When China Stopped Acting Chinese

-

John Mauldin

John Mauldin

- |

- July 31, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinA Transformation Like No Other

China GDP Versus China Beige Book

Economic Stimulus, Like It or Not

Insanely Leveraged Farmers

The Plunge Protection Team – Chinese-Style

The Silver Lining

New York, Maine, New York, and Boston

“The one thing I know for sure about China is, I will never know China. It's too big, too old, too diverse, too deep. There's simply not enough time.”

– Anthony Bourdain, Parts Unknown

Much of the world is focused on what is happening in Greece and Europe. A lot of people are paying attention to the Middle East and geopolitics. These are significant concerns, for sure; but what has been happening in China the past few months has more far-reaching global investment implications than Europe or the Middle East do. Most people are aware of the amazing run-up in the Shanghai stock index and the recent “crash.” The government intervened and for a time has halted the rapid drop in the markets.

There have been a number of concerns about what this means for the Chinese economy. Is China getting ready to implode? Certainly there are those who have been predicting that outcome for some time. In this week’s letter I am going to try to explain both what caused the Chinese stock market to rise so precipitously and then fall just as fast and why we have to view China’s stock market differently from its economy.

As I have been saying for several years, in order for the Chinese economy to continue to grow, the Chinese must shift their emphasis from industrial production and infrastructure investment to a services-oriented economy. That is indeed what they are trying to do, and we are beginning to see signs of the services sector taking on a role as important to the Chinese economy as services are to the US economy. They have a long way to go, but they have begun the trip.

A Transformation Like No Other

When the US stock market crashed in October 1987, commentators on that era’s primitive financial media (I recall seeing them on the large wooden box in my living room) rushed to distinguish between the country’s economy and its stock market.

The American economy, they said, is just fine. Life will go on, and businesses will make money. As it turned out, that was good analysis – and it still is today – and not just for the United States. Stock markets do reflect the economy over time, but they can lead it or lag it for years.

Anyone who owns China stocks has probably sought solace in such thinking the last few weeks. The Chinese stock bubble is deflating in spectacular fashion. The sharp decline and Beijing’s flailing efforts to stabilize the market have many economists seeing deeper trouble.

We’ll compare and contrast the Chinese stock market and economy by looking at an unusual but very reliable data source. With apologies to Anthony Bourdain, whom I quoted at the beginning of the letter, we can know China. We just have to ask the right people the right questions.

Back in 1987, as American investors were licking their wounds, the Shanghai skyline looked like this:

Here is a 2013 view from the same spot:

Photo credit: Carlos Barria, Reuters

A lot can change in 26 years. Transformations like this are commonplace in China. Gleaming cities now tower over what was undeveloped land a decade or two ago. Most of those cities even have people living in them, although the ghost cities are legendary.

You can crunch any numbers you like in any way you like, and it will be clear that China’s rapid growth is unprecedented. It is changing the course of human history. China has moved more than 250 million people from living a medieval lifestyle in the country to living and working in these fabulous new cities. And they have built the infrastructure to connect and supply them.

Worth Wray and I explored China from many different perspectives in our e-book, A Great Leap Forward? Our all-star cast of China experts variously see both opportunity and risk. The book is getting rave reviews. If you’re interested in an in-depth analysis of China, it’s the place to start (Click here for more information and to order the book.)

In thinking about China last week, I skimmed through the book and noticed something that, with the benefit of hindsight, is simply stunning. The paragraphs I read brought all the pieces together to explain the Chinese stock market’s epic drawdown.

China GDP Versus China Beige Book

The part that made me sit up straight was in the contribution by Leland Miller of China Beige Book. His chapter “How Private Data Can Demystify the Chinese Economy” comes at the Chinese economy from a unique angle.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We all know government economic data isn’t always reliable. That is especially true in China. It is the only country in the world that can report its GDP quarter after quarter and never have to revise its calculations. That is just the most obvious of its economic data manipulations.

