The Flat Debt Society

-

John Mauldin

John Mauldin

- |

- October 20, 2014

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinThe Return of the XIX Century Panic?

The Velocity Trap

The Economic Singularity

An Exogenous Cause of the Next US Recession

Chicago, Athens (Texas), Boston, Geneva, Atlanta, and New York

Replace the FDA

International Monetary Fund chief Christine Lagarde says the global economy is facing “the risk of a new mediocre, where growth is low and uneven.”… Lagarde said Europe's 18-nation bloc that uses the euro currency – collectively the world's biggest economy – is facing the "not insignificant" risk of falling back into a recession. (VOA News)

Since at least the beginning of 2006, the most asked question I get after a speech is “Do you think we will have inflation or deflation?” In an attempt at humor, my answer has been “Yes.” I go on to try to explain that we are in a deflationary environment, but eventually we will see inflation. When QE1 was announced, there were many pundits (none of the Keynesian variety) who immediately said the risk was for significant inflation, and there were even those (like Peter Schiff) who talked of hyperinflation and the demise of the dollar. Interest rates would rise, and US government bonds would collapse.

My response at the time was that the Federal Reserve would print more money than any of us could possibly imagine (and who imagined $3+ trillion?), and we would not see any inflation. My reasoning was that we were in a deleveraging world where the velocity of money was clearly falling. I explained – once again – the relationship between inflation and the velocity of money.

Beginning with last week’s letter, “Sea Change,” my answer to that question for the foreseeable future will be simply, “Deflation.” In Endgame Jonathan Tepper and I described the economic environment of a deleveraging world, especially that of Europe. In Code Red we described the coming world of currency wars, with Japan having fired the first shot. Sadly, we continue to see the themes of those books play out in the real world.

Over the coming months we are going to explore the implications of a rising dollar for equity markets, global trade, commodity prices (especially oil), interest rates, and Federal Reserve policy, just to mention a few of the areas that will be impacted as global currency flows shift and protectionism is on the rise. Not all markets and governments will be affected in the same way, and there will be any number of opportunities for investors who are willing to think outside of the status quo.

In this week’s letter we’re going to explore some of the implications of deflation. We will start with an internal client letter from my friend Charles Gave that deserves to be shared. Then we’ll explore a few thoughts on the velocity of money. I should note that I am deeply indebted to Dr. Lacy Hunt for my understanding of the velocity of money. To the extent I get things right it is because of his frequent and long-suffering help, and if I get something wrong it’s because I didn’t understand the things he said correctly or couldn’t communicate them properly. These two men, both of whom I think of as mentors and statesmen, have had a huge impact on my thinking. The fact that they both talk with deeply resonating basso profundo voices that remind me of the voice of God in a movie soundtrack may have something to do with that impact! In any case, it lends an air of authority to their musings. Charles even has the long flowing white hair. (Thanks to David Hay for sending me the following note from Charles.)

The Return of the XIX Century Panic?

The readers may have noticed that for the last few months, I have almost never written on economic activity, monetary policy or inflation. Most of my writings and presentations have been on one topic and only one, how to construct an “antifragile” portfolio to use the terminology coined by Nassim Taleb. For me, the monetary policy followed by the central banks had to lead to a collapse in the velocity of money, and from there to deflation.

My recommendation was thus to hedge any equity positions with a long-dated US zero. So far so good.

Let me hazard for the first time in quite a while a prognosis on the future of ‘economic activity’ in the US. In the 19th century, which was deflationary most of the time, we did not move from a recession to a bear market, but from a bear market, called a “panic” at the time, to a recession. Let me explain.

When there is no inflation [see my notes below – John], the choices are between a deflationary boom and a deflationary bust. And the sober reality is that we move from one to the other only when the stock market crashes. What create the recession are not excess inventories or capital spending as in an inflationary period but the collapse in asset prices which had been pumped up by the general mood of optimism.

