No Soft Landings

-

John Mauldin

John Mauldin

- |

- June 3, 2022

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin“There’s no soft landing when you’re this far out of equilibrium.”

—Tom Hoenig

My last four letters featured highlights from the Strategic Investment Conference. I told you they would build toward a conclusion that might not be obvious. Today we’ll lift that final curtain.

Some of it is good news. Innovation will continue, technology will evolve, living standards will improve in many ways as the 2020s unfold. We had several sessions focused on technology and the future, which I have not written about. Positive things will happen in the background but our attention will be on a less pleasant foreground. News media rarely headline the amazing new technologies that will improve our lives. They focus on the negatives and crisis because that is what we humans read and they get paid by the number of clicks. Sad but true.

In the final panel we talked about what’s coming. No surprise, much depends on what the Federal Reserve and other central banks do. Trying to control the inflation that arose from their own past choices, they will try to tighten policy without going too far. Their history of making such “soft landings” is not impressive.

But the challenge is more than monetary. Fiscal authorities (legislatures and governmental authorities) had a hand in creating all this, too, and they must be part of any solution. Their history isn’t reassuring, either.

I have written before that we’ve reached a point where all the options are bad, but some are worse than others. People talk about the Fed scoring an economic “soft landing,” tightening just enough to control inflation, but not setting off a deep recession.

That would be nice. The chance that all the necessary pieces will line up that way? Somewhere between slim and none, and as my dad used to say, “Slim left town.” And while my memory isn’t perfect, I don’t believe any speaker at the conference believed in the possibility of a soft landing. And even if we get one, we have serious problems that predate this inflation. They haven’t gone anywhere.

But I’m getting ahead of myself. Let’s see what the SIC experts predict.

|

Uncover the foolproof investing strategy that rewards investors without worrying about market volatility. |

Start/Stop

I like to say conferences are my personal art form. I enjoy finding the right mix of speakers and arranging them into a thought-provoking agenda. The SIC closing panel is my artwork’s final touch. I assemble a “dream team” with different perspectives, not knowing exactly where it will go. Then I add a moderator and myself so someone can light the fuse. It’s always a fabulous ending to a fabulous event.

This year’s dream team was Tom Hoenig, former Kansas City Fed president; Bill White, former chief economist at the Bank of International Settlements; and Felix Zulauf, ace money manager and longtime Barron’s roundtable member, your humble analyst, with David Bahnsen ably moderating. The summary you’re about to read doesn’t capture the actual intensity and informative value of the final panel.

The discussion quickly went to one critical question—perhaps the critical question: How hard will the Fed fight inflation? Everything hinges on it. I hope and believe Jerome Powell will keep pushing until inflation drops below 3%. I don’t know how long that will take, and I fully expect the Fed will break some things trying to get there. That’s going to hurt but a 1970s rerun would be even worse. We have no good choices left.

That led to some follow-on questions: Will the Fed keep tightening, and what if it stops too soon? Here Tom Hoenig has a lot to say because he actually sat at the FOMC table for 20 years, through multiple crises. He’s seen how those discussions go. He knows many of the players and how they think. Here was his initial answer:

“I think that the FED will push until unemployment starts to rise too sharply in their opinion. If the unemployment rate starts to rise to 5% or more, I think that they will back off.

“Now, I hope that if they find themselves in that circumstance, they will pause and not reengage in quantitative easing or lower interest rates just to get us out of the slowdown that is inevitable, given where we're starting from with 8%‒8.5% inflation almost. And I think if you look at Powell's spring 2019 actions, when the market threw a liquidity tantrum in the reverse repo market and so forth, his inclination will be to step in. It will take a lot of discipline on his part and on the FOMC’s part to say, ‘Wait a minute, we may pause, but we're not going to stop. We're going to pause in terms of raising interest rates, but we're not going to reduce them and we're going to have to get through this. And yes, unemployment's going to be higher.’

“But if he doesn't do that and he starts to back away, then we're going to have the 1970s all over again. Start, stop, inflation goes up, then comes down, unemployment rises, therefore they back off. That's what you want to avoid and that's the danger going forward.”

A lot to unpack there. Tom noted the inevitable tension in the Fed’s mandate. It is supposed to pursue both price stability and full employment. The unemployment rate stands at 3.6% right now. If 5% is what the Fed considers too high, they still have room to act. (There are plenty of job openings, although this week’s ADT numbers showed small businesses significantly reducing their new hires, and some actually laying off workers.)

The Fed can put a damper on growth and see if inflation responds. That seems to be the plan right now. But if growth declines enough to create 5% unemployment, what do you think markets will be doing? It won’t be pretty. Between politicians yelling about lost jobs and investors upset about falling asset prices, the Fed will get heavy pressure to change course.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Tom Hoenig, having been there, pointed out the Fed has intermediate options. It can pause tightening without actually changing direction. That might be a reasonable choice, too. He said the danger comes if they look reactive. They can’t get into a start/stop pattern. They need to stamp out inflation first, then deal with the damage later. Whether they will do it that way remains to be seen.

