A Code Red World

-

John Mauldin

John Mauldin

- |

- October 26, 2013

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinCentral Bankers Gone Wild

An Introduction: Code Red

Keeping Up with Tech

New York, Florida, Geneva, Saudi Arabia, and Canada

I wasn't the only person coming out with a book this week (much more on that at the end of the letter). Alan Greenspan hit the street with The Map and the Territory. Greenspan left Bernanke and Yellen a map, all right, but in many ways the Fed (along with central banks worldwide) proceeded to throw the map away and march off into totally unexplored territory. Under pressure since the Great Recession hit in 2007, they abandoned traditional monetary policy principles in favor of a new direction: print, buy, and hope that growth will follow. If aggressive asset purchases fail to promote growth, Chairman Bernanke and his disciples (soon to be Janet Yellen and the boys) respond by upping the pace. That was appropriate in 2008 and 2009 and maybe even in 2010, but not today.

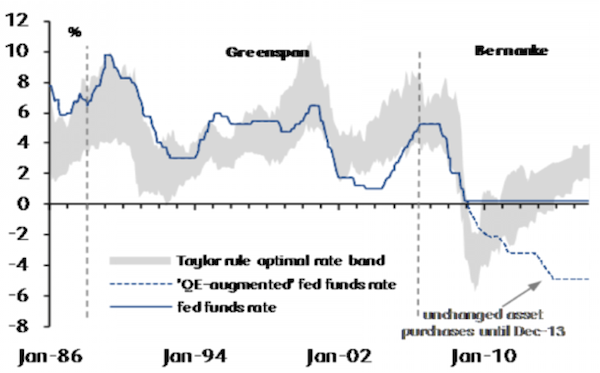

Consider the Taylor Rule, for example – a key metric used to project the appropriate federal funds rate based on changes in growth, inflation, other economic activity, and expectations around those variables. At the worst point of the 2007-2009 financial crisis, with the target federal funds rate already set at the 0.00% – 0.25% range, the Taylor Rule suggested that the appropriate target rate was about -6%. To achieve a negative rate was the whole point of QE; and while a central bank cannot achieve a negative interest-rate target through traditional open-market operations, it can print and buy large amounts of assets on the open market – and the Fed proceeded to do so. By contrast, the Taylor Rule is now projecting an appropriate target interest rate around 2%, but the Fed is goes on pursuing a QE-adjusted rate of around -5%.

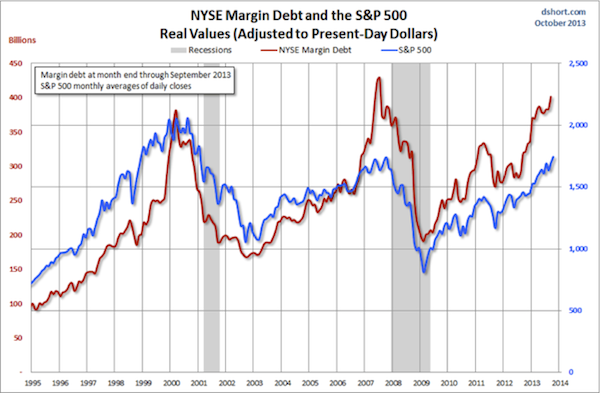

Also, growth in NYSE margin debt is showing the kind of rapid acceleration that often signals a drawdown in the S&P 500. Are we there yet? Maybe not, as the level of investor complacency is just so (insert your favorite expletive) high.

The potential for bubbles building atop the monetary largesse being poured into our collective glasses is growing. As an example, the "high-yield" bond market is now huge. A study by Russell, a consultancy, estimated its total size at $1.7 trillion. These are supposed to be bonds, the sort of thing that produces safe income for retirees, yet almost half of all the corporate bonds rated by Standard & Poor's are once again classed as speculative, a polite term for junk.

But there is a resounding call for even more rounds of monetary spirits coming from emerging-market central banks and from local participants, as well. And the new bartender promises to be even more liberal with her libations. This week my friend David Zervos sent out a love letter to Janet Yellen, professing an undying love for the prospect of a Yellen-led Fed and quoting a song from the "Rocky Horror Picture Show," whose refrain was "Dammit, Janet, I love you." In his unrequited passion I find an unsettling analysis, if he is even close to the mark. Let's drop in on his enthusiastic note:

I am truly looking forward to 4 years of "salty" Janet Yellen at the helm of the Fed. And it's not just the prolonged stream of Jello shots that's on tap. The most exciting part about having Janet in the seat is her inherent mistrust of market prices and her belief in irrational behaviour processes. There is nothing more valuable to the investment community than a central banker who discounts the value of market expectations. In many ways the extra-dovish surprise in September was a prelude of so much more of what's to come.

