Volatile Year Coming

-

John Mauldin

John Mauldin

- |

- August 30, 2019

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinSupply Shocks Ahead

Subnormal Growth

Bond Market Insanity

Paralyzed Business

Bumpy Ride

Florida and a Fire Drill

We have reached Labor Day weekend which, in the US, is a holiday for honoring work and workers. If you’re a Baby Boomer like me, you also grew up knowing school was about to start again. We didn’t do the mid-August thing back then. The first day of school was the day after Labor Day. That meant entering a new grade with unknown challenges.

As adults we do the same in our work—and managing your investments counts as “work.” So today I want to talk about the coming year’s class schedule. We face some tough subjects, and if we get through them, it may mean we get to go on to yet another year with even tougher ones.

I think the last few weeks marked a turning point in the economic narrative. It’s more than the trade war. A sense of vulnerability is replacing the previous confidence—and with good reason. We are vulnerable, and we’ll be lucky to get through the 2020s without major damage.

But that’s getting ahead of ourselves. Let’s talk about the risks facing us in the next year or so and the economic environment in which we will face those risks. I think that environment is one of potential supply shocks, subpar growth, and increasing volatility… among other things.

Supply Shocks Ahead

For some reason, NYU professor and economist Nouriel Roubini is often called “Dr. Doom.” He and I have been friends over the years, and I got to know him pretty well when Shane and I randomly rented an Airbnb in the same NYC building where he had a penthouse apartment. He was gracious with his time and we had more than a few late-night talks in which I felt no sense of doom. But he is indeed currently bearish on the economy.

Nouriel explained his outlook in a recent Project Syndicate piece, The Anatomy of the Coming Recession. To summarize, at a time when the world economy is already slowing for cyclical reasons, we also face three potential shocks, any one of which could trigger a recession.

- The US-China trade and currency war

- A slower-brewing US-China technology cold war (which could have much larger long-term implications)

- Tension with Iran that could threaten Middle East oil exports

The first of those seems to be getting worse. The second is getting no better. I consider the third one unlikely, because neither the US nor Iran would benefit from military conflict. But someone could miscalculate.

In any case, unlike 2008, which was primarily a demand shock, these threaten the supply of various goods. They would reduce output and thus raise prices for raw materials, intermediate goods, and/or finished consumer products. Hence, Roubini thinks the effect would be stagflationary, similar to the 1970s.

Because these are supply and not demand shocks, if Nouriel is right, the kind of fiscal and monetary policies employed in 2008 will be less effective this time, and possibly harmful. Interest rate cuts could aggravate price inflation instead of stimulating growth. That, in turn, would probably reduce consumer spending, which for now is the only thing standing between us and recession.

Speaking of consumer spending, more than a few analysts take great comfort in its resilience. They have a point, but much of this spending is being fueled by debt instead of rising incomes. So, at the macro level, the solution to one problem is adding to another one. Let’s turn to debt expert Dr. Lacy Hunt who, for somewhat different reasons, is as bearish as Roubini.

Subnormal Growth

Most of our problems relate, in one way or another, to debt. Possibly you are among the small minority that is debt-free but collectively, we have way too much of it. And even if you aren’t a debtor, simply having a bank account makes you a lender. And being a citizen of the city, county, state, or country creates its own set of expectations and obligations as far as debt is concerned. This matters to everyone.

Debt isn’t bad and may even be good if it is used productively. Much of it isn’t. In theory, an economy overloaded with unproductive debt should see rising interest rates due to the excess risk it is taking. Yet we are in a low and falling-rate world. Why?

Lacy Hunt explained it well at the Strategic Investment Conference last May. I summarized his two theorems in a letter soon afterward. He showed how government debt accelerations depress business conditions. This reduces economic growth, so rates fall. The data show the amount of GDP each dollar of new debt generates has been steadily declining.

This is a problem because, among other reasons, central banks still think lower rates are the solution to our problems. So does President Trump. They are all sadly mistaken, but remain intent on pushing rates closer to zero and then below. This is not going to have the desired effect.

Here’s how Lacy explained it in his latest quarterly letter (my emphasis in bold).

In a normal cyclical setting, we might assume that lower real yields could boost economic growth, but under current conditions lower real yields may, in fact, merely reflect that returns on capital have declined significantly. When real yields are low or negative, investors and entrepreneurs will not earn returns in real terms commensurate with the risk. Accordingly, the funds for physical investment will fall, and productivity gains will continue to erode as will growth prospects.

On average, over the past 10 years, real 10-year government bond yields have been slightly negative in the UK and Japan and positive by a mere 10 basis points in Germany. In the past five years, when nominal interest rates were slightly negative in Japan and Germany, real yields were even more negative since modest inflation continued. In each of these cases, negative real rates have been no panacea for the growth problems. Indeed, the span of sustained poor economic performance has increased.

