Catastrophic Success

-

John Mauldin

John Mauldin

- |

- September 24, 2011

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin400 Billion Yellow Aspirins

The US Government Is in the “No-Money-Down” Mortgage Business

Crash Alert?

Is Social Security a Ponzi?

Catastrophic Success

Europe, and Breaking the Light-Speed Barrier

Breathes

there a man with brain so dead

Who

never to himself hath said,

“Social

Security looks like a Ponzi Scheme?”

- With apologies to Sir Walter Scott

Today we look at Social Security. In the US, Texas Governor Perry touched the third rail of Social Security and called it a Ponzi scheme, which of course immediately made him the leading candidate in the “shoot the messenger” category. Behind the rhetoric, we look at some actual numbers. No, not the unfunded liabilities, that’s too easy. Let’s look at what a heartless, uncompassionate man President Roosevelt was when he started Social Security (and that’s what many will call me after reading this!). Behind the tongue in cheek, there are some very real issues that do not get addressed when we talk about Social Security, but that need to be part of the discussion. And of course, we must start off with the results of the FOMC meeting, which has me feeling not at all amused. What are they thinking? Apparently, they are seeing the results from another, alternative universe. There is a lot to cover as I head off to London, where I will finish this letter.

But first a very important announcement. I am very excited to be able to introduce my readers to a new mutual fund offered by my friends Altegris Investments. This fund is a blend of five commodity trading advisors or CTAs. Normally, to access a CTA you be to be an accredited investor, with all the net-worth requirements and limited liquidity. But Altegris has figured out how to wrap a mutual fund around CTAs and create a fund of commodity traders with all the usual aspects of a mutual fund (daily pricing, liquidity, etc.).

I have long been involved in the commodity-trading advisor space (some 20 years) and am a proponent of CTAs as a way to diversify portfolio risk. I have written a detailed report on this fascinating sector in relation to the fund, and it is available for free at http://www.altegrismutualfunds.com/landing/mauldinreports1.aspx, along with more information on the fund (including the offering memorandum and important risk disclosures, which are also included at the end of this letter).

The fund has been very well received since its launch and has grown rapidly to over $1 billion. There has been very active interest in the professional community, as advisors and brokers are looking for simple and realistic ways to diversify their clients’ portfolio risk, as well as a way that is truly noncorrelated to typical stock funds and many other asset classes. Whether you are a professional or individual, you really should take the time to research what I think is a very solid fund. My partners at Altegris have decades of experience in the CTA space, with the largest database of CTAs and long-term relationships with many of the managers (I actually started my investment career in the commodity fund space, so have more than a passing knowledge of the arena). Given the potential for volatility in the global markets, I think it makes sense to have some exposure to funds that can go both long and short (depending on their models). I urge you to read my report.

http://www.altegrismutualfunds.com/landing/mauldinreports1.aspx

400 Billion Yellow Aspirins

My mother used to tell me, “John, if you can’t say something nice, then don’t say anything at all.” So let’s see if I can find something to nice to say about the FOMC announcement. How about: “At least they didn’t cause TOO much damage”? As Rich Yamarone tweeted immediately after, they announced they would buy 400 billion white aspirins and sell 400 billion yellow aspirins. This was not something that should have been done, but thankfully they only did some $400 billion and not a few trillion, which could have really screwed (a technical economics term) things up.

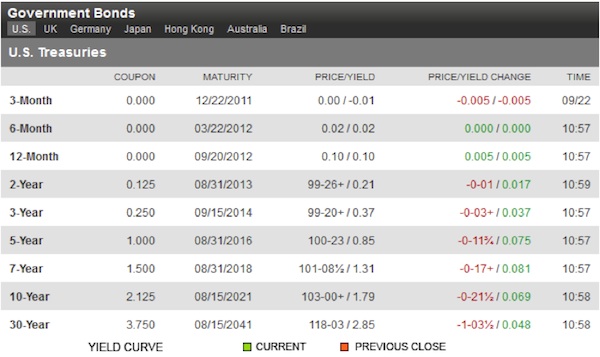

With Operation Twist as part of their new mix, they announced they would sell short-dated and buy long-dated treasuries. This sent the ten-year yield down to 1.72% (yields were already dropping), although as I write it is back up to 1.79%, which without the recent action would be the all-time low. The 30-year is below 3%, at 2.85%, which makes those of us who have been predicting such an event for many years finally right. I think I will just savor the moment and not make any more predictions for a week or so. It was a long time coming. It would have gotten there anyway, even without this Fed action. Which makes what they did impotent and pointless. More below.