Even knowing that, most China analysts still rely on that GDP number, because it is all they have. That is beginning to change because of the work of Leland Miller. Leland, along with his colleague Craig Charney, decided to build an alternative analysis to government GDP numbers. Using the same methodology that the Federal Reserve uses in its quarterly Beige Book, they gather data from a network of observers all over China. Their clients – who include the world’s largest central banks – provide granular data that gives a much deeper view of the Chinese economy.

In A Great Leap Forward? Leland describes how China Beige Book picked up on a major change in Chinese businesses. He says the country’s 2014 slowdown was different.

The slowdown of 2013 was the result of subtle credit tightening, few signs of which were evident in official data right up until the June interbank credit crunch caused a market panic. Small and medium-sized companies during that period still wanted to access credit but found – TSF data notwithstanding – that it was difficult if not impossible to do so. 2014, intriguingly, has proven to be a very different story.

One of the most interesting dynamics we’ve tracked across corporate China has been the historical disconnect between company performance and the willingness of those companies to continue to borrow and spend. In many sectors, particularly troubled ones such as mining and property, firms typically reacted to poor results in a peculiarly Chinese way: they doubled down.

Too often, the thinking appeared to be: good results were good, but bad results were not necessarily bad, because the government was expected to step in and bail them out. Perhaps with subsidies, perhaps by ordering loans to be rolled over to another day. Firms often chose to act in demonstrably non-commercial ways.

Since early 2014, however, our data suggest a startling transformation. During the second quarter, CBB data showed a particularly broad deceleration in revenue growth nationwide: for the first time in our survey, not one sector showed on-quarter improvement. Yet firms reacted to this slowdown in a surprisingly rational way: capital expenditure growth fell broadly, as did capex expectations, as did loan demand – all to the lowest levels in the history of our survey. The third quarter then showed yet another quarter of weak loan demand, with even lower levels of current and expected capex.

Firms watching the economic slowdown didn’t want to spend – and they didn’t want to borrow either. For the time being, they preferred to watch events unfold from the sidelines.

Leland says, and I agree, that this was a positive development. Both businesses and investors need the discipline of free markets. Experiencing failure forces everyone to learn what works and what doesn’t work.

In a phone call this week, Leland told me their data actually pinpointed this change in the second quarter of 2014. He thinks it was the most important single quarter in Chinese economic history. I’m sure that Leland, as an Oxford-educated China historian, doesn’t say that lightly. It was in that quarter, Leland thinks, that Chinese business leaders “stopped acting Chinese.” Faced with falling demand, they did the rational thing and stopped adding new capacity. As he says in the excerpt above, they didn’t want to spend or borrow. They just sat on the sidelines. That was a good business decision. Unfortunately, it wasn’t consistent with Beijing’s master plan.

Economic Stimulus, Like It or Not

At the end of his chapter, Leland appended the executive summary from the December 2014 China Beige Book. A prime question was whether the Chinese economy would slow down enough to elicit more stimulus from the government.

Our finding of no 2014 deflation will likely be challenged in 2015. There has been continuous disinflation since the first quarter of 2013, with sales prices, wages, and input costs still increasing, but more slowly. While outright deflation has not set in, the impact of the collapse of crude oil prices has yet to be felt. Deflationary concerns are now justified.

These deflationary headwinds could prove too tempting an opening for Beijing to resist strong stimulus. To now, despite all the talk of stimulus, CBB data show clearly that the cost of capital has risen since Q2 2014. Moreover, our data continue to show steady performance in both firm profits and the labor market, confirming that the real economy does not need the extra juice.

This next paragraph is critical. He underlined the first sentence and I added boldface to some key words.

Yet the more critical issue is this: if large-scale stimulus is nonetheless attempted, it will not work as intended. Firms have not been interested in borrowing or spending on new projects for a year now. What they might be willing to do, if enough credit is made available, is jump into China’s suddenly frenzied stock markets. Stocks have already seen strong investment inflows, some of it redirected from the floundering construction sector. If falling oil prices and the threat of deflation lead monetary authorities to try strong easing measures, the main result will likely be out-of-control prices for equities.