Now, evidence has emerged that the US real rate, while still positive, is declining and that investors here are being forced to accept lower real yields similar to investors in foreign markets. The implication: Decreased capital returns will prolong the period of poor economic growth in the United States, as has been the case in Japan and Europe. If the solution to the subnormal growth is an even faster acceleration in debt, then this cycle will continue to repeat.

(Incidentally, Over My Shoulder members can read Lacy’s full report with a summary and key points highlighted here. Not a member? Click here to join us. It is the best economic analysis bargain anywhere. You get valuable research curated by me and my team delivered to you with handy summaries at a ridiculously low price. Again, join us.)

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

If Lacy is right, as I believe he is, the Federal Reserve is on track to do exactly the wrong thing by dropping rates further as the economy weakens. The Fed also did the wrong thing by hiking rates in 2018. They should have been slowly raising rates in 2013 and after. They waited too long, as I wrote both during and after that period. This long string of mistakes leaves policymakers with no good choices now.

The best thing they can do is nothing, but that’s apparently not on the menu. Hence, they could meet the recession their own policies helped generate with policies that make it even worse. And the politics surrounding interest rate cuts don’t make it any easier.

Bond Market Insanity

We now have $17 trillion worth of negative interest rate bonds, mostly in the sovereign bond space. That is about 25% of the entire bond market and 43% of bonds outside the US.

There has never been such an animal in the taxonomy of bonds. It is as odd as the Pushmi-Pullyu from the Dr. Dolittle children’s stories. Until a few years ago, traders and investors around the world would have considered negative rate bonds as fanciful as a children’s fairytale. It turns out black swans do exist after all. (I actually saw some swimming in a park in London.)

The German government can issue 30-year bonds at a -0.22 % interest rate. I do not want to embarrass them by quoting them directly, but some name-brand investment managers think negative rates are the market saying that the German government (and presumably others) haven’t borrowed enough money. Sigh…

Mark Grant (whom I will see in Florida next week) wrote this about negative interest rates in Europe:

While the European Union is not creating “Pixie Dust Money,” at the ECB, and then buying their own nations’ sovereign, and corporate debt, to purposefully hurt the financial markets, or the United States, that is exactly the “collateral damage,” that they are causing. The nations of the EU cannot afford to pay for their budgets, or their social programs, so the ECB has moved down their borrowing costs to less than zero, in most cases.

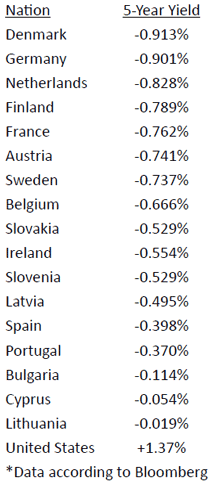

Check out their 5-year sovereign debt yields:

Yields in the United States, and the US economy, and the dollar, are taking it on the nose precisely, and specifically, because of what the European Union is doing. There is no other reason for what is happening here except that the nations of the EU have directed the ECB, the European Central Bank has “NO” independence, to make this “Money from Nothing” and then buy both sovereign and corporate bonds denominated in euros. Now their budgets can be afforded, as they can borrow at less than zero, so they do not have to pay anything for them.

In America when we say, “The Land of the Free,” it means one thing. When they say this in Europe, it means another thing entirely!!!

It is not just governments that can borrow at negative yields. Siemens AG, a German corporation, recently sold $3.9 billion worth of bonds at an average -0.3% and the offering was oversubscribed. Some investors (pension funds) were disappointed they couldn’t buy. Danish banks are selling home mortgages at a -0.5% interest rate. You read that right; they are paying homeowners to borrow money.

David Kotok wrote (in another essay that I sent to Over My Shoulder members):

Lastly, there is a developing body of research that estimates how much damage negative rates and even very low rates are doing. Torsten Slok has published a partial list of those papers. Essentially, negative-rate policies and very-low-rate policies eventually become counterproductive and act as contractionary forces. See Brunnermeier and Koby, “The reversal interest rate,” January 30, 2019. Also see NBER working paper 26040 by Sims and Wu, July 2019, entitled “Evaluating Central Banks’ Tool Kit: Past, Present, and Future”

Paralyzed Business

All this bears down on us as other things are changing, too. Many relate to shrinking world trade. Trump’s trade war hasn’t helped, but globalization was already reversing before he took office. Industrial automation and other technologies are killing the “wage arbitrage” that moved Western manufacturing to low-wage countries like China. Higher wages in those places are also reducing the advantage. This will continue.

Ideally, this process would have happened gradually and given everyone time to adapt. Trump and his Svengali-like trade advisor, Peter Navarro, want it now. I think the president’s recent demand that US companies leave China wasn’t a bluff. He wants that outcome, and he has the tools to attempt to force it. The only question is whether he will.

