Finding the next Uber: 2 stocks with “reformer” potential

- Stephen McBride

- |

- August 7, 2023

- |

- Comments

This article appears courtesy of RiskHedge.

I’m about to show you the most important chart in investing.

Please look at it closely.

It explains much of the stock market carnage we saw in 2022… and hints at where we’re headed next.

It also tells you which types of stocks you should buy and which companies to avoid.

Today, I’ll also show you two stocks to put on your watchlist.

But first, the one chart to rule them all…

- “Money” is getting more expensive.

Below is a chart of the US 10-Year Treasury yield.

This is considered the “benchmark” for interest rates.

It affects everything from your mortgage payments… to car loans… to the crazy high interest rates on credit cards.

You can see rates have been in a steady downtrend since the 1980s. Each time yields touched that upper green line, gravity pulled them back down to Earth.

But something MAJOR changed last year:

This chart suggests the 35-year downtrend in interest rates is broken. We’ve entered a new regime—and it’s turning the investing world upside down.

Without going into all the financial gobbledygook, interest rates influence stock market valuations.

As super-investor Warren Buffett says: “Interest rates are to the value of assets what gravity is to matter.”

In other words, when interest rates are low, stocks can go to the moon. But rising rates pull prices back down to Earth.

When rates were pinned to the floor, investors piled into companies with tons of potential. It didn’t matter if the company was bleeding cash so long as it had a shot at becoming the next Amazon.

But now we’re in a new regime. One which favors profits over potential.

The days of pie-in-the-sky companies with money-losing businesses are over. They were a low-interest-rate phenomenon.

Profits are the hot new thing. You want to invest in companies producing boatloads of cash.

- Remember The Far Side?

The comic strip ran for years in The New York Times and other big-name newspapers.

Here’s my all-time favorite Far Side cartoon:

Source: Gary Larson

To butcher the caption: "Situation's changed, investors. Dump those cash-burners and buy me some moneymakers.”

But where are the moneymakers at in 2023?

The big opportunity lies in “reformers.” These are companies that were previously cash incinerators but now make the big bucks.

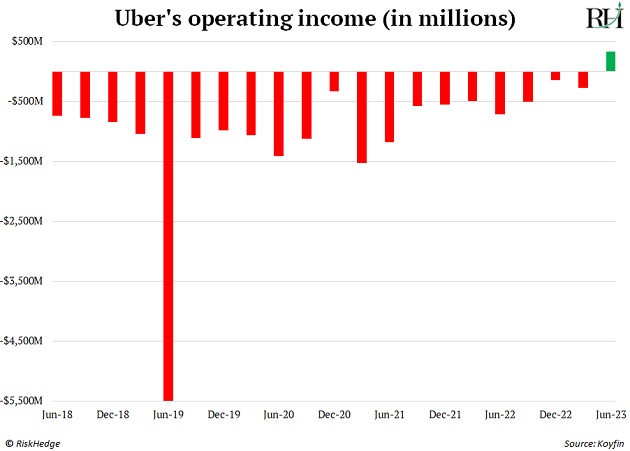

Uber (UBER) is a perfect example.

RiskHedge readers may remember I did a 180 on the ride-sharing giant back in September 2022.

After hemorrhaging money for over a decade, Uber turned “cash flow” positive for the first time last year. And after racking up $31 billion in losses over the same time period, Uber just achieved its first-ever fully profitable quarter.

In other words, the ride-sharing giant has entered the new era:

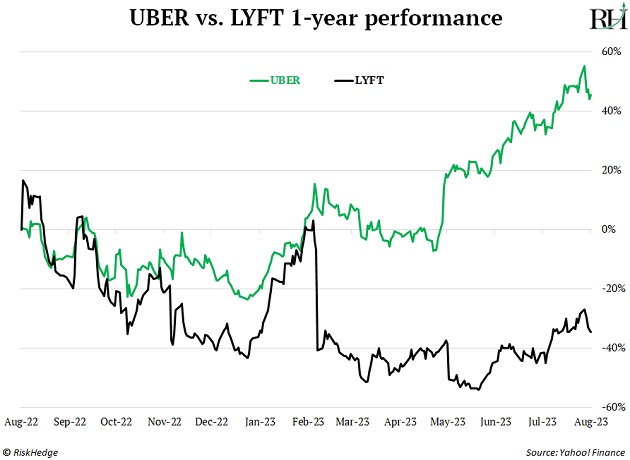

Meanwhile, Lyft (LYFT)—Uber’s ride-sharing competitor—is still leaking cash:

Companies with tons of potential were the belle of the ball for the past decade. But investors are once again favoring moneymakers over cash incinerators.

- The same trend played out after the dot-com crash.

In the 1990s, rookie day traders, housewives, and their mothers piled into internet stocks with little revenue—never mind profits.

When the dot-com bubble burst, “tech” got slammed.

Microsoft (MSFT) crashed 60%...

Amazon (AMZN) collapsed 94%...

And Booking Holdings (BKNG) plunged 99%.

These stocks didn’t eclipse their dot-com highs for years after the crash. But they ultimately bounced back stronger than ever.

You know who never recovered? Internet start-ups that continued to hemorrhage cash.