Which is exactly what happened. And stock-buying companies were accompanied by a horde of new individual investors. Remember, this is what Leland wrote last December. Beijing did add large-scale stimulus in the following months, and it didn’t have the desired effect of increasing business investment. It went instead into the stock market, where it created out-of-control prices.

You can see exactly how out of control prices got in the chart below. The Shanghai Composite Index had a great year in 2014, rising more than 50%, but it really took off this year. (Chart through yesterday.)

Perhaps not coincidentally, the Chinese central bank cut interest rates in November 2014 and reduced the bank’s reserve requirement in April 2015. Both moves sent China stocks into overdrive. Thanks to China’s capital controls, all the new money had to stay in the country. It had nowhere to go but stocks. Presto, instant bull market.

Leland and his team at China Beige Book predicted exactly this scenario if Beijing tried to stimulate businesses that had no use for liquidity. The results are obvious.

This year’s rising stock prices had virtually nothing to do with China’s real economy – which the latest China Beige Book data shows to be on the mend. Stocks rose simply because money poured into the market from all directions.

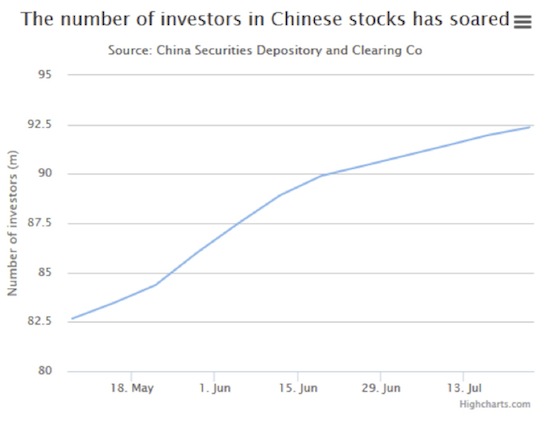

Along with businesses with established credit lines, small retail investors have plunged into the Chinese markets. The growth in the number of investment accounts has been nothing short of phenomenal, as the chart below demonstrates.

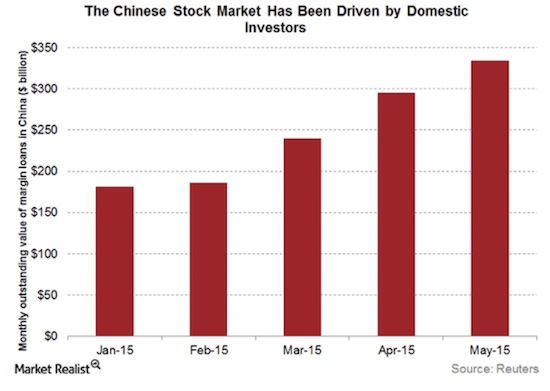

Investors both large and small bought stocks with huge amounts of borrowed money. China’s “shadow banking” sector came into its own in 2014 as companies like Tencent and Alibaba funded new online banks. The chart below shows the more or less official margin in Chinese stocks, which has essentially doubled in five months.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

China has very much needed the shadow banks. In China, credit was for large banks, big companies, and politically favored businesses. Small businesses and individuals could not borrow money on reasonable terms. The shadow banks thus found instant success.

Unfortunately, many shadow bank customers had little experience with debt, so they borrowed too much and used the money unwisely. To some degree, individuals displayed the same “double-down” behavior Chinese businesses had recently abandoned. Thinking the government would protect them, they plunged into the stock market.

In theory, Chinese investors should only have been able to borrow 50% of their stock purchases using margin loans. In practice, they piled loan on top of loan on top of loan, creating giant mountains of debt. It is not unlike what Chinese investors both large and small did several years ago in pyramiding their purchases of copper and other metals.