[Reread that paragraph at least a few times. We’re going to explore this concept further.]

Since we had plenty of debts attached to the prices of those assets, margin calls came in, and from there we moved to a true collapse in the velocity of money, accompanied more often than not by banks going belly up (see Barings with Argentina for a good example).

I have absolutely no doubt that trillions of dollars must have been borrowed one way or the other to play the rise in asset prices engineered by the central banks. Similarly, I have no doubt that huge amounts must have been borrowed to develop new sources of energy and that the break-even price for these new sources is probably being reached as I write. [Emphasis mine.]

To use my usual Wicksellian analysis, it is probable that the market rate is moving very quickly ABOVE the natural rate. If it were not, bonds would have no reason to outperform equities as they have for the last 12 months….

If I am right, it implies that a recession may be arriving and this recession should be preceded by a genuine collapse in bank shares, where most of the bad debt is probably parked and the bank shares are underperforming big time. The good news [is] of course that we are arriving at the end of one of the stupidest periods in economic history; the bad news is that asset prices will have to adjust to the new reality.

I maintain what I have said for a long time: No negative cash flows. No big debts. Hedge with government bonds.

Hold those thoughts for a moment, as we need to explore the velocity of money a little further before looking at the implications of what Charles is telling us.

The St. Louis Fed defines the velocity of money as “the frequency at which one unit of currency is used to purchase domestically produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time.”

Irving Fisher gave us the famous Fisher Equation of Exchange. Reduced to its most simple form, it comes out as P=MV, where P is the nominal gross domestic product (not inflation-adjusted here), M is the money supply, and V is the velocity of money. You can solve for V by dividing P by M. By the way, this is known as an identity equation. It is true at all times and all places, whether in Greece or the US.

Saint Milton Friedman taught us that inflation is always and everywhere a monetary phenomenon. That is, if the central bank prints too much money, inflation will ensue. And that is true, up to a point. A central bank, by printing too much money, can bring about inflation and destroy a currency, all things being equal. But that is the tricky part of that equation, because not all things are equal.

What that means is that to understand rate of change in pricing (known as either inflation or deflation) you must know not only the amount of money in circulation – the money supply – but the rate at which the money is circulating through the economy. If the velocity of money is slowing, the supply of money can rise without an increase in inflation.

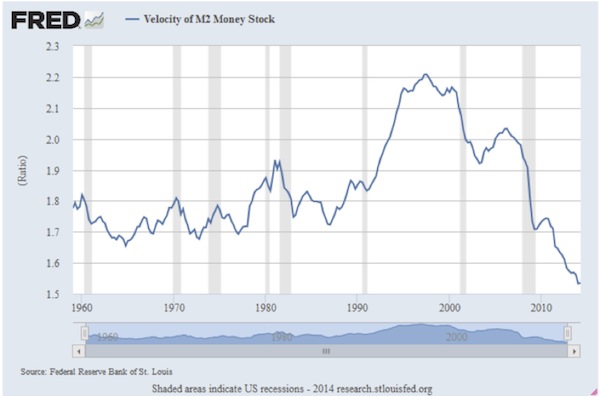

And that is precisely what has been happening. In fact, the velocity of money has been slowing since 1997 (back in the Clinton years – remember him?). But it slowed rapidly prior to both recent recessions and for the past few years has been falling off the cliff. The following chart is from the St. Louis Federal Reserve FRED database.

Note that when Milton Friedman did his famous study on the relationship between money supply and inflation he based his research on the period from the early ’50s until the late ’70s. The only way that inflation can only be solely a monetary supply phenomenon is if Fisher’s equation of exchange is not true. But Prof. Friedman so firmly believed in that equation that he had it put on his license plate:

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

For the period of time that Friedman was studying velocity it was largely stable; but after he had completed his monumental research, velocity in fact did change, as we can see from the graph. (It is actually even more complicated than I will go into in this letter, as one has to look at demographics and population as well as productivity. But let’s not digress.)