I can imagine a day in 2016 when the unemployment rate is still well above Janet's NAIRU estimate and the headline inflation rate is above 4 percent. Of course the Fed "models" will still show a big output gap and lots of slack, so Janet will be talking down inflation risks. Markets will be getting nervous about Fed credibility, but her two-year-ahead projection of inflation will have a 2 handle, or who knows, maybe even a 1 handle. Hence, even with house prices up another 10 percent and spoos well above 2100, the "model" will call for continued accommodation!! Bond markets may crack, but Janet will stay the course. BEAUTIFUL!!

Janet will not be bogged down by pesky worries about bubbles or misplaced expectations about inflation. She has a job to do – FILL THE OUTPUT GAP! And if a few asset price jumps or some temporary increases in inflation expectations arise, so be it. For her, these are natural occurrences in "irrational" markets, and they are simply not relevant for "rational" monetary policy makers equipped with the latest saltwater optimal control models.

The antidote to such a boundless love of stimulus is of course Joan McCullough, with her own salty prose:

And the more I see of the destruction of our growth potential … the more convinced I am that it's gonna' backfire in spades. Do I still think that we remain good-to-go into year end? At the moment, sporadic envelope testing notwithstanding, the answer is yes. But I have to repeat myself: The data has stunk for a long time and continues to worsen. And the anecdotes confirming this are yours for the askin'. The only question remaining is for how long we can continue to bet the ranch on wildly incontinent monetary policy while deliberately opting to ignore the ongoing disintegration of our economic fabric?"

And thus we come to the heart of this week's letter, which is the introduction of my just-released new book, Code Red. It is my own take (along with co-author Jonathan Tepper) on the problems that have grown out of an unrelenting assault on monetary norms by central banks around the world.

I saw the actual book for the first time this week and found myself reading it with fresh eyes. We finished the last draft less than two months ago and rushed it to press; but perusing it again this week, I found it even more timely than when we hit the send button to deliver it to the publisher. So, without further ado, let's jump right into the introduction. (If nothing else, you must read my redo of Jack Nicholson's speech from A Few Good Men – as delivered by Ben Bernanke.)

When Lehman Brothers went bankrupt and AIG was taken over by the US government in the fall of 2008, the world almost came to an end. Over the next few weeks, stock markets went into free fall as trillions of dollars of wealth were wiped out. However, even more disturbing were the real-world effects on trade and businesses. A strange silence descended on the hubs of global commerce. As international trade froze, ships stood empty near ports around the world because banks would no longer issue letters of credit. Factories shut and millions of workers were laid off as commercial paper and money market funds used to pay wages froze. Major banks in the US and the UK were literally hours away from shutting down, and ATMs were on the verge of running out of cash. The world was threatened with a big deflationary collapse. A crisis that big comes around only twice a century. Families and governments were swamped with too much debt and not enough money to pay them off. But central banks and governments saved the day by printing money, providing almost unlimited amounts of liquidity to the financial system. Like a doctor's putting a large jolt of electricity on a dying man's chest, the extreme measures brought the patient back to life.

The money printing that central bankers did after the failure of Lehman Brothers was entirely appropriate in order to avoid a Great Depression II. The Fed and central banks were merely creating some money and credit that only partially offset the contraction in bank lending.

The initial crisis is long gone, but the unconventional measures have stayed with us. Once the crisis was over, it was clear that the world was saddled with high debt and low growth. In order to fight the monsters of deflation and depression, central bankers have gone wild. Central bankers kept on creating money. Quantitative easing was a shocking development when it was first trotted out, but these days the markets just shrug. Now, the markets are worried about losing their regular injections of monetary drugs. What will withdrawal be like?

