An Opportunity in the Chaos

-

John Mauldin

John Mauldin

- |

- August 2, 2019

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinYou Think the Fed Is One and Done?

Awash in Debt

Investment Grade Zombies

Selling Under Pressure

Falling Apart Quickly

Navigating the Waters Ahead

New York, Maine, New York, and Montana

One reason the economy is so fascinating is the way things just… happen. Growth blossoms if everyone just follows their own incentives and nothing gets in the way. The courage, vision and passion of entrepreneurs and those who risk their money backing them is one of the most inspiring aspects of modern civilization. Adam Smith’s Invisible Hand of now tens of millions of businesses, small and large and giant, working to produce and deliver inventions, technologies and cures that help us all.

Think about ants. They’re marvelous creatures. No individual ant knows how to build a colony, or is even aware it is doing so, but it happens because they’re supremely efficient at simple things. Go to that smell, pick up the object, follow that other ant, repeat. The end result is greater than their tiny brains can comprehend.

But like ant colonies, economies sometimes fall apart. In human terms, we call those times “recession.” We can recover from them, but they set us back.

However… they don’t have to set all of us back. Unlike ants, we can see the big picture. And if we see it clearly, recessions can be opportunities. Today I’ll describe just one of the many I think are coming. Of course, before that opportunity develops, people who don’t get out of the way are going to lose a great deal of money.

The good news is an opportunity will follow, as surely as morning follows night.

You Think the Fed Is One and Done?

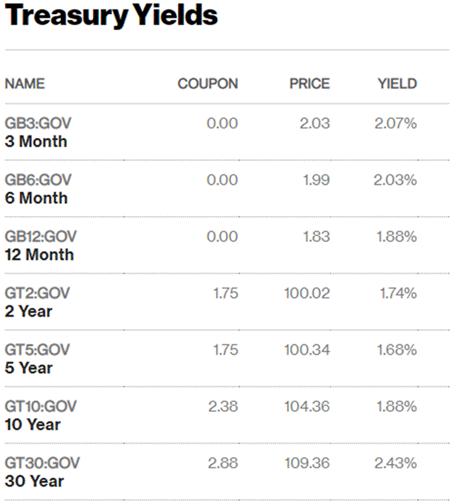

I am sure Jay Powell and the rest of the Federal Open Market Committee didn’t expect Thursday’s bond market action. They cut rates hoping to mitigate or even remove the inverted yield curve, which is a pretty reliable recession precursor. The opposite happened.

Below is a yield curve snapshot from Bloomberg on Thursday after the markets closed. The 10-year bond yield dropped 14 basis points in just a few hours. It was a sporty 3.01% at this time in 2018. The three-month Treasury yield actually rose three basis points in the secondary market, making the yield curve even more steeply inverted than it already was.

Source: Bloomberg News

President Trump didn’t help matters by expanding tariffs on Chinese imports. Powell was quite clear that the Fed is paying close attention to trade data. The president gave them even more concerns for their next FOMC meeting in September.

As I have written many times over the past 20 years (by the way, this week is actually the 20th birthday of Thoughts from the Frontline), the longer an inverted yield curve persists and the deeper it gets, the higher the probability of recession within the next 9–15 months. Typically, the bear markets associated with recessions start even sooner.

Thursday morning, the futures market saw 60% probability of another rate cut in September. By day’s end, it was up to 90%.

Global PMI’s are clearly showing a global growth slowdown, and we see distress signals in a number of US indicators. I don’t think we’re already in a recession, as my friend David Rosenberg argues, but consumer spending is the only thing keeping GDP up right now. As long as that holds, GDP will remain positive. But when consumers get nervous (as a bear market could make them)? I think we’ll see the GDP numbers roll over. I won’t try to predict when, because betting against the US consumer is generally a bad idea, but it will happen.

And rate cuts hurt some 30 million US savers. We are once again on a destructive path of financial repression. This clearly hurts consumers, especially at the lower income levels.