If you were looking only at the St. Louis Fed chart, and you saw the little hook upward for the recent quarter, you might reasonably wonder whether velocity might not now be turning, since it appears to be at an all-time low. If velocity began to rise, would inflation come back?

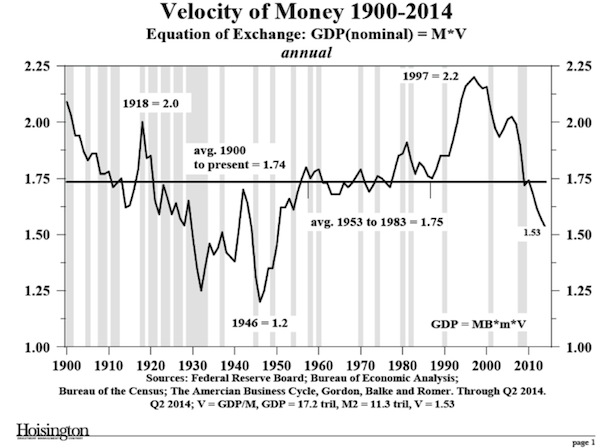

Thanks to a great deal of research done by others and encapsulated by Dr. Lacy Hunt at Hoisington Management, we can actually reconstruct the velocity of money back to 1900. And as the graph below shows, in deflationary periods velocity can slow even more than it has recently. I should point out that Lacy emphasizes that the velocity of money is mean-reverting over very long periods of time. So there will come a day when velocity begins to rise and we will need to start paying attention to inflationary forces.

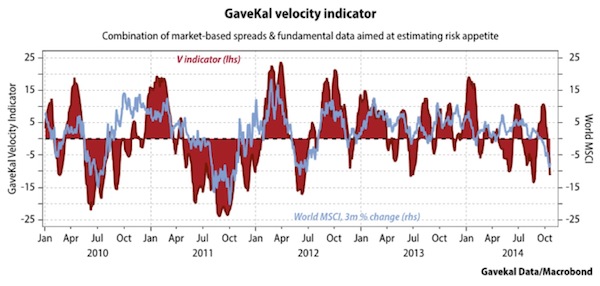

My friends at GaveKal produce their own velocity indicator, which is a combination of multiple market spreads and fundamental data from around the world. I thought I would include it, as it is often useful to look beyond the borders of the United States. Notice that velocity has become quite volatile in the last year but has once again turned to the downside.

There are many factors that affect the velocity of money, but one of the key elements is debt. What matters is not so much the amount of debt but the productivity of debt. Fisher told us you become over-indebted when you get too much unproductive debt.

Debt (leverage) can be a very good thing when used properly. For instance, if debt is used to purchase an income-producing asset, whether a new machine tool for a factory or a bridge to increase commerce, then debt can be net-productive. Hyman Minsky, one of the greatest economists of the last century, saw debt in three forms: hedge, speculative, and Ponzi.

Roughly speaking, to Minsky, hedge financing occurred when the profits from purchased assets were used to pay back the loan; speculative finance occurred when profits from the asset simply maintained the debt service and the loan had to be rolled over; and Ponzi finance required the selling of the asset at an ever higher price in order to make a profit. Minsky maintained that if hedge financing dominated, then the economy might well be an equilibrium-seeking, well-contained system. On the other hand, the greater the weight of speculative and Ponzi finance, the greater the likelihood that the economy would be what he called a deviation-amplifying system.

Minsky's Financial Instability Hypothesis suggests that over periods of prolonged prosperity, capitalist economies tend to move from a financial structure dominated by (stable) hedge finance to a structure that increasingly emphasizes (unstable) speculative and Ponzi finance.