However, such low rates are not cause

for merriment but for thoughtful pause, as low rates might be good for the

government and for those looking for mortgages, but they threaten to wreak

havoc on pension plans, as the bond portfolios on which they are built are

paying less and less, and that means they are becoming more and more underfunded,

and stocks are not helping. The problem pension fund trustees have is that

lower yields require them to raise their assumption for future liabilities, which

must be discounted at a lower rate. Lower bond yields, like falling share

prices, increase funding gaps.

While few are mentioning this aspect, Spencer Jakab of the FT sent me this note: “A sensitivity study by Credit Suisse done in mid-August shows how big an impact this can have. The underfunding for S&P 500 members was then an estimated $390bn. A 25 basis point fall in discount rates would have inflated the deficit to $435bn – about the same as 4 percentage points of investment underperformance this year. In August alone the deficit among the broader S&P 1500 widened by some $75bn, Mercer Consulting found. Slumping equities and bond yields brought the deficit from 12 to 31 per cent since April alone.”

Not to mention what low rates do to people who are trying to live off their savings. How can you survive on 1% yields from a small income portfolio? That means you start reaching for yield in places that are not as safe or liquid, which is precisely what we do NOT want our retirees to be doing. Wrong, wrong, wrong. An unintended consequence of this Fed policy is that retirees are being put at serious risk. And it is an important consequence. So many retirement plans were formed ten years ago, assuming they could safely withdraw 5% a year. Now that is difficult, at least if we’re talking “safely.” There is going to be a plethora of schemes to entice retirees with “safe” higher-yielding investment programs. Please, remember that there are no free lunches. If you are getting above-market yields, you are taking above-market risks.

Now, let’s look at what the Fed is actually likely to do. They have indicated their actions will occur over the next nine months. This also means they will sell most of their short-term treasuries and increase their duration, but not necessarily their risk. It is still US government debt. These projections are from Bridgewater.

Treasuries the Fed will likely sell:

|

|

What the Fed Has |

Likely Sales |

|

0-1 Years |

$138 |

$138 |

|

1-2 Years |

$156 |

$156 |

|

2-3 Years |

$221 |

$106 |

|

Total |

$515 |

$400 |

On average, $400bn at 1.5-year maturity

Treasuries the Fed will likely buy:

|

|

Eligible Total |

Eligible Outstanding |

Eligible New Issue |

Likely Purchase |

|

|

6-7 Years |

$353 |

$179 |

$174 |

$140 |

|

|

7-10 Years |

$581 |

$383 |

$198 |

$160 |

|

|

10-30 Years |

$521 |

$395 |

$126 |

$100 |

|

|

Total |

$1,455 |

$957 |

$498 |

$400 |

|

Rates have already moved in anticipation, as seen below.

One has to go out beyond 5 years to get more than a 1% yield. Who is buying this stuff? Any pension plan doing so is locking in low returns and underfunding for that period. This is just a disaster in the making in the pension and insurance world. If you couple that with a recession, a Muddle Through Economy, and a secular bear market, it is a prescription for a pension-funding train wreck of epic proportions, which means that the large companies will have to start writing checks, which will be a hit on earnings.

Note: Adding to pension concerns about the stock market, the ECRI weekly leading indicator has been down for six of the last seven week. More evidence that we are in for a real slowdown, if not a recession, sooner rather than later. This just in from the Wall Street Journal:

“Providing fresh evidence of weakening global trade, FedEx Corp. said Thursday it is cutting capacity and trimmed its full-year earnings forecast amid weaker demand, mainly due to slowing sales of consumer electronics made in Asia.

“The news comes as a slide in Asian air cargo traffic that started in July has shown no immediate signs of abating. The slowdown extends to the makers of perishable foods, high-end apparel and automotive and industrial parts that fill the holds of planes flown by FedEx and rivals such as United Parcel Service Inc. and Cathay Pacific Airways Ltd.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

“‘The consumer just doesn't have an appetite’ for spending more, Chief Executive Fred Smith said during a post-earnings conference call. As a result, he added, ‘we don't anticipate a significant peak [shipping season] this year.’” –Bob Sechler of the WSJ

But that’s just it. What happened with QE2? The money went into commodities and stocks (for which Bernanke again took credit), giving us inflation and a good feeling. But the economy, in terms of jobs, hours worked, incomes, and GDP, went south or sideways. Where was the carry-through? I somehow don’t remember that the stock market was part of the dual mandate, yet Bernanke listed its rise among the results of QE2. My bet is that with QE off the table, that will come to be seen as a temporary rise. A sucker’s rally.

