Capital Excess

-

John Mauldin

John Mauldin

- |

- December 3, 2021

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinWhy do we invest? Everyone has their reasons, but funding retirement may be the most common one. Whenever the time comes, we want to relax in comfort and security.

Yet this whole “retirement” idea is really quite new. For most of human history, almost everyone worked as long as they physically could, then expired soon after they couldn’t. Capping your life with a few years of leisure wasn’t an option. Without an extended family that would take care of you, life was “solitary, poor, nasty, brutish, and short” (to quote Thomas Hobbes). Comfortable retirement is possible now, or at least we hope it is. But we’re never quite sure—which is why we stay nervous about our portfolios.

“Self-directed” retirement investing is also new. Other than Social Security, US retirement benefits came mostly from employer and union pension plans until just a few decades ago. Your employer would put money into a big pool where professionals would invest it on your behalf and pay you some kind of “defined benefit” upon reaching retirement age. This was normal and worked pretty well.

In 1978 Congress passed a law allowing tax-deferred compensation for bonuses and stock options. The relevant clause was section 401(k). Benefits consultant Ted Benna saw it could be used to create tax-advantaged savings accounts. Companies jumped on the idea quickly because it was simpler and less expensive than funding their defined benefit plans. Workers liked the idea of being in control of their retirement money. Today, the old-style plans are rare in the private sector, but they remain common in state and local governments.

This new arrangement, while an improvement in some ways, generated different challenges. Giving workers control over their own investments presumed they would invest wisely, which is often not the case. It turns out humans are, well, human, with evolutionary survival traits that are not necessarily the best traits for investing. An entire subset of economics called behavioral economics has evolved (pun intended) to describe our human foibles.

But the even bigger problem is the employers who kept DB plans without adequately funding them and/or generating returns sufficient to pay the promised benefits. It is a systemic problem that affects others. Today we’ll discuss this problem and some of its macro-level consequences.

Funding Gap

I’ve written about the underfunded pension problem many times, most recently in October 2019 (see Our Nuts Are in Danger). A few months earlier I had said Your Pension May Be Monetized. It’s a slow-moving crisis that, in theory, shouldn’t be hard to avoid. Fixing it requires cooperation by people with competing interests, so it’s still coming.

Nevertheless, there is some slight improvement. COVID recovery programs injected a lot of federal cash into state and local government coffers even as tax revenues rose (often dramatically) in many places, thanks to higher property values, capital gains, and increased consumer spending (which raised sales tax revenue).

This let some sponsors make additional contributions, some of which were long overdue. A recent Wall Street Journal report said California had transferred an extra $2.31 billion to its teacher and public worker plans (which is a step in the right direction but sadly a drop in the bucket). Connecticut threw in an extra $1.62 billion. New Jersey made its full actuarially-calculated contribution for the first time since 1996 and added another $500 million on top. Again, not nearly enough.

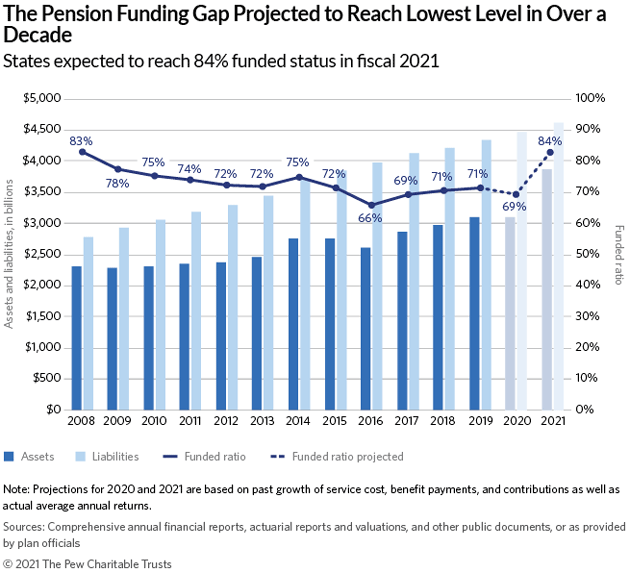

Nationally, a Pew Charitable Trusts report estimates the state plans will reach an 84% funded level this year, up sharply from 69% the prior year. If an 84% funding level could be maintained that would be very positive. Then again, that is the average of all states. Some states are dramatically underfunded.

