Jeffrey Gundlach

Jeffrey Gundlach George Gilder

George Gilder Karen Harris

Karen Harris Lacy Hunt

Lacy Hunt Niall Ferguson

Niall FergusonEssay 1 Featuring Jeffrey Gundlach

The Moment of Truth for the Secular Bond Bull Market Has Arrived

By John Mauldin

“The moment of truth has arrived for [the] secular bond bull market! [Bonds] need to start rallying effective immediately or obituaries need to be written.”

—Jeffrey Gundlach

“Jeffrey started his career as a nearly broke rock and roll drummer, now he goes under the nickname the Bond King. What he says and does literally moves markets”

—Bethany McLean

Welcome to the first installment of this five-part series on the individuals and ideas informing my worldview as of late. My goal with this series is to highlight the ideas which have been deeply influential on me, and share with you what I’ve learned.

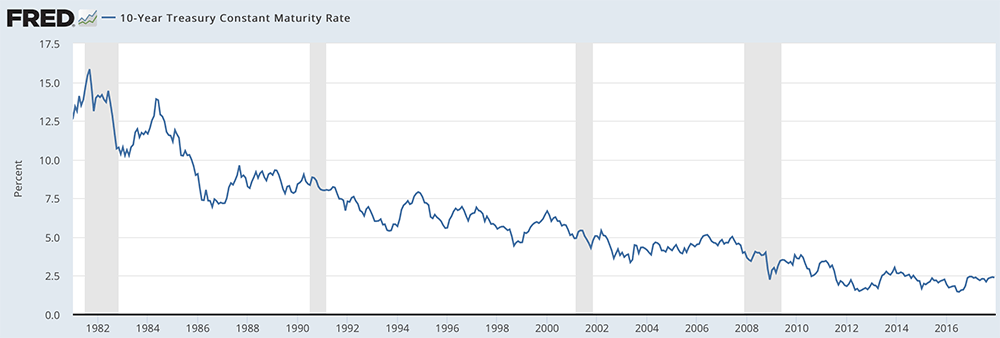

I mentioned in my email to you yesterday that this series will start with a bang, and the following fact certainly hit me like a ton of bricks: Anyone who started investing after 1981 has never experienced a bear market in Treasuries. The vast majority of today’s investors have only ever invested when Treasury yields are falling.

Sources: St Louis Fed

The secular decline in bond yields is one of the most definable trends in financial markets, and also one of the most important. As you know, US Treasury yields are the bellwether for global interest rates. Almost every market and asset class in the world is affected by them.

At every opportunity, I like to point out that interest rates are the cost of money. Unfortunately, at 68, I’m old enough to remember when the cost of money was high.

In the early 1980s, I took out a business loan with an 18% interest rate. The repayments were no fun, but I was one of the lucky ones who could actually afford to borrow money at that time. Those rates created an insurmountable hurdle for most entrepreneurs, and banks were not willing to lend like they are today.

In the 36 years since then, the cost of money has fallen sharply—and demand for it has skyrocketed. Today’s US financial infrastructure is addicted to “easy money.”

-

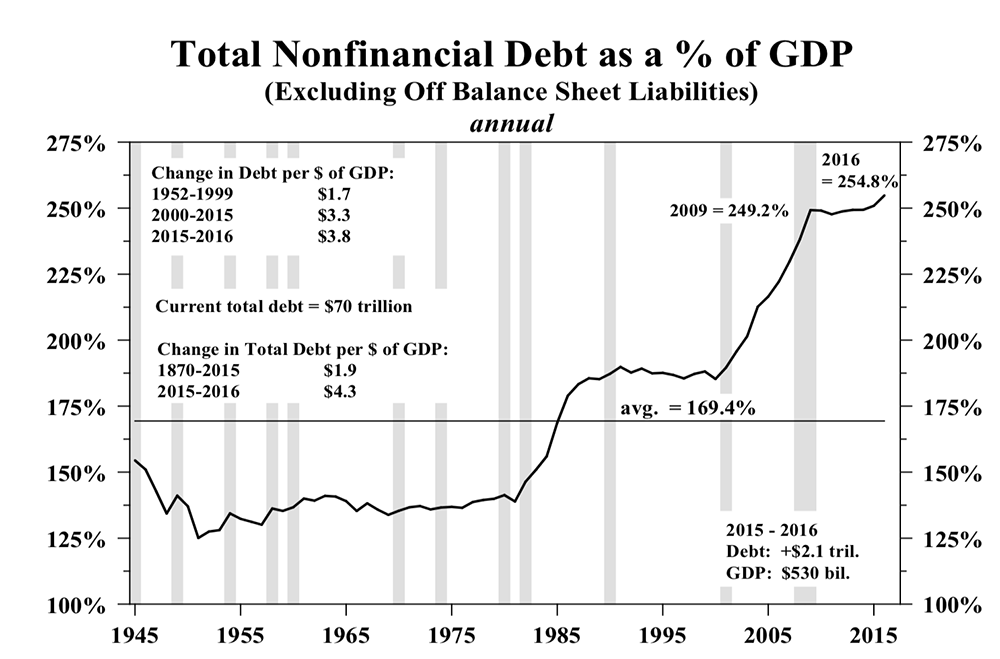

Government: Low interest rates have enabled the Federal government to increase their total debt by 113% since 2008, yet interest payments have risen by only 5%.

-

Corporations: Corporations have borrowed huge amounts of debt to fund stock buybacks and increases in their dividends. Today, nonfinancial corporate debt is 79% higher than it was in 2008.

-

Households: The New York Fed’s latest quarterly report on household debt showed that US households have a total of $12.96 trillion in debt outstanding. That’s $280 billion higher than the previous all-time peak in Q3 2008.

The US economy has become heavily reliant on easy money, which leads to the question, “what would happen if interest rates increased substantially?”

One famed investor who has explored this question is “Bond King” Jeffrey Gundlach. The man needs no introduction, but I’ll give him one anyway. Jeffrey is the CEO of DoubleLine Capital, where he manages $116 billion—and has a stellar track record. Jeffrey has outperformed 92% of his peers over the last five years. His flagship DoubleLine Total Return Bond Fund (DBLTX) has also outperformed its benchmark by a wide margin over the same period.

Although Jeffrey manages one of the world’s largest bond funds, he is an independent thinker who has courage and conviction in his beliefs—maybe because he comes out of left field. Jeffrey holds degrees in mathematics and philosophy from Dartmouth College and was once the lead for a new-wave rock band, back when Paul Volcker had me paying 18% interest on that loan.

Jeffrey has had an ultra-successful investment career and has been spot-on with market timing, especially in 2017. He has called the direction of Treasuries and the US dollar, to almost the exact tick.

However, by far his biggest call, possibly in his entire career, is that the secular bond bull market is over, and that the US 10-year Treasury yield will hit 6% by 2020.

I want to dissect Jeffrey’s thought process behind this call. Let’s look at the three reasons why he believes the secular bond bull market is over and that we are headed into a period of rising interest rates.

Growth is good, but not for bonds

In a December interview with CNBC, Jeffrey commented on the recent economic growth numbers:

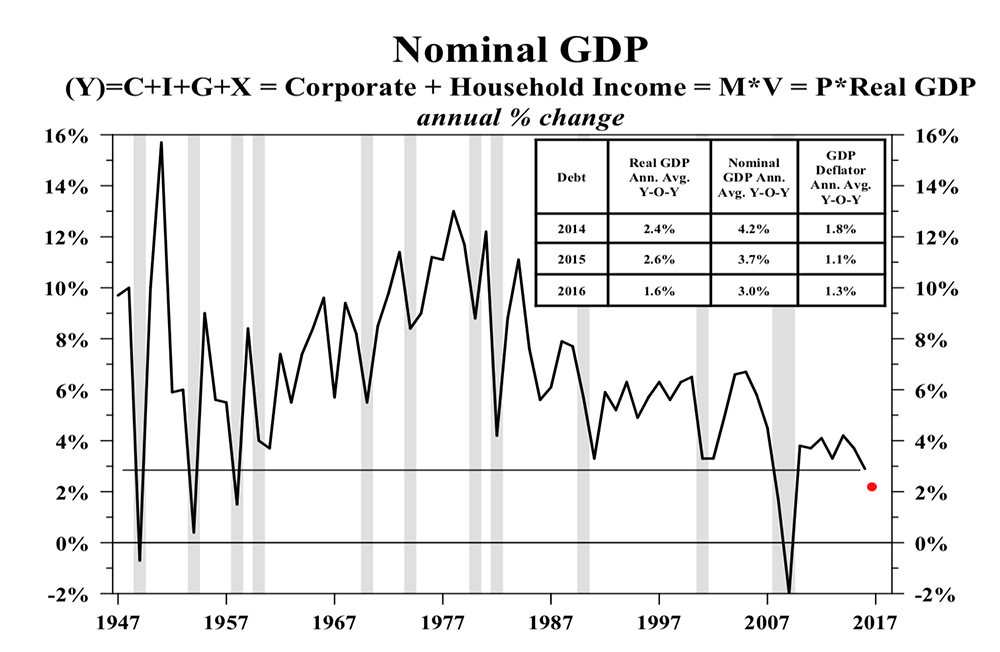

We’ve had 2% real [GDP growth] for three quarters in a row. GDP NOW at the Atlanta Fed is around 3% for the [Fourth] quarter. It seems to me that interest rates should continue to rise as we move into 2018, because bonds don’t like economic growth.

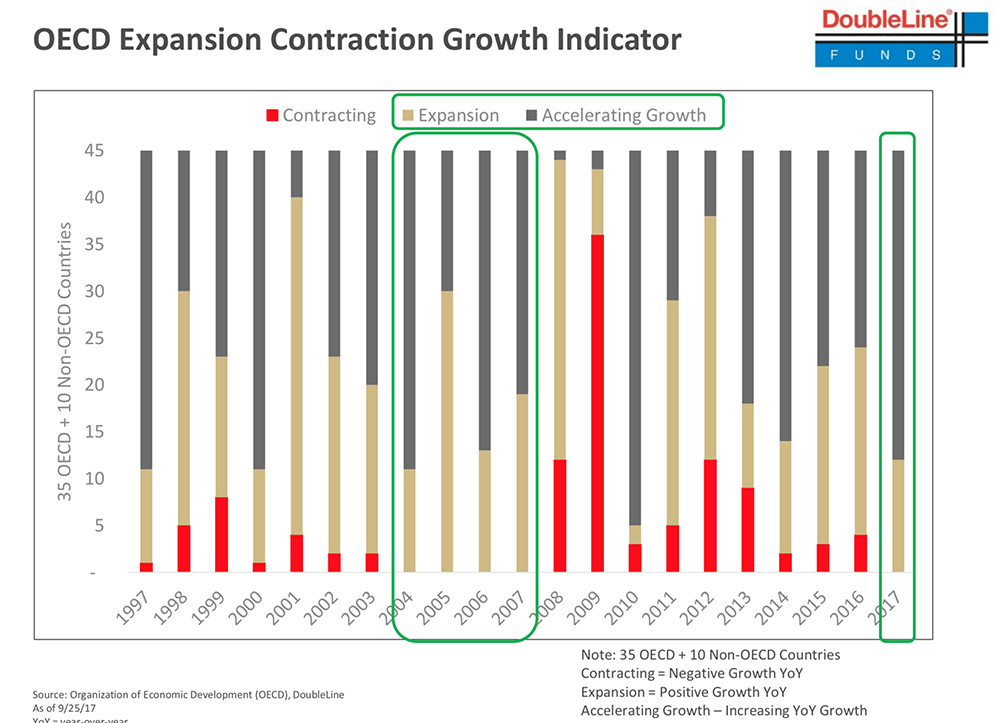

For the first time since 2007, not one of the 45 economies included in the OECD Expansion Contraction Growth Indicator is contracting. The below chart from a recent presentation Jeffrey gave shows this.

