Coronavirus Helicopter Money

-

John Mauldin

John Mauldin

- |

- March 13, 2020

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinPolicy Shocks

My Best Guess on the Future

A Consumer-Led Recession

Don’t Ask, Don’t Test

One Major Caveat

The Right Thing

New York and Back to Puerto Rico

I write this letter early Friday morning after a week in New York visiting with many fellow market participants. And lots of phone calls, both to analysts and medical experts. I had originally planned a completely different letter but circumstances changed.

Humility is a good thing to have when you’re forecasting the economy or markets. You never know what relevant facts you might be missing, so it’s best not to be too confident.

In my annual and decade forecasts, published just two months ago, I said recession probably wouldn’t happen this year, absent an exogenous event. Now, thanks to COVID-19, I am far less confident in that forecast. We have an exogenous event underway that might change everything.

Today we’ll consider where this is all headed and what could happen—not medically (others can address that) but economically. The coronavirus could take us all someplace we really don’t want to go.

Policy Shocks

Some of my libertarian friends like to say the best thing government can do is nothing. I believe there are some things only governments can do. One of them is respond to viral epidemics. So far, the government response has been, let’s just say, not up to par. That finally seems to be changing.

The Federal Reserve injected some $600 billion into the market yesterday and promised a great deal more. The analysts I trust have reached a consensus that US rates will soon be near or at the zero bound. All well and good in a financial or business cycle recession, but that’s not what we have today. We have a biological pandemic (the WHO has finally begun to use that word) that is clearly changing consumer behavior patterns. Low interest rates and easy money are not going to change those patterns.

I am a believer in the free market and individual decisions. I don’t blame anyone who decides it is in their best interest to stay home and avoid crowds. That is their own personal decision. However, the collective decision of many consumers to reduce their activities has the very real probability of causing a recession soon.

RSM economist Joseph Brusuelas produced a handy flowchart showing how these situations tend to evolve (click the link below for a larger image).

Source: Real Economy

We have three different shocks underway.

The supply shock will become more visible in the coming weeks as the Asian export pipeline runs dry, with unpredictable but possibly widespread effects on US businesses.

The demand shock is already hitting as travel slows, people avoid large gatherings, and consumers reduce discretionary spending.

The financial shock is well underway in the markets, as you are probably aware. The last few weeks brought volatility we haven’t seen in a long time.

The response to all these shocks is both monetary (central banks) and fiscal (governments). The monetary side is quite limited in what it can do. Interest rates are already near zero and below zero in some places. Plus, easier credit doesn’t address the problem. Cheap financing won’t speed up the supply chain or make people want to travel again. Nor will it help corporate earnings if customers aren’t spending.

In this scenario, the policy response is mostly fiscal. When Milton Friedman talked about “helicopter money,” he was referring to central banks, but governments have helicopters, too. And the engines are revving up everywhere coronavirus strikes.

In China, the central bank has avoided macro stimulus measures but Beijing and local governments show little restraint otherwise. They are cranking up all kinds of infrastructure projects and subsidizing businesses to pay workers for the containment periods. Banking regulators are letting small businesses delay debt payments. Some are also being exempted from social insurance taxes for the next few months.

Hong Kong is simply giving away cash, with every adult set to get the equivalent of $1,285. I suspect this is about more than virus relief, though. It might also reduce some of the recent protests.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Japan is allocating trillions of yen to subsidize workers who were forced to stay at home, often with children whose schools the government closed. Small companies will get zero-interest loans. Prime Minister Shinzo Abe promises more is coming, too.

In hard-hit Italy, Prime Minister Giuseppe Conte says he will deliver “massive shock therapy” to an economy that, in theory, should be practicing fiscal austerity. That era seems to be over. The government is planning a debt moratorium, including mortgages. How they will do that in one of the world’s weakest banking systems, and still stay in the eurozone, is unclear.

The ever-flexible European Union is preparing to relax limitations on “state aid” its members can provide. They may (shudder) even create a “coordinated” fiscal stimulus package.

Will the US do likewise? I think it’s inevitable. The Trump team and Democrats are already floating ideas. Wall Street people and various industry leaders are practically begging for help. The pressure will only grow as more companies lose revenue and more people find themselves unable to work. This being an election year, some sort of package will pass with bipartisan support. The worse this gets, the larger it will be.