Awash in Debt

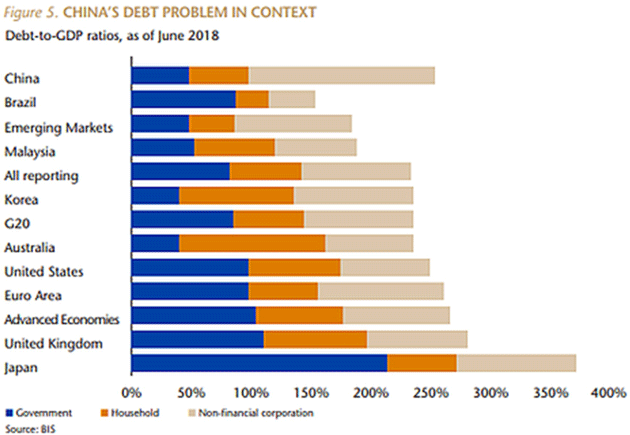

As I keep saying, the world is awash in debt. Some of it is productive, but much is not. Here is a handy BIS chart (via my friends at Glidepath Wealth Management) combining government, household, and corporate debt relative to GDP.

Source: Glidepath Wealth Management

While some countries are more indebted than others, very few are in good shape. Direct your attention to the “All reporting” line. It shows the entire world is roughly 225% leveraged to its economic output. Emerging markets are a bit less and advanced economies a little more. But regardless, everyone’s “real” debt is likely much bigger, since the official totals miss a lot of unfunded liabilities and other obligations.

Debt is an asset owned by the lender. It has a price, which—like anything else—can go up or down. The main variable is the lender’s confidence of repayment, which is always uncertain. But there are degrees of uncertainty. That’s why (perceived) riskier debt has higher interest rates than (perceived) safer debt. The way to win is to have better insight into the borrowers’ ability to repay those loans.

In other words… if a lender owns debt in which his confidence is low, but you believe has value, you can probably buy it cheaply and, if you’re right, make a profit—possibly a big one. That is exactly what happens in a recession.

Investment Grade Zombies

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

While it’s easy to point fingers at profligate consumers, households largely spent the last decade de-leveraging. The bigger expansion has been in government and business. I’ve discussed government debt quite a bit lately, so let’s zoom in on corporate debt.

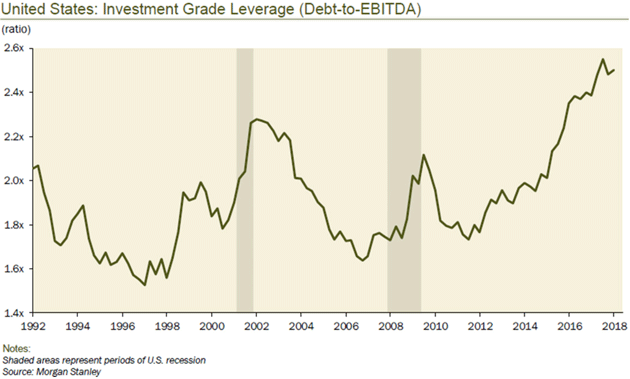

The US investment grade bond universe is considerably more leveraged than it was ahead of the last recession. Here’s a chart Dave Rosenberg shared at the Strategic Investment Conference.

Source: Gluskin Sheff

Compared to earnings, US bond issuers are about 50% more leveraged now than in 2007. In other words, they’ve grown debt faster than profits. Many borrowed cash not to grow the business, but to buy back shares. It’s been, as Dave calls it, a giant debt-for-equity swap.

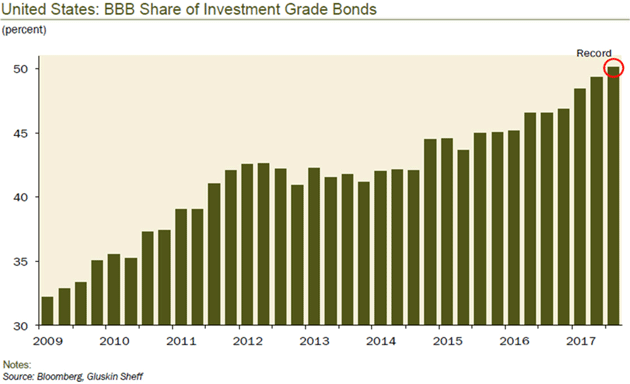

There’s another factor, though. Today’s “investment grade” universe contains a higher proportion of riskier companies. The lowest investment grade tier, BBB, now constitutes half of all issuers. All these are just one downgrade away from being high-yield “junk bonds.” The best data I can find shows that there are roughly $3 trillion worth of BBB bonds and another roughly $1 trillion worth of lower-rated bonds that would still be called “high-yield.”

Source: Gluskin Sheff

If it happens like last time, the ratings agencies will wait until their fate is already sealed before they cut ratings on these zombies. But that’s only part of the problem.