And now that we have used that QE bullet, where are we? The stock market is tanking, as are commodities. Bond yields are making new lows. The dollar is getting stronger. Can someone tell me why we went through this exercise? It seems we are right back where we were, yet with even more uncertainty. And now we start something that my Dad would call a piss-ant (a small, rather noxious and foul variety of Texas ant) program called Operation Twist, which has no real hope of doing anything that will help the dual mandate. It simply creates the illusion the Fed is doing something.

I said at the time of the 2nd QE that the main problem I had was that we were wasting a bullet that we would (and now do) need when the next liquidity crisis came. And we have now kicked inflation up. As Rob Arnott wrote me in a private message, when you look at the next four months, which will “drop off” the year-over-year rate of inflation, it’s not pretty. Core could easily run up to more than 2.5%. The Fed may have handcuffed itself at the very time we need some liquidity. QE2 was a very bad and ill-conceived move, as is the current one. It is not smart to mess with Mother Market. (Can anyone say Fisher for Fed Chair?)

The US Government Is in the “No-Money-Down” Mortgage Business

The Fed was very clear in its statement that it wants mortgage rates to go down. But anyone with a pulse knows that the problem in the housing market is not that rates are too high. Dropping rates another 25-50 basis points is not going to help all that much if you can’t get the 20% down you need to finance a house, let alone get a nonconforming loan or, God forbid, a jumbo loan. With banks feeding into the market “REO” homes they get from foreclosures, it will be several years until we get close to a bottom in housing. But new homes are being built. So what gives?

This week I went to a fund presentation on new-home construction and sales. I was invited by a very knowledgeable real estate consulting firm (John Burns), and I was interested to know, how do you raise money in this market for new-home “spec” construction? The numbers and the company sales history they presented looked very impressive, but I could not figure out how they were closing the rather significant number of homes per development they did. No one else I knew of was close, from what I have seen (I watch these things). When the person who presented sat down, I looked at the mailer they send out by the millions. They send it to apartment renters. It says, “Why would you rent an apartment when you can buy a new home for $699 a month with NO MONEY DOWN?” And at very low rates, I might add.

These are starter homes, smaller but quite nice. (Note: a lot larger than the houses I grew up in with three siblings!) But they are on the outskirts of town, and that triggered a thought in the back of my head. Joan McCullough had tipped me to this.

“Are you using USDA financing to get the no-money-down?” The short answer was yes, along with FHA (3% down) and VHA. And what, you may be asking, is USDA financing? And how do I get some?

The USDA is the US Department of Agriculture. They currently have $24 billion they can use for government-guaranteed financing of homes (up from $12 billion last year). This is not Fannie or Freddie, this is the good old US D of A. As in farms and stuff (and food stamps and housing and… basically they got all these odd mandates long ago, when congressional agricultural committees wanted to expand their power). From Real Estate Economy Watch:

“Founded in 1949 to spur home sales and development in rural areas, the US Department of Agriculture’s popular direct and guaranteed rural housing loans today are one of the few places in America you can still get a mortgage with no money down at competitive rates.

“Borrowers don’t have to be lower income; in fact they can make slightly more than the median. To qualify for the government guaranteed loans, borrowers can earn up to 115 percent of the median income for the area. Nor do they have to buy in a rural area. They can live relatively close to a major urban area or in a popular resort community, however qualifying areas were recently redrawn to comply with the program’s rural mandate.

“Best of all, no down payment is needed to get financing through approved lenders, which makes the USDA program more attractive to borrowers who qualify than FHA.” (emphasis mine)

And there are actually subsidies available, so that you might not need to make the entire payment. Now, you can’t use this to buy a McMansion. You have to be in a rural area, which has come to be defined as outside the city limits (except in certain areas). There are income limits. The program does attempt to help lower-income families, and I am not trying to be snarky here, but these are government-guaranteed loans (read: taxpayer-guaranteed) at 100%, being handed out in areas where in the city homes are going into foreclosure and need someone to live in them, yet right outside the city you can buy this cute new home. Which is a situation more or less guaranteed to keep home values down in the rural outskirts, yet we want first-time buyers to snap these up!