The amount of money central banks have created is simply staggering. Under quantitative easing, central banks have been buying every government bond in sight and have expanded their balance sheets by over nine trillion dollars. Yes, that's $9,000,000,000,000 – twelve zeros to be exact. (By the time you read this book, the number will probably be a few trillion higher, but who is counting?) Numbers so large are difficult for ordinary humans to understand. As Senator Everett M. Dirksen once probably didn't say, "A billion here, a billion there, and soon you're talking about real money." To put it in everyday terms, if you had a credit limit of nine trillion dollars on your credit card, you could buy a MacBook Air for every single person in the world. You could fly everyone in the world on a round-trip ticket from New York to London and back. You could do that twice without blinking. We could go on, but you get the point: it's a big number.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

In the four years since the Lehman Brothers bankruptcy, central bankers have torn up the rulebook and are trying things they have never tried before. Usually interest rates move up or down depending on growth and inflation. Higher growth and inflation normally mean higher rates, and lower growth means lower rates. Those were the good old days when things were normal. But now central bankers in the US, Japan, and Europe have pinned interest rates close to zero and promised to leave them there for years. Rates can't go lower, so some central bankers have decided to get creative. Normally central banks pay interest on the cash that banks deposit with them overnight. Not anymore. Some banks like the Swiss National Bank and the Danish National Bank have even created negative deposit rates. We now live in an upside down world. Money is effectively taxed (by central bankers, not representative governments!) to get people to spend instead of save.

These unconventional policies are generally good for big banks, governments, and borrowers (who doesn't like to borrow money for free?); but they are very bad for savers. Near-zero interest rates and heavily subsidized government lending programs help the banks to make money the old-fashioned way: borrow cheaply and lend at higher rates. They also help insolvent governments by allowing them to borrow at very low costs. The flip side is that near-zero rates punish savers, providing almost no income to pensioners and the elderly. Everyone who thought their life's savings might carry them through their retirement has to come up with a Plan B when rates are near zero.

In the bizarre world we now inhabit, central banks and governments try to induce consumers to spend to help the economy while they take money away from savers who would like to be able to profitably invest. Rather than inducing them to consume more, they are forcing them to spend less in order to make their savings last through their final years!

Savers and investors in the developed world are the guinea pigs in an unprecedented monetary experiment. There are clear winners and losers as prudent savers are called upon to bail out reckless borrowers. In the US, UK, Japan, and most of Europe, savers receive close to zero percent interest on their savings while they watch the price of gasoline, groceries, and rents go up. Standards of living are falling for many and economic growth is elusive. Today is a time of financial repression, where central banks keep interest rates below inflation. This means that the interest savers receive on their deposits cannot keep up with the rising cost of living. Big banks are bailed out and continue paying large bonuses while older savers are punished.

In the film A Few Good Men Jack Nicholson played Colonel Nathan Jessup. He was guilty of using an unconventional approach to discipline by ordering a Code Red, an extreme discipline method, on his soldiers. Colonel Jessup explained in court towards the end of the film that while his methods are grotesque and abnormal, they are necessary to preserve freedom. While central bank Code Red policies are unorthodox and distasteful, many economists believe they are necessary to kick-start the global economy and counteract the crushing burden of debt. David Zervos, chief market strategist at the investment bank Jeffries & Co., humorously observed that if Ben Bernanke, the Chairman of the United States Federal Reserve, could be honest with the public, he would paraphrase Colonel Jessup's speech:

You want the truth? You can't handle the truth! Son, we live in a world that has unfathomably intricate economies, and those economies and the banks that are at their center have to be guarded by men with complex models and printing presses. Who's gonna do it? You? You, Lieutenant Mauldin? Can you even begin to grasp the resources we have to use in order to maintain balance in a system on the brink?

I have a greater responsibility than you can possibly fathom! You weep for Savers and creditors, and you curse the central bankers and quantitative easing. You have that luxury. You have the luxury of not knowing what I know: that the destruction of savers with inflation and low rates, while tragic, probably saved lives. And my existence, while grotesque and incomprehensible to you, saves jobs and banks and businesses and whole economies!

You don't want the truth, because deep down in places you don't talk about at parties, you want me on that central bank! You need me on that Committee! Without our willingness to silently serve, deflation would come storming over our economic walls and wreak far worse havoc on an entire nation and the world. I will not let the 1930s and that devastating unemployment and loss of lives repeat themselves on my watch.

We use words like "full employment," "inflation," "stability." We use these words as the backbone of a life spent defending something. You use them as a punchline!

I have neither the time nor the inclination to explain myself to a man who rises and sleeps under the blanket of the very prosperity that I provide, and then questions the manner in which I provide it! I would rather you just say "Thank you," and go on your way.

Central bankers must hide the truth in order to do their job. We may dislike what they are doing, but if politicians want to avoid large-scale defaults, the world needs loose money and money printing.