Sources: DoubleLine Funds

By this measure, the global economy is in a synchronized upswing for the first time in a decade—and the short-term outlook is positive. Leading economic indicators in all major regions are flashing green. In the US and Europe, the purchasing managers indices (PMIs) are at multi-year highs. This is good news for everything, except bond prices.

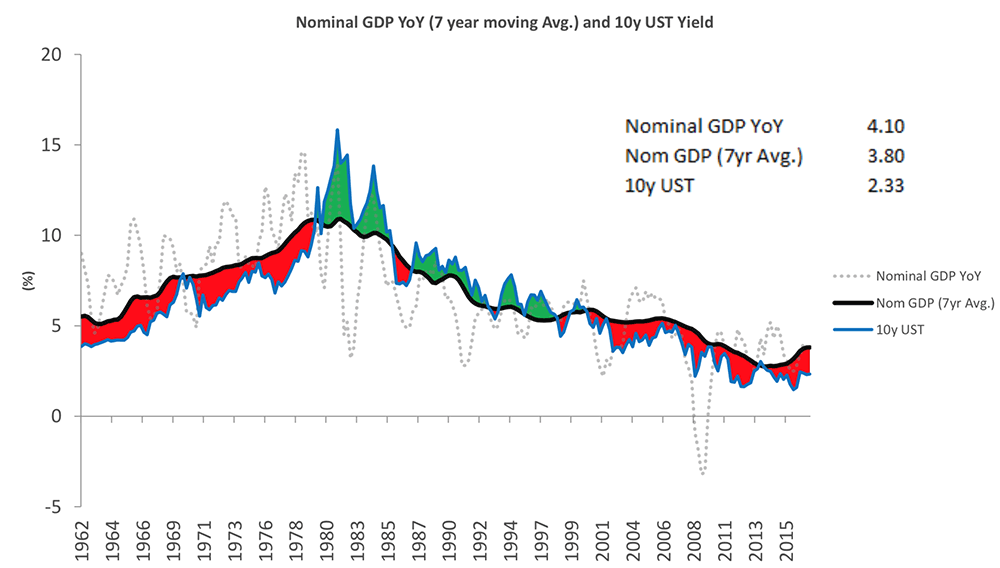

Higher economic growth means more demand for credit, which drives up its cost. In this case, the cost is interest rates. This relationship between economic growth and interest rates is why, over time, bond yields track nominal GDP growth.

The below chart from the recent presentation by Jeffrey shows that when the 7-year moving average of nominal GDP growth is higher than the US 10-year Treasury yield, yields should rise. The current setup suggests that bond yields should now be rising.

Sources: DoubleLine Funds

I have my doubts about the sustainability of growth in the US because of the rising debt burden and anemic growth in productivity and the working age population. With these headwinds, I believe it will be almost impossible to achieve sustained growth, like what we experienced in the 1990s. However, I concede that growth could continue to rise over the next 2–3 years.

Along with rising economic growth, Jeffrey sees the return of inflation as the second “building-block” to higher bond yields.

An arch enemy returns to the fray

In his December webcast, Jeffrey gave his thoughts on the current inflation numbers:

If [inflation] continues to rise, the Fed would have ample reason to follow through on its indicated three rate hikes in 2018.

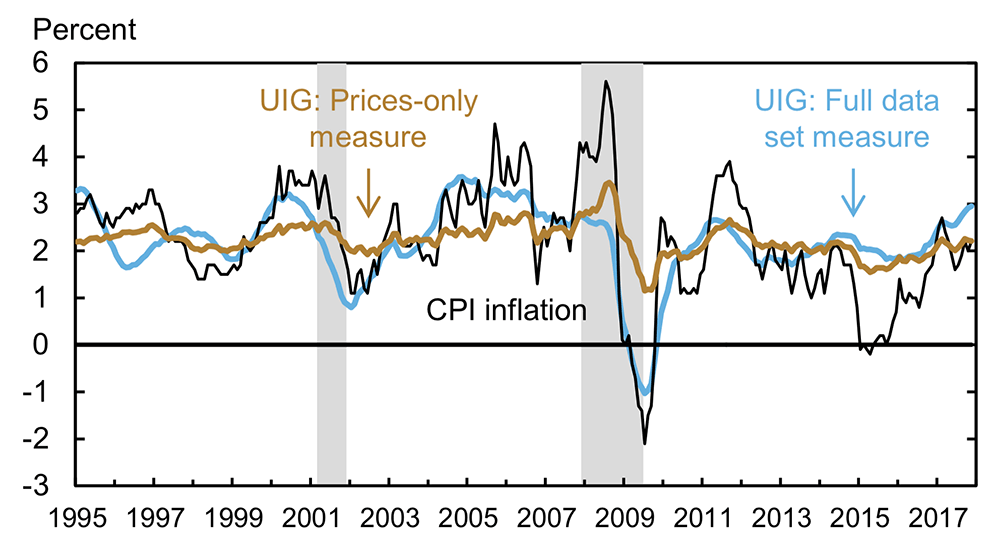

Despite the best efforts of central banks, inflation has remained largely absent from the US and other advanced economies over the past decade. In 2015, the US CPI annualized at just 0.11%. Finally, it appears that bonds’ arch enemy may be making a comeback.

Inflation, as measured by the CPI, is on track for its highest annual growth rate since 2011. It is also at multi-year highs in Europe, the UK, and Japan. Longtime readers know I have been a critic of the CPI, for a host of reasons I won’t go into now.

The indicator I use to get a broader, real-time measure of inflation is the New York Fed’s Underlying Inflation Gauge (UIG). This gauge captures sustained movements in inflation from information contained in a broad set of price, real activity, and financial data. In December, the UIG hit its highest level since August 2006, as the below chart shows.

Sources: New York Federal Reserve

We know that inflation erodes purchasing power. Therefore, if it continues to rise, bond yields will have to move higher to meet investor expectations. Remember, when the 10-year Treasury yielded 15% in 1981, inflation was running at 11%.

Since 1960, the average spread between the 10-year Treasury and the CPI is 2.4%. Today, it is just 0.15%. It’s likely to widen as investors’ inflation expectations increase.

Furthermore, at their December meeting, the Fed hinted that they are willing to let inflation run a little over their 2% target. Although they upgraded GDP growth, their forecast for three hikes in 2017 remained unchanged. Given that Janet Yellen once said, “To me, a wise policy is occasionally to let inflation rise even when inflation is running above target,” this is no surprise.

The last building block to higher bond yields, which Jeffrey has identified, is the coming tidal wave of supply in the bond market.

Price is a function of supply and demand

Jeffrey provided insight into how the supply and demand dynamics of the bond market are going to change in his December webcast:

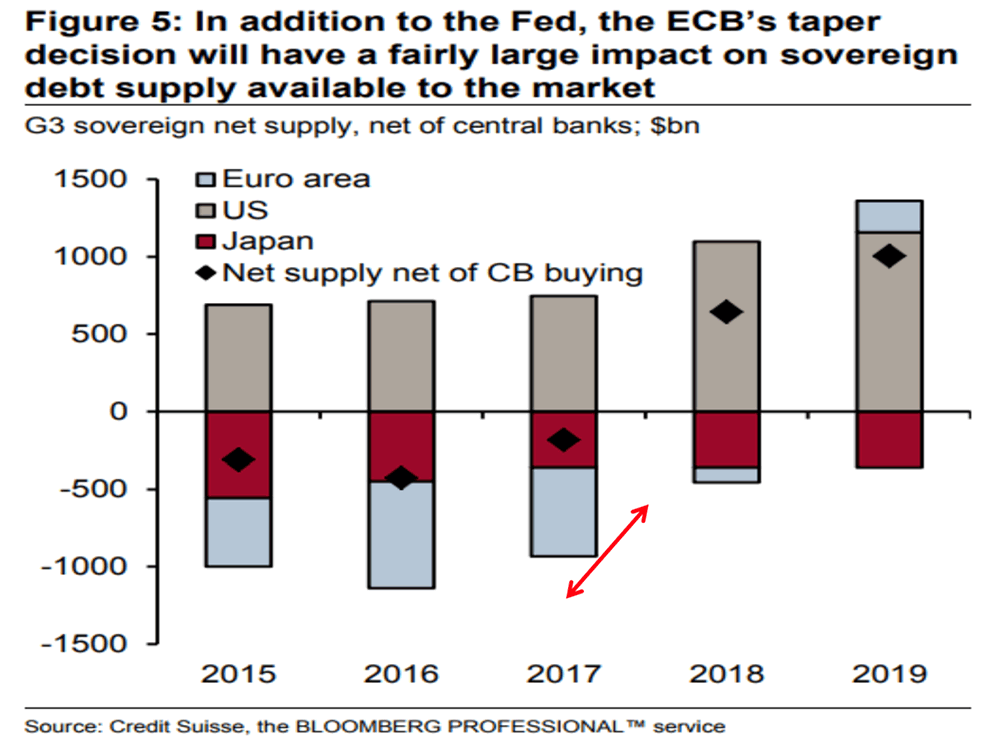

One thing that has helped rates stay low is the lack of [bond] supply. For the last three years, there was negative net supply of bonds from the G3 central banks, and that’s about to change with quantitative tightening. There is a lot of bond supply coming.

The third reason Jeffrey believes the secular bond bull market is over is the coming tsunami of supply about to hit the bond market.

By purchasing a huge amount of sovereign bonds through quantitative easing (QE), central banks have suppressed bond yields over the past decade. For example, demand for sovereign bonds exceeded issuance by around $250 trillion in 2017, thanks to QE by the G3 central banks.

With the Fed now reducing the size of their balance sheet by $30 billion per month, and the European Central Bank scaling back bond purchases by $20 billion per month, this dynamic is going to change, radically. There will be a shift from a $250 billion net demand in 2017, to a $550 billion net supply in 2018. As the below chart shows, that is quite a large swing.

Sources: DoubleLine Funds

There will be an additional $800 billion in sovereign bond supply in 2018, compared to 2017. Econ 101 tells us that this will push bond yields up. But central banks stepping off the gas is not the only trend that is going to contribute to a glut of supply in the bond market. We also have higher budget deficits to factor in.

According to the Congressional Research Service, mandatory Federal spending is set to increase $1.56 trillion by 2026. To pay for this additional spending, more bonds will be issued.

For me, the increasing supply of bonds is the most compelling reason for the end of the secular bond bull market. I have no doubt that quantitative tightening will cause interest rates to rise. Plus, increases in mandatory Federal spending are baked in the cake.

Along with providing reasons why he thinks the secular bond bull market is over, Jeffrey has given insight into how he thinks it will happen. One of his favorite anecdotes about how he sees it playing out is a famous dialogue from Ernest Hemingway’s 1926 novel, The Sun Also Rises.

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

In other words, interest rates will rise gradually over several years, and then everyone will notice, suddenly.

If Jeffrey is correct, and the secular bond bull market is over, the entire financial infrastructure will change.

For starters, how will the governments, corporations, and households who have become dependent on cheap money, react? In 2008, we saw forced deleveraging in action—and it wasn’t pretty.

What will happen to global stock markets if interest rates continue to rise? As Warren Buffett said in a recent interview, “Measured against interest rates, stocks actually are on the cheap side compared to historic valuations. But the risk always is that interest rates go up, and that brings stocks down.”

Now, a world with a 6% yield on the 10-year Treasury is hard to imagine. Saying that, if you had told me when I took out that business loan in the early 1980s that in 30 years, the 10-year yield would be less than 2%, I would have called you crazy.

