Why the World Needs the US Economy to Struggle

-

John Mauldin

John Mauldin

- |

- January 4, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinOn the Verge of a Disaster… or a Miracle

Boom & Gloom

Emerging Markets & the Next Global Financial Crisis

Why the World Needs the US Economy to Struggle

Head-Banging Central Banks

Cincinnati, the Cayman Islands, Zurich, and Florida

The headlines this morning talk about the US dollar hitting an 11-year high. I have been saying for years that the dollar is going to go higher than anyone can imagine. This trade is just in the early innings. And the repercussions will be dramatic, not only for emerging markets that have financed projects in dollars, but also for commodities and energy, gold, and a variety of other investments. The world is at the doorstep of a new era of volatility and currency wars.

In this week’s letter, my associate Worth Wray explores what a rising dollar means for emerging markets and what central banks are likely to do in response. Can they smooth the ride, or will it be the world’s scariest roller coaster? This letter will print long because of the number of fabulous charts Worth provides. I might make a brief comment or two at the end. Here’s Worth.

On the Verge of a Disaster… or a Miracle

By Worth Wray

Twenty years after the first divergence-induced currency crisis of the 1990s, commodity prices are tumbling, the US dollar is rallying, and externally fragile emerging markets are reliving the horrors of their not-so-distant past. Except, this time, major economies like the United States, the United Kingdom, the Eurozone, Japan, and the People’s Republic of China may not be able to side-step the ensuing contagion.

With 2014 now behind us, I want to focus this week's letter on what may prove to be the most important global macro pressure points in the coming year(s):

- The growing divergence among the world’s most important central banks

- The ongoing collapse in oil and other commodity prices as a function of excess supply and/or weakening global demand

- The rise of the US dollar, driven by divergence and risk aversion… and the squeeze it’s putting on the multi-trillion-dollar carry trade into emerging markets

- The vicious slide in emerging-market currencies

- The rising risk of 1990s-style contagion and financial shocks

- And what, if anything, can avert the next global financial crisis

But first, let me tell you a story.

As some of you already know, I was born and raised in Baton Rouge, Louisiana – an old Southern city built on a bluff above the Mississippi River. It’s about an hour northwest of New Orleans – you can see it circled on the map below.

Given its inland position, Baton Rouge is fairly insulated from the fiercest impact of coastal storms; but hurricane season still tends to be the most stressful time of year. Our oak-covered neighborhoods and low-lying swamplands are vulnerable to the high winds and flood rains that can accompany a direct hit – not to mention the violent tornadoes that occasionally occur in the unpredictable northeastern quadrant of the tropical cyclone zone.

These storms don’t hit us often, but locals recall a handful of hurricanes that dealt heavy blows to the area over the years. And it goes without saying that the damage from any storm gets dramatically worse the closer you get to the Gulf of Mexico. Entire towns along the Gulf Coast have been swallowed up and swept away over the years by catastrophic storms like Camille (1969), Andrew (1994), and more recently Katrina (2005).

Twelve years ago, my father and I found ourselves in the path of such a storm.

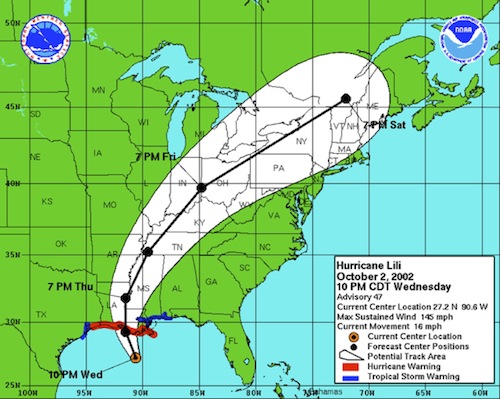

According to the National Hurricane Center, Hurricane Lili was “supposed” to make landfall as a relatively weak storm. Just another named hurricane for the record books that would soon fade from our collective memory… or so we thought.

At 10:00 PM on Tuesday, October 1, 2002, Lili was a Category 2 hurricane with maximum sustained winds of 105 mph. Routine hurricane season stuff.

I went to sleep that night expecting a little rain and few uneventful days home from school; but when I woke up on Wednesday, October 2, I was shocked to see Lili develop an incredibly well-articulated eye wall and grow more powerful by the hour – from 110 mph at 7:00 AM that morning to 135 mph at 1:00 PM and finally to 145 mph at 10 PM that night.