Note, all this will be on top of whatever they allocate to pay for coronavirus testing, treatment, and (eventually) vaccines. It also doesn’t count the various “automatic stabilizer” programs that will kick in as more people lose jobs and income. And it will all happen as tax revenue falls for the same reasons.

Whether or not all this helps the economy or not, it will certainly expand a federal deficit that was already set to exceed $1 trillion this year. I suspect it will end up doubling that number even if the coronavirus threat recedes soon. The politicians now have a perfect reason to spend more money and they are going to seize it. That is just how it works.

|

My Best Guess on the Future

As bluntly as I can put it, this is not a financial recession (yet). We are in a biological crisis and it is creating panic. Much of that panic is simply because of the “unknown unknowns” surrounding COVID-19. We know it is more contagious and it appears to be more lethal. We are not really sure how lethal, but clearly none of us want to get the virus. This is introducing an enormous amount of uncertainty into the markets and the business world, neither of which like uncertainty.

This is the yield curve as of Friday morning before the markets opened from Bloomberg. Rates have risen a bit from their bottom two days ago, but this is still rather shocking.

Source: Bloomberg

In a conversation last night, several participants mentioned well-known names who feel that the US 10-year government bond may approach zero before this is over. Dear gods…

A Consumer-Led Recession

This graph hit my inbox this morning from the brilliant Danielle DiMartino Booth of Quill Intelligence. It shows clearly how travel is slowing, which we knew, and will likely slow even more as major events are cancelled or postponed.

Source: Danielle DiMartino Booth

A few anecdotal observations:

As I walked around New York this week, I would ask the taxi drivers and restaurant personnel how business was. They all said it was down. Interestingly, higher-end restaurants seem to be slow - perhaps because they have been ordered to use only 50% of their normal seating capacity. I mentioned this to my friend Ian Bremmer and he pointed out that many New Yorkers have second homes outside the city. They have either left town or are working from home.

One money manager noticed that his trades were executing more slowly. In trying to figure out why, he finally realized the traders he uses were all at home on their Wi-Fi which was slower than the Wi-Fi at their offices. Not a big deal, but those traders also aren’t going out to buy a sandwich for lunch. Bad news for restaurants.

My associate Patrick Watson and his wife Grace run a rather high-end hair salon in Austin. They’ve been doing so for almost 20 years. Their sales fell 14% in early March from the same point a month ago. Haircuts and color are discretionary spending. Gray-haired people can, and some evidently are, deciding to let their roots show rather than go to the salon.

Question: Does this change behavior going forward? Do we find out that staying home with Netflix and pizza is as good as an upscale Italian restaurant and theater? I mean, not the quality of the food, but just the experience and how we enjoy life.

How many other hundreds of ways is this particular pandemic going to affect our lives and our lifestyles going forward? That is completely unknowable, but it is something to ponder.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I get that the Federal Reserve and the government feel they have to do something. But their tools are generally geared to helping Wall Street, not Main Street. I think this note from Woody Brock sums it up very well.

More on the Crisis and the Markets

Two weeks ago, I sent out a crisis memo warning that the market could soon drop to 17,500 on the Dow. I stressed that the true threat to the economy and to profits and employment was not only interruptions in the supply chain, but more importantly the first implosion of the SERVICE sector we have ever seen.

This is now just what we are seeing as movie theaters, airlines, “events” of all kinds, schools, universities—all closed down. And the Dow today is down from 29,000 to 21,000. A further drop to our predicted 17,500 could occur within a week or two.

In this brief Memo I wish to add a few points regarding the volatility of the market.

Pricing Model Uncertainty

The main point concerns the role of what we have called “Pricing Mode Uncertainty” (PMU)—a concept we introduced some 14 years ago.

Our fundamental theorem was that the greater the amount of PMU there is in a market, the greater the degree of price overshot upward and downward there will be. The proof was game theoretical and was presented at a conference at Stanford University.

The degree of PMU rises with the degree to which investors admit that they do not understand the mapping of “news” into prices.

In the efficient market theory, it was simply assumed that all investors would—upon hearing the news—agree on the “correct” new price of the asset. There was thus no PMU and thus very low volatility.