Jeffrey thinks that we are headed into a much tougher environment because “the Central Bank balance sheets will stop growing at the beginning of 2018, [and] the liquidity that’s helped drive the market is going to reverse. That is not favorable for risk markets.” As such, Jeffrey and his team at DoubleLine have been de-risking their portfolios and have cautioned investors to do the same.

However, the Bond King is not bearish on everything. Jeffrey made a big multi-year call on emerging markets earlier this year and just came out with his top trade idea for 2018: add commodities to your portfolio.

Getting back to Jeffrey’s call on the end of the secular bond bull market, given its wide-ranging implications, it might be the biggest call of his investment career.

Where interest rates go from here will change how we invest and how society functions. I don’t think that’s an exaggeration given the amount of debt in the system and the expectations that the era of easy money will continue, indefinitely.

Because of this, I want to get Jeffrey’s most up-to-date thoughts on how it may play out, and what he believes the implications will be for investors and the economy. That’s why I’ve asked him to give a keynote speech at my Strategic Investment Conference in San Diego, next March.

Jeffrey is a truly independent thinker who is never afraid to make bold, out-of-consensus calls. That’s why I know when he takes the stage at the SIC, he will provide insight into much more than the secular bond bull market. I’m really excited to welcome Jeffrey back to the SIC, and I hope you can be there with me to experience it, first-hand. If you would like to learn more about attending the SIC 2018, and about the other speakers who will be there, you can do so here.

I’ll admit I was somewhat skeptical when you claimed it was the “best conference,” but after last year, I couldn’t praise the SIC enough to my colleagues. (I think they actually got tired of me talking about it.) As a principle, I try NOT to attend the same events but rather experience new and different forums. However, I couldn’t resist returning for the SIC and have once again talked the ears off my fellow traders on the desk.

—Danny A. (past SIC attendee)

That wraps up the first part of this series. In the next installment, you’ll get my thoughts on George Gilder and his new theory of economics.

Now I want to hear from you

If you have a moment, I’d like to get your thoughts and questions regarding Jeffrey’s call that the secular bond bull market is over.

If you have any questions or comments about Jeffrey’s big call, or this five-part series, you can post them in the comment section below.

Your wondering where yields go from here analyst,

John Mauldin

Chairman

![]()

Essay 2 Featuring George Gilder

The Man Who Is Laying the Foundations for a New Economics

By John Mauldin

Flawed from its foundation, economics has failed to improve much with time. As it both ossified into an academic establishment and mutated into mathematics, [it] became an illusion of determinism in a world of human actions. Economists became preoccupied with mechanical models of markets and uninterested in the willful people who inhabit them.

—George Gilder

Knowledge and Power is one of the most fascinating examinations of how wealth is created in a very long time. It makes the moral dimension of entrepreneurship more visible in this age of decreasing confidence in the virtues of wealth creation. Gilder's ideas are new, yet so compelling that they simply cannot be ignored.

—Reverend Johannes Jacobse

One of the most important concepts that my mentors have drilled into my head is this simple statement: Ideas have consequences. As a corollary to that, bad ideas have bad consequences.

Let me offer a somewhat controversial statement: Economics is populated by a lot of bad ideas. Many of which have come to be accepted as the correct interpretation of how the economy functions, and thus have become the basis for economic and monetary policy.

The chief bad idea in economics today is that most economists regard the discipline as a “pure science.” Economists have succumbed to what I call physics envy: They want their less-than-precise discipline to be considered a hard science, too. Unfortunately, economics—which concerns itself with unpredictable human behavior—is fundamentally incompatible with science.

Hard science, like physics, has rules you can’t break. The law of gravity makes for very specific physical behavior that can be mathematically modeled. Economists want us to believe that their own models are as reliable as the law of gravity. But the real world is a complex, dynamic, out-of-balance mess that doesn’t fit inside anyone’s model. You can’t model a system that is as chaotic and unpredictable as an economy in an Excel spreadsheet or even in the latest and greatest statistical software.

You may say, this is all well and good, but it’s just economic theory. How does that matter to my investment portfolio? The direct answer is that these models drive the policies of central banks and determines the price of money. And the price of money is fundamental to the prices of all our assets.

Further, using models to determine policy has damaged the economy in many ways, including:

-

Dysfunctional and counterproductive tax/regulatory/entitlement/trade policies

-

Private-sector credit growth encouraged by central bank mismanagement, and

-

A massive expansion of Federal Government power and spending

Worse again, these models are all backward looking and measure only that which has already happened. But the economy, and its millions of economic actors, are forward looking, striving to create and do things which have never happened before. Yet another reason why the models we rely on are incompatible with how the economy functions.

This is why I believe it is time for a new economics. An economics which focuses not on mechanistic models, but on the creations and innovations which have driven economic progress since the beginning of time.

The brave man who has taken on the task of crafting a new economics is my good friend George Gilder. For those who don’t know, George wrote the seminal work Wealth and Poverty, back in the early '80s, selling over one million copies and influencing a generation. He was Ronald Reagan’s most-quoted living author.

He has written many books since then, but Knowledge and Power is, in my opinion, the most important. I did not simply read this book, I thought through it, as the core premise is truly pivotal for my own thought process.

In Knowledge and Power, George attempts with some success to turn economics on its ear. His great insights are that entrepreneurial creations are the keys to understanding economic progress, and that accumulated knowledge is wealth.

Now, entrepreneurial creativity and innovations are not going to make it into any models that economists can concoct. Because we simply do not have the tools to model that kind of complexity. Let’s dive into George’s theory of “an economics of disorder and surprise that could measure the contributions of entrepreneurs,” and extrapolate out what it means for us.

Identifying the key driver of economic progress

In Knowledge and Power, George lays the groundwork for a new economics:

Capitalism is not chiefly an incentive system but an information system. The key to economic growth is not acquisition of things by the pursuit of monetary rewards, but the expansion of wealth through learning and discovery. The economy grows by accumulating surprising knowledge through the conduct of the falsifiable experiments of free enterprises.

Conventional economics holds that it is incentives—carrots and sticks—which drive individual economic actors to do what they do, and thus leads to economic growth. Although incentives are important, they are not the main driver of growth. The Neanderthal in his cave had the same incentive to eat and access to the same raw materials as we do today. Yet, our economy is vastly more advanced, why?

George says that it is accumulated knowledge, brought about by entrepreneurial efforts, that creates growth and prosperity. I agree. Whether it’s the discovery of penicillin, the creation of the automobile or the printing press, all the “things” which make our lives better and create wealth originate in the mind of the entrepreneur.

Thus, the economy is driven not by “centralized” institutions wielding rewards and punishments, but by an ever-growing pool of knowledge. This knowledge, in a real sense, is the source of wealth: wealth that is ultimately distributed throughout an economy.

But here’s a crucial point: Entrepreneurial creations—the source of wealth—are unpredictable and always come as a surprise. George often quotes former Princeton economist Albert Hirshman on this: “Creativity always comes as a surprise to us. If it didn’t, we would not need it; we could plan it.”

So, if we recognize that entrepreneurial creations are the key driver of growth, but that economic models cannot measure or predict these “surprises,” then we must recognize that traditional economics is useless at measuring the true wealth of the economy.

Thankfully, George has a better way to measure the contributions of entrepreneurs and demonstrate how economics works in the real world.

The foundation of the internet, and a new economics

With traditional economics incapable of measuring how an economy grows, George has applied the principals of information theory to create a new economics:

[A] new economics—the information theory of capitalism—is already at work. Concealed behind an elaborate apparatus, the theory drives the most powerful machines and networks of the era. Information theory treats human creations as transmissions through a channel—whether a wire or the world—in the face of noise, and gauges the outcomes by their surprise. Now it is ready to transform economics as it has already transformed the world.

Developed in 1948 by Claude Shannon, information theory is the basis for all telecommunications and the internet. At its core, it is complex and mathematical, but its implications for economics can be expressed by how it defines information.

The fundamental principal of information theory is that all information is surprise; only surprise qualifies as information. Sound familiar? George recognized the tie between entrepreneurial surprise and information theory: “Claude Shannon defined information as surprise, and Albert Hirshman defined entrepreneurship as surprise. Here we have a crucial tie between the economy and information theory. For the first time, it became possible to create an economics that could capture the surprising creativity of entrepreneurs.

Let’s flesh out how George applies the principals of information theory to economics. At its root, information theory is about distinguishing signal from noise. In technology, a signal goes down a telephone line or through a fiber-optic cable. The challenge is to sort out the actual signal from the noise that accompanies it.

Since communications can be business ideas, information theory is applicable to anything transmitted over time and space—including entrepreneurial creations. In the economy, the entrepreneur has to distinguish amidst the noise, a signal that a particular good or service is needed. But if some force—a government or central bank—distorts the signal by adding “noise to the line,” the entrepreneur could have difficulty interpreting the signal.

It is vitally important that the entrepreneur be able to separate the “signal from the noise,” as processed information leads to knowledge. And as we established above, knowledge is wealth. If the signal cannot be separated from the noise, then no new wealth can be created.

Admittedly, it took me a while to take in the full effects of George’s information theory of economics. I really had to think through the core ideas, and the more I did, the more “a-ha” moments I got.

George lays the groundwork for an economics which places entrepreneurial creativity—the creator of prosperity—at the heart of the economy. It is an economics that appreciates the powerful connection between chaos and creativity, between the disorder and surprise which engender growth. This recognition is the first step toward changing the policies that govern our nation and affect entrepreneurs and investors.

While the information theory of economics is concerned with the forces that create growth, it is also focused on those which hinder it.

Can low-entropy carriers make America entrepreneurial again?

While the information theory of economics recognizes that entrepreneurial creations drive economic growth, it places equal importance on the environment in which they operate:

One fundamental principal of information theory distills that the transmission of a high-entropy, surprising product requires a low-entropy, unsurprising channel largely free of interference.

Another concept George borrows from information theory is entropy, which is defined as “a measure of surprise, disorder, noise, and complexity.” I think of entropy as a spectrum:

-

The low end: Predictable and stable carriers. In technology, a fiber-optic cable is an example of a low-entropy carrier: a system which is largely free of interference and doesn’t cause distortions of the all-important signal it is carrying.

-

The high end: Surprising and unexpected signals. In economics, new creations and inventions by entrepreneurs are examples of high-entropy signals: these signals are disorderly, always come as a surprise, and inject new knowledge into the system.

While “high entropy” signals create knowledge and drive economic growth, they cannot do so without the existence of a “low-entropy” environment or channel.

For example, the success of a radio or internet signal depends on the existence of a low-entropy channel that does not change substantially during the course of communication. If there is “noise on the line,” then the communication may be distorted.

Likewise, the entrepreneur needs low-entropy “channels” to turn the idea in his mind into a product or service. George defines these predictable carriers as “The rule of law, the maintenance of order, the defense of property rights, the reliability and restraint of regulation, the transparency of accounts, the stability of money, and a level of taxation commensurate with a predictable role of government.”

For me, this is the most important part of George’s new economics. The entrepreneur must know that if his product or service succeeds at the market, it won’t be regulated out of existence. And the profits will not be taxed away. If he doesn’t have that assurance, the likelihood of turning his idea into a product or service is greatly diminished. That results in less entrepreneurial creations, which means less knowledge and wealth in the economy.

I would argue, as George does, that the business environment in the US has moved away from being a “low entropy” carrier in the past few decades. The tens of thousands of pages in The Code of Federal Regulations and Tax Code speak to that.

In order for innovation to thrive, and living standards to rise over the coming decades, we must return to a “low-entropy" legal, regulatory, tax, and monetary policy. Too much noisy interference from governments and central banks distorts market signals. They also increase the hassles of doing business, which stifles innovation and discourages entrepreneurship. Ultimately, this makes the country less wealthy and prosperous.

Identifying both the drivers and destroyers of economic growth is what George does so well with his information theory of economics. It has changed how I think about the economy, and what policies we should pursue going forward.