I remember the nervous look on my dad’s face that night as the two of us boarded up our doors and windows. A little earlier that evening, one of his local government contacts shared that, behind closed doors, state and local officials were expecting “mass casualties” from Morgan City (on the coast) to Baton Rouge… but it was already too late to order an evacuation so far inland. Given the mild forecasts, few were prepared for a major hurricane; and at that point in the day, making a public announcement would do little more than spark a panic. The best we could do was hunker down and pray.

This was the last advisory I saw before my head hit the pillow that night: Lili had strengthened to a strong Category 4 hurricane with maximum sustained winds around 145 mph, reported gusts above 210 mph, and the very real possibility of making landfall as a merciless Category 5. If you look at the Saffir Simpson hurricane scale, there’s a reason the first word you see next to Category 4 and 5 storms is catastrophic. These storms are real killers.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Expecting to wake up early the next morning to sounds of thunder, pounding rain, and the eerie whistle of gale-force winds – or worse, I went to sleep Wednesday night with this image swirling through my mind:

But when I woke, I was shocked once more to learn that Lili – for reasons no one had anticipated – had all but died in the night and made landfall that morning as a small Category 1 hurricane with maximum sustained winds of only 90 miles per hour. In less than twelve hours, it had sharply decelerated from what could easily have been one of the most catastrophic storms on record to an inconvenience for most inland communities. Sure, it inflicted some damage along the coast – tearing up marshlands, knocking down power lines, blowing over trees, and flooding homes – but a Category 4 or 5 storm would have swallowed those areas whole.

As far as I know, there was no precedent in the Gulf of Mexico – or anywhere in the world – for Lili’s sudden death. It baffled even the most experienced meteorologists and left us all scratching our heads. Some people talked of miracles; others insisted there had to be a logical explanation. I imagine there’s some truth to both ideas.

While the press coverage surrounding Lili’s remarkable weakening has largely faded into obscurity, I was able to find one surviving article from USA Today that captures the confusion in the storm’s aftermath: “Scientists Don’t Know Yet Why Lili Suddenly Collapsed.”

Hurricane Lili showed forecasters there is still a lot they don't know about hurricane intensity. Lili weakened in the hours before landfall Thursday as rapidly as it had strengthened into a ferocious storm the day before. Forecasters with the National Hurricane Center in Miami had hinted as early as Monday that Lili could rev up into a dangerous hurricane over the extraordinarily warm Gulf of Mexico, though they were surprised to see it grow so strong so quickly. But Lili's quick demise … had them admitting they didn't know what had happened…. National Hurricane Center Director Max Mayfield agrees. At a loss to explain Lili's fluctuations, he says, “A lot of Ph.D.s will be written about this.”

We still don’t have a definitive answer, but three theories emerged in the immediate aftermath:

1) Dry air was pulled into the storm and ate away at its moisture-sucking core;

2) Winds aloft increased across the storm, creating wind shear and tipping the delicate balance that keeps intense storms going;

3) Water cooler than the 80° necessary to sustain a hurricane sapped Lili's strength when it moved over the same part of the north-central Gulf of Mexico that had been churned up by a smaller hurricane, Isadore, a week earlier.

Regardless of why it happened, I learned something that day that will stay with me for the rest of my life: Even when a disastrous course of events is set in motion, disaster does not always strike. Surprises happen. Even miracles. Forecasts are often wrong – but it always pays to prepare.

Let me explain…

Just before Halloween, I wrote a letter (“A Scary Story for Emerging Markets”) explaining that the widening gap in economic activity among the United States, Japan, and the Eurozone was starting to demand a dangerous divergence in monetary policy.

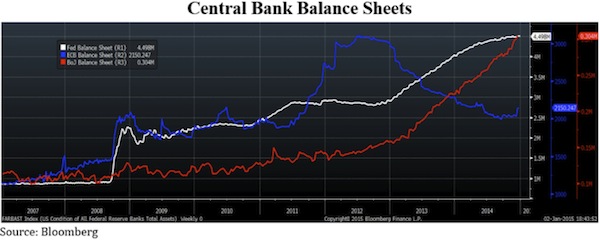

Within a matter of days, the FOMC announced the end of its QE3 program... and then the Bank of Japan shocked the world, announcing a massive expansion in its own asset purchases timed to coincide with the government pension fund’s announcement that it was getting out of JGBs and into global equities.