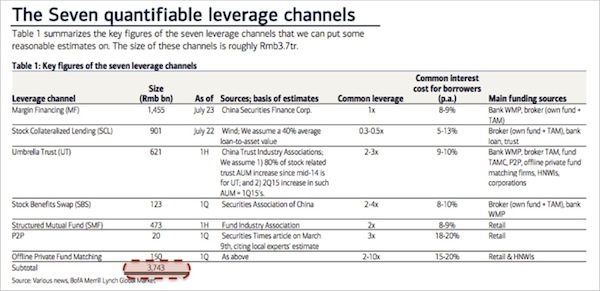

Estimates vary widely as to how much cash found its way into the stock market. This chart from Bank of America/Merrill Lynch (via David Stockman) outlines the leverage they believe went into Chinese stocks this year.

If this is right, something like 3.7 trillion RMB of borrowed money hit the stock market. That’s about a third of the free float in China A-shares. With that much leverage, it is no surprise the market exploded higher — before it just exploded.

My good friend Doug Kass shared this remarkable CNBC clip about a rural farmer who bought $1 million in stocks at an incredible 6x leverage. You can probably guess how it ends, but you might want to watch the story anyway. The poor farmer in the video was sold out of his positions, and he now owes the brokerage company more than his original investment.

Anyone who reads this letter knows that investing everything you have and then borrowing six times more money that you don’t have to throw it all into a single stock is a really bad idea. Apparently, this is not so obvious to Chinese farmers.

Chinese investors are basically momentum players. Combine that approach with the well-known Chinese predisposition toward gambling and you get an explosive mix. I was on the phone this morning with my old friend Jack Rivkin (who is now the new CEO of Altegris), talking about his experiences in China. He told me two fabulous stories. Rather than trying to retell them myself, I asked him to shoot an email to me so that you could get it straight from the source:

In major cities in modern China there is a multi-story bookstore on every fifth corner. The first floor is almost always stacked with the following mix:

Half the floor is filled with the equivalent of Mobil guides, showing the latest version of the road maps for various parts of the country including the location of rest stops and restaurants. These change monthly as, in spite of the “slowdown” there, roads are still being constructed at a rapid pace – rapid enough to call for new maps quite often. The other half of the store has two adjacent and, at times, commingled sections. The most significant section, in Chinese and other languages, has books on numbers – their importance in quotidian living and how one would go about picking lucky numbers for various lotteries and other gambling activities. That section, I am told, gets a lot of traffic when there is a group planning a trip to Macau.

The other quarter consists of books on “investing” – many in English. Based on the titles I saw, some of these would appear interchangeable with those in the numbers section. Gambling seems to be in the DNA, and the Chinese approach to the stock market would certainly seem to fall into that category. Much as the Chinese in Macau increase their bets as a hot streak progresses, the same appears to apply to the stock market. Of course, there is a segment of “investors” in the US market who might also fall into that category. But at this stage in the development of capital markets in China, the percentage would seem to be much higher there. Classic growing pains in a less-than-mature capital market, but as with everything in China, it does go to extremes. The Chinese government seems to want equities to rise. They may not yet have gotten it quite right on how to do that; but with lots of volatility, at some point they may succeed. Could be painful between now and then. [It’s] a little tough already when they haven’t opened almost 20% of the [stocks] for several days.

The second story has to do with the changing mix of the Chinese economy. I did a webinar yesterday with Henry McVey and David McNellis, who run the Global Macro Asset Allocation process for KKR. They had a more sanguine view of China’s growth than the consensus, for sure. When I questioned Henry on this view, he said that people were overlooking the amazing growth of the Chinese services sector. He agrees with the major, major slowdown in fixed asset investment; but the services sector, which in many ways relates to internal elements of the China story and the consumer, is quite robust. They have a very specific window on this as investors in several service sectors in the country. It was not a story that I had previously heard spelled out so specifically. It’s not that there won’t be some hiccups or worse, but there is a transformation occurring underneath all this turmoil. It may mean slower growth in the long run, but with China following the path of the now-developed economies from agrarian to industrial to services. I am paying attention.