My hope is that President Trump will read Knowledge and Power and give a copy to all cabinet members—as Ronald Reagan did with Wealth and Poverty. Maybe I’m too optimistic, but if we began basing economic and monetary policy on George’s information theory of economics, I believe there would be a complete revitalization of the American entrepreneurial spirit.

If this can happen, I have great hope for the future. That’s because knowledge and wealth originate in the minds of entrepreneurs. As George once said to me, “An economy is a noosphere, and it can be transformed as rapidly as human minds and knowledge can change.”

I often say that every great thinker has one “big idea.” George’s information theory of economics certainly qualifies as one of those. You’ve likely heard me mention how important exposing yourself to these big, powerful ideas is. Well, that’s exactly what I aim to do with my Strategic Investment Conference. I have invited George to speak at the SIC 2018 in San Diego, this coming March.

What a great conference it was this year: great organization and amazing speakers! I was really enthusiastic about it when I came back to the office and now I think my other colleagues want to go as well next year.”

—Herman G. (past SIC attendee)

George is well versed in several areas, so I’m sure we will get into many intense discussions on topics ranging from technology to finance to economics. Yet, George is only one of the speakers that attendees will get to hear and meet. I really hope you can be there to experience it in person, with me. If you’re ready to learn more about the SIC 2018, and the other speakers who will be there, you can do so, here.

That does it for the second installment in this five-part series. Next, you’ll get my insights into Karen Harris’ pioneering work into the declining cost of distance, and the life changing effects this trend is going to have on our lives.

What do you think?

I’d like to get your thoughts and questions regarding George’s theory for a new economics.

You can post any questions or comments about George’s information theory of economics, or this five-part series, below. I’m looking forward to hearing from you.

Your hoping Washington adopts this new economics analyst,

John Mauldin

Chairman

![]()

Essay 3 Featuring Karen Harris

The Declining Cost of Distance Is Going to Change Everything

By John Mauldin

“It’s hard to be a pioneer. But you can’t expect universal approval when you’re doing something completely different.” – Karen Harris

“By 2025, we see the US and other technologically advanced countries at the forefront of defining a new post-urban economy. Spatial economics will give rise to new markets, more innovative businesses, new lifestyles and different career opportunities.”– Karen Harris

In the past few years, automation and the effect that it’s having on the workforce has become a hot topic of conversation.

Almost daily, in the WSJ or on Bloomberg, you’ll see an article about automation and how it’s negatively impacting employment. At the same time, major research institutions like McKinsey, Brookings, and Pew are releasing studies on the topic.

Findings from these studies all draw the same conclusion: 30–40% of US jobs will be lost to automation over the next 20 years. When I see multiple forecasts, which arrive at the same conclusion, I get a little nervous.

When the consensus expects one thing to happen, quite often the exact opposite ends up occurring. Here are two reminders of just how wrong the consensus can be.

Sources: The Economist, Forbes

-

March 1999: Oil was at $12, and the consensus said it was headed lower. As we know now, that was pretty much the bottom for oil prices.

-

November 2007: Nokia had a 37% market share, and its stock price was $39. Today, it has less than 2% of the market, and its stock price is below $5.

Needless to say, investors who allocated capital according to these prevailing thoughts would have been on the wrong side of two seismic shifts.

While automation and technology are having a massive effect on employment, when I see everyone falling into line with the consensus, my “inner-contrarian” alarm bells go off. When this happens, it tells me that I should seek out independent and unique perspectives.

Someone who offers exactly that is Karen Harris. I would wager you have never heard of Karen. If not, it’s my delight to introduce you to her and her ideas.

Karen Harris is the Managing Director of Bain & Company's Macro Trends Group. Karen and her team at Macro Trends focus on developing insights about global macroeconomic and social trends. They also work with institutional clients to embed macro strategy into their investment and business decisions.

I am featuring Karen in this five-part series because of her pioneering work on the declining cost of distance–a topic which fits hand in glove with automation, and has profound implications for investors and entrepreneurs.

Before we proceed, I want to let you in on a secret: Karen’s work on spatial economics and the declining cost of distance made me rethink my thoughts on the US economy, and how society will function in the future.

The declining cost of distance may be the one of the overarching trends that shapes the economy and financial markets in the coming decades. When I say this is one of the most critical concepts to grasp going forward, I mean it.

Today, I’m going to take you through this concept, and show you what it means for us. Let’s dive straight in.

The key driver of where you live and work is changing rapidly

Macro Trend’s report, titled: Spatial Economics: The Declining Cost of Distance, opens with this thought:

“For centuries, the cost of distance has determined where businesses produce and sell, where employers locate jobs and where families choose to live, work, shop and play.”

While not widely recognized, the cost of distance—that is, the cost of moving information, people, and goods—is a key driver of business and individual decision-making.

For example, the cost of moving goods is the reason why companies like Amazon strategically place their warehouses near major transportation routes. On an individual level, the cost of moving oneself is the reason you would ideally live near your workplace.

The need to minimize the cost of distance has caused businesses and individuals to cluster around urban areas. This trend began during the Industrial Revolution 250 years ago, when millions of people moved to cities to work in factories. As Karen notes “Cities are dense urban hubs that minimize the cost of moving raw materials, labor and finished goods.”

To date, the cost of distance has remained a critical calculation for businesses and individuals regarding where to operate and live.

Which leads to the question: How would the world change if the cost of distance fell dramatically and greatly reduced the importance of location? Well, thanks to technology and automation, we’re starting to find out.

Technology is enabling a post-urban world

From the Macro Trends report:

“The catalyst for this historic shift [are] new technologies that have pushed the cost of distance to the tipping point. Robotics, 3-D printing, delivery drones, logistics technology and autonomous vehicles are giving rise to new products and services that sharply erode the cost of moving people, goods and information.”

Let’s look at how technology is reducing the cost of moving information, goods, and people:

-

Information: Compare the cost of sending information via an email to sending it by postal letter. Or the cost of making a long-distance phone call today versus two decades ago.

-

Goods: Data from The World Bank show that the cost of transporting goods by air and ocean freight has dropped substantially over the past 40 years. Going forward, autonomous vehicles and delivery drones are expected to reduce the cost of transporting goods by a further 75%, according to Macro Trends.

-

People: The rise of online communication channels and computer systems has enabled many individuals to work from remote areas, so they no longer have to travel to an office.

Technology is creating a post-urban world in which physical location will not be the primary driver of where people live. This is the biggest shift in how economies function since the Industrial Revolution, when the population of London and other English cities doubled in just 50 years.

The declining cost of distance will allow millions of individuals to reassess where they live. At the same time, constraints on businesses such as scale and density will be reduced, creating new opportunities for businesses, investors, and entrepreneurs.

Think about where you would live if you could work from anywhere. Or, what would happen to urban economies and real estate prices if millions of people decided to leave? These are just two factors to consider on how the declining cost of distance is a complete game changer.

Let’s run through some of the implications.

How businesses will change when distance doesn’t matter

From the Macro Trends report:

“As the cost of distance declines, companies will be able to deliver economic output at smaller scale. Advances in technology already are beginning to lower costs in manufacturing and service, allowing both to be profitable at reduced scale.”

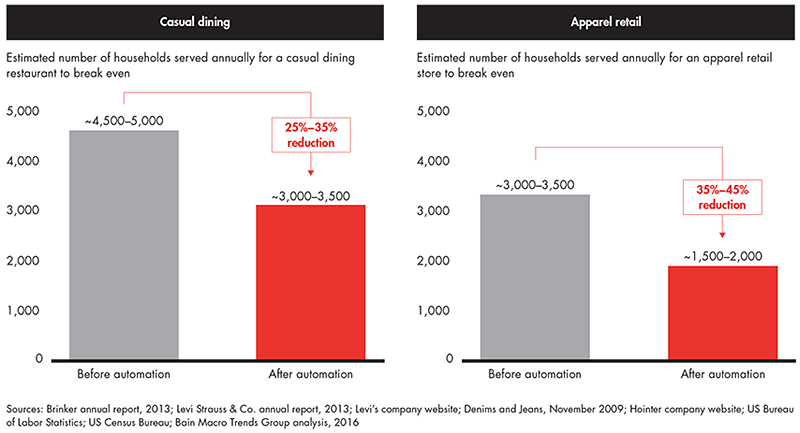

The declining cost of distance will allow businesses to operate at a smaller scale, which will disrupt the tight constraints that most operate under, today. Let’s use the average Apple store as an example of how this is going to completely change the economic landscape.

Today, a 6,000–8,000 square-foot Apple store requires a population of roughly two million people within its target radius to be profitable. This required population density is a huge barrier to entry, making small operations completely unviable. But I have good news, automation is changing that.

According to research from Macro Trends “with service robotics, an Apple store will potentially be able to thrive in a population center with 200,000 inhabitants instead of 2 million.”

Automation is also changing the business model of casual dining outlets like McDonalds and Burger King. As the following chart from Macro Trends shows, with the help of automation, these outlets will be able to reduce their break-even costs by 30%, annually.

Now, here’s why the declining cost of distance fascinates me—and why it offers a unique perspective on the link between automation and employment.

On the surface, automation is bad for jobs. For example, Macro Trends estimate that by employing service robots, casual dining outlets could reduce staff from 25 to 8 people. However, as automation will enable businesses to operate at a smaller scale and scope, it may create jobs net-net. Hear me out.

While automation will reduce the number of people working at each location, by lowering operating costs, automation will make smaller scale and scope locations economically viable. In effect, the volume of stores would increase, while the number of people working at each location would fall.

For the first time ever, large retailers and dining chains will be able to operate in smaller, less dense markets. The large retail stores and restaurant chains that I have the pick of here in Dallas, may open locations in the much smaller neighboring cities of Allen and Katy.

As I mentioned above, when there is a strong consensus on a topic, it almost always pays to seek out an independent view. While automation will render some jobs obsolete in the coming decades, I believe it will also create a lot of opportunities. Karen and Macro Trends’s groundbreaking research into the declining cost of distance has convinced me of that.

Along with changing how businesses operate, the declining cost of distance will also alter where individuals choose to live and how they work.

How does low-cost, rural living with a city wage sound?

From the Macro Trends report:

“Individuals may opt to live further from city centers, as advances in transportation and connectivity allow them the abundant space of a rural town combined with many of the employment options, goods and services once available only in cities.”

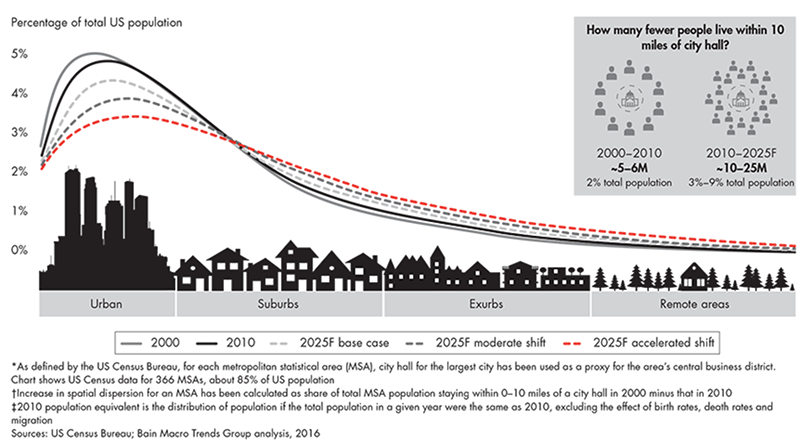

According to the US Census Bureau, the percentage of the US population that lived within 10 miles of a city center declined by 2.2% between 2000 and 2010. That might not seem much, but it represents almost 6 million people—more than double the population of Chicago.

While the declining cost of distance is only beginning to gather pace, it is likely one of the reasons for this move away from cities.