Source: The Pew Charitable Trusts

Moreover, some of the improvement represents new Treasury debt. It was essentially a federal bailout under another name. The problem was transferred, not resolved.

But much of the funding ratio improvement came from gains in the existing plan portfolios. These gains exist mostly on paper, on the assumption the plans could sell all their assets at the current lofty market prices. That is a fantasy and so are their numbers.

It also doesn’t address inflation. Many plans give beneficiaries a “cost of living” adjustment based on CPI or some other benchmark. It’s been generally low for the last decade or two. This may not be the case going forward and I’m relatively sure their funding assumptions don’t reflect that possibility. The liabilities these funding ratios have to cover could be significantly bigger than expected. Even if inflation is only 4–5% for two years, that is a large change to their future liabilities.

Unwieldy Size

Back to all this new cash. Pension plan managers face the same challenge as other large investors: The more money you need to invest, the fewer choices are available to you. You can’t invest in the market when you are big enough to be the market. But staying in cash isn’t good, either, because it dilutes your returns and prevents you from achieving long-term objectives.

Some hedge funds and a few mutual funds try to solve this by closing to new investment when they reach an unwieldy size. Many more should do so. They don’t because it reduces fee income. They instead come up with “multi-strategy” programs far afield from the expertise that built their original record. (A multi-strategy format can work. I use some myself. Few managers make that transition well, though).

This isn’t a new problem, of course, and the nice thing is it’s also an opportunity for smaller investors and managers. Back in the 1990s I was involved in selling hedge funds designed specifically to seek “under-the-radar” financing opportunities that were simply too small for giant funds to pay attention. We were able to get very attractive returns for exactly that reason. (Sadly, those halcyon days came and went. What was by any standards remarkably good returns attracted large money and drove down the returns. Sic Transit Gloria.) This is still the case today though in different markets. There’s a sweet spot, which varies by asset class, where a manager is big enough to attract talent and “deal flow” but small enough to be nimble.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Pension plans make a big splash of allocating money to funds they claim are like this, but they really don’t. A $50 million allocation, which is big enough to swamp many niches, doesn’t even move the needle of a $10 billion fund. There simply aren’t enough niches or managers to let them invest that way. That’s why we see so many market segments stop achieving their historic returns when the institutions find them.

Let me give you a real-world example. Without mentioning the name of the fund, a group of managers split off from a well-known endowment fund to set up their own shop. Their largest initial investor was the endowment they left. They opened up to “outside investment” for $100 million. We were given a small piece of that because of personal relationships. The bulk of it went to other endowments. Here’s the problem: If you are a pension fund trying to put $50 billion to work, even assuming you could get $50 million into the fund, that would be 1/10 of 1% of your fund, not even a rounding error. You need to be putting $500 million to work at a time. Sadly, the returns on that size of investment are significantly lower (in general).

Yes, large pension funds are making even larger allocations to private equity, private credit, real estate, and venture capital, but because there is so much money in the system competition is driving down returns. It is most easily seen in the high-yield (junk bond) market. One might think it is individual investors reaching for yield. And to an extent, they are. But the simple fact is that endowment funds, pension funds, insurance funds, etc., act just like individual investors. They, too, reach for yield.

This is why the bulk of these assets go into indexed products (or variations thereof) that simply buy “the market” or, more likely, some collection of markets. And because the indexes are capitalization weighted, more money goes to the biggest names, making the indexes grow more and more top-heavy over time.

Irrational Exuberance

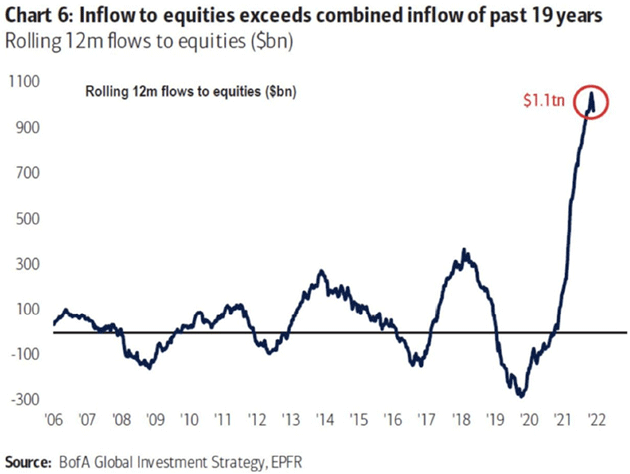

Worse, the incoming cash raises valuations at a time when other incoming cash is doing the same thing. Here’s a chart we shared in Clips That Matter last week. It shows year-over-year money flow into equities. You may notice a slight change recently.