The intention here is all well and good. And the buyers are seeing it as a way to reduce their monthly payment, and a house is still the American Dream. And, over time, it will be. If they stay in them long enough and don’t need to move, etc. I just think the unintended consequences (there are those words again, as we’re talking about a government project) are likely to be larger than anyone thinks.

I invite you to go to http://www.rurdev.usda.gov/Home.html. Look around. Notice that 4 of the first 5 press releases on the home page have the words job creation in their titles. Plus a lot of other current buzz words, like energy, environment, etc.

This whole side trip got started with our analysis of the Fed and its recent actions. Let’s quickly return, before moving on to Social Security. This week’s action is not useful. It falls under the category of “Let’s do something to show we know there is a problem.” It will provoke suspicion or opposition among those of a conservative monetary bent, probably hurt small and medium-sized banks (as it drives down the yield curve, which bankers depend on to make money), and lower interest rates for savers.

Crash Alert?

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

This is from my good friend Art Cashin today (he’s head of floor operations of UBS, and you see him all the time up on CNBC). I thought it should go here, after the market action of the last few days. Just as a heads-up.

“The Thursday/Monday Syndrome – We had suggested yesterday that we should probably explore the history of what old fogey traders refer to as the Thursday/Monday syndrome. While it would be pretensions to say that was prophetic, it was, to say the least, serendipitous, for yesterday’s action looked like the perfect first step in a Thursday/Monday setup.

“We had intended to give you a more thorough history of the syndrome with lots of analytical examples starting with the classic one – October 1929. Unfortunately, events are moving too fast this week, so we have neither the time nor space to wax poetic on the topic. So, you will just have to rely on my recollections of 50 years of watching markets and hundreds of nights studying market history.

“The classic Thursday/Monday syndrome starts with the kind of action we saw yesterday. The markets open under pressure and selling accelerates in swelling volume. By early afternoon, there is a virtual stampede of selling. Then, later in the session, stocks stabilize a bit based on some reassurance. On Thursday, October 23, 1929, that reassurance came in the form of Richard Whitney bidding ‘205 for 10,000 steel’ on behalf of the bankers’ rescue pool. (Read a terrific account in the chapter ‘The Crash’ in Fredrick Lewis Allen’s marvelous and essential ‘Only Yesterday’.)

“The action on Friday (and Saturday in the case of 1929) is uneven, often ending choppily steady or somewhat weaker.

“Then on Monday, the trapdoor opens with liquidation and margin calls bringing tsunamis of selling.

“Is that what’s going to happen? Who knows? If it were that easy, kindergarten kids could do this. But chance favors the prepared mind. Old fogeys will guard against undue risk and exposure. Some may even get out a special shopping list. They will set their basket right, put in silly bids and hope some panicky soul throws a bargain in. Recall the story of the floor messenger boy, who, in 1929, according to legend, bought White Sewing Machine with his silly bid of one dollar when all other bids canceled.

“One final note on the syndrome. Not infrequently, the Monday massacre spills over into Tuesday morning – a capitulation bottom in mid-morning resulting in a massive reversal to the upside.”

Is Social Security a Ponzi?

Breathes

there a man with brain so dead

Who

never to himself hath said,

“Social

Security looks like a Ponzi Scheme?”

- With apologies to Sir Walter Scott

Governor Rick Perry has been getting slammed of late for his comment that Social Security is a Ponzi scheme. Note: This is NOT an endorsement of Perry or any other candidate; it is a segue into the more important issue of Social Security.

Perry is not saying anything that has not been said for over 20 years. I seem to remember that back in my younger days (as in the ’80s) I actually published a book on Ponzis. The classic Ponzi is where you get money from one group and then find another group to pay the “returns” to the first, and so on, until you run out of people and the game is up. The difference between a Ponzi and Social Security is that SS is legal and is done in full view of the public with everyone knowing the deal.

As long as each succeeding generation is willing to pay and is large enough, SS can go on. But now we have trillions in unfunded liabilities. All Perry is suggesting is that we admit the problem and fix it. Not exactly radical or suggesting we end Social Security, as Romney and the others claimed.

(Side note. I found that use of the attack mode disgusting and totally devoid of the leadership I want to see on that stage. It was trying to create a “gotcha” moment. Why not turn it into a teaching moment, to say how you would fix Social Security or admit you have no clue as to the true nature of the problem? Afraid to touch the third rail of Social Security? Then get out of the race. You have no ability to lead this country through what will be a crisis presidency if you can’t even admit to some basic, obvious truths. And how will you even get to the real problem, Medicare?)