The Plunge Protection Team – Chinese-Style

Keeping the masses content is one of Beijing’s top priorities. Stories of farmers losing everything in a mining stock are not helpful in that regard, but I thought the farmer’s fruitless trip to ask regulators for help was a nice touch.

In fact, the government was already frantically throwing everything it had into propping up the stock market – and everything they’ve done still hasn’t been enough. China’s leaders thought their version of the “plunge protection team” could keep the stock market afloat. Right now, they are learning it isn’t so easy.

Among the first things they did was to ban short trading and put together a syndicate of brokerage firms to buy stocks. They essentially bought massive amounts of Chinese ETFs and pledged that they would not sell those shares until the market went above 4500. That approach creates massive convexity, synthetic shorts and puts, and game-playing potential that is way beyond the sophistication of most US investors, let alone what are essentially Chinese rookie investors and regulators.

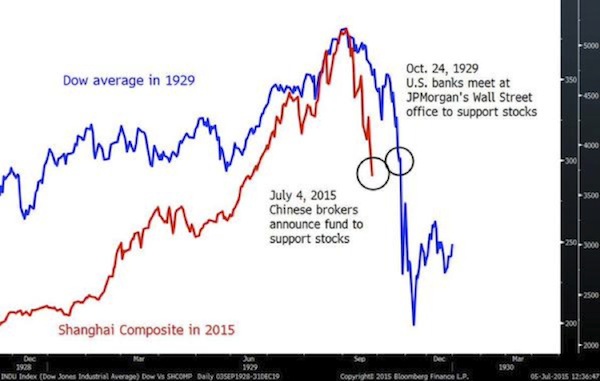

While not a clear parallel, on October 24, 1929, a number of the biggest investment banks in the US met at JP Morgan’s Wall Street bank and declared a syndicate to support stocks. You can see from the chart below how that worked out. Superimposed on that is a chart of the Chinese stock market (hat tip Murat Köprülü). I realize there is a difference between the regulatory and market climates in 1929 US and today’s China, but trying to monkey around with the market is generally a bad idea.

We are reading a story today from Reuters that the Chinese regulator is asking brokers in Singapore and Hong Kong to turn over their stock-trading records, as China is pursuing investors who are short selling. Ostensibly, the objective is to go after individuals and funds that “naked short” (a practice that I personally think should be patently illegal), but asking for records from brokerage firms in countries outside your regulatory structure is unusual. The story implied that the brokerages would cooperate.

The Chinese also essentially suspended trading in over 50% of their stocks for a time in July, although it appears that some 80% of stocks are trading now. I suppose they’re letting them trade on the basis that if the price of a stock can’t drop then there won’t be losses.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

It’s not clear how the Chinese markets will eventually respond, but my suspicion is that they will end up lower. And in the meantime the authorities will continue to try to manipulate the market and to delay, only to find out that once you let multiple millions of individuals into a market, it is going to have a mind of its own.

As painful as it is, this stock crash will make China stronger in the end – if the government takes the right lesson from it.

What we see in China is something like the “moral hazard” that was much discussed over here in the States during the 2008–2009 financial crisis. Would government bailouts send the wrong signal to banks, businesses, homeowners, and investors? When you know the government has your back, you are naturally prone to take unwise risks.

If that’s the case here in the US, imagine how much more intense the phenomenon must be in a communist society where the government keeps a tight grip on the economy. Of course people expect the government to save them. After all, the regime has always claimed to be their savior. People know nothing else.

Leland says his greatest fear is that the government will continue trying to boost the economy with artificial measures. This intervention will send unrealistic messages, and people will keep expecting help from the state. If that happens, China is setting itself up for an even greater collapse at some point. The nation will learn only after a very hard landing that could set progress back by decades.

What is the best-case scenario? Here is how Leland describes it in A Great Leap Forward?