Many responses to last week’s Digging a Hole to China letter boiled down to, “China is bad and we have to do something.” I fully agree… but the fact that we must do something doesn’t make everything feasible or advisable. I’ve shown repeatedly how tariffs are a counterproductive bad idea. Severing supply chains built over decades in less than a few years is, if possible, an even worse idea. It will kill millions of US jobs as factories shut down for lack of components.

Some say this is just more Trump negotiating bluster. Maybe so, but the mere threat paralyzes business activity. CEOs and boards (I know this because I talk to board members and sit on several boards myself) don’t make major capital commitments without some kind of certainty on their costs and returns. The president is making that impossible for many.

It is not the case, as Trump seems to think, that China or other economies can collapse and the US proceed merrily along. Like it or not, we are all connected. If US companies want to export their products, they need other countries who can afford to buy them. That’s a growing problem anyway. We don’t need to make it worse.

Gavekal’s Andrew Batson recently wrote:

The closer the US presidential election gets, the less incentive China has to deliver Trump any reward for the trade war, and the more incentive it has to let him suffer the consequences. Falling stock markets, declining exports, and a weaker Chinese currency are arguably bigger political problems for Trump than they are for China’s leadership. After all, a slowdown to below 6% GDP growth would hardly be a disaster for China.

Europe is rapidly turning into a major problem, too. Negative interest rates there are symptoms of an underlying disease. Italy is already in recession. Germany suffered its first negative quarter and may enter “official” recession soon.

Germany is highly export-dependent. The entire euro currency project was arguably a plot to boost German exports, and it worked pretty well. But it boosted them too much, bankrupting countries like Greece which bought those exports. China, another big customer, is buying less as well. A German recession will have a global effect. Automobile sales are down and Brexit could mean further declines. That would most assuredly deliver a German and thus a Europe-wide recession. And it will affect US exports and jobs.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Then there’s Brexit. At this point we still don’t know if the UK and EU will reach terms, but there is some risk of a hard end to this drama. News focuses on the damage within the UK, but it will also affect the EU countries, mainly Germany, who trade with the UK. These supply chains are no less intricate and established than the US-China ones. Tearing them down and rebuilding them will take time and money. The transition costs will be significant.

Bumpy Ride

Remember when experts said to keep politics out of your investment strategy? We no longer have that choice. Political decisions and election results around the globe now have direct, immediate market consequences. Brexit is just one example.

A far bigger one is the looming 2020 US campaign. None of the possible outcomes are particularly good. I think the best we can hope for is continued gridlock. A Democratic Congress and White House would likely give us major spending and tax increases and possibly some form of MMT. A Trump re-election will mean four more years of volatility, probably far more intense than we have seen so far. Choose your poison.

But between now and November 2020, none of us will know the outcome. Instead, a never-ending stream of poll results will show one side or the other has the upper hand. That will generate high market volatility, inspiring politicians and central bankers to “do something” that will probably be the wrong thing.

Polls aren’t necessarily reliable, but that will be the only thing businesses and investors have to go on. And those polls will move markets in ways that we are simply not accustomed to. I expect 2020 to be one of the most volatile market years of my lifetime.

As noted above, if Roubini is right then rate cuts aren’t going to help. Nor will QE. Both are simply ways of encouraging more debt which Lacy Hunt’s work shows is no longer effective at stimulating growth. They are, however, effective at blowing up bubbles. The closer yields are to zero (or below), the more impossible it is for both small savers and giant institutions to reach their goals with fixed-income assets. They will have to take on more risk and it probably won’t end well for them.

But no matter who you are, you’re going to have a bumpy ride between now and next fall. Now is the time to get ready.

Florida and a Fire Drill

I had lots of phone calls and emails this past week from friends worrying about me being in Puerto Rico. It seems the news was all about Dorian coming to devastate us. And we did go through storm preparation. I spent Tuesday morning playing nine holes of golf with friends who had the day off for a storm preparation day. We made sure that we had the normal emergency supplies, plenty of fuel for the diesel generator, and so on. It turned out to be basically a fire drill, as the storm mostly missed Puerto Rico. We barely even got a puff of breeze and a few sprinkles. But at least we have all the essentials for next time.

Tuesday I fly to Miami, where Florida will likely be having its own hurricane preparation unless Dorian changes paths again. After an airport meeting with Jim Mellon to talk about biotech, I will meander up to Fort Lauderdale to meet Mark Grant and discuss the bond market. What’s an income investor to do? There are answers, just not easy ones like there used to be.

It’s the end of summer and Labor Day, but I always enjoy this time of year. As I said at the beginning of the letter, Labor Day still makes me feel like part of something new and changing. And in just four months, we’ll have a new decade and the new year. I hope to spend it with you, and thank you for taking time to read my musings. I do look forward to your feedback and my staff makes sure that I get to read all the emails and letters. So have a great week!

Your expecting a great deal of volatility analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.