Felix Zulauf was more pessimistic. He thinks the Powell Fed is quite different from the Volcker Fed, and not just because of the personalities. It’s a different situation and a different financial zeitgeist. He doesn’t think the Fed, or any other central bank can get away with imposing the kind of pain Volcker did and will stop as soon as this year.

Then Bill White, in his quiet, studious way, dropped the real bombshell.

“Back into Deflation”

David Bahnsen mentioned to Bill White that the Fed would be looking not only at unemployment and the stock market, but also the credit markets for signals. Bill agreed and noted the banks are weaker than many think. Then he said this:

“My real worry on the downside is that it may be that the fragilities are so great at the moment that a moderate degree of tightening will in fact spark a downturn of such a magnitude that even if the Fed does back off, that there's not much that can be done about it, that will have a downward momentum... that we really won't be able to handle.”

Whoa. During Bill White’s tenure at the BIS, he was remarkably correct in his analysis. He often went against the common narrative, one of the reasons he is my favorite central banker. He’s never shied away from telling it like it is.

We’re all (correctly) worried about inflation getting out of hand and what to do about it. Bill said, very matter-of-factly, our escape hatch may already be closed. The “fragilities” prevent us from making that soft landing. Relatively mild tightening will “solve” the inflation problem by sending the economy into deflation instead.

Bill then elaborated on what will happen when the Fed hits these fragilities. It will back off and then…

“All that does is generate another asset price boom, and another upward surge in inflation. And then eventually they have to turn to it. It is just making the underlying fundamentals worse and then things collapse and it's even worse.

“So at this juncture, I think I'm really worried about [future] debt deflation and sooner rather than later. And I don't think we're prepared for it. We're not prepared for it in terms of public psychology, and we're not prepared for it in terms of the facilities that we've got, not just in the US, but perhaps more importantly, worldwide to deal with the degree of debt restructuring that's got to come out of a deep debt deflation problem.

“We don't have either the administrative means, or for that matter, we don't have any principles about sovereign restructuring to guide restructuring.”

He said that so calmly, I suspect the audience wasn’t sufficiently terrified. The only thing worse than out-of-control inflation is out-of-control debt deflation, and Bill is worried about it “sooner rather than later.” That should leave you shaking in your boots. Let me explain why.

Inflation isn’t great but it has a silver lining: It favors debtors by letting them repay their loans with cheaper money. A few years of moderate inflation might have helped everyone reduce their leverage. Far better not to have accrued so much debt in the first place, but it’s where we are.

Deflation does the opposite, making debt repayment harder. That would be a guaranteed global crisis. Many overextended debtors (especially emerging market corporations with dollar-denominated debt) would be unable to pay—probably including some governments. Then what? Bill White—one of a handful on our planet who will have the answer if one exists—says we aren’t ready for it.

Yes, we have a system for individual and corporate bankruptcies. It works but slowly. Exponentially increasing its case load will be a problem. We don’t have a good system for handling sovereign defaults. Are we going to foreclose on China? Italy? Brazil? That won’t go well.

Then there’s Washington—the biggest debtor of all, when you count the obligations like Social Security and Medicare. Inflation just increases the size of the obligations for these entitlement programs. I was actually surprised to see how much my Social Security check increased last year and we haven’t even gotten into this year’s big inflation.

Fiscal Takeover

Felix Zulauf observed that already-staggering government debts will probably get bigger.

“I think monetary policy has reached the point where it is not effective anymore in stimulating the economy to a very large extent, or to the extent it used to be in the past. And therefore, we are at the point where fiscal policy takes over. What you see as a result of that is that we will run larger deficits over the next couple of years than in the past.

“You will also see that the government share of GDP will continue to rise. Yours in the US was in the low 20%. It's now in the upper 30%. In Europe, the EU is at 54%. France is at 64%, government share of the economy. And the government is the least effective part and least productive part of the economy. In a sense, all the others, the private sector has to support that economy.

“The private sector's percentage is shrinking while the government sector’s is growing. And that creates structural problems that eventually will be financed over the printing press in a way. That's the way we are going, I believe.”

This is the box we’re in. Stopping inflation will create unemployment and other pain, such as falling stock markets and a potential credit crisis, to which governments will have to respond. That will add to already high and growing debts. As Felix says, government spending is both the least productive part of the economy and a growing share of the economy.

