The Key To Success In Investing In P2P Loans

- Stephen McBride

- |

- September 21, 2017

- |

- Comments

This article appears courtesy of RiskHedge.

Peer-to-Peer (P2P) lending is gaining a momentum among investors. P2P loans have less volatility, a low correlation, and yield much higher returns compared to other fixed-yield investments. Median risk adjusted returns average 7.3% on a 36-month loan.

The sector is also very easy to enter. An investor can set up a profile in less than a day and invest as little as $25 per loan. Once invested in a loan, investors usually start receiving payments within 30 days.

However, the unsecured nature of the market means investors must be well aware of its dos and don’ts. So, I discussed P2P lending with several industry experts and outlined a few key factors to success in this industry.

The first among them is…

Diversification

The P2P lending nature means that you must build a portfolio of hundreds of loans where each loan is a fraction of the total portfolio. And this is not an asset basket into which you put too many of your investment eggs.

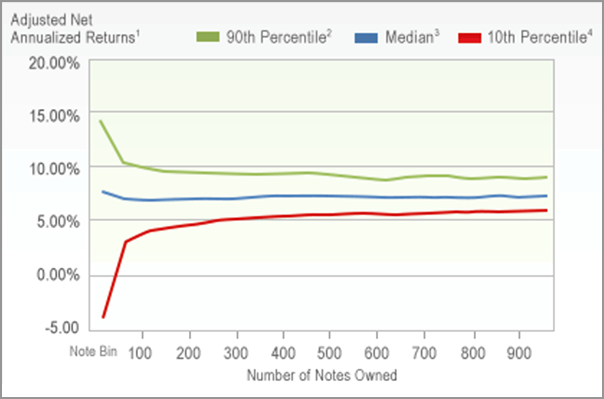

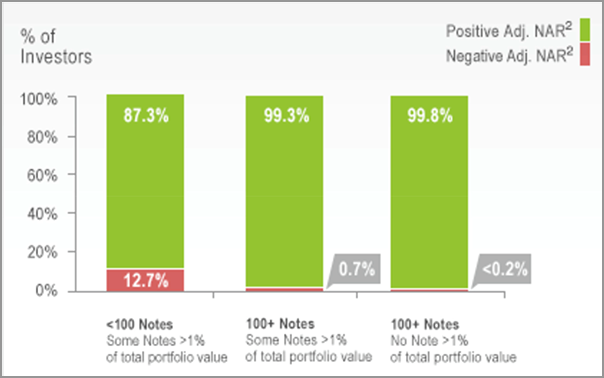

Both Lending Club and Prosper have released statistics that show diversified portfolios give the greatest return and minimize risk.

Diversification at Lending Club:

Source: Lending Club

Source: Lending Club

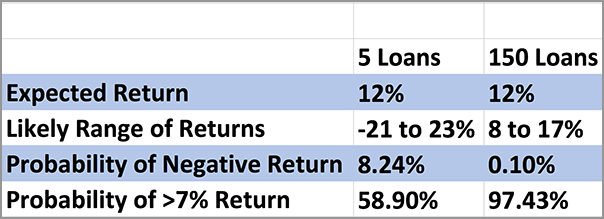

Diversification at Prosper:

Source: Prosper

Prosper also has statistics that show since July 2009, every portfolio of 100 notes or more has had positive returns.

The low minimum investment at these services makes diversification easy. However, loan selection takes time, and speed is key to getting the best loans.

With the recent influx of institutional money, P2P has become much more competitive. The best-quality loans can be snapped up within minutes of being posted. This is why investors must use third-party marketplace tools, which we detail next.

Tools for Success

The fast pace of loan purchases on platforms demand automation tools. One of the best tools of this kind is NSR Invest.

NSR Invest is a registered investment advisor that offers managed accounts to P2P investors. Investors link their Lending Club and Prosper accounts to the website and have NSR experts invest for them based on their loan selection criteria.

Loan filtering can help investors consistently outperform the market. Based on back testing from NSR, the most effective filters are: loan grade, credit inquiries in the last six months, and loan purpose.