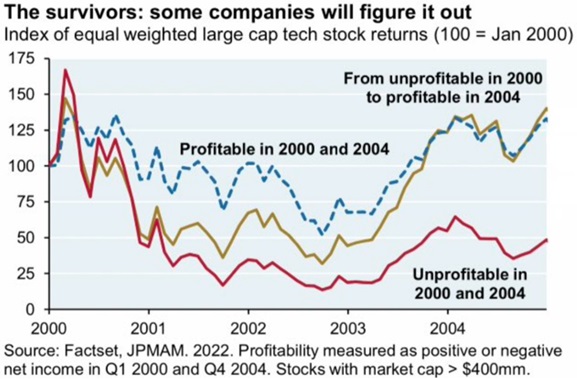

Below is a great chart from JPMorgan showing how different types of stocks fared after the dot-com blowup.

“Reformers”—previously unprofitable companies that turned the ship around—came out on top (brown line).

Firms that were profitable all along (blue line) weren’t far behind.

Meanwhile, money losers (red line) kept sinking:

Source: JPMorgan

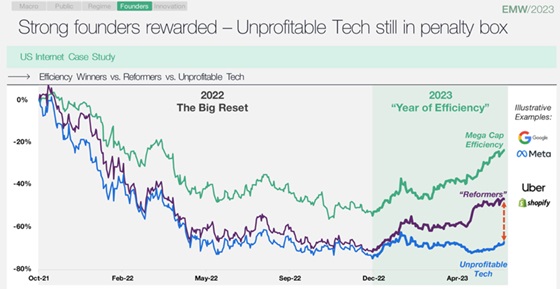

History is repeating itself today.

Reformers like Uber are bouncing back. But money losers like Lyft remain in the penalty zone.

Source: Coatue

In the era of profits over potential, I recommend you stay away from them.

- “Stephen… what other reformer stocks should I buy?”

RiskHedge readers who bought Uber when I recommended it in September are sitting on 60% gains today.

I still like Uber and think it will climb higher.

But the real question is… Who’s the “next” Uber?

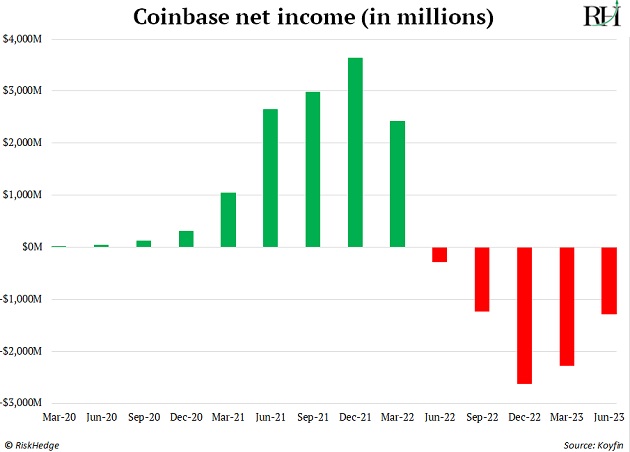

I did a U-turn on crypto exchange Coinbase (COIN) in January.

Coinbase was raking in money when crypto prices were hitting record highs. Degenerate gamblers were waking up and buying tokens before they brushed their teeth.

Coinbase gets most of its revenues from trading fees. So when bitcoin collapsed and interest waned, so too did Coinbase’s profits:

When interest in crypto picks back up—and it will pick back up—Coinbase will make boatloads of cash once again.

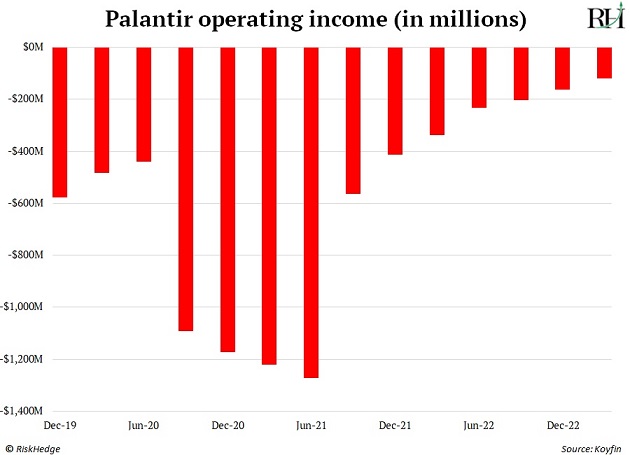

Palantir Technologies (PLTR) is the other reformer to watch.

Palantir specializes in big data analytics. The US government has used its tools to catch “bad guys,” including Osama Bin Laden and Bernie Madoff.

The company’s been bleeding the past couple years. But you can see below things are moving in the right direction.

Like Uber, I expect Palantir to achieve its first-ever profitable quarter this year.

We’re in a new investing era, friends.

Profits reign over potential. That’s the golden rule.

You want to own reformers. These companies can successfully transition from cash burners to moneymaking machines…

And their stocks will soar to new heights.

Continue to avoid money losers. These stocks will be in the penalty zone for years… just like their dot-com ancestors.

Stephen McBride

Chief Analyst, RiskHedge

|

This article appears courtesy of RH Research LLC. RiskHedge publishes investment research and is independent of Mauldin Economics. Mauldin Economics may earn an affiliate commission from purchases you make at RiskHedge.com