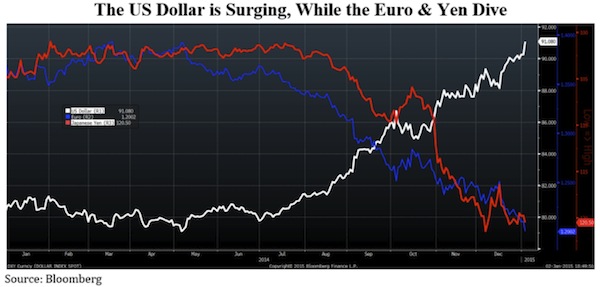

Just as I had feared, the US dollar and Japanese yen were breaking out in opposite directions on real policy action, as Mario Draghi meanwhile continued to talk the euro down with the threat of future action. This may seem like a trivial shift in global FX markets, but it may have been the most important development we have seen since the global crisis peaked in 2008.

Since then, global economics has been a story of boom, gloom, and doom, as Marc Faber likes to say. We’re seeing a boom in US economic activity (or as much of a boom as you can expect with a massive debt overhang); a gloomy slowdown and slide toward deflation across Europe and China, along with the still-likely failure of Abenomics in Japan and renewed signs of FX contagion in emerging markets; and doom in commodities markets, particularly oil.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I’ve shared this next chart before, but it’s worth an update. Those of us who watch the US dollar were not surprised by the collapse in oil prices, because the dollar’s surge was already telling us something about global demand.

What did surprise a lot of economists (myself included) was the breakdown within OPEC, particularly Saudi Arabia’s willingness to accept whatever price the market offered in order to protect its market share. Conspiracy theories aside as to whether OPEC’s move constitutes an anti-American trade war against US shale producers or a pro-American squeeze on Russia, Iran, and Venezuela, it’s already putting a serious squeeze on Texas oil men, Russian “oiligarchs,” and oil-exporting emerging markets.

We’ll revisit the oil shock in a bit, but for now let’s get back to the US dollar.

As my friend Raoul Pal has argued in the public media and explained in depth in a recent Real Vision TV presentation, “The Law of Unintended Consequences,” the dollar has just broken through the trendline of the biggest wedge pattern in the history of fiat money.

For readers who are unfamiliar with technical analysis, breaking out from a wedge pattern often signals a complete reversal in the trend encompassed within the wedge. As you can see in the chart above, the US Dollar Index has been stuck in a falling wedge pattern for nearly 30 years, with all of its fluctuations contained between a sharply falling upward resistance line and a much flatter lower resistance line.

Any breakout beyond the upward resistance is an incredibly bullish sign for the US dollar and an incredibly bearish sign for carry trades around the world that have been funded in dollars. As you can clearly see, the US Dollar Index, sitting at 91 today, has clearly broken above that trendline. This is a VERY big deal and a clear sign that we may be on the verge of the next phase of the global financial crisis, where financial repression finally backfires and forces all the QE-induced easy money sloshing around the world to come rushing back into safe havens.

The US dollar gained against all 31 of its major counterparts in 2014 (for the first time in 25 years), but whether its upward surge continues depends on three factors: (1) continued policy divergence, which largely depends on continued economic divergence among key developed economies, (2) short covering by investors making levered bets in foreign markets with US dollar funding, and (3) global risk aversion and/or outright capital flight from emerging markets.

Any one of these forces, if it becomes strong enough, is capable of driving the other two. For example, an early Fed rate hike, a serious easing announcement from the ECB, or perhaps even a surprise devaluation by the People’s Bank of China would be enough to send the US Dollar Index soaring into the mid-90s, which in turn would cause a rush of short covering, which would likely trigger a series of violent currency crashes across the emerging world. Or, it could be the other way around: a major balance of payments crisis in the emerging world – as we’ve started to see in Russia – could easily spread to other emerging markets; and if enough of those dominoes start to fall, the resulting backwash into US dollars would likely trigger short covering, which would only intensify the broad outflow pressures on emerging markets.

As Lacy Hunt of Hoisington Investment Management explains, even leaving aside contagion effects and dollar short covering, the divergence in debt loads among the United States, Japan, and the Eurozone is enough to explain a lot of the economic divergence we are seeing; and he suggests that the trend should continue for the forseeable future:

US growth is outpacing that of Europe and Japan primarily because those economies carry much higher debt-to-GDP ratios. Based on the latest available data, aggregate debt in the US stands at 334%, compared with 460% in the 17 economies in the euro-currency zone, and 655% in Japan. Economic research has suggested that the more advanced the debt level, the worse the economic performance, and this theory is in fact validated by real-world data [not to mention recent experience].