Minsky proposed theories linking financial market fragility, in the normal life cycle of an economy, with speculative investment bubbles that are seemingly an inevitable feature of financial markets. He claimed that in prosperous times, when corporate cash flow rises beyond what is needed to pay off debt, a speculative euphoria develops; and soon thereafter debts exceed what borrowers can pay off from their incoming revenues, which in turn produces a financial crisis. As the climax of such a speculative borrowing bubble nears, banks and other lenders tighten credit availability, even to companies that can afford loans, and the economy then contracts.

“A fundamental characteristic of our economy,” Minsky wrote in 1974, “is that the financial system swings between robustness and fragility and these swings are an integral part of the process that generates business cycles.”

Singularity was originally a mathematical term for a point at which an equation has no solution. In physics, it was proven that a large-enough collapsing star would eventually become a black hole, so dense that its own gravity would cause a singularity in the fabric of space-time, a point where many standard physics equations suddenly have no solution.

Beyond the “event horizon” of the black hole, the models no longer work. In general relativity, an event horizon is the boundary in space-time beyond which events cannot affect an outside observer. In a black hole it is “the point of no return,” i.e., the point at which the gravitational pull becomes so great that nothing can escape.

This theme is an old friend to readers of science fiction. Everyone knows that you can't get too close to a black hole or you will get sucked in; but if you can get just close enough, you can use the powerful and deadly gravity to slingshot you across the vast reaches of space-time.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

One way that a black hole can (theoretically) be created is for a star to collapse in upon itself. The larger the mass of the star, the greater the gravity of the black hole and the more surrounding space-stuff will get sucked down its gravity well. The center of our galaxy is thought to be a black hole with a mass of 4.3 million suns.

We can draw a rough parallel between a black hole and our current global economic situation. (For physicists this will be a very rough parallel indeed.) An economic bubble of any type, but especially a debt bubble, can be thought of as an incipient black hole. When the bubble collapses in upon itself, it creates its own black hole with an event horizon beyond which all traditional economic modeling breaks down. Any economic theory that does not attempt to transcend the event horizon associated with excessive debt will be incapable of offering a viable solution to an economic crisis. Even worse, it is likely that any proposed solution will make the crisis more severe.

In Endgame, we explored the idea of a Debt Supercycle, the culmination of decades of borrowing that finally ends in a dramatic bust that unfortunately is almost by definition deflationary. Unfortunately, much of the developed world is at the end of a 65-year-long Debt Supercycle – and thus we approach our economic singularity.

A business-cycle recession is a fundamentally different thing from the end of a Debt Supercycle. A business-cycle recession can respond to monetary and fiscal policy in a more or less normal fashion; but if you are at the event horizon of a collapsing debt black hole, monetary and fiscal policy will no longer work the way they have in the past or in a manner that the models would predict.

There are two contradictory forces battling in a debt black hole: expanding debt and collapsing growth. Raising taxes or cutting spending to reduce debt will have an almost immediate impact on economic growth. But there is a limit to how much money a government can borrow. Clearly that limit can vary significantly from country to country, but to suggest there is no limit puts you clearly in the camp of the delusional.

When unproductive debt (Minsky’s Ponzi finance) takes over, velocity will continue to fall until you clear up the debt. Debt overhang must be dealt with. One of the amazing things about Irving Fisher is that he did not have access to the data we have today, but he inferred the entire process from having lived through it during the Great Depression. It is Friedman who compiled the data. (Friedman also said that Fisher was the greatest economist.) One of the critical things Fisher understood was that extreme over-indebtedness was the prime problem, and falling velocity was merely one of the symptoms. Velocity’s falling as precipitously it has in the last decade is a warning sign that we are on the wrong track.