In a best-case scenario, China will continue to slow over time – in the healthiest and most orderly way possible. Beijing will attack its system of financial repression, which sucks capital out of the pockets of households in order to subsidize state corporates; resist the urge for further mass stimulus; combat overcapacity by allowing insolvent firms to go bankrupt; permit financial products to default; and, most important, fix a broken credit transmission mechanism that has left some sectors of the economy bereft of capital despite the largest credit expansion in world history.

A year ago, I wrote that Beijing under the leadership of President Xi Jinping was going in exactly that direction. Now I’m not so sure. Beijing’s stimulus efforts created the stock market bubble; now their unsuccessful efforts to keep it from bursting are shaking my confidence in their desire to allow market forces to play a greater role in the transition from a top-down society to a consumer-driven, bottom-up society.

Still, I’ve learned not to underestimate the Chinese leadership. They make mistakes but usually recognize them and change course quickly. We’ll see what they learn from their current misadventures in stimulus and their attempts at top-down control of an essentially uncontrollable market. If they don’t learn the right lessons, China will face an even harder lesson in the future.

Regardless, we have to remember that Chinese stock prices, whatever they do, have very little to do with economic fundamentals. China Beige Book’s latest data show improvement in most indicators this year, consistent with continued, albeit slower growth.

(If you or your clients have China exposure, I highly recommend China Beige Book’s research. It is unlike whatever else you may have now. Visit the China Beige Book website to learn more. Full disclosure: I am on the China Beige Book advisory board.)

For those who want further information on China, I would direct you to two speeches that were given at my Strategic Investment Conference, one by Louis Gave and the other by Michael Pettis, Peking University professor and true expert on China. These are among a number of speeches available through my friends at Altegris Investments. You can click on this link and register to see those and other speeches.

New York, Maine, New York, and Boston

I fly to New York on Tuesday with my youngest son, Trey. I will have dinner with Art Cashin, Jack Rivkin, and a few of the other usual suspects, along with some new friends whom Danielle Dimartino has invited. Danielle recently retired from the Dallas Fed, where she was Richard Fisher’s personal research associate and helped him craft some of those wonderful speeches he gives. Now that she can “go public,” I predict you will be hearing a lot more from her.

On Thursday we fly to Bangor and then on to Leen’s Lodge at Grand Lake Stream, Maine. I will be there with about 50 economists analysts, and other friends for three days of fishing, talking investments, and partaking of fabulous food and wine. It’s a bit of a rustic venue, but the views are fabulous.

We return on Monday, and I will turn around and fly to Vancouver and then on to Whistler, British Columbia, to spend a few days with Louis Gave and his team. I then return home for a week before heading back to New York and Boston for a little vacation, mixed in with meetings, of course. I will be spending the weekend with Jack Rivkin at his home in the Hampshires. I am told I can take a ferry to Rhode Island and then a train up to Boston, where I will then have to figure out how to get to Gloucester to spend a few days with Dr. Woody Brock. Woody has been a bit under the weather but tells me that he’s fully recovered, and I look forward to what are always some of the most fascinating and wide-ranging discussions I have anywhere. Truth be told, hanging out with Woody is like talking as a young student with a wise old professor, although I no longer qualify as a young student. And I may be older than Woody.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Then I will return to Boston to be with Stevie Cucchiaro, the brilliant founder of Windhaven, who is now in retirement and has offered us a few days on his new racing catamaran. Stevie is a world-class sailor who competes at the highest levels of yachting. He has promised me there will be smooth sailing when I am on his latest purchase, which is just now going through its final stages of vetting.

I’m not sure yet what we will do after that. I have lots of places I need to be and people I need to talk to and work to do and lots of reading, not to mention that I’m working a lot on my new book.

Sunday the family is gathering for brunch. For a variety of reasons, everyone has been in different places, and I just haven’t had a Sunday brunch with the kids in what seems like forever. I’m going to go ahead and hit the send button and take the rest of the evening off. I think I will read a little science fiction that has no socially redeeming value other than it is just great writing and tons of fun. Have a great week!

Your ready for a relaxing August analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.