From that perspective, there’s no reason we should expect a major departure from easy monetary policy in Japan or from the expectation (if not the realization) of easy-money policy to come in Europe. Inflation expectations are far too low in both regions, and the erosion of economic activity is far too worrying.

That leaves the United States as the economy to watch if the nasty combination of short covering and emerging-market contagion does not trigger a massive rip in the dollar in the next several months. (All bets are off under that scenario, which is certainly possible.) That said, if US economic activity continues to accelerate or just muddle through at present levels, the odds are very high that the Federal Reserve will hike its target interest rate in the next three to six months. I know it sounds extreme, and a lot of people will point to the myriad delays in hiking the rate under Ben Bernanke’s leadership, but the Yellen Fed now finds itself in a bit of a box.

Despite the fact that US trend economic growth is running far below its long-term average, we’ve just seen Q3 2014 real GDP growth revised to 5%, the fastest quarterly rate in 10 years, which puts the trailing 12-month average at roughly 2.5%. The current account deficit has collapsed to a 16-year low of 2.2%. And, as of November, the US headline unemployment rate is sitting right on its 60+ year average of 5.8%.

What looks weak here relative to history? What warrants accommodation?

Of course, the Fed’s decision also depends largely on inflation and inflation expectations, which may not take as hard a beating as some people expect, even in a scenario of $40 to $60 oil. Of course, the headline inflation rate could flirt with negative territory, but core inflation is likely to remain largely intact and near its 2% target. It’s creating a difficult call for those in Washington.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I don't know if the Fed WILL hike interest rates this summer, but I do believe Chairwoman Yellen and Vice-Chairman Fischer INTEND to do so. And I think they are communicating their intention clearly for central banks around the world to hear. In his speech on the Fed and the global economy this past October, the vice-chairman (who, bear in mind, ran the IMF during the Asian Financial Crisis in 1997, the Russian default in 1998, and the related collapse of Long Term Capital Management) essentially said that clear communication is the FOMC’s only responsibility to the rest of the world:

My teacher Charles Kindleberger argued that stability of the international financial system could be best supported by the leadership of a financial hegemon or a global central bank. But I should be clear that the US Federal Reserve System is not that bank. Our mandate, like that of virtually all central banks, focuses on domestic objectives. As I have described, to meet those domestic objectives, we must recognize the effect of our actions abroad, and, by meeting those objectives, we best minimize the negative spillovers we have to the global economy. And because the dollar features so prominently in international transactions, we must be mindful that our markets extend beyond our borders and take precautions, as we have done before, to provide liquidity when necessary…. In the United States, we are working to ensure that our financial institutions and other market participants are prepared for the normalization of monetary policy and the return to a world of higher interest rates. It is equally important that individuals, businesses, and institutions around the world do the same. For our part, the Federal Reserve will promote a smooth transition by communicating our assessment of the economy and our policy intentions as clearly as possible. [emphasis mine]

Keep in mind that the slide in oil prices did not deter the FOMC from replacing its “considerable time” phrase in December with a slightly more hawkish tone of “patience,” which seems to be a clear cue to the central banking community, even if Wall Street interpreted it as being more dovish than it really was. Some people hear what they want to hear, but I imagine that Raghuram Rajan and his peers at the other emerging-market central banks heard something very different than did the Wall Street strategists and retail investors who bought equities that day.

While my friends remind me that “patience” can mean a very long time, I’m unsettled by the fact that the FOMC’s language transition is very similar to the one it employed ahead of its 2004 rate hike.

Of course, intents and purposes can change. But after a year and a half of the Fed’s telegraphing its steady march toward the exits, US economic data remains remarkably robust, even if the strong dollar and the US shale slump eventually weigh on growth and employment.

In addition to the contagion we are already seeing in the wake of oil’s global nosedive, US dollar strength leaves me seriously cautious about the reversal it could trigger in emerging markets.

Emerging Markets & the Next Global Financial Crisis

Hyman Minsky taught that instability often emerges from the excess leverage and misallocation that naturally grow during long periods of perceived stability; yet central banks have now manufactured one of the longest-running periods of global market complacency in the modern era.