Most of the “fixes” are some combination of increasing the retirement age, raising the cap on how much is subject to SS taxes, and/or some form of means testing. Social Security can be fixed if the political will is found to do one or all of those. Some comments on those choices:

First, there is some resistance to means testing, as it would be an admission that Social Security is a form of welfare and not a “savings account” that is in some hidden lock box. By now, anyone with a neuron firing knows there is no lock box and the Social Security funds are an entry into a government accounting book that don’t really exist except as an IOU. Politicians of all stripes have used the Social Security money to pay for other government expenses. Those funds were even counted to offset the deficit, although now that Social Security is no longer in a surplus, that has gone away.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Isn’t that what Ponzi did? He took money from one group, telling them they would get it back later, and then spent the money with another group, telling them the same thing.

OK, think using the term Ponzi is harsh? Some Republican theme? Then let’s quote uber-liberal Paul Krugman from 1996:

“Social Security is structured from the point of view of the recipients as if it were an ordinary retirement plan: what you get out depends on what you put in. So it does not look like a redistributionist scheme. In practice it has turned out to be strongly redistributionist, but only because of its Ponzi game aspect, in which each generation takes more out than it put in. Well, the Ponzi game will soon be over, thanks to changing demographics, so that the typical recipient henceforth will get only about as much as he or she put in (and today’s young may well get less than they put in).”

Let me say, I am all for Social Security. While I supplement my mother’s income, her Social Security check is very important to her. Not enough to live on, but every bit helps. (I have friends whose parents’ sole income is Social Security, and I totally get how small it is in today’s world.)

I also have seven kids. Hopefully, most or all of them will not need Social Security when they retire in 40-50 years. But some might. I want it to be there for them if they need it. But if we don’t properly fix it, it won’t be. I want it fixed.

I turn 62 next month. I am eligible for Social Security. I have paid in a lot of money over the last 45 years of working, for the last 20 years at the max level (with some off years here and there). Am I “due” something? Based on the current law, I am. But I must confess that life has been good of late (there have been times when I thought I would need every penny of Social Security!).

I think Social Security should be means tested. We should recognize it for what it is, for what Krugman called it: a redistributionist scheme. And a good and necessary one from the perspective of civilized society. Means testing would go a long ways to “fixing” the problem. But it doesn't get us there.

We need to raise the retirement age, and by more than a few years. And this is where I get called a heartless (insert expletive)! “How could you want us to work until 70 or even later? How can we do that? Is that fair?”

Let’s use as our model that icon of the left, the King of Compassion, President Franklin Delano Roosevelt (FDR). He created the Social Security Act in 1935. He put the retirement age at 65. From today’s perspective, that seems about right, if not a little early. But what did it look like back then? I refer you to a report from the US Senate in 2006 on life expectancy in the US. Interesting reading, but for our purposes we will scroll down to page 26 and the detailed life-expectancy tables. (http://aging.senate.gov/crs/aging1.pdf)

In 1900, the average life expectancy was 47 years (shockingly, the life expectancy for black males was only 32). By 1930 it was 59, which, if they kept such records then, would have been what they were looking at when the designed Social Security. In 1935 it had risen to 61.

So FDR set the retirement age four years above the average life expectancy. So much for compassion. He (they) assumed you would work into what was for them advanced old age. Today, 62 does not seem all that old (at least from my vantage point!). Look around – there are lots of people in their 60s and 70s with very active lifestyles.

Why is that? Let’s fast-forward. In 2003 life expectancy was up to 77. Today it is 79 and change. Life expectancy has been rising more or less steadily rate at about 1 year for every 4 years of the calendar. So that means that in 40 years life expectancy, if it continues as it has, will be around 90. Under today’s laws one could retire at 62 or 65 or 67 and, if you just lived an average lifespan, get far more in benefits than you paid in. Remember, 90 will just be the average.

So when someone suggests that we move the retirement age to (gasp!) 70 in a few decades, I just smile and think back to what FDR would do. If Social Security had been set up to track life expectancy in 1935, when it was formed, then retirement would be set at 83 or 84 today! Not exactly the golden-years concept, is it?

Catastrophic Success

But then we come to what I call Catastrophic Success. Advances in medicine and biotech in the next 10 and then 20 years are going to radically alter life expectancy. Alzheimer’s disease will be gone. I will tell you about a potential cure for cirrhosis of the liver (and all kinds of cirrhosis) in a future letter. Heart disease? Soon be something that can be dealt with. Diabetes? Will be controlled or gone.