Selling Under Pressure

Last year, I wrote extensively about a forthcoming High Yield Train Wreck. The Fed was still tightening rates at the time; their subsequent policy change has slowed down the process, but the train is still moving. I expect liquidity in these below-investment grade bonds to disappear quickly in the next financial crisis.

We got a small hint of how this will look in the December 2015 meltdown of Third Avenue Focused Credit Fund (TFCVX), which had to suspend redemptions and then spend two years liquidating its assets. As I said at the time, the fund managers made the right call to liquidate their holdings slowly, getting the best values they could. They ultimately recovered far more of the losses than they would have by selling under pressure. But that won’t work if the entire fund industry is strained at the same time.

This is a structural problem with mutual funds and ETFs. They must redeem their shares on demand, usually in cash (though some reserve the right to do it in-kind). This can, if enough shareholders want out at the same time, force them to sell fund assets on short notice.

Average investors who don’t trade large blocks often don’t get how hard this is. Let’s try a more familiar example.

Say you want to sell your house and move to a different state. Normally, you would set your price, take your time, and wait for a buyer who will pay it—or at least get close. You generally have the luxury of “price discovery” over time.

But imagine your mortgage lender says you must make a balloon payment three days from now or lose the house completely. You will then have to find a buyer fast or face a giant loss. In that scenario, you can’t really afford to wait. You take the first minimally acceptable offer and run.

That’s more or less what happens when a mutual fund gets mass redemptions, particularly in already-illiquid segments like junk bonds. Those who might buy its assets smell blood and make lowball offers. The fund manager must either take them, or do what Third Avenue did and shut down the entire fund permanently, slowly liquidating and paying investors over a much longer period. That is a career-ending, business-ending event for the managers, not to mention investors who can wait years to get back what’s left of their money.

This is a horrible situation for both fund manager and investors. Even long-term investors get hurt. But we don’t hear much about the other side: those who buy the distressed, must-sell-now assets at steep discounts to face value. Which would you rather be?

Falling Apart Quickly

When the recession hits, we will see junk bonds—and the riskier end of corporate debt generally—go into surplus. There will be more available for sale than investors want to buy. The solution will be prices dropping to a point that attracts buyers. I don’t know where that point is, but it’s a lot lower than now.

But there’s a problem. We talked about that $3 trillion worth of BBB bonds. Any that are downgraded by merely one grade will no longer qualify as “investment grade.” That means that many pension funds, insurance funds, and other regulated entities by law won’t be able to hold them. They have a very short time to sell them back into the market.

Let’s say company X issues $100 million of a bond rated BBB by Moody’s or Standard & Poor’s. There is a high likelihood that some will be in regulated pension or insurance funds, and there will be forced selling at lower prices. This will set a new price for that bond issue. Every mutual fund and ETF that holds those bonds will have to use the lower price when they mark-to-market at the end of the day.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

This happens all the time, but in a recession, there is a great deal of forced selling. Investors in huge high yield and “investment grade” bond funds start to look for an exit as the price of their funds fall, which forces the funds to sell bonds “at the market price.” Except in a high-yield bond bear market, the bids go much lower or simply disappear. The normal buyers of those funds are what you would typically characterize as “distressed debt” funds. They will be looking to buy as cheaply as they can. At moments like that, distressed debt funds sit back and see how far down prices will go before competing distressed debt funds step in and start to buy—establishing a “floor,” if you will.

I have seen this happen three times in my career. Yields go from fairly low to 20% or more at what seems like warp speed. If you are in one of those funds, you’re going to see your value drop precipitously. Unless you are a professional and/or have some systematic trading signal that tells you when to trade, it’s probably best to avoid anything that looks like a high-yield mutual fund or ETF.

More money is going to be lost by more people reaching for yield in this next high-yield debacle than all the theft and fraud combined in the last 50 years.

I can understand the plight of retirees who are struggling to live on today’s meager yields. Those high-yield funds have been so good for so long, it’s easy to forget how disastrous a bear market can be. But it gets worse.

Quick personal story, and I have to be vague about names here. Some bond issues have been bought in their entirety by a small handful of high-yield bond funds. The problem is that the company that issued these bonds has defaulted on them. Not just missed a payment or two, but full default. Their true value, if the funds tried to sell them, might be 25–30% of face if they actually traded, according to the people who told me this. But the funds still value them at the purchase price of $0.95 on the dollar.

How is it they’re still valued much higher? Because the funds haven’t tried to sell them. No transactions mean they can still be “priced” at the last trade, and since there have been no subsequent trades, there is no “mark-to-market” price.