Against the backdrop of extremely accommodative central bank policy in the United States, the United Kingdom, and Japan, and the ECB’s “whatever it takes” commitment to keep short-term interest rates low across the Eurozone, global debt-to-GDP has continued its upward explosion in the years since 2008… even as slowing growth and persistent disinflation (both logical side-effects of rising debt) detract from the future ability of major economies to service those debts. It should come as no surprise that the consequences stretch far beyond our borders.

Despite the urgent need to get debt growth under control, the short-sighted combination of financial repression and excess liquidity has fueled overinvestment and capital misallocation in developed-world financial assets…

… but the real explosion in debt and financial assets has played out across the emerging markets, where the unwarranted flow of easy money has fueled a borrowing bonanza on top of a massive USD-funded carry trade.

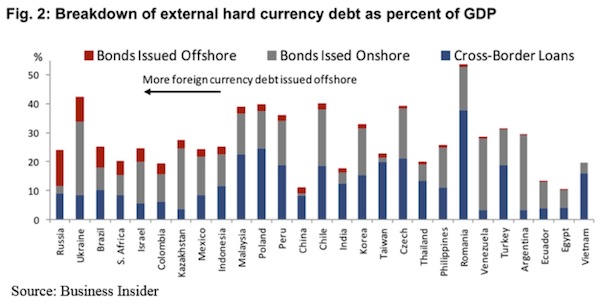

In a recent presentation at the Brookings Institution, BIS Head of Research and Princeton University Professor Hyun Song Shin shared his research revealing that dollar-denominated credit to non-bank offshore borrowers is now more than $9 TRILLION.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

While some of that new funding has come through equity issuance, the vast majority has come from bank loans and corporate bond issuance…

Source: Business Insider

… with the growth in offshore credit to emerging markets showing a striking correlation to Fed policy since 2009:

If you step back and take a look at how dependent many of the emerging markets have become on offshore bond issuance and/or cross-border loans, you’ll see that a number of countries are seriously addicted to foreign capital in one form or another.

If and when investor risk appetites change, this shaky funding structure will leave a number of emerging market borrowers in the firing line. Buttiglione, Lane, Reichlin, and Reinhart expand on that idea in their latest Geneva Report on the World Economy:

The super-low interest rate environment in advanced economies has encouraged a new wave of debt issuance by firms in emerging economies. In contrast to the mid-2000s phase, this new wave of global liquidity has been primarily intermediated through the bond market rather than the international banking system.

The result was the strong increase in the ratio of total debt (ex-financials) to GDP for emerging economies, by a staggering 36% since 2008. Higher leverage, although helping to shield these economies from the chilling wind blowing from advanced economies, is an increasing concern in terms of the future risk profile given the ongoing steep slowdown of nominal growth, which reduces the ‘debt capacity’ of emerging economies exactly when they would need to expand it.

Moreover, a substantial proportion takes the form of offshore issuance through the foreign affiliates of domestic corporations. These offshore liabilities pose an indirect risk to domestic financial stability in emerging markets, since a disruption in offshore funding would compromise the consolidated financial health of the issuing corporates, damaging economic performance and generating a reduction in corporate deposits in the domestic banking system. In terms of funding risks, the surge in issuance leaves these firms vulnerable to shifts in appetite among global bond investors.

That leaves us with a BIG question: how great a portion of the recent inflows can depart quickly? The short answer is, no one knows. The longer answer is, it depends on the shorter-term carry trade into those markets, which might come unwound at any moment. While it’s very difficult to know for certain, reasonable estimates of the size of that trade range from $2 trillion to $5 trillion – which makes it the largest carry trade in modern history.

Keep in mind that we have now seen three major carry trades in the last twenty years. The first fueled an obviously overextended credit boom in Southeast Asia that culminated in the Asian Financial Crisis of 1997 and served as a major catalyst for Russia’s default and the collapse of Long Term Capital Management. That carry trade has been estimated at several hundred million dollars – nowhere near the current flow. The second was largely funded in yen in the days leading up to 2008 and has been estimated at roughly $1 trillion. Its forceful reversal was one of the major causes for the collapse in emerging-market credit conditions and the sharp rally in the Japanese yen during the 2008 crisis. We simply have no historical precedent to suggest what will happen if and when a $2 trillion to $5 trillion carry trade unwinds, but I can assure you it will be ugly.

As I wrote in October, we need to seriously prepare for a bigger wave of EM crises that could be induced by (1) a reversal in capital flows triggered by central bank policy divergence, a strengthening US dollar, and the resulting unwind in the USD carry trade, (2) a dramatic fall in commodity prices as global growth decelerates, or (3) both.