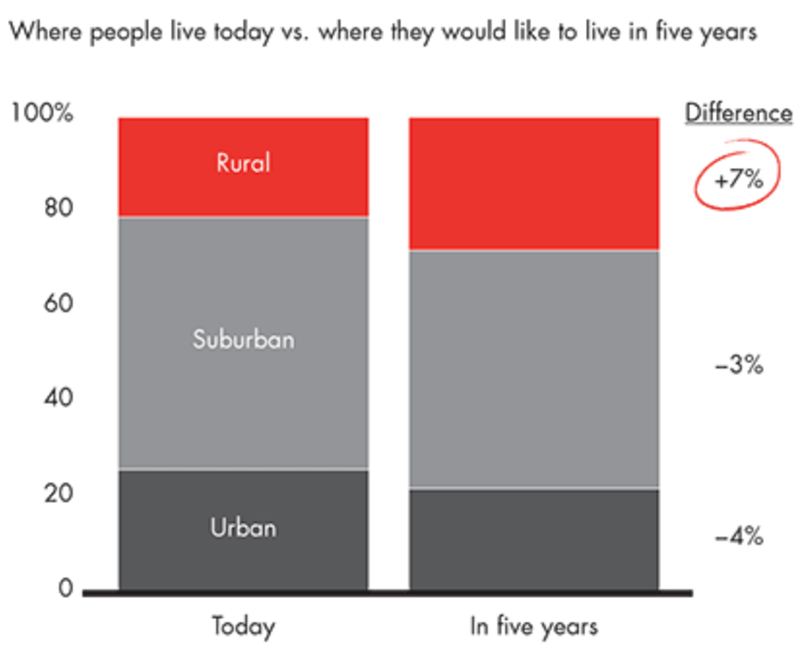

As more businesses open locations in less dense, rural areas, these areas will become more attractive places to live. A 2016 Macro Trends poll shows that an increasing number of people want to live in rural areas.

However, a greater variety of amenities is only the start of how the declining cost of distance is going to transform rural areas… and possibly cities, too.

Virtual communication tools and computer systems are giving people who live in rural areas access to many of the same employment opportunities that city dwellers have.

As opportunities to telecommute (work remotely) increase, fewer people will need to travel to work. Already, 37% of US workers say they work remotely or have done so in the past. That’s a four-fold increase since 1995.

This trend toward working remotely is actually very close to my heart, it’s how Mauldin Economics operates. Since my partners and I founded the company back in 2012, we have been a “virtual business.” Although we have over 40 members of staff, no more than three of us are in the same location. Right now, my team lives in a wide range of locations: from Dallas to Dublin, Ireland, and Vermont to Vilnius, Lithuania.

While we operate across several time zones and live in vastly different locations, thanks to online communications tools and shared computer networks, we operate as if we were all under the one roof. At the same time, the absence of an office greatly reduces overhead costs. Best of all, each one of us gets to work from wherever we please.

Take my friend and colleague Jared Dillian, for example. When Jared was working at Lehman Brothers in New York, there was no escaping the ultra-high cost of living. Today, Jared is able to work from his beachfront home in South Carolina. Geographic arbitrage.

Karen and the Macro Trends team believe this trend of de-urbanization is accelerating:

“The declining cost of distance has the potential to trigger a major lifestyle shift away from city centers, similar in scope and impact to the US suburban exodus between 1950 and 1980. Based on that scenario, we would expect the move out of US urban centers between 2010 and 2025 to rise to about 6% of the population per decade, or up to 24 million people in total by 2025.”

As the following chart from Macro Trends shows, its base case is that a further 10 million people will move out of urban areas by 2025.

A move of this magnitude would have massive implications for the economy and the employment landscape.

For example, a mass exodus to rural areas could create a boom in the construction industry, akin to what took place in the 1950s. Conversely, urban real-estate prices, which are notoriously high across the globe, could plummet as demand falls.

Still, there are a lot of unknowns. Would millions of Americans switching from urban to rural living ignite a baby boom and cure our demographic problems? It’s certainly not out of the question. After all, birthrates are substantially higher in rural areas. Plus, families could dramatically reduce their cost of living by moving out of cities, allowing them to feed more mouths.

This is just the tip of the iceberg. I have many more questions I want answered about the declining cost of distance.

For example, what are the opportunities and risks for investors, and how will the reduction in the scale and scope of businesses in advanced economies affect emerging markets?

Karen will address these questions and provide other insights from her team’s work at Bain, when she delivers what promises to be an enthralling speech at my Strategic Investment Conference in San Diego, next March.

Yet, Karen is only one of the brilliant minds that you’ll get exposed to and have the chance to meet at the SIC. It’s going to be an intellectually thrilling event, and I hope you can be there with me to experience it firsthand. To learn more about attending the SIC 2018, and about the other speakers who will be there, I encourage you to click here.

I attended my first conference this year and loved it! I am a small investment manager just starting out, so I was looking to gain some perspective on how to protect my portfolio and profit from likely events that will be occurring in the future.

—Matthew (past SIC attendee)

That concludes the third part of this series. In the next installment, I share my thoughts on Lacy Hunt’s “big idea” that fiscal and monetary policy have become incapable of generating growth.

Before you go...

I want to get your thoughts and questions regarding Karen and her insights into the declining cost of distance.

You can post any questions or comments about Karen and her team’s work, or about the other essays in this five-part series, in the comment section below.

Your memorized at how technology is changing the entire world analyst,

John Mauldin

Chairman

![]()

Essay 4 Featuring Lacy Hunt

The Fed Has Put Itself Out of Business, Where to Now?

By John Mauldin

New federal initiatives—whether tax cuts, infrastructure, or otherwise—will not provide a boost to the economy if they are funded with increases in debt.

—Lacy Hunt

As a young bond manager during the Great Inflation and Richard Nixon’s wage and price controls, Lacy Hunt saw the bear market in bonds coming in the late 1970s and made a fortune for his clients.

—Bloomberg

I often write about the Fed’s abysmal track record in managing the economy. The main reason they have consistently got it wrong is that they are hampered by their “dual mandate,” which sets “the goals of maximum employment, stable prices, and moderate long-term interest rates.” I know, that is actually three goals, not two, but let’s run with it.

The rationale behind their dual mandate is that by keeping inflation and interest rates steady, they will create a stable economic environment, which will be conducive to employment growth. In theory, the Fed’s mandate works well:

-

When the economy is slowing: The Fed lowers interest rates, spurring economic activity. This helps the economy avoid recession.

-

When the economy is booming: The Fed hikes interest rates, slowing activity. This stops the economy from overheating.

It’s like the Fed has a leaver that they pull, which keeps the economy at near equilibrium. In reality, it doesn’t work that way.

As there is a time delay between the Fed’s actions and the impact of those actions, they invariably overshoot the mark. Fed actions end up working in a pro-cyclical, instead of a counter-cyclical, manner. The Fed’s failures are directly tied to the problems facing the US economy today.

Strict adherence to their dual mandate has made them blind to certain economic developments. For example, while the Fed was focused on unemployment and inflation during the 1990s and early 2000s, they failed to do anything about the massive buildup of debt. This laid the groundwork for the financial crisis.

Sources: Hosington Investment Management

The Fed’s failure to address over-indebtedness has caused irreversible damage to the economy. When debt levels rise past a certain threshold, additional debt-financed stimulus becomes ineffective. Worse yet, when an economy becomes extremely indebted, monetary policy stops working altogether.

I often get asked if I am still a deficit hawk. The answer is, “Yes, more than ever,” because current debt levels are rendering monetary and fiscal policy ineffective. And that, my friends, is a game-changer.

With traditional methods of stimulus incapable of spurring growth, what will happen in the next downturn? As this trend develops, it could force a rewiring of the financial system and a deleveraging of the global economy. Given the wide-ranging implications, this is a critical trend for investors to grasp.

When I need insight into the relationship between debt and the economy, there is one person I turn to. And that is my dear friend, Lacy Hunt. You almost certainly know Lacy, but in keeping with the spirit of this series, I’ll give him a brief introduction.

Lacy Hunt is the executive vice president and chief economist at Hoisington Investment Management. Lacy was also the chief US economist for HSBC, and senior economist for the Federal Reserve Bank of Dallas.

I’ve known Lacy for over 25 years, and I can say without hesitation that he has been, and continues to be, one of the most influential people on my thought process. I really do enjoy picking his brain about all things economics. I regularly phone him on a Monday morning when something is puzzling me.

Today, I want to focus on Lacy’s insights into the debt overhang and how it has made the US economy resistant to fiscal and monetary stimulus. As Lacy says, “By allowing the country to become extremely over-indebted, the Fed has put themselves out of business.”

Let’s begin with Lacy’s thoughts on the huge debt burden, and why it is having a dilapidating effect on the economy.

The Definition of Insanity

In a recent interview, Lacy cited a study by the McKinsey Global Institute which analyzed dozens of instances where countries had become over-indebted:

In 2010, McKinsey looked at 24 advanced economies that became extremely over-indebted. [The findings] show that an indebtedness problem cannot be solved by taking on additional debt. McKinsey says that a multi-year sustained rise in the savings rate, what they term austerity, is needed to solve the problem. As we all know, in modern democracies, that option doesn’t seem to exist.

A decade on from the financial crisis, instead of deleveraging, our debt burden has increased. I referenced these figures in the first part of this series, here’s a quick reminder:

-

Since 2008, total Federal government debt has increased by 113%

-

Nonfinancial corporate debt is up 79% over the same period

-

Household debt has surpassed its previous all-time peak which was made in Q3 2008

All this debt hasn’t spurred economic growth because the economy was over-indebted to begin with. As Lacy often says to me, “starting points are critical, John.”

Research from Carmen Reinhart and Kenneth Rogoff shows that when a country’s government debt-to-GDP ratio stays over 90% for more than five years, its economy loses around one-third of its growth rate. Lacy also points out that “the longer the debt overhang persists, the relationship between economic growth and debt becomes nonlinear.” This is happening to the US today with the economy growing at only half its long-term growth rate.

Sources: Hosington Investment Management

Until the debt burden is reduced, further debt-financed stimulus will not spur growth. It’s that simple. One only has to look at the insignificant effect that the $800 billion+ American Recovery & Reinvestment Act had on growth in 2009 to see this problem in action.

While nobody in Washington seems to have realized that our debt problem cannot be solved by more debt, it is important for investors to keep this in mind when allocating capital. Future tax cuts and other fiscal measures may generate spurts of growth, but given the debt burden, it will fizzle out shortly thereafter.

Although the amount of debt in itself is acting like a millstone around the economy’s neck, the type of debt being created is worsening the problem, significantly.

Pouring Money Down the Consumption Drain

At my Strategic Investment Conference this past May, Lacy commented on the type of debt being borrowed:

The composition of our debt is becoming increasingly inferior. We have the wrong type of debt. We’re taking on debt that is not going to generate an income stream, and that feeds financial speculation. That may benefit some, but not the society at large.

The debt has become so burdensome because much of it is for consumptive purposes and doesn’t generate an income stream to repay the principal and interest.

For example, look at Federal government spending. In 2017, mandatory spending totaled $2.7 trillion, of which almost half went toward social security. As Lacy puts it: “The [debt being created] is going back into our household sector, not into productive end uses. It’s going to finance daily living needs, the least productive type of debt.”

But the government doesn’t have a monopoly on borrowing debt for unproductive uses, corporations are also quite good at that.

