Muddling Through Shanghai

-

John Mauldin

John Mauldin

- |

- September 5, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinTo Hike or Not to Hike – That Is the Question

Repeat After Me: Chinese Stocks Are Not the Chinese Economy

China Good, China Bad, & China Ugly

Enter a Billion Dragons

Detroit, Toronto, NYC?

“He who knows when he can fight and when he cannot, will be victorious.”

– Sun Tzu

A couple of weeks ago I was complaining about 47,000 China reports clogging my e-mail. The number now feels like it is well into six figures (perhaps a slight exaggeration). Maybe my memory is going, but there wasn’t nearly as much China talk on the way up. Funny how that works.

Is China collapsing? I think parts of China are under severe pressure if not outright recession, and clearly the stock market is a disaster. Anyone who bought Shanghai or Shenzhen stocks on margin this year is probably on the brink.

That said, China itself is not collapsing. There are parts of China that are doing just fine, thank you very much. It does have serious problems, though. The Pollyannas and the Cassandras are both wrong. The change in tone in the Financial Times is quite amusing. Their recent hyperbolic, bearish section called “China Tremors” is a case in point. Of the last 30 articles on China on their website, I found less than a handful that were positive on China. My take? China will muddle through, at least for the near term.

China is in transition, a transition that was clearly telegraphed if you have been paying attention. Our recent book on China (A Great Leap Forward?) clearly laid out this new path. Today we are going to talk about this precarious, difficult transition, which may impose profound impacts on much of the rest of the world. This transition is going to change the way global trade has worked in the past. There will be winners and losers.

But first, a brief comment on today’s employment report and how it impacts the need for a rate hike by the Federal Reserve in September. I offer a little different perspective on the coming decision.

To Hike or Not To Hike – That Is the Question

Today’s unemployment report was lackluster, as has been the case for the initial reporting for the last two Augusts. Both were revised significantly upward – August 2012 was eventually revised up 96,000 jobs, while August 2013 saw a final revision upward of 69,000 jobs, and August 2014 saw a final count of +213,000 jobs. Part of the reason for the major revisions is that only some 70% of the potential survey participants actually responded (hat tip Joan McCullough). Evidently the United States is becoming like Europe, and we are all going on vacation in August. Or at least the department personnel responsible for handling employment figures are. Expect to see significant upward revisions in the coming months, just as July saw another 30,000 added and June saw a plus 14,000.

This report was not so ugly that it would take the breath away from hawks wanting to raise rates or force doves into agreeing to a rate increase. Nothing changed, really. That is illustrated by the two articles below that were side-by-side on the New York Times website within an hour of the release of the report (hat tip Brent Donnelly). Everybody got to see what they wanted to see.

I can’t remember a time when there was such serious disagreement over what the Federal Reserve should do regarding a rate hike. I have been in several groups of analysts and economists in the last few months, and I must confess to being surprised at the split in opinions.

Upon reflection, I think I can actually understand both positions. First, the Fed keeps reiterating that they are “data-dependent” – thus the focus on every little bit of data, no matter how trivial. Let me see if I can explain why both sides can feel they are right and then why, to my way of thinking, they are missing the point.

On the side of those who feel that a rate hike should be postponed at the September meeting, it must be remembered that most rate hikes are in anticipation of an economy beginning to pick up speed. The Fed has said they want to see low unemployment, and under the leadership of Bernanke and now Yellen, they have a 2% inflation target. Remember, their congressional mandate is to promote stable prices and full employment.

While unemployment did drop to 5.1%, that is a “soft” unemployment figure. The participation rate is down. The number of part-time workers wanting full-time jobs is still high. And the new employment trend is not encouraging.

August's gains were well below trend. The average of the previous five months is 211,000; for the previous six before that it was 282,000. The yearly employment gain, 2.1%, is off 0.2 point from the late 2014/early 2015 rate. The private sector gain is 60,000 below the average of the previous six months. (The Liscio Report)

We are not close to 2% inflation; and, frankly, it doesn’t look like we’re going to get there for a while. The economy is, at best, stuck in a low, Muddle Through gear (as I predicted years ago); and getting back to a stable 3% growth rate, let alone the occasional 4–5% that we used to see, seems out of reach. The dollar is strong and getting stronger and is not only holding down inflation but also, anecdotal evidence suggests, slowing down exports in various sectors of the economy. There were those who argued that a bubble was developing in the stock market, but it appears the stock market is taking care of itself to make sure it doesn’t become overheated. There is no need to pile on to see if we can drive asset prices even lower. Further, we are just in the beginning of a housing recovery. Why raise mortgage rates, etc., at the beginning?