Trouble is, the story has gotten a LOT more complicated than it seemed when I first started thinking about this idea in the wake of Fed Chairman Bernanke’s initial taper comments… or even when I outlined my thesis in October.

The first signs of EM crisis – now affectionately and erroneously known as the “taper tantrum” – saw local markets and currencies slip in proportion to their reliance on foreign funding. Countries with both current account and fiscal deficits, relatively high inflation rates, and slipping growth prospects immediately found themselves in the firing line.

Global markets were quick to lump countries such as India, Turkey, South Africa, Indonesia, Argentina, Brazil, and Russia into a common category and threatened the quick withdrawal of funding in the event that the Fed moved forward with its plans to tighten – first to taper its ongoing QE3 asset purchases and then presumably to move on to rate increases.

The immediate response was painful. Each of these countries’ currencies suffered sharp depreciations, with the Indian rupee, Brazilian real, and Indonesian rupiah taking the hardest hits.

While the Indian rupee initially fell the hardest, incoming RBI governor Raghuram Rajan was quick to take note of the Fed’s signal and, as a first order of business, immediately began hiking interest rates in September 2013. But rather than admit that he was acting to shore up the rupee – and risk eroding the FX market’s confidence – Rajan argued that, like Fed Chairman Paul Volcker in the 1980s, he was putting India on a credible path in the fight against inflation. And he stuck to his guns in the following months, as fears about capital flight quieted and the USD carry trade continued to grow.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

At that moment, Rajan was an outlier among EM central bankers – most of whom did nothing as the imminent risk of flow reversal seemed to recede. When Bernanke’s successor, Janet Yellen, established a credible trend of tapering the Fed’s asset purchases by $10 billion at every meeting, fear and panic returned, but only for a few months. In stark contrast to India, the Reserve Bank of Turkey was forced to hike rates – acknowledging their desperate need to shore up the lira – and then to hike again as market confidence eroded.

But those events were like the faint hints of an earthquake far offshore. And global markets were a little TOO calm. From February to May 2014, the fear receded again, and capital flows returned even to the most fundamentally weak emerging markets… including Turkey.

The latest “tantrum” has been more about falling commodity prices, largely due to the slowdown in China’s massive investment boom, along with weakness in Japan, Europe, and much of the emerging world. As a result, the demand for commodities – particularly oil (where a glut in supply from US shale production is playing a role) – has started collapsing… and the once steadfast alliance among OPEC nations has been shattered.

As prices fall, the immediate balance of payment risks in emerging markets are falling on those countries that rely on commodity export revenues. As foreign demand falls and prices with it, countries that were large net exporters six months ago are becoming net importers… revealing increasingly dangerous and fragile twin deficits in countries like Russia and Brazil… while countries like India and Turkey are actually seeing their current account deficits improve, given the lower costs of commodity imports. Of course, modest improvements in economic fundamentals only count for so much when contagion strikes.

For now, it’s worth noting here that even the Turkish lira and the Indian rupee are getting pulled into the contagion from Russia’s financial crisis, despite what lower oil and other commodity import prices mean for their current accounts and inflation rates. It’s an important lesson.

It remains to be seen whether the ruble’s collapse will continue as Russia’s financial crisis deepens or if it will be halted as China steps in and prevents the sudden breakout of the USD for the time being. But we need to look at Russia's ongoing experience in handling the first divergence-induced crisis. It’s the first major domino to fall, of the many that may topple in the coming months, quarters, years… and the first of the fragile currencies to depreciate in a meaningful way. I doubt it will be the last.

If the Federal Reserve does not back off from its tightening path, or if it simply pauses where it is for several quarters, allowing contagion and risk aversion to take over, that could be enough to set off a major rally in the USD and the subsequent unwind of the USD-funded carry trade. Regardless of the actual number (which is almost impossible to pinpoint accurately), the amount of capital that could be quickly withdrawn from EM markets could be massive. And more importantly, funding would stop, forcing local firms to borrow within their own potentially crippled financial systems rather than through international bond markets.

While a carry trade reversal would almost certainly exacerbate the slowdowns already in progress in several major emerging countries, it doesn’t necessarily mean total currency collapse. Then again, a number of these economies are inviting just that. And when one or two currencies start to go, they could easily push the USD even higher, putting pressure on a whole additional set of countries. Think 1994 to 1998 on steroids… with all the risks such pressures could pose to our highly levered, highly interconnected global financial system.