Ben Bernanke and his colleagues worldwide have effectively issued and enforced a Code Red monetary policy. Their economic theories and experience told them it was the correct and necessary thing to do – in fact, they were convinced it was the only thing to do!

Chairman Ben Bernanke could not be further from Colonel Nathaniel Jessup, but they are both men on a mission. Colonel Jessup is maniacally obsessed with enforcing discipline on his base at Guantanamo. He has seen war and does not take it lightly. He is a tough Marine who would not hesitate to kill his enemies. He is not loved, but he's happy to be feared and respected. Ben Bernanke, by contrast, is a soft-spoken academic. You can't find anyone with anything bad to say about him personally. His story is inspiring. He grew up as one of the few Jews in the Southern town of Dillon, South Carolina; and through his natural genius and hard work, he was admitted to Harvard, where he graduated with distinction, and soon he embarked on a brilliant academic career at MIT and Princeton. Sometimes when Bernanke gives a speech, his voice cracks slightly, and it is certain he would much prefer to be writing academic papers or lecturing to a class of graduate students than dealing with large skeptical audiences of senators. But Bernanke is one of the world's experts on the Great Depression. He has learned from history and knows that too much debt can be lethal. He genuinely believes that, without Code Red-type policies, he would condemn America to a decade of breadlines and bankruptcies. He promised he would not let deflation and another Great Depression grip America. In his own way, he's our Colonel Jessup, standing on the wall fighting for us. And he gets too little respect.

Bernanke understands that the world has far too much debt that it can't pay back. Sadly, debt can only go away via: 1) defaults (and there are so many ways to default without having to actually use the word!), 2) paying down debt through economic growth, or 3) eroding the burden of debt through inflation or devaluations. In our grandparents' age, we would have seen defaults. But defaults are painful, and no one wants them. We've grown fat and comfortable. We don't like pain.

Growing our way out of our problems would be ideal, but it isn't an option. Economic growth is elusive everywhere we look. Central bankers are left with no other option but to create inflation and devalue their currencies.

No one wants to hear that we'll suffer from higher inflation. It is grotesque and not what central bankers are meant to do. But people can't handle the truth, and inflation is exactly what the central bankers are preparing for us. They're sparing some the pain of defaults while others bear the pain of low returns. But a world in which big banks and governments default is almost by definition a world of not just low but (sometimes steeply) negative returns. As we said in Endgame, we are left with no good choices, only choices that range from the merely very difficult to the downright disastrous. The global situation reminds us very much of Woody Allen's quote, "More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly." The choice now left to some countries is only between Disaster A and Disaster B.

Today's battle with deflation requires a constant vigilance and use of Code Red procedures. Unfortunately, just as in A Few Good Men, Code Reds are not standard operating procedures or conventional policies. Ben Bernanke, Mario Draghi, Haruhiko Kuroda, and other central bankers are manning their battle station using ugly means to get the job done. They are punishing savers, encouraging people to borrow more, providing lots of liquidity, and weakening their currencies.

This unprecedented global monetary experiment has only just begun, and every central bank is trying to get in on the act. It is a monetary arms race, and no one wants to be left behind. The Bank of England has devalued the pound to improve exports by allowing creeping inflation and keeping interest rates at zero. The Federal Reserve has tried to weaken the dollar in order to boost manufacturing and exports. The Bank of Japan, not to be outdone, is now trying to depreciate the yen. By weakening their currencies, they hope to boost their exports and get a leg up on their competitors. In the race to debase currencies, no one wins.

Emerging market countries like Brazil, Russia, Malaysia, and Indonesia will not sit idly by while developed central banks weaken their currencies. They are fighting to keep their currencies from appreciating. They are imposing taxes on investments and savings in their currencies. Countries are turning protectionist. The battles have only begun in what promises to be an enormous, ugly currency war. If the currency wars of the1930 and 1970s are any guide, we will see knife fights ahead. Governments will fight dirty, they will impose tariffs and restrictions and capital controls. It is already happening and we will see a lot more of it.

If only they were just armed with knives. We are reminded of that amusing scene in Raiders of the Lost Ark where Indiana Jones, confronted with a very large man wielding an even larger scimitar, simply pulls out his gun, shoots him, and walks away. Some central banks are better armed than others. Indeed, you might say that the four biggest central banks – the Fed, BOE, ECB, and BOJ – have nuclear arsenals. In a fight for national survival – which is what a crisis this major will feel like – will central bankers resort to the nuclear option; will they double down on Code Red policies? The conflict could get very messy for those in the neighborhood.