A great deal of the blame for slower growth can be laid at the foot of debt. As Lacy Hunt writes this week:

Over the latest five years ending June 30, 2014, real GDP expanded at a paltry 2.2% annual rate. In comparison, from 1791 through 1999, the growth in real GDP was 3.9% per annum. Similarly, real per capita GDP recorded a dismal 1.4% annual growth rate over the past five years, 26% less than the long-term growth rate. A large contributor to this remarkable downshift in economic growth was that in 1999 the combined public and private debt reached a critical range of 250–275% of GDP. Econometric studies have shown that a country’s growth rate will lose about 25% of its “normal experience growth rate” when this occurs. Further, as debt relative to GDP moves above critical threshold levels, some researchers have found the negative consequences of debt on economic activity actually worsens at a greater rate, thus becoming non-linear. The post-1999 record is consistent with these findings as the U.S. debt-to-GDP levels swelled to a peak as high as 360%, well above the critical level noted in various economic studies.

The modern economic equivalent of the Flat Earth Society is the Flat Debt Society, whose members contend that there is no negative impact no matter how large the debt gets. They point to Japan and note that their debt has risen to 250% of GDP – and the country still exists. The fact that nominal GDP is where it was 20 years ago is only evidence to them that Japan has not spent enough. But Japan is not a special case. They’re going to have to deal with a great deal of pain in absorbing their debt back into the central bank. It is going to dramatically impact the value of the yen, hurting retirees, pensioners, and consumers. There is no free lunch.

The boom of the last 60 years roughly correlates with ever-increasing debt. History teaches us (with over 200 incidents to learn from) that there is an endpoint beyond which debt becomes destabilizing and has to be dealt with, generally through a period of great destabilization.

An Exogenous Cause of the Next US Recession

I (and others) have argued that while the US is in a slow-growth period, there is nothing internal that could push us into recession. Rather, the catalyst for recession would have to be something from outside the country – what economists call an exogenous event. The two primary risk factors I see on the horizon are China and Europe having crises of their own that seriously affect the world.

I argued last week that we are moving into a far more deflationary environment, brought on by a rising dollar. Above, Charles Gave pointed out that in a deflationary environment the typical causes of business-cycle recession are no longer the primary culprits. Let’s review this paragraph from Charles:

When there is no inflation, the choices are between a deflationary boom and a deflationary bust. And the sober reality is that we move from one to the other only when the stock market crashes. What creates the recession are not excess inventories or capital spending as in an inflationary period but the collapse in asset prices which had been pumped up by the general mood of optimism.

In one of the great ironies, if he is right, it is precisely the inflation of assets brought on by QEs 2 and 3 that has put us in the greatest danger of another recession. The parallels with the 1920s and ’30s is an obvious but not very pleasant one. Growth in leverage and asset inflation during the ’20s led to the crisis of the ’30s.

Rather than using the time that monetary policy has bought us to restructure our fiscal policy, we have doubled down on increasing government debt and student loans. Can anyone seriously argue that transfer payments and other government debt are productive debt? We are already seeing current consumption seriously impacted by student loans.

If Charles is right, then we (I include myself in this group) are looking for the cause of the next recession in exactly the wrong place. The argument many economists and analysts have been making it that since there is nothing fundamentally wrong with the economy, any correction in the stock market is simply a pause on the way to further bull-market highs. What Charles is saying is that the correction itself leads to the recession in a deflationary environment.

This is something that no developed-market participant has any personal experience with. The last time we saw a true deflationary environment was in the 1930s. Charles argues that at the zero point, at the zero bound between inflation and deflation, there is a change in the forces that drive economic growth.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

This is as profound a change as the one that occurs when liquid water turns to ice. Except that we know precisely the temperature at which water starts to freeze. Unfortunately, our measures of inflation are nowhere near as precise as our measures of temperature. Our measures of inflation are subjective (as I have shown in numerous letters) and are only generally useful in getting the direction right. Different measurement and analytical techniques might show strong inflation or outright deflation, based on the same underlying data.