Why the World Needs the US Economy to Struggle

Looking back on the 1990s, most economic historians, central bankers, and investment strategists continue to think of Mexico's Tequila Crisis, the Asian Financial Crisis, and the Russian default crisis as if they were separate incidents. I think that’s an enormous error that derives from a misunderstanding of the true causes of contagion.

The Tequila Crisis in 1994 was the first divergence-induced accident of the period, and it could easily have bubbled over into full-blown contagion had it not been for $40 billion in emergency loans and guarantees from the US government. Instead of merely seeing their currencies slide in the oft-forgotten “Tequila effect,” Brazil, Argentina, Chile, et al. could easily have been thrown into another decade of full-blown disaster... and who knows how far the sickness could have spread.

While it might be somewhat misleading to speculate about what might have happened, we do know two things: (1) the capital that fled Mexico in 1994 and 1995 did not return quickly, and (2) those Latin American events marked a turning point for the US dollar.

Although US government intervention in Mexico restored a sense of calm to FX markets, it also sent US dollar investments running to Asia, where the USD's rise was a major contributing factor to the eventual collapse of the Southeast Asian growth miracle. And investment managers' collective memories of the 1982 and 1994 Mexican peso crises likely contributed to the panicked mood as they dumped the Thai bhat, Malaysian ringgit, Indonesian rupiah, Philippine peso, and South Korean won in 1997. Furthermore, the Asian crisis (which drove the USD higher and destroyed commodity demand across SE Asia), along with a global glut in oil supply, was a major catalyst for Russia's disastrous default in 1998.

All of these events were connected by initial surges in private-sector credit – largely funded in US dollars – and all of the countries involved fell as a consequence of capital flight, either as a function of policy divergence (which eventually pushed the USD higher), risk aversion (which immediately pushed the USD higher), or both.

While the US can probably decouple from global growth conditions long enough to justify a Fed rate hike in the coming months, our global financial system is far too levered, far too interconnected, and far too gravely mismanaged for the US to continue booming as commodity prices collapse and the emerging-market borrowing bonanza comes to an abrupt and violent end. The deflationary storm can blow back at us far more quickly than the FOMC believes.

If the last thirty years have taught us anything about cross-border capital flows and financial contagion, it’s that herding behavior – especially among fund managers, who have piled in to emerging-market corporate bonds in recent years – can amplify distress, even in small economies with limited trade and financial linkages, into legitimate threats to the world’s strongest markets.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I don’t know if the divergence we are seeing among central banks will continue. I don’t know if the US dollar will keep breaking out of its 30-year downtrend. I don’t know if commodity prices will continue to collapse or if a rapid unwind in the US dollar-funded carry trade will spark emerging-market contagion capable of further destabilizing the global financial system. But these forces are playing out just as I’ve feared over the last eighteen months, and they are creating an economic storm capable of shaking the world in far more profound ways than a Category 5 hurricane crashing into the Louisiana coastline.

Just as Hurricane Lili may have died when it hit a patch of cold water just before making landfall, the only thing that can stop a major breakout in the US dollar and an ensuing global financial crisis may be a cold patch of economic data such as collapsing US inflation expectations and, most likely, another round of job losses in the very near term. I just don’t see either happening quickly enough to stop the dollar in its tracks. Everything – from the Fed’s policy stance to the ECB’s resolve – will change once the big unwind begins, but that’s a story for another letter.

It may be time to pray for a miracle but prepare for a disaster.

John here. Worth actually wrote a much longer piece that we had to edit for the letter, but the rest will show up in the new book that we are beavering away on. It will be about the major changes that are in store for the global economy over the next five years. Plus some discussion about what central banks will try to do to smooth out the disruptions. We are in for some very volatile markets. Anything and everything will be on the table.

The following quote is from Stan Fischer, vice-chairman of the Fed and one of the true global thought leaders on the role of central banks in crises. When he speaks, everyone listens. He made this comment during a panel discussion about the actions central banks might take in the next crisis:

Finally, what to do about the lender of last resort. Rajan emphasized liquidity, and so did the discussants. That is what central banks can provide in a crisis, but you have to bear in mind the rule that the lender of last resort should lend to the market and not to specific institutions. This whole development is paradoxically reemphasizing the role of the central bank in the management of the system. If he is right, Raghu said the key problem is going to be liquidity. That is what central banks are about.