In such an environment, why would you raise rates in order to keep the economy from overheating? The last thing we seem to be doing is overheating, let alone even getting to a slow boil. Instead, we may already be cooling down. If the economy does start to pick up and inflation becomes an issue, we could raise rates then as fast as we would need to. Or so Kocherlakota and his friends on the FOMC say. And thus we should postpone a rate increase until we see a reason for it. Kind of like, don’t shoot till you see the whites of their eyes.

Those who think we should raise rates likewise have an array of data to support their case. GDP grew 3.7% in the second quarter. If you take out the weather-related first-quarter 2015 GDP figure, GDP growth is running well over 3%. Given the global headwinds currently buffeting economies, that’s about as good as it’s going to get. This economy has weathered tax increases and the abrupt changes of Obamacare, as well as a significant drop in capital spending related to oil production and has “kept on ticking.” If there is a recession in our near future, as David Rosenberg points out, it would be the first recession ever that did not see consumer spending or employment go down for the count.

We’ve always been able to find negatives in the unemployment rate. Even if unemployment were somehow to ratchet down to less than 200,000 per month, it will be for only two quarters at the most; and it may be that before the end of the year we will be under 5% unemployment.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We just set a record for all measures of corporate profits in absolute terms. We finally set a new record for real disposable personal income in July, again in absolute terms. As Jim Smith says,

What all this means is that when the FOMC meets on September 16 and 17, they will be looking at a US economy in which more people are employed than ever before, earning more money than ever before, producing more goods and services than ever before, and with personal consumption expenditures and corporate profits at the highest levels ever seen. If that is not a prescription for finally raising the Fed Funds rate, then I can't imagine what it would take to get them to move. (source)

Despite the significant slowdown in the oil patch, the level of investment in the second quarter was almost 4% higher than last year. Businesses are optimistic. Even given the turmoil in Canada, China, the Eurozone, and the rest of the BRICS, and even though global trade is beginning to fall off a little bit, the US economy seems to be doing quite well in spite of it all.

What else do you need in order to begin to normalize rates? Inflation is under control and according to most Fed economists seems to be ticking higher. Unemployment is moving lower. The economy is doing quite well. If not now, when? How much better do you want things to get before rates are taken back to something close to normal?

I must confess that I personally lean toward the latter argument, but I have a few additional reasons for thinking the Federal Reserve should act in September. As I have presented in previous letters, there are real reasons to think that low interest rates are not only creating malinvestment but also encouraging companies to use financial engineering and to buy their competition rather than purchasing the tools of production and actually competing head on. These behaviors distort an economy over the long term. They frustrate Schumpeter’s forces of creative destruction.

Further, what policy tools does the Federal Reserve still have available if we enter a recession? I admit that doesn’t seem to be a likely possibility today, but there are many potentials for exogenous shocks to the US economy that could cause a recession. Further, in the history of the United States we have never had a period longer than nine years without a recession. This recovery, relatively weak though it is, is getting long in the tooth. Do we want the Fed to confront the next recession with another round of massive quantitative easing as the only policy tool left to deploy? When their own research shows that QE wasn’t very useful and when we can clearly see the distortions caused by QE in emerging markets around the world?

The Federal Reserve is functionally incapable of not feeling the need to “do something” in the midst of a recession. If the only tool they have is further massive quantitative easing, they will use it. Damn the distortions, full speed ahead!

I would not argue for a rapid rate hike. In fact, I would prefer 1/8 of a point at every meeting, rather than the typical quarter point. But there is no reason not to raise a quarter of a point at this meeting, skip a meeting to make sure everybody can take a deep breath, and then raise once more before the end of the year.

I mean, really? Does the Fed think this economy is so fragile that it can’t take a lousy quarter-of-a-point increase in interest rates? The Federal Reserve needs to begin to restock its policy tool chest now. While I personally think we are a long way from ever seeing 5% Fed funds rates again, a 2% rate can probably easily be absorbed if it comes slowly. And that rate would give the Fed some policy tools when, not if, we enter the next recession.