In the current case where no one understands what the “news” really is, much less how it will impact asset prices, PMU is MAXIMAL thus implying huge price swings of the kind we have and will experience.

Intuitively, the reason underlying our theorem is that the greater the PMU level, it will be rational for all investors to drive price trends much further up and down. The logic is fascinating—the math very complex.

One very important form of investor ignorance today concerns the markets view that it is prospects for corporate earnings that will matter most. This is wrong.

What will matter are the collapse in profits and survivability of millions of privately owned proprietorships and partnerships whose profits are not even included in index earnings data.

It is these firms who could end up firing millions of workers and going under. THIS is what will impact Main Street and unemployment—often long before official earnings of large corporations are even computed.

The data we have for understanding the lives and behavior of these small firms that employ most Americans is sparse and scarcely looked at.

This is one further reason not to listen to data-junkies or self-styled “quants” who loathe anything subjective.

This is the time for very subjective judgements—backed up by compelling deductive LOGIC of a kind that has all but disappeared in today’s rage for “evidence-based truth”—a fatuous concept at best.

Don’t Ask, Don’t Test

My friend Ben Hunt wrote two weeks ago that we were in a period of “don’t ask, don’t test.” He has been extremely critical, and rightly so, about the slow response in getting tests available. There is real reason to believe that the promised 1 million tests are really not there.

That being said, it will get better and when we actually start testing at scale, I suspect we will find a lot of people have the coronavirus. My extremely informed sources, who do not want to be named, consider it quite reasonable to expect 100,000 people in the US will test positive in a relatively short time.

The mainstream media will breathlessly report each increase and their locations and what is happening at the local hospitals. How do you think people will respond as the number of cases approaches 100,000 with no sign of slowing?

Eventually the number of cases will begin to decline. Dr. Mike Roizen thinks there is an 80% chance that by the end of April we will have seen the total number of cases peak and begin declining, and that the coronavirus is like its predecessors. This particular coronavirus is worse in that it is more contagious and that it will live outside the body for a period of time. Warm weather in the past generally helped.

There’s been a great deal of concern about the outbreak and number of deaths in Italy. The Italian hospital system is, to be kind, simply inadequate for this scenario. The WSJ noted a few days ago:

In Italy, which has the oldest population in the world after Japan, 58% of COVID-19 patients who died so far were over 80 years old, and a further 31% were in their 70s, according to the National Institute of Health, Italy’s disease-control agency… It should also be noted that, like many socialized medical systems, Italy’s system has a personnel challenge… There aren’t enough specialized doctors and nurses to staff intensive-care units.

On a positive note, the US has three times the per-capita number of ICU beds as Italy, and they are far better equipped. So hopefully we will fare better, if it reaches that point.

This is an economic/investment letter, so when should we think about getting back into the market? Consider this chart from Gavekal, which again came this morning. It shows Chinese equities bottomed when daily new COVID-19 cases peaked.

Source: Gavekal

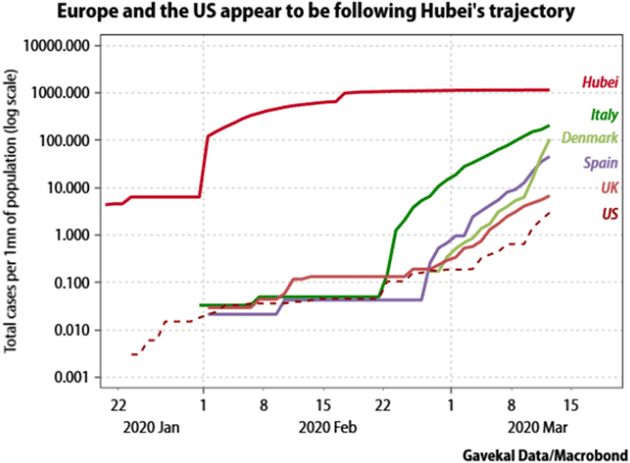

Europe and the US seem to have the same pattern of cases as China. Which means that we will peak as well at some point.

Source: Gavekal

My personal plan for my own portfolio, other than the private funds that I own, is to wait until the number of US COVID-19 cases begins to peak, as I believe that will probably be the time of peak panic, and then I will get back into the market.