While I can find no rhyme in Charles’s assertions, I can certainly see the rhythm, a simple synchronicity. It is exactly what you would expect to happen at the end of an Debt Supercycle. And it is precisely that relationship among debt, asset prices, and deflation that the Flat Debt Society will tell you does not exist. They will tell you the chance of too much debt creating a problem has precisely the probability of hell freezing over. It is just that in their theory hell never gets to 32°. Classical economists, on the other hand, do see the potential for too much of the wrong kind of debt to freeze up the markets. Minsky Moment indeed!

It is not just in the US that there are problems. The problems of Europe, Japan, and China have all been chronicled in this letter. Michael Pettis has been arguing for some time that the world must be seen in the context of global imbalances. For instance, if China is consuming 60% of the world’s iron ore production, that is not a sustainable trend. Ore production has risen to meet demand, but as China inevitably begins to rebalance, it is causing iron ore demand to collapse (and Pettis thinks it has further to go); and that deep dip in demand is putting pressure on the economies of countries like Australia and Brazil that produce iron ore. There are scores of such imbalances that have built up in the world. In his latest blog, Pettis writes:

“[But I do think that the framework [the imperative of global rebalancing] I have used over the past decade has been useful, at least to me, in understanding both the rebalancing process in China and the events that led up to the global crisis of 2007-08. And I think it continues to be useful in judging the adjustment process – or, more likely, the lack of adjustment – that explains why we still have a rough ride ahead of us. This framework has made it relatively easy to make predictions, sometimes “surprising” ones, because by working through the imbalances and assuming – safely, I think – that deep imbalances always eventually reverse one way or the other, we can work out logically the various ways in which this rebalancing must take place.

I have argued that since the 2007-08 crisis we have seen some adjustment in the US, very limited adjustment in China or Japan (except to the extent that Beijing under Xi Jinping has stopped imbalances from getting worse), and worsening imbalances in Europe, and it is for this reason that I have never been impressed by the strong market recoveries we saw around the world. If I had to summarize the key points about the framework I use, I would make four main points:

- The adjustment process. All growth creates imbalances, and in every case these imbalances will eventually reverse. What really determines a developing country’s long-term success, I believe, is not how well it does during the growth years, but rather how well it manages the subsequent adjustment. Growth miracles are very common, but real success stories are rare. The reason, I would argue, is that developing countries too easily reversed the great gains they made during the good years because the adjustment turned out to be far more costly than anyone had anticipated. It is far more important, consequently, for economists and policymakers to understand how to manage adjustment and minimize adjustment costs than to figure out how to generate rapid growth.

- Debt and balance sheets. Probably the single biggest sources of adjustment costs are the amount and structure of debt, or, more generally, the structure of balance sheets. Economists must understand (but almost never do) national balance sheets and sovereign financial distress as well as corporate finance specialists understand business balance sheets and corporate financial distress.

- Savings imbalances. The purpose of savings is to fund productive investment, and while the amount of productive investment opportunities is probably infinite, institutional constraints in every country significantly can reduce the ability of productive investment fully to absorb the total amount of savings created within an economy. These constraints vary from country to country, and until we understand how to remove these constraints, rising income inequality and mechanisms that repress the growth of median household income (relative to GDP growth) often result in what I would call excess savings. The consequences of excess savings include speculative asset booms, trade imbalances, unemployment, and unsustainable increases in debt.

- Globalization. In a “globalized” world, no country, not even the US, can protect itself from the consequences of imbalances elsewhere. The global economy is a system in which certain types of imbalances are impossible. I especially focus on the requirement that global savings and global investment always balance, but there are others. Because an imbalance at the global level is impossible, if there are imbalances in one country or region, there necessarily must be the opposite imbalances in another, and the more open an economy, the more likely it is to respond to imbalances elsewhere. It is impossible, in other words, to understand any non-autarchic economy in the world except in the context of global imbalances.

This rebalancing process that Pettis describes (we will review his new book when it comes out in a few weeks) will almost certainly mean an adjustment in asset prices around the world. That adjustment is going to lead to the increased volatility that I was talking about last week, and that volatility is going to lead to a flight to a safe-haven currency, which the world sees as the US dollar. The potential is growing for a real correction leading to outright recession in a period when inflation is receding.