Source: Jesse Felder

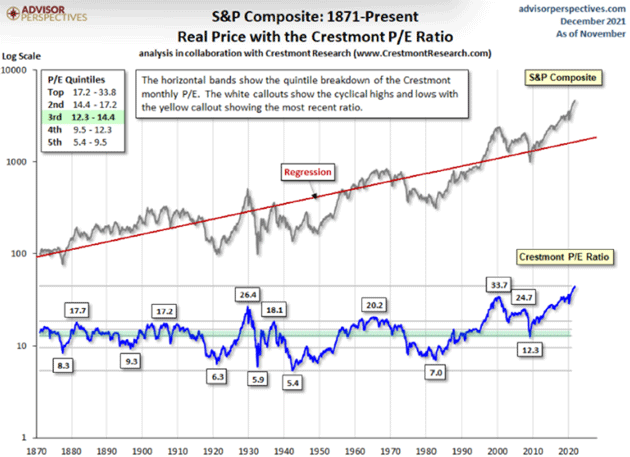

Needless to say, but I’ll still say it: This is not normal. Everything we see about today’s markets screams “overvalued.” Let’s look at some data from my friend Ed Easterling at Crestmont Research who provides the raw numbers to, again, my friends at Advisor Perspectives (it’s good to have a lot of friends).

First, the Crestmont P/E ratio is at its highest level ever. I really think Ed’s P/E ratio is the best out there in terms of taking into account history and trends. But you can do this with the Shiller ratio or the S&P data. It all shows the same result.

Source: Crestmont Research

As Jill Mislinski and Doug Short of Advisor Perspectives note:

“The Crestmont P/E of 43.9 is 198% above its average (arithmetic mean) and at the 100th percentile of this fourteen-plus-decade series. We've highlighted a couple more level-driven periods in this chart: the current rally, which started in early 2014, and the two months in 1929 with P/E above the 25 level. Note the current period is within the same neighborhood as both the tech bubble and the 1929 periods, all with P/E above 25 and is certainly in the zone of ‘irrational exuberance.’”

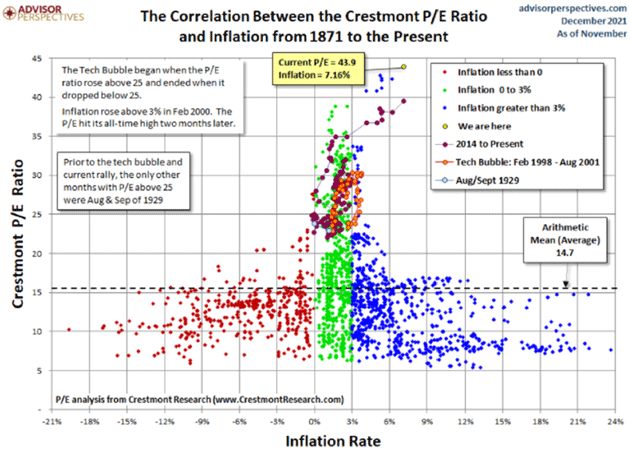

But that has to be put into context and sadly, the current context is not exactly bullish. You don’t have to be an economic rocket scientist to know that both inflation and deflation aren’t good for stock investments. Ed and I have written about that off and on for the last 20 years. Advisor Perspectives gives us a new graphical representation:

Source: Advisor Perspectives

(Click the link above for a larger version.) The “sweet spot” is generally when inflation is between zero and 3% and valuations are much lower. We are well past the valuation and inflation metrics of the tech bubble.

That suggests one of two things needs to happen: either inflation needs to drop dramatically or the stock market needs to drop significantly, or some combination of the two—at least from a historical perspective. Depending on how you measure standard deviation, we are somewhere between 4–5 standard deviations from the mean. Again, dramatically higher than the Roaring 20s (well more than double) or the tech bubble (more than 50% higher).

I keep repeating: Friends don’t let friends buy index funds (except as trading vehicles). But pension sponsors, by nature, don’t think in those terms. They have cash to invest and they have to put it in something. Right now, anything they do is enormously risky one way or another. I don’t know how this will end but I’m confident it will not end happily.