Now, let’s turn back to China.

Repeat After Me: Chinese Stocks Are Not the Chinese Economy

It’s easy to assume that a country’s stock market reflects the condition of its economy, but that is not always the case. Further, what the stock market really does reflect is the consensus estimate of an economy’s future condition. More specifically, stock prices reveal future expectations for corporate profits.

This generally applies to both the United States and China. One key difference, though, is that most American stocks represent companies that seek to make profits. In China, that isn’t necessarily the case.

The Chinese stock market includes many state-owned enterprises (SOEs), whose executives answer to bureaucrats in Beijing. The government views them as public policy tools. Everyone is happy if the SOEs make a profit, but profit is not the first priority.

If US stock prices generally tell us more about the future than the present, except in times of serious over- or undervaluation, then Chinese stock prices tell us even less about either.

Just as last year’s incredible run-up in Chinese stocks did not signal an economic boom, the ongoing decline does not signal an economic bust. The correlations aren’t just weak, they are nonexistent.

China’s official economic data is also questionable and would be so even if GDP were a precise measurement tool. As we discussed last week, it usually isn’t.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

It is no stretch to say we are flying blind about China.

Fortunately, we have diligent researchers like Leland Miller of China Beige Book, whose research firm does the hard work of gathering reliable data each quarter from thousands of companies in China and assembling it in comprehensible form. His data shows that China’s economy has actually been in good shape since China stopped acting Chinese last year. But even then, you have to separate the Chinese economy into several categories.

China Good, China Bad, & China Ugly

Among the many letters and reports on China that I received over the last month, I’d like to single out an excellent research note that the team at Gavekal Dragonomics published last week, called “What to Worry About and What Not to in China.” I appreciated this piece, because it really helped me structure my worrying. I dislike spending energy worrying about the wrong things. Further, worrying about the wrong things can be dangerous. It’s when you are paying attention to the wrong things that what you should have been paying attention to jumps up and bites you on the derrière.

In the spirit of the Gavekal note, here is the good side of China. We’ll get to the bad and the ugly below.

Chinese real estate prices will stabilize. We hear a lot about China’s massive infrastructure boom and the resulting “ghost cities.” These aren’t just rumors. The government mandated the construction of entire cities to house the formerly agrarian population as it shifts to industrial jobs. Provincial governments earned as much as 80% of their revenues from land sales. Essentially, this is a process where they take possession of rural land that has very little value in price terms, declare it to be available for development, and can make profits several orders of magnitude greater than their costs. Nice work if you can get it.

The ghost cities will not stay empty forever. They will fill with people over the next few years (in some cases more than a few). The recent housing bubble is more a function of young people wanting to cram into certain popular areas. The broader internal migration will support housing prices even as the bubble areas pop.

It might be helpful to think of the Chinese ghost cities as analogous to the overbuilt condos in Florida. Prices in Florida did in fact collapse, and places were selling for a fraction of their construction cost. I wrote at the time that I thought they would be very good investments, because the number of people wanting to retire to Florida is actually a fairly steadily growing figure. Low taxes, good weather, positive infrastructure, excellent medical care – what’s not to like, other than it’s not Texas? Just saying…

While it will take time, those ghost cities will eventually fill up. Further, most of that real estate was bought with significant capital, often 50% or more. Those apartments, which are essentially shells because they have not been finished out, function more like stores of value or bonds than they do as traditional apartments. While the original investors may not get the inflation-adjusted returns they want, inflation will eventually mean that they will get some return on their investments. While this may not make sense to most of us in the Western world, given the Chinese experience, owning something that is tangible might make sense. The reality is that there are hundreds of millions of people who are going to want to find a place to live in China over the next few decades. That seemingly endless source of buyers will eventually turn the ghost cities into real ones.

Note: that doesn’t that all of the ghost cities will be developed. Some probably won’t, as they are too far outside the path of growth. But most of them have excellent infrastructure and connectivity to the rest of China. Think of how satellite cities developed throughout the South and Southwest of the United States. Admittedly, in the US this was generally a demand-driven process. In China it was a way to prop up GDP and actually create something tangible, unlike the ephemeral transfer payments and other congressional pork that the US used as “stimulus.” I would argue the Chinese are better off putting their money into some kind of infrastructure than we were putting ours into temporary, nonproductive stimulus.