The stock market is down only 5% from its high, and the last two times the Fed has exited QE the market dropped roughly 20% over three months. Even Jim Bullard, who only a few weeks ago was writing about dealing with the risk of inflation and normalizing interest rates sooner than the expected June 2015 FOMC meeting, said in a speech last week that “We could go on pause on the taper at this juncture and wait and see how the data shakes out into December.” When a “hawk” like Bullard (who represents the normally monetarist St. Louis Federal Reserve) started talking about postponing the end of QE, the markets responded with a massive upward move. Talk about your whipsaw communication.

I am pretty sure that Yellen and team are not all that pleased with the corner into which they are now painted. While $15 billion a month is not all that significant in the grand scheme of things – and I think the market, on reflection, will understand that – it has been enough to get the rockets roaring.

The Federal Reserve is in danger of losing the narrative. And the pressure on them to do something will grow if we continue to see the dollar rise and inflation fall. If the markets respond as they have to the end of past QEs, will the Fed once again feel that it needs to respond with yet another round of QE to forestall a drop in asset prices?

Ambrose Evans-Pritchard argued this week that the world economy is so damaged that it may need permanent QE:

Combined tightening by the United States and China has done its worst. Global liquidity is evaporating.

What looked liked a gentle tap on the brakes by the two monetary superpowers has proved too much for a fragile world economy, still locked in “secular stagnation”. The latest investor survey by Bank of America shows that fund managers no longer believe the European Central Bank will step into the breach with quantitative easing of its own, at least on a worthwhile scale.

Markets are suddenly prey to the disturbing thought that the five-and-a-half year expansion since the Lehman crisis may already be over, before Europe has regained its prior level of output. That is the chief reason why the price of Brent crude has crashed by 25pc since June. It is why yields on 10-year US Treasuries have fallen to 1.96pc, and why German Bunds are pricing in perma-slump at historic lows of 0.81pc this week.

We will find out soon whether or not this a replay of 1937 when the authorities drained stimulus too early, and set off the second leg of the Great Depression.

While I believe that central banks should not focus on asset prices but instead on ensuring overall stable monetary prices, the reality is that markets have responded quite positively to quantitative easing. I along with many others argued that the withdrawal process from QE was never going to be easy. As Minsky taught us, the longer the central banks try to maintain a period of stability, the greater the problems of instability will be at the end of the process.

I’m not certain where I read it, but someone suggested that the world economy should be checked into the Betty Ford clinic to learn to withdraw from the massive overdose of quantitative easing that various central banks have foisted upon it.

Recessions are by definition deflationary. Two things we learned from This Time is Different by Rogoff and Reinhart are that economies are more fragile and volatile than we knew and recessions are more frequent after a credit crisis.

When we enter the next recession (and there is always another recession), the Flat Debt Society will be screaming for more stimulus, more quantitative easing, and more debt. Count on it. Their prescription for dealing with the problems arising from debt is similar to telling an alcoholic to drink more whiskey. They deny that debt can be a problem. Their theories prove it. They even have books and papers by noted academics to show that there is no such thing as too much debt, at least as long as you can print money. Currency wars be damned.

We’re entering a period of renewed global volatility. Adjust your portfolios and hedges accordingly.

Chicago, Athens (Texas), Boston, Geneva, Atlanta, and New York

I’m back on the road. Tomorrow is jam-packed with meetings and ends with a late-night discussion with Woody Brock here in Dallas. Tuesday I go to Chicago for a speech, fly back very early to a meeting with Kyle Bass and friends at his Barefoot Ranch in Athens, Texas, and then fly out to Boston to spend the weekend with Niall Ferguson and some of his friends at his annual briefing. I am sure I will be happily surfing mental stimulus overload that week. I fly from Boston to Geneva for a few days and then more or less directly to Atlanta for a day (board meeting), before heading back to Dallas. I will also be going to New York in the middle of November.