And cancer? There are numerous approaches, but I am following one that will be in human trials next year and that, in numerous mice studies, shows the potential to be a silver bullet for cancer in general, and relatively inexpensive (not a public company).

I could go on and on, but the point is that this Boomer generation is not going to live up to its part of the generational Social Security bargain. We are not going to die on time in anything close to the actuarial certainty the government now assumes (nor do the private pension funds!). Short of a Soylent Green-type debacle, Boomers will not only break the deal, they may destroy it, if we do not tie Social Security to the average lifespan.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Health care will soon be a Catastrophic Success. Wildly successful from the point of view of the individual, but a catastrophe from the point of view of Social Security. And we are debating whether to raise the retirement age from 67 to maybe 70 at some distant time in the future?

We need to be raising the retirement age by one year every four years. That means in 20 years the retirement age needs to be five years higher. I can hear the screams and moans from those 45 and under. “What a heartless [insert expletive] Mauldin is. How long does he think I should have to work? It is all well and good for him,” etc.

I want the Social Security system to be there for my kids in 40 years. And not dealing with the rapid age increase is one way to make sure it is not. OK, I will offer a way to retire earlier. If you agree to forego any new medical treatments introduced after, say, 2014, then I will say you get to retire at the current SS levels. Like that trade? I didn’t think so.

Think I am being overly optimistic about lifespan? I am not even close. I am having a small private dinner in a few weeks with Mr. Optimistic Future himself, Ray Kurzweil (among other books, he wrote The Singularity Is Near – a very important work on the waves rolling toward us from the future). We will talk of many things, and I hope to get him to contribute to my next book, The Millennium Wave, which is all about how the world will look in 20 years. If we stay on his track, then shortly after that time (by 2032) we will be regenerating the entire human body. Ray (and many others) see a path to humans living to 150 and beyond, in good health, with younger bodies. It doesn’t make you immortal. You can still look the wrong way and step in front of a London bus or climb the wrong mountain and fall off. (Note: Ray does see a path to immortality of a sort, when we can download our minds into machines and then reverse the trip. But that’s a whole different level of discussion and farther down the road.)

I am talking to scientists who are doing the human trials on the first real regeneration of a human organ, the cardiovascular system. How about a 50-year warranty on your new heart and cardio system? Then it’s on to the next organ system. One down, 203 to go. (Start with cardio, as it’s the easiest to deliver the targeted stem cell to.) Sadly, it will be done in Asia and not in the US, so we lose tens of thousands of high-paying jobs and don’t get to train a cadre to physicians on how to do it. Nothing against Asia, but this is US-developed technology … that would take five years to get through the FDA. For the management team of the company doing the work, who really do hate the concept of people dying from old age, that’s too many deaths as a result of waiting. And there is still a long way to go before we get true regeneration. We (as in those of us over 60) won’t have time for 20th-century regulators to get in the way. The clock is ticking.

(Side note for those of you who don’t want to live a very long time: I am sorry your life is so boring. I see nothing but wonder and new worlds to explore and cultures to find and tens of thousands of books to read. Ask me in a few thousand years how it’s going. I’m in no hurry to knock on the gates of the Other Side. We get there soon enough.)

Social Security as it is set up today is close enough to a Ponzi scheme for government work. That can be changed, but we have to have the will to do so. Let’s hope that not just Perry can decide to lead us there.

Europe and Breaking the Light Speed Barrier

Heads up, you Junior Rocket Man Kids (remember those days?). Physicists are doing amazing things. My son Trey and I got a private tour this summer of CERN, the great physics lab in Geneva. Very cool. But Wall Street is also legendary for the number of physicists it hires to work on high-frequency trading programs. Evidently, they have figured out how to get trades done 190 milliseconds in the future. Is the race on to see who can cross the one-day mark? What is the speed of light when compared to the speed of money?

“Nanex: On September 15, 2011, beginning at 12:48:54.600, there was a time warp in the trading of Yahoo! (YHOO) stock. HFT has reached speeds faster than the speed-of-light, allowing time travel into the future. Up to 190 milliseconds into the future, or 0.19 fantaseconds is the record so far. It all happened in just over one second of trading, the evidence buried under an avalanche of about 19,000 quotes and 3,000 individual trade executions. The facts of the matter are indisputable. Based on official UQDF/UTDF exchange timestamps, there is unmistakable proof that YHOO trades were executed on quotes that didn't exist until 190 milliseconds later!” (http://www.nanex.net/Research/fantaseconds/fantaseconds.html)

Going forward in time is cool, and the same day I got the above notice I read that the physicists at CERN and in Italy have found subatomic particles that move slightly faster than the speed of light, making it possible to travel back in time (only a few nanoseconds, but it’s a start):

“But now it seems that researchers working in one of the world's largest physics laboratories, under a mountain in central Italy, have recorded particles travelling at a speed that is supposedly forbidden by Einstein's theory of special relativity.