China is shifting from investment to consumption. The phase of China’s emergence led by exporting and infrastructure growth is ending. The next task is to build an economy that relies less on exports and more on consumer demand and services. This path was detailed in our China e-book. It has been the plan for some time.

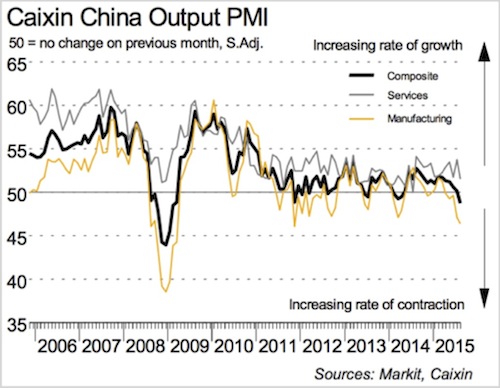

This process will continue to be ugly at times. Last week’s Purchasing Manager Index for Chinese manufacturing fell even deeper into contraction territory, where it has languished for six months. Services PMI also fell but not nearly as much; and more importantly, it continues to show a mild expansion.

I know this is anecdotal, but in secondhand conversation with a very-high-profile private equity group here in the US, they report that they have four significant investments in China. None are in the manufacturing area; all are in the services sector. The slowest of their companies is growing at over 20% per year, and some are doing significantly better.

The China of today is not your father’s China. Fifty percent of the economy is now services. That part of the economy is growing – and evidently growing enough to offset the contraction in the manufacturing sector. And we must remember that China actually added twice as much to its GDP in either dollar or yuan terms in the past year than it did in 2003 when its growth was a “miracle.” That helps to put their reduced growth in context. As I have pointed out, the law of large numbers requires that their growth will be slower in percentage terms in future years.

Room for More Stimulus. The Chinese government is spending big bucks to prop up the stock market and the renminbi through various interventions. Estimates vary, but $200 billion to date is a good guess. They will have to spend more. The good news, if you can call it that, is that they can afford it. There is, of course, reason to question the wisdom of trying to prop up a stock market – especially in the rather ham-handed (one is tempted to say “rookie”) way they have gone about it. More about this later.

Aside from its multi-trillions in FX reserves, the People’s Bank of China still has plenty of room for monetary stimulus. Short-term interest rates in China are over 4%, far higher than in most of the rest of the world. That means the PBOC can probably make several more small cuts without overly weakening its currency. Yes, I know that they devalued their currency a whole 2–3% recently. Given that the euro and the yen are down well over 30% against the dollar, I really find the overreaction in the West quite laughable.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The IMF says China has to float its currency in order to be included in the SDR (Special Drawing Rights). Okay, so they’re starting that process. As I have said repeatedly for the last four years, when they finally float their currency, the likely direction of the renminbi is down, not up. All the ranting of Donald Trump and US senators combined cannot push back the tide of what the market sees as the true value of the renminbi.

China’s banking system is also on a strong footing. Banks have little exposure to the stock market. Chinese brokers have very conservative (by Western standards) capital requirements. Gavekal says not to worry about a systemic crisis. (The Chinese shadow banking system is something else altogether. See below.)

Despite all this, China is enduring an economic slowdown that may get worse. We have plenty of legitimate worries. Now, here come the bad and ugly parts.

Idle Industrial Capacity. The transition from an investment-driven export economy to a consumption-driven service economy will take years. Further, it won’t be easy for those on the industrial side of the house. While it may be hard to believe, over the years China has lost more steelworkers than the US and Europe have. They overbuilt steel mills. It seemed that every province wanted its own mills, and their production capacity just grew too large. It likely still is too large.

The government hopes to reuse some of the idle capacity in its very ambitious (and quite expensive) “One Belt, One Road” or New Silk Road initiative. That strategy may help – as long as lower exports don’t slow down the plan. But that is a decades-long process and is unlikely to relieve much pressure over the next few quarters or years.