This weekend I flew to Houston to be with Worth Wray and his new bride, Adrienne. It was a lovely wedding, and the bride was beautiful. One of the interesting episodes had nothing to do with the wedding but rather with my taxi driver. He’s an engaging fellow from Ethiopia who is been in the States for years, and the first time he drove for me I took his card and have called on him for four trips. We have gotten to know each other, and this time around he began to express his frustrations over the response to Ebola.

The world ignores Africa. Just a little help would save so many lives, but we don’t even get the basics. And they ignore what we have learned about Ebola. The doctors and other healthcare workers in Africa know how to take care of these patients and keep from getting the disease themselves. But nobody wants to pay attention to what we have learned.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Sadly, last night I learned that the situation is even worse than he thought. Presbyterian Hospital in Dallas is one of the finest institutions in Texas, but their initial procedures for dealing with their first Ebola patient were simply incompetent. The details will eventually come out, and Presbyterian is doing the right things now, but our entire healthcare system is simply unprepared to deal with what should have been a very foreseeable crisis. While I don’t think that Ebola in its current form will be a serious risk to developed-world countries, it does expose some major flaws in our system.

But the worst flaw is in our drug regulatory process. Only a few months ago the FDA (Food and Drug Administration) was doing everything it could to slow down the development of new drugs for Ebola. Now that there are a few cases of Ebola in the US and we have a general news panic, it seems they can’t encourage drug development fast enough. Nothing changed except the politics.

A few people in the US contract Ebola and suddenly the FDA allows companies to pull out all the stops. My side bet is that we will have a cure for Ebola in the not-too-distant future.

The serious tragedy here is that millions of people die every year from all sorts of diseases that are on the verge of being cured. There are very hopeful new technologies in the labs, but the FDA is preventing them from getting to you. When I say millions of people that is NOT an exaggeration. But those diseases haven’t caused a political firestorm. We need to change that. We need to create a firestorm to force change on the most deadly bureaucracy in America.

There are hundreds of life-saving drugs and other therapies that are being kept from you and me because bureaucrats are using 19th-century science to try to deal with technologies developed in the 21st century. They are more interested in protecting their personal fiefdoms and reputations than in saving lives. Gods forbid we have a drug that might cause a problem, so they sacrifice progress and our collective health – indeed our very lives – on the altar of self-interested bureaucratic expediency. Oh, they couch it in all sorts of high-sounding words, but the results are the same. You and I are prevented from making good choices about our own healthcare and saving the lives of our loved ones.

The FDA does not need to be reformed; it needs to be replaced. We need as a country to create a commission to design a 21st-century Drug Regulatory Authority and then turn over the regulatory process to this new authority. If any of the current structure fits in the new system, then fine. Otherwise, close it down.

As an economist, I would point out that we are leading the world in biotechnology research, but we’re going to see that research create jobs elsewhere if we don’t figure out how to develop the cures and procedures in this country. We need to slash the cost of drug development by 90%. If we do that, we will see the number of new drugs and procedures increase by orders of magnitude.

Pat Cox and I are watching companies that have the ability to cure scores of some of the most debilitating diseases known to mankind, but they are frustrated at every level by the FDA. And the technologies that are on the drawing board are even more mind-blowing. We simply have to get our heads around this situation and make the needed changes.

I’ve talked with a number of other people around the country and am quite serious about trying to form a group to launch an initiative to replace the FDA with sensible 21st-century regulation. It will take some money and time to build an organization. If you have either, drop me a note and let me know, and I will get in touch with you.

It is time to hit the send button. I am excited about all the meetings and people I will get to see in the next 12 days, but the travel schedule is going to be a little rough. Nothing I haven’t done before, and it will totally be worth it. You have a great week!

Your seeing deflation everywhere analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.