“Scientists at the Gran Sasso facility will unveil evidence on Friday that raises the troubling possibility of a way to send information back in time, blurring the line between past and present and wreaking havoc with the fundamental principle of cause and effect.

“Researchers on the Opera (Oscillation Project with Emulsion-tRacking Apparatus) experiment recorded the arrival times of ghostly subatomic particles called neutrinos sent from Cern on a 730km journey through the Earth to the Gran Sasso lab.” (http://www.guardian.co.uk/science/2011/sep/22/faster-than-light-particles-neutrinos?newsfeed=true)

Now, just in case you buy this (and if you did, contact me about a bridge I have), let me attempt to disappoint. First, as my curmudgeon PhD from MIT and VC friend Bart Stuck writes, “I think they both had time-stamp errors.” I can’t vouch for the Swiss and Italians, but I would bet the keys to the kingdom that there is a computer glitch at the NYSE. High-frequency trading (HFT) is distorting the markets. It is enriching a few pockets (and that of the exchange), and I simply do not see how it is in the interest of the public to allow it.

I also know that fighting HFT is spitting into the wind, as faster tech comes along every few months. If you force the HFT funds to put their servers across the street (losing the time advantage of not being co-located with the exchange servers – milliseconds count!), it will only be a few years until technology has given the edge back to them. In ten years, when artificial intelligence and connection speeds are far more advanced, how will human traders compete? Hire yet another AI to fight back? Wire yourself into the system (already being done, by the way, in rudimentary ways)?

The only way to effectively end HFT is for the exchanges to stop giving incentives for such trading. I can see the profits for the traders and the exchanges. I just don’t see the benefit to the rest of us. The SEC should step in and settle some hash over missed time stamps. If a small broker-dealer has a wrong time stamp, they are all over us, and you can bet there are fines. Something is wrong here. If one trade can go “back to the future” then how many more? Really? A one-off or a symptom? And to finish this on a light note, here’s a cartoon from my favorite cartoonist, Gary Larson.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

It is getting close to time to hit the send button. It has been good to be home for almost seven weeks and let my body recharge, and spend more time with my kids and grandkids. Life is not easy for all of them at times. Poor Lively (perfect angel that she is) was getting a “spanking” as I left for the airport. I can’t imagine her doing anything naughty, but her mother (Tiffani) thought otherwise. Two of the adult kids needed some help. It is never the same two at the same time. And on and on.

This trip should be fun. I love London. And I’ll be in Malta with my European partner, Niels Jensen of Absolute Return Partners. I will be hosting CNBC Squawk Box on Wednesday in London. Then it’s on to Dublin and lots of meetings, as I try to get a handle on the crisis there (my first trip to Ireland). And a little time driving through the Irish countryside, on our way to Galway. Then to Geneva to be with friends and clients for two days as I turn 62. First, dinner with the always fascinating Lord Alex Bridport (the only lord I know, so I love applying that title) and then a birthday dinner hosted by Herwig van Hove of Notz Stucki. And then it’s back home to Texas.

In four weeks I head to Cape Town, South Africa, where I will speak at the Momentum Wealth Investment Summit, and then, back in Texas, I’ll speak November 6 for a charity fund-raising event sponsored by Hedge Funds Care, a wonderful group that raises money for children’s causes. You can learn more by going to http://www.hedgefundscare.org/event.asp?eventID=74. I hope to see you there!

Have a great week and enjoy the weather if you can. The forecast for Europe is beautiful.

Your wondering if he’ll find his Irish ancestors analyst,

John Mauldin

John@FrontlineThoughts.com

Disclosures

Altegris Advisors LLC is an SEC-registered investment adviser that advises alternative strategy mutual funds that may pursue investment returns through a combination of managed futures, fixed income and/or other investment strategies.