Although default rates are higher on grades D–G at Lending Club and grades D–HR at Prosper, it doesn’t mean the ROI is lower. With smart loan filtering, you can invest successfully in those lower grades, too

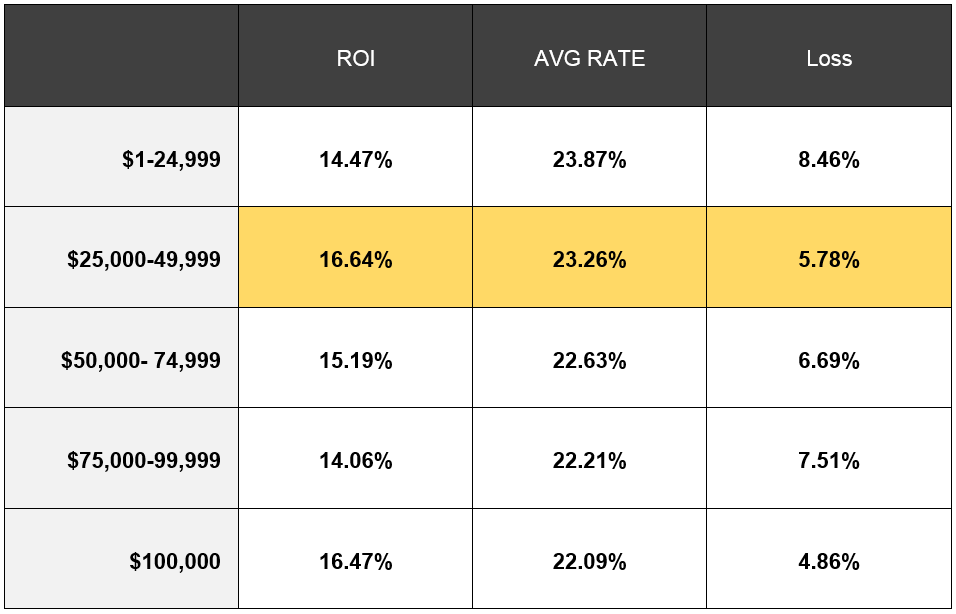

In this table, you see how the annual income filter can affect returns on D- to HR-rated loans on Prosper.

NSR also offers investors access to liquidity with automated secondary-market trading. Users pay a fee of between 0.45% and 0.60% of the total value of all notes purchased on NSR Invest (excluding charged-off loans).

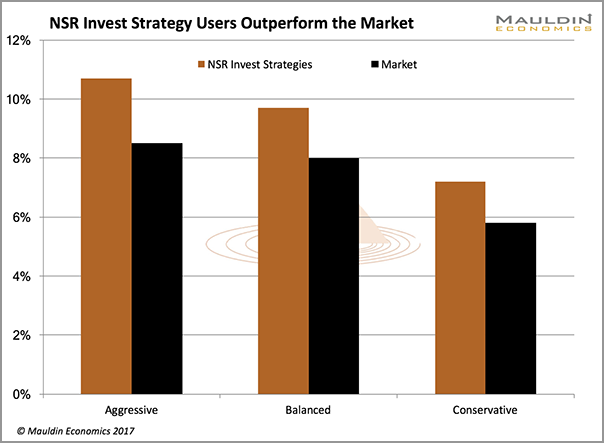

Depending on the strategy selected, NSR users outperform the market by as much as 2.6%; the average is 1.5%.

Source: NSR Invest

Another great tool is LendingRobot, a registered investment advisor offering fully automated P2P investing for individuals. Investors link their Lending Club and Prosper accounts to the website, select from several criteria that determines their individual strategy, and have LendingRobot execute the investments.

LendingRobot is very fast, executing investments in less than one second after loans have been listed on a platform. The first $5,000 is managed for free. After that, users pay a 0.45% monthly fee on assets under management.

BlueVestment and PeerCube are two other automated P2P investing platforms that can help users. Both platforms perform the same function as LendingRobot.

Free Report: The New Asset Class Helping Investors Earn 7% Yields in a 2.5% World

While the Fed may be raising interest rates, the reality is we still live in a low-yield world. This report will show you how to start earning market-beating yields in as little as 30 days... and simultaneously reduce your portfolio’s risk exposure.

This article appears courtesy of RH Research LLC. RiskHedge publishes investment research and is independent of Mauldin Economics. Mauldin Economics may earn an affiliate commission from purchases you make at RiskHedge.com