I have reflected a long time on the Long Term Capital Management crisis. The thing that struck me most was [that] the story of LTCM could have appeared in Clappin’s book on 19th-century crises. It is a very modern crisis, but the way it was resolved was almost identical to the way that crises always used to be resolved. The central bank was brought in and banged a few heads together. There was an argument about whether they should have done it, but in the end, that was how it was resolved.

Central banks as head bangers. Who knew? Actually, Volcker did the same thing during the crisis caused by the Hunts cornering the silver market. Nearly every major investment bank and a few major commercial banks were technically insolvent. Volcker sat in the room and listened to the back and forth and then told everyone exactly how it would be solved. No one in the room was happy, but the country dodged a major crisis.

The powers that central bankers have this time around are even headier than they were in the ’80s or ’90s. But will they lose their ability to assuage the markets through injections of liquidity when the fundamental problem is not liquidity but too much debt?

We are also going to do something in this book that I have not done in a very long time. We are going to lay out very specifically how we think you can keep your investment portfolio working for you while avoiding much (though not all) of the escalating risk. The next five years are going to require that you rethink your strategy. Worth and I have been working on this for a couple of years and are now just about ready to write about it. Stay tuned.

Cincinnati, the Cayman Islands, Zurich, and Florida

I see Cincinnati, Grand Cayman, Zurich, and Florida on my schedule. I will be in Cincinnati on the 13th for the CFA forecasting dinner. Then in February it’s on to the Caymans. It has been awhile since I was in the Cayman Islands, and this time I’ll take a short hop over to Little Cayman to visit my friend Raoul Pal for a few days. A brilliant macroeconomist and trader, Raoul has now based himself in Little Cayman, although he frequently flies to visit clients. He is also a partner with Grant Williams in Real Vision Television, a fascinating new take on internet investment TV.

And speaking of Raoul, if you want to learn more about the US dollar carry trade and what its rapid unwind could mean for the global economy, my good friend and legendary global macro investor Mr. Pal explains it all in a recent video presentation on Real Vision TV called “The Law of Unintended Consequences.” I asked him to make that video public so that Mauldin Economics readers can get an exclusive behind-the-curtain preview of Real Vision and hear from a man who comes up with macro trades and ideas that are implemented by some of the world’s largest hedge funds. We have been exchanging notes for years, and I can tell you without a doubt that this guy is the real deal. I don’t say this very often, but you REALLY don’t want to miss this video.

And if you like the video, we’ve negotiated a special discount rate that will let you subscribe to Real Vision TV for $295/year instead of the regular $400. Consider it a nice dinner on us and a chance to tap into mind-blowing conversations with some of the brightest minds in finance… whenever you’re in the mood.

I want to say congratulations to my good friend Art Cashin, who rang the opening bell to commemorate his 50th year as an NYSE member (and over 60 years working on the floor). It is rare for anyone to have such an anniversary commemorated by an opening bell, but Art is that rare man. He is easily the most respected man on the floor and the true sheriff of the exchange, settling arguments and disputes over trades with his word and with the actual investors’ best interests in mind. As the world moves to electronic trading, we are going to miss the days when men like Art could walk the floor of the Exchange and settle a heated debate or a true pricing quandary with a simple on-the-spot call that all would acknowledge as fair, rather than taking days and teams of lawyers and judges. I have seen him do it on a few occasions, and it is a truly amazing experience. Will have to stop by the Friends of Fermentation to buy a few rounds of Dewars and listen to a few stories.

I will resume my regular weekly writing schedule next week with my own forecasting issue; but this time, instead of predicting (and being wrong) about where the S&P will end up this year, I am going to do a five-year forecast about events I feel confident about. Of course, that confidence is relative, since I have zero confidence in my ability to predict where the S&P will be in 12 months.

It is time to hit the send button, but first a few of my resolutions. Besides losing the 15-20 pounds I still carry from last year’s failed resolution, I intend to read more books this year and less news. And I’ll try to travel less. I have really enjoyed the reduced travel of the last few months and feel much better physically because of it. This morning I actually did 80 pushups, which was a little surprising to me, but I guess the training is paying off.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Let me wish you the very best and most prosperous of New Years from the whole team here at Mauldin Economics. We will do our best to help you prosper, this year and every year.

Your starting to see how the pieces of the future puzzle fit analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.