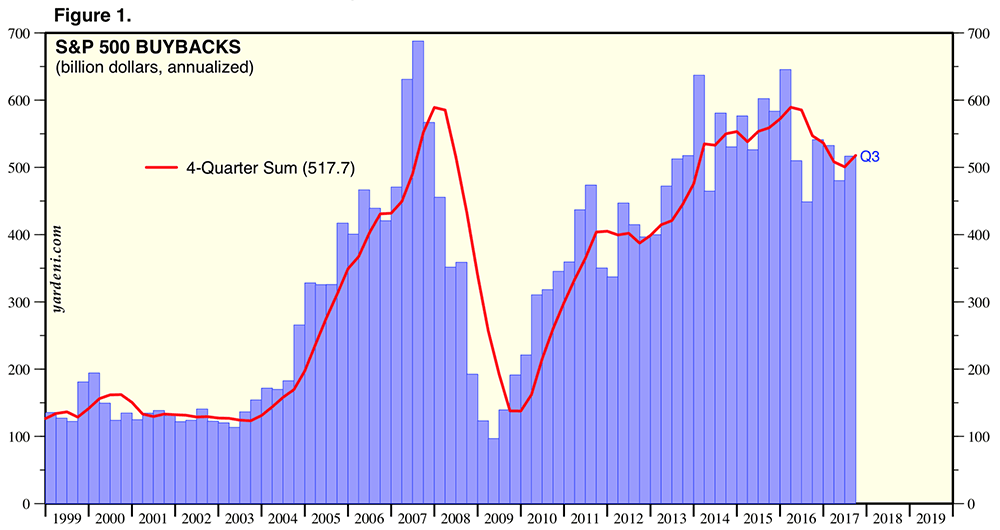

In 2016, total corporate debt increased by $717 billion, yet investment in plant and equipment fell by $21 billion. Where did the money go? The majority of it has gone toward share buybacks and dividend payouts. It has been a similar story over the past decade as buybacks have risen to near record levels.

Sources: Yardeni Research

The Fed is at the heart of why corporations have preferred financial investments over real investments. In Lacy’s words, “When the Fed undertook QE, they gave a signal to the corporate managers: Your financial investments are protected by us, but we can’t do anything for you on the real side.”

While equity prices and shareholders have increased as a result of financial engineering, it has done nothing to increase the growth capabilities of the US economy.

Economists have been perplexed by the absence of growth and inflation over the past decade. The unproductive nature of the debt being borrowed goes a long way to explaining why. As I discuss next, this trend is ensuring growth is unlikely to return anytime soon.

Velocity Is Freefalling

In a recent interview, Lacy detailed why economic growth has been poor and will continue to be so:

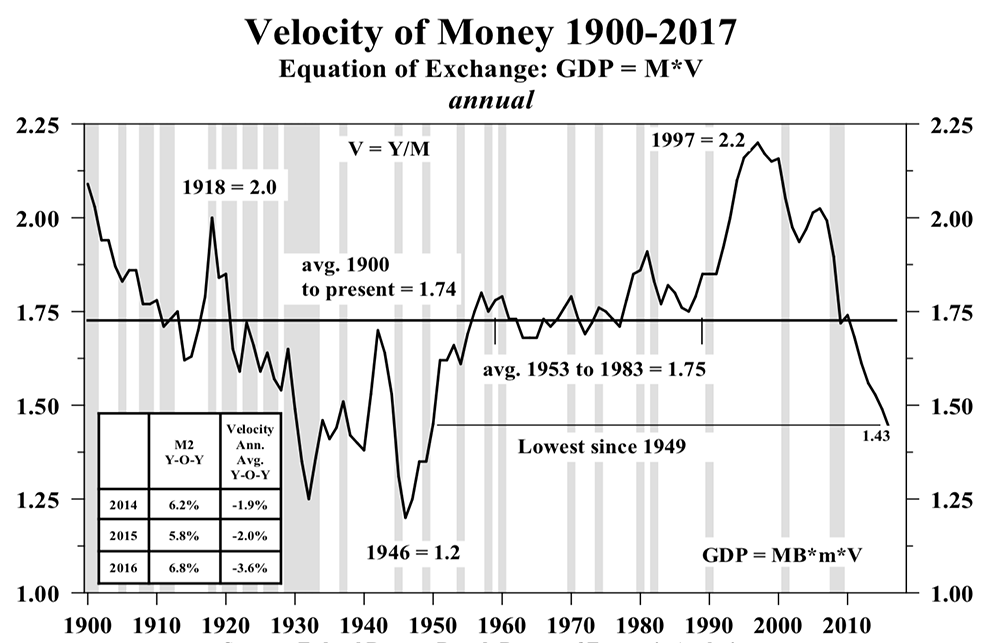

The critical factors that determine GDP are both working lower. [We are] experiencing considerably slower growth [in the] money supply, at the same time the velocity of money is in a major downtrend. In 1997, $1 of new [money] increased GDP by $2.20. [Now] it is $1.43. This reflects the fact that we have too much of the wrong type of debt.

You may think the velocity of money is some obscure indicator used only by economists. But as Lacy pointed out, it is one of two determinates of nominal GDP, our most important economic indicator.

Put simply, the velocity of money measures the rate at which money is exchanged from one transaction to another, and how much it is used in a given period of time. Therefore, if money is being used for unproductive purposes and doesn’t generate an income stream, velocity will fall.

I think of velocity as a machine which money has to go through to produce economic activity. If the machine is on a low setting, it doesn’t matter how much money you put in—you won’t get growth. The falling velocity of money, which is at its lowest point since 1949, is another reason why growth has remained subdued in the post-financial crisis world.

Sources: Hosington Investment Management

Velocity can also tell us about the long-term direction of bond yields. As velocity is a main determinate of nominal GDP, and yields track nominal GDP, Lacy believes that the secular low for interest rates are not in hand: “In my view, we will not see the secular low in interest rates until the velocity of money reaches its secular trough, and that is not something that’s going to happen soon.”

This is why I consider Lacy’s insights invaluable. His ability to always see the big picture in spite of short-term market moves is truly exceptional. It’s no coincidence that his mutual fund has beaten its benchmark by a wide margin over the past two decades.

While the debt burden is putting downward pressure on velocity, which is dampening growth, it is also incapacitating monetary policy.

Monetary Policy Has Become Asymmetric

Here is Lacy explaining how debt has rendered monetary policy ineffective at stimulating growth:

The root cause of [monetary policy’s] underperformance is extreme indebtedness. The debt creates a situation where monetary policy capabilities are asymmetric. In other words, a lot of action is needed to provoke even a muted impact on the economy, whereas the slightest monetary tightening goes a long way in depressing economic activity.

Again, the reason why inflation and growth have remained anemic despite record-low interest rates and multiple rounds of QE is the over-indebtedness of the US economy.

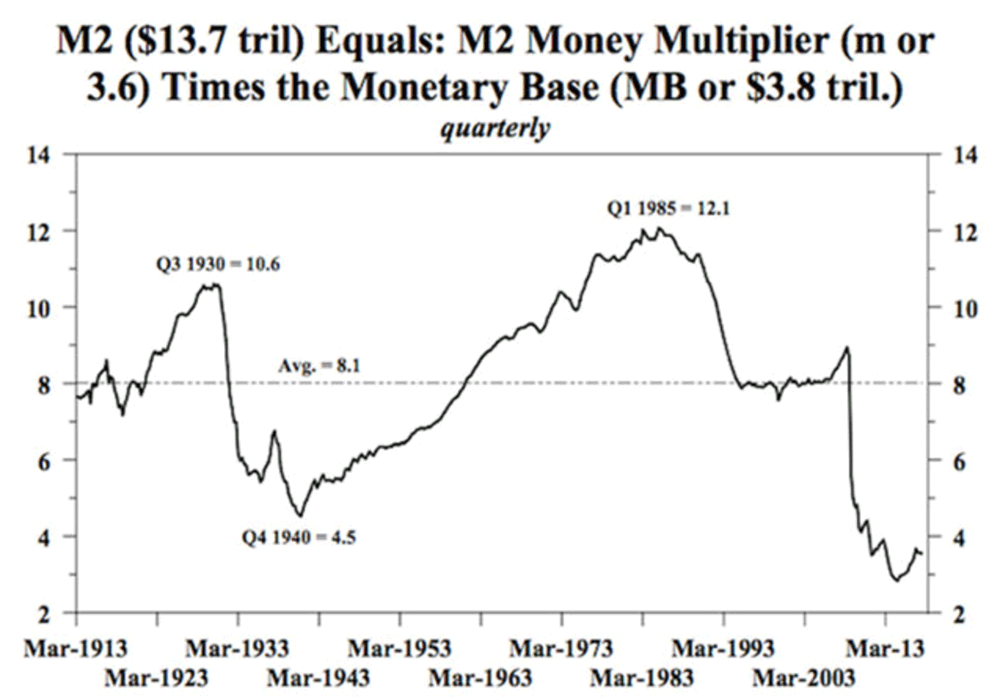

I don’t wish to get too deep into the weeds here, but to explain this, you have to look to the money multiplier. The money multiplier is the amount of money that banks generate with each dollar of reserves. Due to the over-indebtedness of the economy—or more precisely, the lack of “savings”—the multiplier has plunged from 12.1 in 1985, to 3.6 today.

Sources: Hosington Investment Management

Just as falling velocity has blunted fiscal stimulus, the decline in the money multiplier has made monetary easing less effective in generating growth.

Unfortunately for the Fed, monetary tightening has become more powerful because of the debt. Lacy mentioned in his latest quarterly review that, “Excessive debt, rather than rendering monetary deceleration impotent, actually strengthens central bank power because interest expense rises quickly. Therefore, what used to be considered modest changes in monetary restraint that resulted in higher interest rates now has a profound and immediate negative impact on the economy.”

This outsized effect can be seen by looking at how the five rate hikes since December 2015 have produced a noticeable slowing in the growth of the money supply and several important areas of bank lending.

Given the strong impact the five 25-basis-point hikes have had on the money supply and bank lending, I am highly doubtful that the Fed can continue on their current tightening path. I am more convinced than ever that the over-indebtedness of the nation is the biggest challenge facing the US economy.

Where Do We Go from Here?

Lacy often quotes David Hume, the great Enlightenment thinker, regarding the debt situation: “When a state has mortgaged all of its future liabilities, the state, by necessity, lapses into tranquility, languor, and impotence.”

Will the US and other advanced economies lapse into languor and impotence now that monetary and fiscal policy become incapable of generating growth? Even before we reach the endgame, there are many questions to be answered.

Given the outsized effect that monetary tightening is having on the economy, will the Fed be able to continue on its current tightening program? How are stocks and bonds likely to perform in this environment? And how will the coming wave of retirees, which will significantly increase mandatory spending, affect the measures I discussed in this letter?

There are many twists and turns ahead. As investors, we must prepare for every eventuality.

I know nobody better qualified to provide insight into where we are today, and where we are headed, than my dear friend, Lacy Hunt. That’s why I’ve invited him back to speak at my Strategic Investment Conference, in San Diego, next March.

Lacy has spoken at almost every SIC since inception and each time he has put on a masterclass for attendees around debt, monetary policy, and the economy. I know this year will be no different because he always brings his A-Game.

His expertise is the reason why Lacy is one of the highest ranked speakers, every single year. I’m really excited to see what Lacy has to say at the SIC, and I hope you can be there in person to experience it with me. Learn more about attending the SIC 2018, and about the other speakers who will be there, here.

“Another great conference. I will echo what many others say... that this is the best conference that I attend each year.” —Michael P (past SIC attendee)

So, that’s the fourth installment in this series wrapped up. Although we have covered four groundbreaking ideas, I think the best may be yet to come. In part five, you’ll get my insights into Niall Ferguson and his thoughts on why the liberal international order is over.

Before you go...

What are your thoughts about Lacy’s research into debt and the effect it is having on the economy?

I’d love to hear your questions or comments about Lacy’s insights—or anything else on this five-part series. Please post them in the comment section below.