Jerome Powell, who is all but assured his continuing role as Federal Reserve chair, decided to remove the word transitory from Fed-speak and is talking about ending quantitative easing faster so that they can get on to actually raising interest rates and leaning into inflation. If he follows through on this signal, I will applaud him. Notwithstanding the bipolar market movements of the last week, I am not sure that investors will be as pleased. While I think that the market could rise into year-end (the typical Santa Claus rally), I am not as sanguine about the first half of 2022. The potential for a real bear market triggered by earnings compression and Federal Reserve actions is quite real.

The question of the day, and it is truly a question that I don’t have an answer to, is what will Jerome Powell do if the stock market falls 20% and inflation is still at 4%? And they haven’t even begun to raise interest rates? Does he follow the Fed’s mandate and lean into inflation, calling up his inner Volcker, or does he look to his unwritten mandate of giving the stock market what it wants?

Those of us who were in the “business” in the 1970s know they were burning effigies of Paul Volcker for his tight money policies. It was the right thing to do, but it was not popular on Wall Street.

I think Jerome Powell (can I call you Jay?) has the personality and personal financial stability (a nice way of saying that he is rich) to take the heat. The markets will adjust and go on to new heights, eventually.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

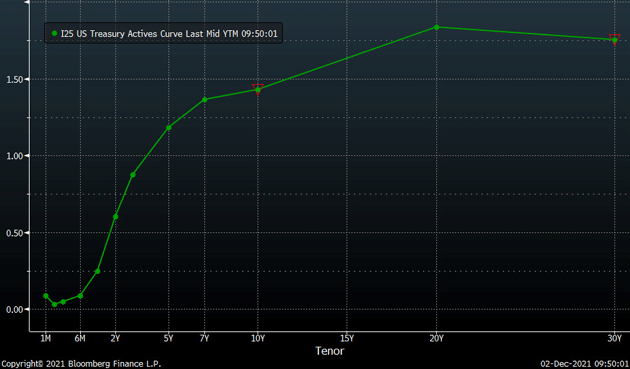

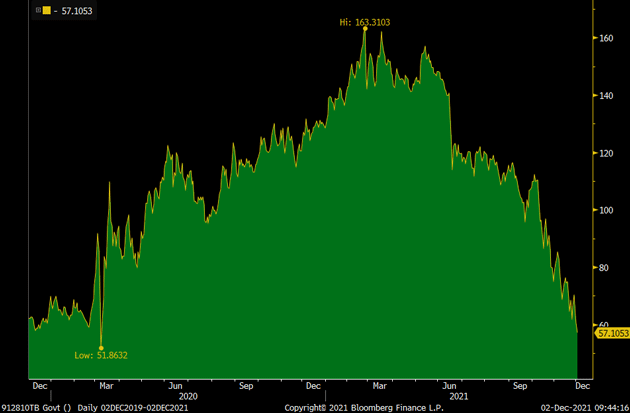

“Eventually” is the operative word, though. Interest rates are behaving oddly for a high-inflation environment. Long-term rates are falling and short-term rates except for the lowest end are rising. As a student of inverted yield curves, I can tell you this is what the beginning of an inverted yield curve looks like.

Source: Peter Boockvar

What if the Fed raises short-term rates to (gasp!) 1%? Or even slightly higher? You think that’s not a possibility? Tell me what inflation is going to be. How serious is Jay Powell going to be in fighting inflation? There are way too many known unknowns in our future to be complacent.

As Peter Boockvar wrote this last Wednesday:

“The yield curve continues to flatten today with the 2s/10s spread now at 82 bps. It was 102 bps on Monday, the day before Powell endorsed a faster taper. The 5s/30s spread is narrower by another 3 bps to just 57 bps vs 70 bps on Monday. AGAIN, historically the curve flattens when the Fed is tightening or is about to.”

Note how dramatically the 5s/30s spread has narrowed over the past few months and especially this week:

Source: Peter Boockvar

Unknown Territory

Next year is truly unknown territory. The Fed has signaled it will begin to reduce quantitative easing. Even though its balance sheet will be expanding, it is a tightening of monetary conditions. It remains to be seen how fast they will do it. There are other unknowns, too.