Investors should carefully consider the investment objectives, risks, charges and expenses of Altegris alternative strategy mutual funds. This and other important information is contained within the individual Fund’s Prospectus, which can be obtained by calling (877) 772-5838. The Fund Prospectus should be read carefully before investing. Altegris alternative strategy mutual funds are distributed by Northern Lights Distributors, LLC member FINRA. Altegris Advisors, JP Morgan Investment Management Inc., and Northern Lights Distributors are not affiliated.

MUTUAL FUNDS INVOLVE RISK INCLUDING POSSIBLE LOSS OF PRINCIPAL.

The Fund is “non-diversified” for purposes of the Investment Company Act of 1940, which means that the Fund may invest in fewer securities at any one time than a diversified fund. When the Fund invests in fixed income securities or derivatives, the value of your investment in the Fund will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities or derivatives owned by the Fund. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities. Other risk factors include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments). These risks could affect the value of a particular investment by the Fund possibly causing the Fund's share price and total return to be reduced and fluctuate more than other types of investments. To respond to adverse market, economic, political or other conditions, the Fund may invest 100% of its total assets, without limitation, in high-quality short-term debt securities and money market instruments. The Fund's indirect and direct exposure to foreign currencies subjects the Fund to the risk that those currencies will decline in value relative to the U.S. Dollar, or, in the case of short positions, that the U.S. Dollar will decline in value relative to the currency that the Fund is short.

Currency rates in foreign countries may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates and the imposition of currency controls or other political developments in the U.S. or abroad. In addition, the Fund may incur transaction costs in connection with conversions between various currencies. The Fund will invest a percentage of its assets in derivatives, such as futures and options contracts. The use of such derivatives may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities and commodities underlying those derivatives. The Fund may experience losses that exceed losses experienced by funds that do not use futures contracts and options. There may be an imperfect correlation between the changes in market value of the securities held by the Fund and the prices of futures and options on futures. Although futures contracts are generally liquid instruments, under certain market conditions there may not always be a liquid secondary market for a futures contract. As a result, the Fund may be unable to close out its futures contracts at a time which is advantageous. Trading restrictions or limitations may be imposed by an exchange, and government regulations may restrict trading in futures contracts and options. Because option premiums paid or received by the Fund are small in relation to the market value of the investments underlying the options, buying and selling put and call options can be more speculative than investing directly in securities. Over-the-counter transactions are subject to little, if any, regulation and may be subject to the risk of counterparty default. A portion of the Fund's assets may be used to trade OTC commodity interest contracts, such as forward contracts, option contracts in foreign currencies and other commodities, or swaps or spot contracts. A substantial portion of the trades of the global macro programs are expected to take place on markets or exchanges outside the United States. Some foreign markets present additional risk, because they are not subject to the same degree of regulation as their U.S. counterparts. Trading on foreign exchanges is subject to the risks presented by exchange controls, expropriation, increased tax burdens and exposure to local economic declines and political instability. An adverse development with respect to any of these variables could reduce the profit or increase the loss earned on trades in the affected international markets. International trading activities are subject to foreign exchange risk.

The Fund may employ leverage and may invest in leveraged instruments. The more the Fund invests in leveraged instruments, the more this leverage will magnify any losses on those investments. Leverage will cause the value of the Fund's shares to be more volatile than if the Fund did not use leverage. The Fund may take short positions, directly and indirectly through the Subsidiary, in derivatives. If a derivative in which the Fund has a short position increases in price, the underlying Fund may have to cover its short position at a higher price than the short sale price, resulting in a loss. Structured notes involve leverage risk, tracking risk and issuer default risk. Taxation Risk involves investing in commodities indirectly through the Subsidiary, through which the Fund will obtain exposure to the commodities markets within the federal tax requirements that apply to the Fund. However because the Subsidiary is a controlled foreign corporation, any income received from the Subsidiary’s investments in Underlying Funds/Pools will be passed through to the Fund as ordinary income, which may be taxed at less favorable rates than capital gains. Underlying Funds/Pools in which the Subsidiary invests will retain investment managers and be subject to investment advisory and other expenses which are indirectly paid by the Fund. As a result, the cost of investing in the Fund may be higher than other mutual funds that invest directly in stocks and bonds. Each Underlying Fund/Pool will pay management fees, brokerage commissions, operating expenses and performance based fees to each manager it retains. Performance based fees will be paid without regard to the performance of any other managers retained or to the overall profitability of the Underlying Fund/Pool. Underlying Funds/Pools are subject to specific risks, depending on the nature of the managers they retain. There is no guarantee that any of the trading strategies used by the managers retained by an Underlying Fund/Pool will be profitable or avoid losses.

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.