If any of those few funds sold any of these bonds, it would set a “market price” and all would have to mark down the entire holding. So naturally, they aren’t even trying. They would rather hold these bonds at what they know, realistically, is a huge loss, than take the hit to their NAV.

So here’s my question: How many other junk bond issues are in similar positions? Note this isn’t just high-yield funds. Lots more “conservative” bond funds try to juice their returns by holding a small slice in high-yield. Regulations let them do this, within limits, but these funds are so huge the assets add up.

If funds are carrying assets whose market value (if there were a market) is half or less of their currently booked value, that tells me this game could fall apart very quickly. Any event that triggers redemptions could set off an avalanche.

I don’t know what that event would be, but I’m pretty sure one will happen. My own goal is to be a buyer, not a seller, whenever it occurs. For now, that means holding cash and exercising a lot of patience.

If I’m right, the payoff will be a once-in-a-generation chance to buy quality assets at pennies or dimes or quarters on the dollar. I think the next selloff in high-yield bonds is going to offer one of the great opportunities of my lifetime.

In a distressed debt market, when the tide is going out, everything goes down. Some very creditworthy bonds will sell at a fraction of the eventual return. This is what makes for such great opportunities. They only come a few times in your life.

There will be one in your near future.

Navigating the Waters Ahead

Quick commercial. As many of you know, in 2018, I joined CMG as chief economist and co-portfolio manager of the CMG Mauldin Smart Core Strategy. This was not a decision I took lightly as my time is a valuable resource. What pushed me to jump onboard is the feeling I had in 2007 that something bad was coming. While my timing wasn’t perfect, my research and letters regarding subprime and bubbles were in fact primary triggers to an awesome (meaning large and not fun) recession.

In 2019, I have a similar feeling about the global debt supercycle. To help investors navigate what I call “The Great Reset,” I’ve partnered with CMG and my close friend Steve Blumenthal to launch Mauldin Smart Core. Since the exact timing of such events is difficult to predict, I wanted a place where my own portfolio could participate in a continued bull run but still have protection from the coming bear market. We use a multi-manager approach that diversifies trading strategies, not just asset classes, which can all go down together. I think of Smart Core as my bridge over troubled waters.

I invite you to listen to a recent quarterly conference call with me, Steve Blumenthal, and two of the managers in Mauldin Smart Core where we discuss the current economic landscape and asset markets. Click here to hear the conference call. You will also receive a copy of my paper “Investing During the Great Reset” where I discuss the genesis of the strategy and how the portfolio works.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

(Please note, while I personally receive compensation from CMG, neither CMG nor Mauldin Smart Core are affiliated with Mauldin Economics.)

New York, Maine, New York, and Montana

I leave for New York on Monday for a few days of meetings. On Thursday, I fly to Bangor, meet up with Steve Blumenthal and other friends, and then drive to Grand Lake Stream for the annual economic fishing trip, now called Camp Kotok. I have so many friends who will be there. It will be a great three days of talking economics and catching up. This will be my 14th year to go.

I look at the roster of my fellow attendees, many of whose names you know, and am salivating about the discussions. $14 trillion of negative bonds? The trade weighted dollar rising even with a rate cut? Tariffs blowing up world trade? The high yield crisis? The timing of recessions? Where are the opportunities? And so much more.

Honestly, it feels like August of 2007, and that was a great year for debates and discussions. Confession: most campers use two-man canoes plus a guide. I have a long time guide with a larger bass boat and I get three of us where we fish and talk. Ben Hunt and Jonathan Ward for three hours alone? Priceless. Peter Boockvar? Jim Bianco? And 50 more just as smart attendees? With the beauty of Maine? And fresh fish for lunch every day? Gourmet dinners? (Singing, “Heaven, I’m in heaven.”

The next Tuesday, I fly to Missoula, Montana where I will meet Shane and good friends Patrick and Cheryl Cox. We will spend much of the time relaxing, but Pat and I will work on a few chapters of my next book. I actually finished my last book five years ago at Darrell Cain’s home on Flathead Lake, and while I won’t finish the next one this trip, I expect to get a lot done. In yet more heaven. Life is good. And then Shane and I fly back to paradise. Not bad for a west Texas country boy from the wrong side of the tracks.

And with that, I will hit the send button and wish you a great week! And while you may not be able to be with as many friends as I will, try and round up a few.

Your ready for a little fishing and economics conversation analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.