The Boomer generation that once blasted hiring managers with hundreds of resumes for each opening is leaving the workforce, one way or another. Subsequent generations are smaller because birth rates and immigration fell. Add in the COVID effects and we now have a severe labor shortage.

I am not sure we have processed how profound this change will be. Because workers are scarce relative to demand for their services, they have more influence. They can demand and receive higher wages. This is inflationary.

At the same time, available investment capital greatly exceeds the demand for it. This is one reason interest rates are persistently low. If you want to earn interest income by lending your capital, you are competing with many others who want to do the same. Borrowers naturally choose the best terms, so you get a race to the bottom.

In sum, we are shifting from a capital-constrained economy to a labor-constrained economy. I don’t think this is temporary. Yes, we’ll see ebbs and flows, but this is generally the way it will be for a while. Corporate CEOs will spend less time finding capital and more time finding talent. The tech world has been that way for some time. Now it’s becoming normal for every sector.

This will be a different investing environment than most of us have ever known. Quite frankly, we won’t be in the driver’s seat anymore. Businesses who need equity or debt financing will have many choices. We will have to give them reasons to choose us. But that’s not entirely new, at least to some of us. Anyone involved in “small” deals knows the intangible factors often matter more than the cold financial terms. That’s how you get the edge.

The giant funds will have far greater problems. Plans that are already underfunded are having to invest in overvalued markets that will swing to undervalued at some point, possibly just as the plans need cash to pay benefits. They will become even more underfunded and then have to face an investing environment where their size makes above-zero returns very difficult to achieve.

If you are counting on one of those funds to pay your living expenses for a long retirement, you may be in for a shock. Now would be a good time to start making alternate plans.

A Brief Commercial

While I would never profess to be like Bill Clinton, I feel your pain. Every quarter my investment manager partners and I lose access to a really nifty fund or program that simply says “we have all the money we need.” Or even worse, they are bought by a large private equity firm and access is shut down. We have teams devoted to developing new relationships. That being said, we are quite picky. We only want the “right stuff” to get on the shelves of the Mauldin Kitchen.

The good news is that we’re still small enough to be able to access some really incredible, at least to me, investment potentials that are too small to be on the radar of the larger funds. I am really proud of what my partners and my relationships have been able to blend into a well-stocked “Mauldin Kitchen.”

I encourage you to click on the link, talk to one of our very polite professionals and find out what is in my kitchen. I truly believe you will find something on our menu that puts a little spice into your portfolio.

Home for the Holidays and Black-Eyed Peas

This was a very difficult letter to write. I could literally expand this letter 4X and not even begin to mention all the data that reaches my inbox. When so much is happening that I can’t keep up, it reminds me of the old saying about “interesting times.”

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I am sorely tempted to make a quick trip to New York to be with friends (and Art Cashin who was sick and couldn’t make our last dinner). However, I think I will postpone that to next year and just enjoy the holidays in Puerto Rico. Shane and I are learning after three years that my fellow Puerto Ricans take holidays seriously. Lots of parties and fireworks. It is actually quite fun.

We are going to try to introduce my own traditional “New Year’s Day party.” For years, we would host a New Year’s Day party featuring a very special spicy black-eyed peas and bacon/ham, honey baked ham, cornbread, chili, etc., starting about noon going to 5 o’clock. Upwards of 150 people would show up. We would serve 10 gallons of black-eyed peas plus multiple gallons of chili and separately (never mixed) pinto beans. (Only pagans and Yankees put beans in their chili.)

Black-eyed peas are a southern tradition. My mother from Mississippi told me that they bring good luck. I didn’t like her black-eyed peas. No seasoning and bacon. I am told that in certain parts of the Northeast the tradition is sauerkraut. Ugh. My black-eyed peas are to die for.

On the anecdotal inflation front, the prime roast for Thanksgiving was $390, well over 20% increase. Ditto for mushrooms. Everybody was complaining about the cost of the food. My son Trey has moved to Florida to take his dream job and he and his SO are finding that rents are at least 25% higher than just eight months ago. The OER number used by the BLS to compute CPI is so broken. The good news is his salary is also way up. Bacon is $12 a pound here in Puerto Rico. I know it is anecdotal, but all my kids are complaining about prices. Here’s hoping Jay sticks to his inflation-fighting DNA.

And with that I will hit the send button. You have a great week. And don’t forget to follow me on Twitter!

Your overwhelmed with information analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.