Providing more debt and more credit after a bust that was caused by too much credit is like suggesting whiskey after a hangover. Paradoxical as the cure may be, many economists and investors think that it is just what the doctor ordered. At the star-studded World Economic Forum retreat in Davos, Switzerland, the billionaire George Soros pointed out the contradiction policy makers now face. The global financial crisis happened because of too much debt and too much money floating around. However, according to many economists and investors, the solution may in fact be more money and more debt. As he said, "When a car is skidding, you first have to turn the wheel in the same direction as the skid to regain control because if you don't, then you have the car rolling over." Only after the global economy has recovered can the car begin to right itself. Before central banks can be responsible and conventional, they must first be irresponsible and unconventional.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The arsonists are now running the fire brigade. Central bankers contributed to the economic crisis the world now faces. They kept interest rates too low for too long. They fixated on controlling inflation, even as they stood by and watched investment banks party in an orgy of credit. Central bankers were completely incompetent and failed to see the Great Financial Crisis coming. They couldn't spot housing bubbles, and even when the crisis had started and banks were failing, they insisted that the banks they supervised were well regulated and healthy. They failed at their job and should have been fired. Yet governments now need central banks to erode the mountain of debt by printing money and creating inflation.

Investors should ask themselves: if central bankers couldn't manage conventional monetary policy well in the good times, what makes us think that they will be able to manage unconventional monetary policies in the bad times?

And if they don't do a perfect job of winding down condition Code Red, what will be the consequences?

Economists know that there are no free lunches. Creating tons of new money and credit out of thin air is not without cost. Massively increasing the size of a central bank's balance sheet is risky and stores up extremely difficult problems for the future. Central bank policies may succeed in creating growth, or they may fail. It is too soon to call the outcome, but what is clear (at least to us) is that the experiment is unlikely to end well.

The endgame for the current crisis is not difficult to foresee; in fact, it's already underway. Central banks think they can swell the size of their balance sheet, print money to finance government deficits, and keep rates at zero with no consequences. Bernanke and other bankers think they have the foresight to reverse their unconventional policies at the right time. They've been wrong in the past, and they will get the timing wrong in the future. They will keep interest rates too low for too long and cause inflation and bubbles in real estate, stock markets, and bonds. What they are doing will destroy savers who rely on interest payments and fixed coupons from their bonds. They will also harm lenders who have lent money and will never be repaid in devalued dollars, if they are repaid at all.

We are already seeing the unintended consequences of this Great Monetary Experiment. Many emerging market stock markets have skyrocketed, only to fall back to earth at the hint of an end to Code Red policies. Junk bonds and risky commercial mortgage-backed securities are offering investors the lowest rates they have ever seen. Investors are reaching for riskier and riskier investments to get some small return. They're picking up dimes in front of a steamroller. It is fun for a while, but the end is always ugly. Older people who are relying on pension funds to pay for their retirement are getting screwed (that is a technical economic term that we will define in detail later). In normal times, retirees could buy bonds and live on the coupons. Not anymore. Government bond yields are now trading below the level of inflation, guaranteeing that any investor who holds the bonds until maturity will lose money in real terms.

We live in extraordinary times.

When investors convince themselves central bankers have their backs, they feel encouraged to bid up prices for everything, accepting more risk with less return. Excesses and bubbles are not a mere side effect. As crazy as it seems, reckless investor behavior is, in fact, the planned objective. William McChesney Martin, one of the great heads of the Federal Reserve, said the job of a central banker was to take away the punch bowl before the party gets started. Now, central bankers are spiking the punch bowl with triple sec and absinthe and egging on the revelers to jump in the pool. One day the party of low rates and money printing will come to an end, and investors will make their way home from the party in the early hours of sunlight half dressed, with hangovers and thumping headaches.

The coming upheaval will affect everyone. No one will be spared the consequences – from savers who are planning for retirement to professional traders looking for opportunities to profit in financial markets. Inflation will eat away at savings; government bonds will be destroyed as a supposedly safe asset class; and assets that benefit from inflation and money printing will do well.

This book will provide a roadmap and a playbook for retail savers and professional traders alike. This book will shine a light on the path ahead. Code Red will explain in plain English complicated things like zero interest rate policies (ZIRP), nominal GDP targeting, quantitative easing, money printing, and currency wars. But much more importantly, it will explain how what is in store will affect your savings and offer insights on how to protect your wealth. Code Red will be an invaluable guide for the road ahead.