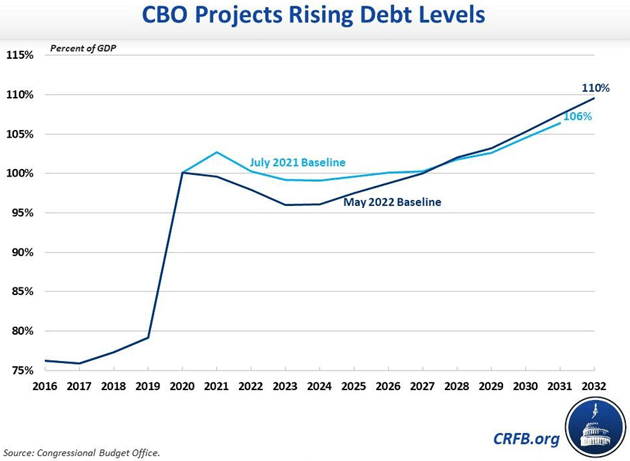

Last week the Congressional Budget Office released new debt projections, the first since July 2021. They now expect federal debt will be 110% of GDP by 2032. [Frankly, that is ludicrous. We are already at 129% according to usdebtclock.org.]

Source: CRFB

That calculation involves a bunch of assumptions, one of which is that real GDP growth will average 1.7% over the next 10 years, with no recessions. CBO also presumes PCE inflation will average 2.1%. They also assume away much of the real world. These seem like overly optimistic expectations, so there’s every reason to think reality will be far worse.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

This also assumes Congress and the White House don’t aggravate the situation. That is also unlikely, no matter which party is in charge. There is no constituency for fiscal sanity in the US. The parties are simply irresponsible in different ways.

See that big jump in 2020? That was all the COVID spending, some of which helped spark the current inflation. But from the politician’s perspective, the reaction is, “Hey, we got away with it.” They’ll do it again in the next major crisis, and there’s a good chance we will have one before the 2020s end.

That’s a depressing outlook, I know. But we also know the Earth will keep rotating, and the clock won’t stop. We won’t be able to hide indefinitely. At some point, we’ll have to face these problems and resolve them. That will be what I’ve called “The Great Reset” (not the WEF version).

And to a great extent, the final panelists each saw a similar “finale” coming. They differed on some details, but none saw it being pleasant or easy.

We are going to rationalize all this: the debt, the entitlements, the other government spending, the overvalued assets, all of it. I believe part of the answer will involve rationalizing our tax system. I think we’ll have to supplement the income tax with a value-added tax. It will hurt, yes. But we as a country need to learn that government and its benefits aren’t free. If we want those services, we have to pay for them fairly and quickly, and stop passing the buck to future generations.

We’re going to learn a very hard lesson about balancing budgets. We either have to deeply cut entitlements, to which I assign 0% probability (except for tinkering around the margins), or we have to raise taxes to a point that balances the budget. That can’t be done with income and corporate taxes, though they will certainly rise. It can only be accomplished with a VAT, which will somehow have to be designed to not inflict too much pain on the bottom portion of the economy. I think this is possible, but it will only happen in the middle of a crisis of severe proportions.

And that was my closing point:

“We're going to come to the edge of the abyss and we're going to look over it and go, ‘Oh my God, we're all going to die. What are we going to do?’ And then like Winston Churchill said, after we've tried everything else, Americans will finally do the right thing.

“It will be uncomfortable. We're going to hate it. It's going to be worse than castor oil, but we'll get through it. Our lives will go on. We'll still have family. We're going to live longer. We're going to be healthier. We're going to have more cool toys. So, I don't feel too sorry for us in the future.”

The saddest part is that the coming pain was avoidable. We had alternatives. Collectively, we didn’t choose them, and now we’ll pay the price. But we will get through it and find something better on the other side. Using George Friedman’s concept, we might call it “the Storm before the Calm.” I expect this storm in the mid- to late 2020s, leading to a boom and renewed growth in the 2030s.

And for the astute investor? There are going to be opportunities all along the way.

Dallas and Visitors

My trip to Dallas last week was quite successful, and I will likely make a few more trips there this summer. I am increasingly convinced that the environmental movement and the ESG movement, along with large oil producers making sure their investors get paid rather than invest in new drilling, means that oil and gas prices will remain elevated for quite some time. In one sense, the ESG movement is handing smaller investors a real opportunity in the oil patch. I truly wonder how Russia will be able to maintain its oil production without Halliburton and Schlumberger.

I still want to get to New York. And I am starting to get invitations to speak at various gatherings. Hopefully I will be coming to a city near you.

Starting next week, Shane and I will have visitors, many of them family, for much of June and early July. Lots of granddaughters in my future.

And with that I will hit the send button, wishing you a great week and hoping you get together with family and friends. All the best and don’t forget to follow me on Twitter. John Mauldin unplugged late at night can be fun.

Your looking forward to a relaxed summer analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.