Your wondering how this debt situation gets resolved analyst,

John Mauldin

Chairman

![]()

Essay 5 Featuring Niall Ferguson

What Does the End of The Liberal International Order Mean for Markets?

By John Mauldin

“Globalization [has] overshot and produced a quite legitimate backlash. While people like me were enjoying Davos and Aspen and saying how marvelous the Liberal International Order was, a rather large number of ordinary Americans were not feeling quite so chipper.”

—Niall Ferguson

“Niall Ferguson is not the kind of historian who suffers from understatement. He writes big, muscular books with high-concept ideas that target current concerns through the prism of the past. They are pull-yourself-together warnings to the present by way of arresting historical precedent.”

—The Guardian

If there is a sentence (or two) that encapsulates my thoughts on globalization, it is the William Gibson quote I’ve used many times at the opening of my letters: “The future is already here. It’s just not evenly distributed yet.”

The benefits of globalization have been unevenly distributed, and those who have been on the short end of the curve are pushing back. Given the dire situation millions of Americans are in today, I don’t wonder why they are doing so; I wonder what took them so long.

According to a 2017 study by the Federal Reserve, 44% of Americans wouldn’t be able to cover an unexpected $400 expense without borrowing or selling something. Yes, nearly half the country can’t come up with $400 cash in an emergency. That’s stunning. The slightest mishap—a toothache, a minor car problem—will send them into debt or force them to sell something.

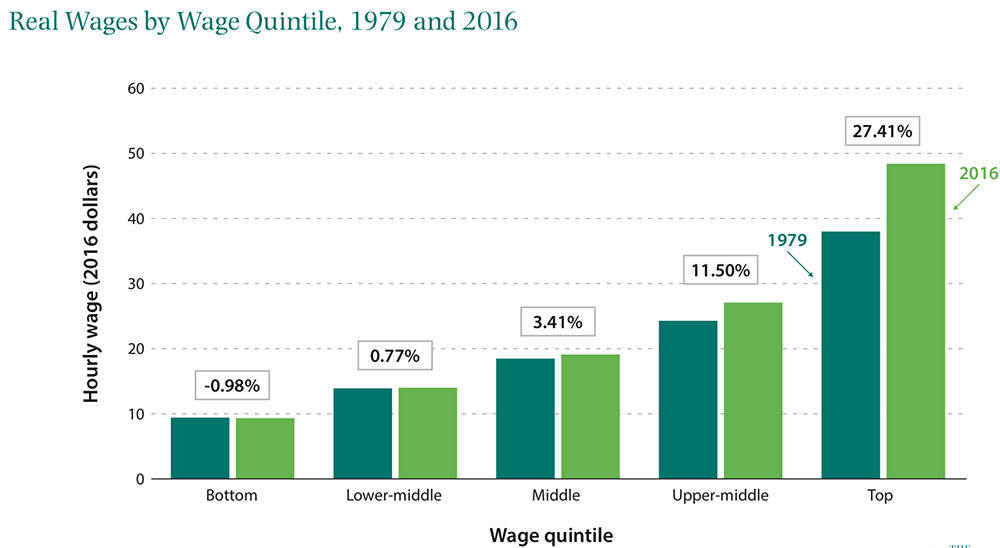

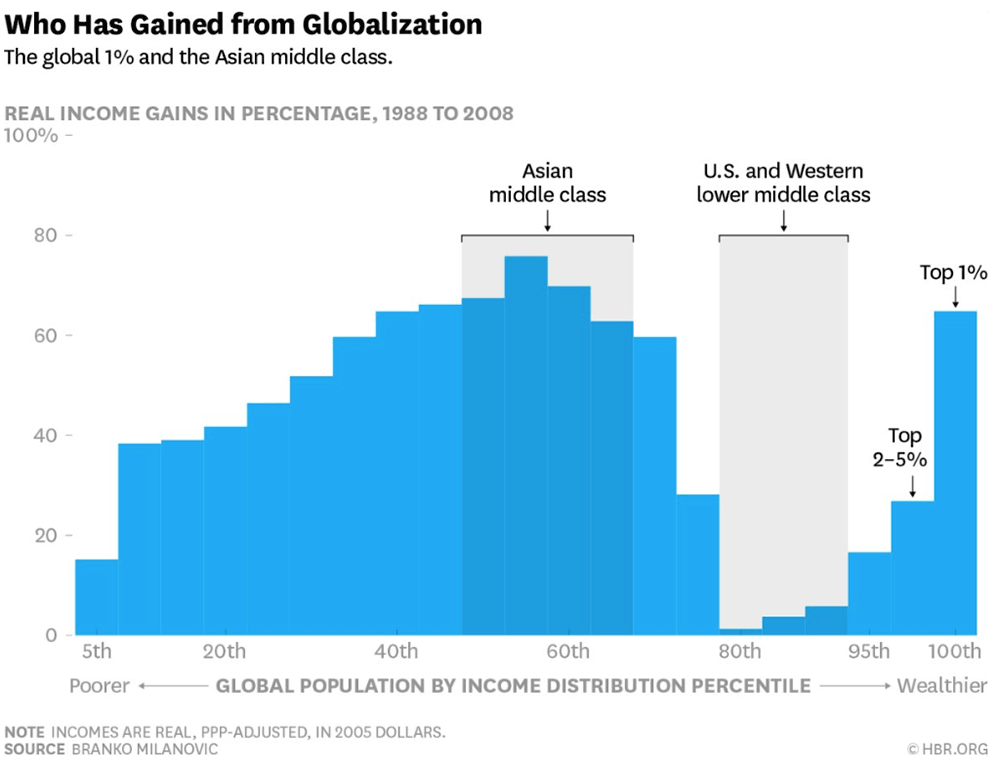

This situation is the result of decades of stagnant wage growth. Since 1979, real (inflation-adjusted) hourly wages for the bottom quintile of earners fell by 1%. Worse, the inflation adjustment is based on the CPI, which as I’ve said many times, understates the real cost of living for most people. But wages haven’t stagnated for everybody. As the below chart shows, real hourly wages for the top quintile of earners have increased by over 27% in the same period.

Source: Brookings Institute

Income gains for the top 10% of the population rose roughly in line with that of the bottom 90% from 1930 to 1970. What happened in the 1970s to cause this divergence? The chief suspect is China’s opening to world trade and the onset of globalization.

Over the past four decades, globalization has enabled the transfer of millions of jobs from the US to various emerging-market countries. It changed the relative value of capital and labor all over the world. The top earners started getting a larger share of their income from investments than from their labor. They own the “means of production,” and the producers did increasingly well from the ’70s forward.

Nobody paid much attention to the unevenly distributed benefits of globalization, until around 40 million Americans lost their jobs in the 2007–2009 recession. Now, the backlash has begun, and it’s not going to stop until the situation improves for those who have been left behind.

Globalization has lost its political support, and that raises an important question about the future of the global economy. If globalization has fallen out of favor with large swaths of the voting public, what does the future look like for the American-led order which has promoted economic liberalization and liberal values around the world since the end of WWII?

This system, defined as the Liberal International Order, is the framework of rules, alliances, and institutions that is credited with the relative peace and prosperity the world has enjoyed since 1945. So, if the order has lost support, will the world plunge into beggar-thy-neighbor protectionism? Worse, without the threat of military intervention by the US and its allies, will regional powers start to challenge one another?

One man answering these pressing questions is my good friend, Niall Ferguson. I’m sure most of you have heard of Niall, but for those who haven’t, it is my great pleasure to introduce him to you.

Niall Ferguson is a senior fellow at Stanford University, and a senior fellow of the Center for European Studies at Harvard, where he served for twelve years as a professor of history. Niall is one of the finest economic historians on the planet; but he isn’t only an academic. What many people don’t know is that he works with a small group of elite hedge fund managers and executives as the managing director of macroeconomic and geopolitical advisory firm, Greenmantle.

Niall has made a habit of tackling topics that have significant importance in his career. But in my opinion, this is the most critical question Niall is attempting to answer: “Is the Liberal International Order over?”

Before we dive in, I want to make clear that the goal of this letter is not to say whether liberal internationalism is good or bad, or defend the backlash against it. My objective is to highlight the current state of the order and give insight into Niall’s argument behind why he believes it is over. As investors, it is imperative we understand this trend because it has major implications for financial markets we need to think about. With that being said, let’s dive straight in.

The fate of the Liberal International Order rests on Pax Americana

In a recent interview, Niall pointed out the potentially fatal flaw in the Liberal International Order:

“If the world has been more peaceful since WWII, the main reason is not because of the Liberal International Order, it’s because the United States had decided to play a leadership role. The big story after 1945 was the Pax Americana. The big story since 9/11 has been its crumbling.”

While the Liberal International Order and its institutions are credited with the relative peace the world has enjoyed since 1945, Niall says, “That's a very implausible argument.” He believes the world has been more peaceful because of the will and capacity of the US to be the principal guarantor of the system. This is often referred to as Pax Americana, in which the US employed its overwhelming military power to shape and direct global events.

This reliance on US strength hasn’t been a problem for the past seven decades, but times are changing. Since the financial crisis, the US has been less willing to bear the costs needed to be the guarantor of the international order. Niall highlights the inaction over Russia’s annexation of Crimea in 2014, and the “little more than cosmetic” strikes against Syria as signs that the US is starting to take a more ambivalent approach to global conflicts.

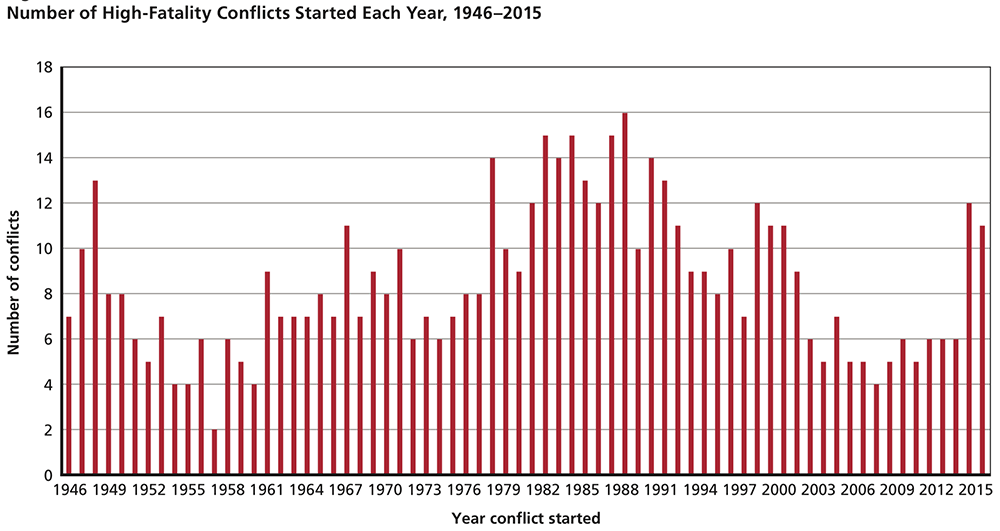

Without US willingness to use military power to establish balance across the world, it’s likely the liberal order will buckle under the unrestrained competition of regional powers. As the below chart shows, there has already been a sharp rise in the number of armed conflicts around the world.

Source: RAND Corporation

As Niall pointed out: “Things are becoming quite disorderly for the liberal order.” Before we go on, I want to make a critical point. Whether you support military intervention, or not, isn’t the issue here. The issue is that without the US playing the role of guarantor, we are likely to see a rise in conflicts. That is going to affect financial markets and your portfolio.

The second “pillar” of the Liberal International Order, economic liberalization, is also under strain.