As every parent and employer knows, idle hands are never a good thing. You have to keep people occupied, or they will find suboptimal things to do. The last thing Beijing needs right now is a few million idle, i.e., unemployed factory workers. It is some somewhat ironic that China is facing the same problem as the US is: what do you do with excess manufacturing workers, and how do you help them transition to jobs in the service economy? I guess the best you can say for the Chinese is that the jobs in their manufacturing economy were not high-paying so the transition will not be as economically wrenching.

Chinese Stocks Are Still Overvalued. Calculating “fair value” is difficult for Chinese stocks. As mentioned above, many companies are subject to government interference. Data integrity can be a problem in others. We can’t always make apples-to-apples comparisons with non-Chinese stocks.

Whatever yardstick you use, Chinese stocks are still quite richly valued, even after recent losses. The losses, recall, are simply the undoing of a rally that was never justified in the first place. It was a momentum-based rally in a market of retail investors who come to the stock investing with a gambling mentality.

It’s also worth noting that some Chinese stocks haven’t traded a share in weeks. Further, the government has forbidden insiders from selling in other cases, so it’s hard to know whether the index values and share prices we see are trustworthy right now. I suspect many are not. Which leads to the “ugly” part…

We Don’t Know Whom to Trust in China. Until 2–3 months ago, most China watchers believed that the country’s leaders had a thoughtful, comprehensive economic plan. I don’t know many people who think so anymore. I should note that in our book I was very clear that I thought the Chinese government was not prepared to deal with the nature of the transitional economic crisis they were faced with. None of the leadership has any true experience in dealing with major economic issues in a modern economy.

Walt Whitman Rostow wrote a book back in 1960 called The Stages of Economic Growth: A Non-Communist Manifesto. He outlined five stages that mark the transformation of traditional agricultural societies into modern mass-consumption societies. The first three stages are actually suited to top-down command-control governments. The fourth and fifth stages – at least according to him, and he has been proven right over the ensuing 55 years – can’t happen under the same type of government. There must be a bottoms-up, consumer-driven economy.

So when I say that China’s leadership has no experience in dealing with a modern economy, I mean it in that context. They’ve done a heck of a job for the last 35 years, especially given where they started. What they have done is unprecedented. So hats off. But just as we keep reminding investors that past performance is not indicative of future results, so should we be skeptical about the future quality of government decisions. And frankly, I did not expect the truth of that assertion to become apparent so quickly and so blatantly in China.

If the leadership did have a plan going into the stock market tumble, it must have gone out the window. The on-again, off-again interventions and conflicting statements could not have been part of any rational plan, unless the plan was to confuse everyone. They succeeded, if that was the case. They are clearly making up their game plan in the middle of the game.

In the space of about two months, Beijing reversed years of statements that had almost convinced the world that China really believes in market discipline. That PR campaign is now in shambles. The best-case interpretation is that the leadership is in disarray amid Xi Jinping’s corruption crackdown and unable to coordinate its messaging and intervention strategies – which is obviously not good, either.

Many people thought that at least the central bankers at the PBOC were competent and as immune from political interference as it is possible to be in China. No more. The PBOC may well have tried to assert its independence; but if it did, it failed.

The Chinese government is once again a “black box,” at least in terms of its economic policy. We don’t know who is making the decisions, nor can we be sure what they want to accomplish.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Just a few weeks ago, we all thought China wanted to float the renminbi so it could go in the IMF’s reserve currency basket. The IMF has bent over backwards trying to help China do this, even extending the review period by a year so China would have more set-up time. Beijing is not taking the hints. Either they have abandoned that goal or they don’t understand what they need to do to accomplish it.

As Worth Wray and I wrote in A Great Leap Forward?, China is engaged in a transition from which it cannot turn back. Well over a billion Chinese are in various stages of joining the modern world. Our planet has never seen anything like this, so it’s no surprise that the process is rocky. The transition will continue regardless, because China has no other option. If you want to know more about China, you really should get a copy of this book now. I priced it at a very reasonable $8.99 as an electronic book. It now appears that my regular book publisher, Wiley, is going to bring the book into print and will take over the e-book marketing, so prices will go up.

Investors want to know about China’s stock market and currency. Even after all of this year’s stimulus, the Chinese leadership still has plenty of ammunition. They can prop up the markets for a long time if they are willing to spend the money. Of course, that will drain reserves.