Code Red will be available on Amazon on Monday, Oct. 28. You can get it here.

I said at the beginning of the letter that central bankers had run right off the monetary-policy map into unexplored territory. But to be perfectly honest about it, we are all forever venturing into the unknown territory that we call the future. But we certainly do live in an unprecedented, absolutely extraordinary time. New inventions and technologies, global expansions and collapses, and amazing developments of all kinds arrive to challenge us every day. To thrive we must adapt!

Patrick Cox’s new Transformational Technology Alert is the best way I know of to stay up to speed on the tech advances with the greatest potential. How Patrick conducts his research is easy to understand. He investigates the latest science by reading journals and peer-reviewed studies, then gets in touch personally with the scientists and CEOs behind the biggest breakthroughs. He compares notes with his Rolodex of industry leaders and tech experts, and then writes up his findings. Wall Street firms pay many tens of thousands a year for research like this, so we’re lucky to have Patrick on our team. Besides, I think Patrick’s work is better. Click here to see the full story behind three tiny but highly promising companies that recently caught Patrick’s attention, and sign up for his new letter at the best rate you’ll see.

New York, Florida, Geneva, Saudi Arabia, and Canada

Jonathan and I have been in NYC this week doing media for Code Red. Tom Keene was very gracious with his comments –

I say this with immense respect, in that it is easy to do doom and gloom, and it is easy to write a book – what a world, it's terrible, we're all going to die. John Mauldin doesn't do that. He says here are the challenges. Here are the cautions. Now, what are you going to do about it? No one has a cautious view, and then gives you a constructive prescription like John Mauldin, and we welcome him now. Code Red.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Then there were interviews at Yahoo, the WSJ, Barron's, Reuters, Fox and more taping at Bloomberg. I did an earlier interview with Kim Parlee for BNN out of Toronto, which you can see here, and another fun, short piece with Paul Vigna at the WSJ.

While waiting in the WSJ green room, I got to meet Todd and father Jack Hoffman of the reality TV series Gold Rush, who were a hoot. I recognized the wild-eyed passion, that certain something that is about a half-bubble off dead center that I've seen in other gold miners and Texas oil wildcatters I have met over the years. We traded emails and pics, and I think it would be fun to follow up. Not exactly high-tech mining but high fun anyway.

I finish this letter from Dallas after flying back today. I will return to NYC November 12 for a one-day meeting. Then I'll fly down to be with my good friend Cliff Draughn at Ponte Vedra, Florida (south of Jacksonville), on November 14. You can find out more by going to Cliff's website at http://www.excelsia.com. And then it's back to NYC in early December (Dec. 3-6), and later that month I'll head to Geneva. In January I will visit sunny Saudi Arabia for the first time and am open to other speaking engagements in the region. I go from there to a speaking trip in late January that will take me through three cities in Western Canada (Vancouver, Edmonton, Regina), where the weather will be quite the opposite.

I came back to my rented apartment and almost immediately went to see how construction on the new place had gone while I was away. I am scheduled to move in three weeks from today, and I guess I was expecting to see more done. Yes, there were at least ten people there, painting and hammering away, but it is still a construction site. Don't panic, said Carol (the general contractor), "Everything is more or less on time. Just a few things here and there for me to worry about." I am so ready to move out of a rather small one-bedroom office with a very small closet and a single chair. It has been almost ten months since I have been able to have all the kids over and settle in for a day or evening. And have my "stuff" at hand, although I am learning that I can make do with a lot less than I have accumulated over the years. While I am not going to continue this minimalist lifestyle, I doubt I will ever again allow a lot of extra things to pile up.

It is time to hit the send button. I am actually going to be able to go out on a Friday night! Another season for the Dallas Mavericks is beginning, and I want to go and see what Mark Cuban has in store for me. I have been a season ticket holder for 30 years and have seen bull and bear markets in the team, but it has always been entertaining. I think NBA basketball is the most beautiful of sports. Even the guys we think of as average can do things that we mere mortals can never hope to aspire to. But it's sure fun to sit and watch. And my seats are better now than 30 years ago, when I was literally on the very top row in the corner. I think they were something like $2. Good thing there's been no inflation since 1982.

Have a great week and make sure you have some fun here and there. Life was made for a little fun every now and then.

Your wondering about the reviews analyst (even though I know I should never read them!),

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.