I will be looking for dividend and fixed income opportunities, as after all I am 70 years old, and I tell all my clients at that age they should be looking for more fixed income. Right now, I don’t have enough but I think there’s going to be a great buying opportunity in the not-too-distant future.

There are going to be some opportunities of a lifetime in the not-too-distant future. Please be prepared to take advantage of them.

Seriously, as troubling as this pandemic is, I’m confident humanity will invent vaccines and treatments while hospitals develop ways to deal with it. Next year, and for a few years after that, it would not surprise me if we all get our COVID-19 vaccine just like normal flu shots.

One Major Caveat

Right now, the corporate bond market seems to be relatively (and I use the word loosely) not acting as badly as you might expect. However, the oil price crisis brought on by Saudi Arabia and Russia could push some energy companies to the brink of insolvency. Those assets will be bought by firm hands, as it was in the last oil crisis. But if it triggers a problem in the high-yield and junk bond markets, this recession can get a lot worse. It is something we have to pay attention to.

The Right Thing

I think it highly likely our government will do some crazy things in the next few months. However, there are some fiscal policies that actually make sense. I’ll give you three specific ideas.

First, President Trump should suspend the tariffs he has imposed on China and other countries. They represent billions in taxes on American consumers. It is not the case, as he claims, that China is paying them. We are paying them, to the tune of billions every month, in higher prices for imported goods. (Yes, we’re importing less since China shut itself down, but that won’t last forever.)

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Ending tariffs would be a large, direct stimulus to the US economy. Better yet, it can happen immediately. The president imposed the tariffs on his own authority and he can end them that way, too. He doesn’t need to negotiate with Congress, nor does he need Democrats to cooperate. It could happen almost immediately. Markets would celebrate, too.

Second, with Treasury bond yields now below 1%, and actually below zero after inflation, we should start refinancing as much of the federal debt as markets will accept—which at the moment seems to be a lot. The Treasury Department already has wide authority to issue new debt and it could sharply reduce the government’s interest costs. Those savings could be applied to more helpful programs. As with the tariffs, this could happen quickly.

Third, issue very long-term bonds (50 years+?) and use the proceeds to rebuild our crumbling infrastructure. We Americans who travel internationally (or used to) and see the airports, highways, and trains in other developed countries are constantly ashamed of what we have in the US. There’s just no excuse. This is the one kind of spending where government debt actually makes sense, and would provide plenty of jobs, too. Make money available to completely rebuild the crumbling water systems in many cities.

Will they do any such thing? I know we are all cynical about politics, and with good reason. But if we can’t get past politics-as-usual and pull together in what threatens to be a genuine national crisis, then we have even deeper problems.

I am an optimist and I have faith in my country. As Winston Churchill supposedly said, “Americans can always be counted on to do the right thing, after they’ve tried everything else.” The process may be ugly but I believe we will reach the right place, eventually. Let’s try to skip some steps.

New York and Back to Puerto Rico

As I finish this letter, I will be heading off to another meeting before going to the airport and back to Puerto Rico. I have been in New York putting some final touches on a radically new investment management service, sort of my dream team on steroids. Literally, what we will be doing was not even possible a few years ago. Technology has opened doors that absolutely boggle my mind. More on all that in a few weeks.

As I wrapped this up, Mike Roizen called to report 60% of the patients he was going to see today have cancelled. This is one of the nation’s top doctors. Appointments with him are tough to get and are often people with serious conditions. Yet many are giving them up. That’s how bad the fear is getting.

One last point, at dinner last night, there was universal agreement on our frustration with President Trump’s decision to suspend air travel from Europe. That may be the right call. I am not privy to the information they see. But to do so without giving our allies a heads up is simply unforgivable. They found out just like the rest of us. You simply do not treat your allies like that.

Not to mention your own citizens who are in Europe wondering if they will be able to get back. Really? If you have to close off air traffic for our own safety, fine. Make the hard call. That’s what presidents are supposed to do. But you pick up the phone and call your allies and give them some notice.

We have to work with Europe. I think they are going to be a lot less willing to work with us in the future when they can’t even trust us to tell them in advance of difficult decisions. I am in agreement with many things that Trump has done. But this one mystifies me.

And with that I will hit the send button. You have a great week and as I said last week, start putting together a watch list of things to buy at fire sale prices.

Your looking to make a bull market call analyst…

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.