Peak globalization is in the rearview mirror

Niall points to falling global trade and capital flows as another symptom of the Liberal International Order being over:

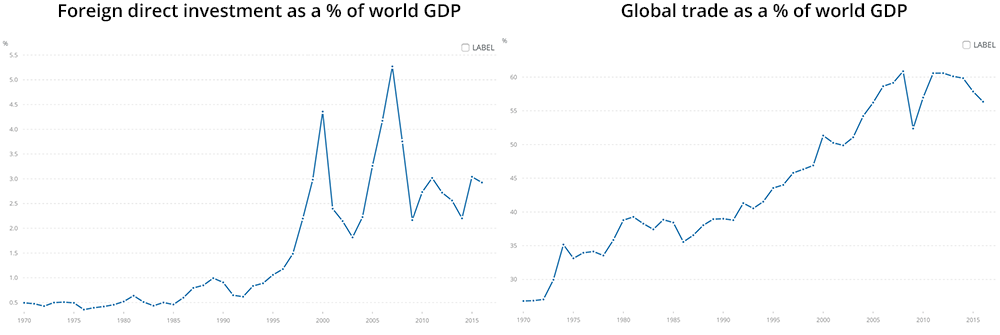

“Peak globalization is already behind us. Trade is no longer growing at the rate it did prior to the financial crisis, and international capital flows have fallen too.”

Since peaking in 2007 and 2008, respectively, trade and foreign direct investment as a percentage of world GDP have fallen sharply. McKinsey Global Institute found that global flows of goods, finances, and services have declined by 15% since peaking in 2007.

Source: World Bank

I believe “peak globalization” is in the rearview mirror. I say that not only because cross-border flows have declined precipitously, but because we are headed into a period of protectionism. US withdrawal from the Trans-Pacific Partnership is the most high-profile instance so far, but there are several more.

The governments of Australia and Canada have taken measures to curb foreign ownership of real estate. New Zealand has taken this a step further by outright banning foreign ownership of real estate. In Europe, there have been several “behind the border” restrictions enacted by countries, which are designed to bolster domestic industries. Thus, it seems to me even the most liberal of countries are realizing globalization has overshot.

The rise of protectionism has serious implications for investors. We have become used to companies being able to break into new markets and the idea of “multinational corporations.” This may not be the case going forward. Investors will have to pay a lot more attention to where the companies they choose to invest in operate, and where their sales come from. In short, protectionism is on the rise and investors must prepare accordingly.

Longtime readers will know that I’m second to no one in defending free trade—but I also see the reality, which is that it has had a dark side. And that dark side is another symptom Niall has pointed to as proof that the International Liberal Order is over.

Globalization has killed the goose that lays the golden eggs

Although the Liberal International Order has benefited some, Niall points out that it has been very bad for millions of ordinary Americans:

“While it's great to say that 300 million Chinese people have been pulled out of poverty, the reality is that there has been, at the same time, a significant erosion of living standards for middle-class and working-class Americans.”

I mentioned at the beginning of this letter that the benefits of globalization have been unevenly distributed. As the below chart shows, the big losers have been the American middle and working classes.

Source: Harvard Business Review

Globalization has been bad for these sections of society because it changed the relative value of capital and labor. When capital and goods could flow freely between the US and emerging market countries, the value of labor in the US fell dramatically. Today, we are at a point where labor share of income has fallen to an all-time low of 57%. That means a growing fraction of the gains have been going to capital, and those who have it.

This has resulted in the loss of millions of US jobs. Since 1979, manufacturing employment has dropped by approximately seven million jobs. Studies show that technology accounts for around half of these losses. But Niall makes a very succinct point about these findings:

“The distinction [between globalization and technology] is arbitrary. What distinguishes the technological revolution is precisely that things like iPhones could be designed in California but made in China. The paradox of the Liberal International Order is that it made a lot of technology affordable, while at the same time destroying manufacturing jobs.”

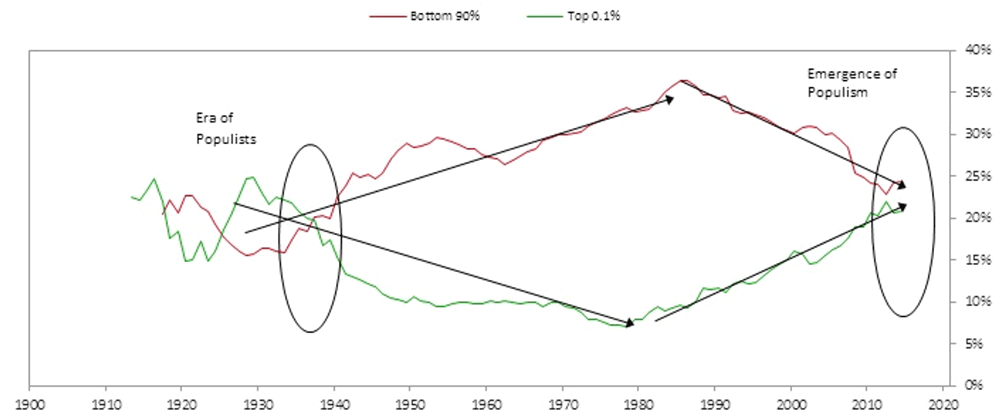

The hardship experienced by millions of Americans has happened at a time when the wealthy have done increasingly well. Today, we have a situation where the top 0.1% of the population has roughly the same share of the US national wealth as the bottom 90%. Cue: the re-emergence of populism.

Source: Ray Dalio, Bridgewater Associates

It’s not a coincidence that populism emerged as a political force in both the 1920s–1930s, and again today. In each case, people at the bottom could tell the economy wasn’t working in their favor. The best tool they had to do something about it was the vote, so they elected FDR then, and Trump now. Two very different presidents, but both responsive to the most intensely angered voters of their eras.

You only have to observe how the word “globalist” has become a slur to see that people have turned against liberal internationalism and those who support it. Globalization has been terrible for millions of middle- and working-class Americans, and they are very unlikely to vote for politicians who support it. By lowering the living standards for millions of Americans, the Liberal International Order has become the architect of their own downfall.

Niall has also highlighted events taking place on the other side of the Atlantic as another sign that the Liberal International Order is indeed finished.

The European Union has a crisis of confidence

Niall says the EU’s mishandling of the financial and migrant crises have resulted in a total loss of confidence in the institution:

“The European Union is a perfect illustration of why the Liberal International Order is over. The EU wholly mismanaged the financial crisis, massively amplifying the effects on member states. But it will turn out to have committed suicide because its leaders got the immigration issue wrong. The Europeans forgot that borders are really the first defining characteristic of a state. As they became borderless, they made themselves open to a catastrophe, which was the uncontrolled influx of more than a million people. The most basic roles that we expect a state to perform, from economic management to the defense of borders, were flunked completely by the EU over the past 10 years.”

The EU’s incompetence in both situations has ignited a wave of populism across the continent:

-

Austria elected a 31-year-old, anti-immigration candidate as Chancellor.

-

Italy’s populist Five-Star movement are leading in the polls for the general election, which takes place March 4.

-

The Visegrad group, which consists of the governments of Poland, Hungary, Czech Republic, and Slovakia, have strongly opposed the resettlement of refugees and are battling with the EU over the issue.

-

Angela Merkel did win the German elections, but four months later, she hasn’t been able to form a government because of the strong showing by the populist Alternative for Germany party.

The empirical evidence supports Niall’s thesis, and so does the academic research. A 2017 study from the Brookings Institution found that there is a high correlation between jobs losses which occurred as a result of the financial crisis, and increased support for anti-establishment political parties in Europe.

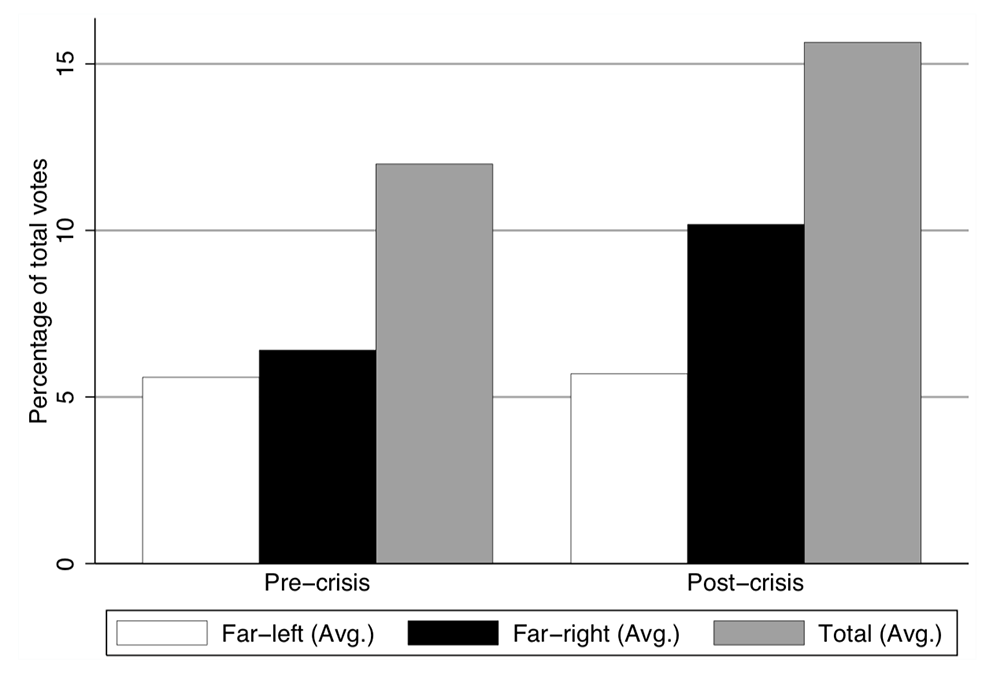

This populist backlash shouldn’t come as a surprise to us. During a recent discussion, Niall pointed out that: “If one looks at all the elections back to 1870, financial crises lead to backlashes against globalization that erode to the political center.” Here’s a chart which shows this trend:

Source: Funke, Schularick, Trebesch (2015)

This is why I love talking with Niall. He makes sense of current trends by providing a historical perspective. Getting Niall’s insight not only allows you to understand what is currently happening, but how things are likely to unfold in the future.

While the EU’s handling of the financial crisis hasn’t been good for business, I believe their mismanagement of the migrant crisis will prove to be their real downfall. According to Frontex, the EU border surveillance agency, over the course of 2015 and 2016, more than 2.3 million illegal crossings into Europe were detected. This influx of migrants hasn’t gone unnoticed.

A recent survey by Paris-based think-tank, Fondapol, found that nearly two-thirds of EU citizens surveyed believe immigration has a negative impact on their countries. As the below chart shows, a similar percentage of respondents said they are “very worried/worried” about Islam.

Source: Fondapol, Financial Times

Despite the concerns of people all across Europe about immigration, EU officials continue to push refugee resettlement on member states. The EU’s actions in the face of these concerns proves that there is a complete disconnect between those in Brussels and ordinary Europeans.

I can’t see how this doesn’t cause a further increase in support for populism around Europe, and ultimately lead to the demise of the EU—which would certainly prove that the Liberal International Order is over. To be clear, I don’t think the collapse of the EU is imminent, but it is certainty on a downward trajectory.

We saw this movie before, will it have the same ending?

As I mentioned, Niall has a special ability to dissect historical trends and extrapolate out what they can tell us about the future. He did this recently with the Liberal International Order:

“The big lesson of history is that we have run the experiment of hyper-globalization before. In the late 19th century, many of the forces we are seeing [today] were at work: International migration reached levels we have begun to see again, the percentage of the US population that was foreign born reached 14%, and free trade and international capital flows reached new heights. At the time, the 1% were tremendously happy. Unfortunately, they underestimated the backlash that happens when globalization runs too far. The populist backlash [in the late 19th century] was just the beginning of a succession of crises that culminated in 1914 with WWI. War can be global too, and we will know the Liberal International Order has failed when it does what the last one did, and that is to produce a major conflict.”