhile since I was in the Cayman Islands, and this time I’ll take a short hop over to Little Cayman to visit my friend Raoul Pal for a few days. A brilliant macroeconomist and trader, Raoul has now based himself in Little Cayman, although he frequently flies to visit clients. He is also a partner with Grant Williams in Real Vision Television, a fascinating new take on internet investment TV. I’ll be writing more about it in the future.

And speaking of Grant, I wish him well as he embarks upon a new endeavor, that of turning his passionate avocation of writing his brilliant newsletter Things That Make You Go Hmmm… into a business. It has been an honor and privilege to publish Grant for these last years and to help bring his wicked (not to say warped) humor and dazzling writing style to a larger audience. But the far greater reward has been getting to know Grant personally. I appreciate the kind words he wrote about me in his letter last week, and the feeling is mutual. Grant is just one of the most genuinely nice people I have ever met.

Next week all my kids and grandkids and their extended families will gather for Christmas, whereupon I will cook, lose complete control of everything, and try to savor the chaos. There will be lots of presents and watching sports and eating and siblings catching up with each other on events that have played out over the past few months.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

“Dad, will you be going to the Lakers game the day after Christmas?”

It was my daughter Abbi, who, of all my children, is the biggest sports fanatic. She lives in Tulsa, so she doesn’t get to attend many games, so how could I say no? And I do thoroughly enjoy watching Kobe and Dirk do their dance.

I find it a fascinating thing about us humans that we somehow feel better if “our” team of overpaid athletes beats “your” team of overpaid athletes. I guess it’s somewhat genetic, inherited from the days when tribal identity was an all-important survival trait. And even though I know that my survival is not dependent upon the success of the Dallas Mavericks (for which I’m grateful), I do enjoy watching the game along with 17,000 other screaming fans. After having an office above right field in the ballpark of the Texas Rangers and watching so many games over the 15 years I was there, about the only professional sport I watch now is NBA basketball. I truly think it is the most beautiful of sports.

Abbi was the one to alert me a few days ago that the Mavericks had traded for Rajon Rondo. Rondo is a four-time all-star point guard. One of the good things about being a Dallas Mavericks fan is that Mark Cuban is your owner. I know he’s somewhat controversial, but the guy truly cares whether or not the Mavericks win every season. You really can’t have a better owner. This year he assembled the deepest bench I have ever seen on any NBA team. Right now teams can carry 15 players, but they will have to cut that to 12 as we get deeper into the season. We were going to have to cut one or two players who could put in solid minutes for any other team in the league. Before the addition of Rondo, the team was a collection of a few great players and a lot of very good players. Not enough to win a championship but enough to compete.

Simply competing is not enough for Cuban. Mark traded three very good players (and a first-round draft pick) for one potentially great player who can take us to another level. But given that we already have four other great players, his move is clearly a gambit to try and win it all this year. We still need a second big man, but with this trade we go from competing as a second-round team to potentially getting to the finals. And we still have a lot of players who might be traded for that big man. This last trade is a big gamble by Cuban that he can re-sign Rajon at the end of the year and keep him around.

So “my” team just got better, at least for this year. The local tribe part of me (I’m always somewhat amused that it even exists) is quite happy. As is the rest of the local tribe.

It is time to hit the send button. Let me take this opportunity to wish you and all your families and friends the merriest of Christmases and the happiest of New Years. This is one of those times when our tribe expands to encompass the globe, to become part of a greater celebration, one in which the other “team” does not have to lose in order for us all to be happy.

Have a great week. I forecast that the final episode of The Hobbit will be coming to a theater very near me very soon. And that forecast has a very narrow cone of uncertainty.

Your gathering my own small tribe together this week analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.