The Giant Debt Problem Everyone Is Missing

-

Patrick Watson

Patrick Watson

- |

- May 21, 2024

- |

- Comments

Patrick Watson

Patrick WatsonThe US Treasury borrows staggering amounts of money. It’s basically a huge bet that future tax revenue will suffice to pay off the loans.

A good bet? No one knows. Tax revenue is a function of both policy choices and economic growth. The economy is in good shape now but may not remain so. Recessions aren’t the only risk; years of sub-par GDP growth (a distinct possibility) can have the same effect over time.

It gets worse. I think those who worry about the debt are probably not worried enough.

A giant new risk is brewing, one that could generate gargantuan new expenses for the government on top of everything we already expect.

What is this risk? You may be inside it right now.

Source: Pixabay

Unprofitable States

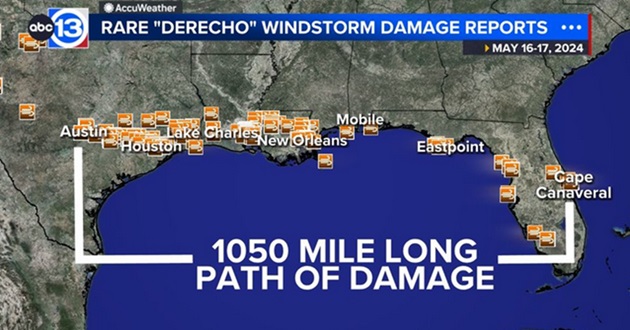

People along the Gulf Coast are cleaning up from a May 16 “derecho” windstorm. It killed at least 7 and left hundreds of thousands without power along a 1,050 mile path from Central Texas to Cape Canaveral, Florida. AccuWeather estimates $5 billion in physical damage for Houston alone.

Fortunately for residents and businesses, insurance will pay to repair much of the damage… this time. The bigger question is whether the insurers will be around next time.

Source: ABC13

Like what you're reading?

Get this free newsletter in your inbox regularly on Tuesdays! Read our privacy policy here.

Property and casualty (“P&C”) insurers agree to pay for damage to your property because, behind the scenes, they’ve calculated the risk you and other customers will file claims. Then they set everyone’s premiums to a level that covers the expected claims cost.

If the premiums aren’t enough, companies also have reserves and reinsurance. Those have limits. So, insurers also control their risk by not selling insurance in places they deem too risky.

This is increasingly common, and not just in disaster-prone coastal areas.

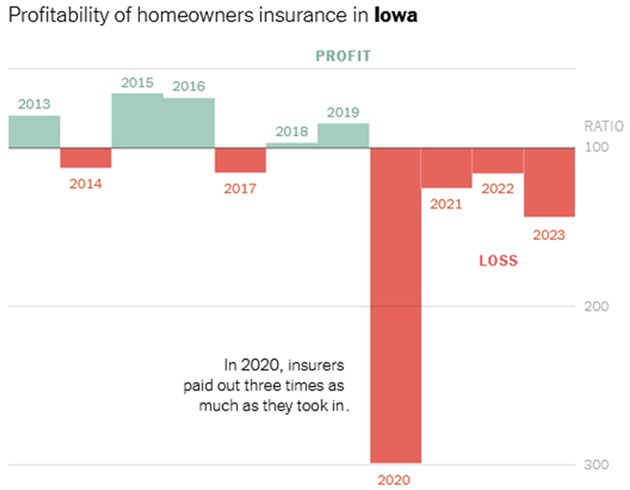

Iowa, for example, might seem like a pretty safe place. Until recently, big disasters there were rare enough to make Iowa a profitable market for P&C insurers. Not anymore.

Insurance rater AM Best uses a “direct combined ratio” to assess profitability. It shows homeowners insurance has been a losing proposition for Iowa insurers every year since 2020.

Source: The New York Times

Iowa was hit especially hard in 2020, when storm damage wiped out many years of profits. The next three years were better, but still showed bigger losses than anything seen from 2013‒2019.

It’s not just Iowa. Last year, insurers lost money on homeowners coverage in 18 states. The number of unprofitable states seems to be growing, too.

Source: The New York Times

A single bad year now and then is manageable. A string of unprofitable years in the same state, like the last four in Iowa (or 8 of the last 10 in Colorado), makes insurers wonder if they should keep doing business there.

For example, Bill Montgomery, CEO of Celina Insurance Group, pulled his company out of Iowa last year. He told The New York Times, “We can’t raise rates fast enough or high enough.”

The same is happening elsewhere. Why? It’s a combination of problems. Climate change is producing more erratic weather, construction costs are rising, people are building more homes in hazardous areas, and local regulations often prevent companies from charging enough to cover their risks.

Like what you're reading?

Get this free newsletter in your inbox regularly on Tuesdays! Read our privacy policy here.

This is a problem for homeowners, who increasingly must turn to last-resort, state-sponsored risk pools. But those pools face the same challenges as private insurers.

That’s where it becomes everyone’s problem.

When the private sector can’t profitably provide an essential public service, that service usually falls on the government. In fact, that’s almost the definition of government. It exists to do important and necessary things that aren’t always profitable.

In the US, when an essential service’s cost is greater than states can handle on their own, it falls on the federal government.

|

Homeowners insurance is definitely essential, not just for homeowners but for their lenders, too. Loan agreements usually require homeowners to carry insurance. But if they can’t get it and a disaster destroys the home, then what?

This has economic consequences. If you can’t insure a home at reasonable rates, lenders won’t make a loan for anyone to buy it. Imagine how far home prices will drop if that becomes widespread.

Where we are headed, I suspect, is a federal takeover of the homeowners insurance industry before it disappears completely. All that risk and claims cost will fall on Washington.

Congress will hate doing this, but the only alternative will be a housing market collapse even bigger than 2008. This isn’t some far-off threat. I’d bet it happens within a decade.

The numbers are overwhelming. According to Redfin, the total value of US homes was $47.5 trillion last year. Total mortgage debt is about $20 trillion. And we haven’t even talked about commercial buildings, whose owners face the same insurance problems. That could be an even bigger issue.

Worst of all, even Congress has no magic way to reduce the underlying costs. It just has deeper pockets to cover the losses, which will continue and likely grow.

Like what you're reading?

Get this free newsletter in your inbox regularly on Tuesdays! Read our privacy policy here.

If underwriting P&C insurance becomes a federal obligation, and disaster risk keeps increasing as it has been, our already-giant federal debt burden will get much, much worse.

See you at the top,

Patrick Watson

@PatrickW

P.S. If you like my letters, you’ll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.