Beijing has always prioritized stability over free markets, and I think they will continue to do so. The risk they run is that shoving problems under the rug simply stockpiles them instead of solving them. Eventually they become unmanageable, and you have to throw back the rug and confront them. What that will look like in a Chinese context, I don’t know; but I bet it won’t be pretty.

Before we Yankees get too smug, let’s remember that we have our own black box over here, called the Federal Reserve. Its independence is also questionable at times, and it just spent the last six years interfering in our own economy via multi-trillion-dollar QE programs. What would we say if the PBOC did the same thing in China? And now we can say the same thing about Japan and Europe.

In the short term, I think the major risks lie not with China itself but with China’s energy and raw materials suppliers. Countries like Australia, Brazil, Chile, Angola, Saudi Arabia, and Russia are all going to lose as China continues shifting to services and away from infrastructure building and manufacturing. China is not going to turn off the spigot, but it will reduce the flow of materials into the country. Those commodity-exporting countries will, in turn, reduce their purchases of US, Canadian, and European goods and services.

We’ll all feel China’s pain to some degree. That, ironically, is the main reason I think China will get through this. By virtue of its sheer size, it has spread its impact over practically the whole globe. Just as we all shared in China’s growth, we will all share in its contraction.

My September travel schedule looks surprisingly light. Right now there is nothing until the end of the month, when I will go to Detroit for a day and then on to Toronto for a few days. In Toronto I will be speaking at the annual CFA Forecast Dinner. I am told there will be some 1200 people there. For whatever reason, I have been making the circuit of Canadian CFA forecast dinners for the past few years. I have done British Columbia, Alberta, and Manitoba. Thankfully this one is not in January – Edmonton was cold; Winnipeg was colder. I find speaking for CFA groups somewhat intimidating, as the majority of the audience knows more about what you are talking about than you do. I will also be doing a completely different presentation the night before for my Canadian partners, Nicola Wealth Management. More info on all the events in a later letter.

I will probably have to be in New York for a few days sometime in the middle of this month. Then October looks to be busier, but not too much so. Which is fine by me, as I am really diving into the new book I’m writing on how the world will change over the next 20 years. I’ve been wanting to write this book for at least 10 years, and now seems the right time to do it.

I have to confess that I was not as diligent with my diet and in working out in August. There were just too many fabulous meals with friends and too much temptation, so when I got back last Sunday I put myself on the most serious diet and workout schedule I’ve ever attempted. Before this, my concept of diet was to cut back a little, as opposed to the more controlled calorie restriction that both my friend Pat Cox (who is the biotech expert at Mauldin Economics) and my doctor Mike Roizen, head of wellness at Cleveland Clinic, keep telling me to try. To my utter surprise, it is working better than I could have imagined.

I was surprised at how quickly I could get out of shape. The Beast has been putting me through my paces this last week. Yesterday, I finished my workout by walking the 17 flights of stairs to my apartment. I will admit I had to stop a few times to catch my breath. It brought to mind my experience in Zimbabwe some 23 years ago. I was with my friend Pat Mitchell, who lived in Johannesburg. I had done him a big favor, so to repay me he treated me to a long, first-class vacation in Botswana and Victoria Falls. The Chobe Lodge was fabulous. Amazing safaris. Highly recommended. The last day we white-watered the Zambezi below Victoria Falls, which is a class 5 rapids.

It was hot as Hades (it was summer there), and the rapids could get your adrenaline pumping. We came to the end of the run in a canyon, where we were informed that we had to walk to the top in order to get back to the hotel. It was some 400 vertical feet of switchbacks. Fortunately for me, Pat was seriously out of shape and had to stop every 30 or 40 feet to rest, so I didn’t have to reveal how out of shape I was. What was embarrassing, though, were the 60-year-old men who were running up and down porting the equipment back up. I swear I saw the same man four times, and he couldn’t have been much younger than I am now. The young guys weren’t intimidating, but I still recall that old man walking rapidly up that trail carrying a kayak. Today, I decided I needed to walk up to my apartment more often.

This is Labor Day weekend in the United States. My brother and his family and all but one of my kids, along with six of my grandkids, will show up Sunday night for a cookout by the pool. Six of my seven kids have harassed me into playing a game called Cards Against Humanity, which they swear is fun. Have a great week.

Your hoping the Fed raises rates analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.