Thoughts from the Frontline: A Most Dangerous Era

- Patrick Cox

- |

- February 10, 2014

- |

- Comments

"In the economic sphere an act, a habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen. The other effects emerge only subsequently; they are not seen; we are fortunate if we foresee them.

"There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must be foreseen.

"Yet this difference is tremendous; for it almost always happens that when the immediate consequence is favorable, the later consequences are disastrous, and vice versa. Whence it follows that the bad economist pursues a small present good that will be followed by a great evil to come, while the good economist pursues a great good to come, at the risk of a small present evil."

– From an essay by Frédéric Bastiat in 1850, "That Which Is Seen and That Which Is Unseen"

The devil is in the details, we are told, and the details are often buried in an appendix or footnote. This week we were confronted with a rather troubling appendix in the Congressional Budget Office (CBO) analysis of the Affordable Care Act, which suggests that the act will have a rather profound impact on employment patterns. You could tell a person's political leaning by how they responded. Republicans jumped all over this. The conservative Washington Times, for instance, featured this headline: "Obamacare will push 2 million workers out of labor market: CBO." Which is not what the analysis says at all. Liberals immediately downplayed the import by suggesting that all it really said was that people will have more choice about how they work, giving them more free time to play with their kids and pets and pursue other activities. Who could be against spending more time with your children?

Paul Krugman noted that the data means that potential GDP will be reduced by as much as 0.5% per year, which he dismissed as a small number. And he states that people voluntarily reducing their work hours does not have the same economic effect as people being laid off or fired. Which is true, but not the point nor the import of that pesky little appendix.

Where Will the Jobs Come From?

To me the economic and employment effects of Obamacare are another piece of the larger puzzle called Where Will the Jobs Come From? This may be the most important economic question of the next 30 years. Because this topic has been the focus of my thinking for the past few years, I could be reading more into the CBO's report than I should, but indulge me as I make a few points and then see if I can tie them together in the end.

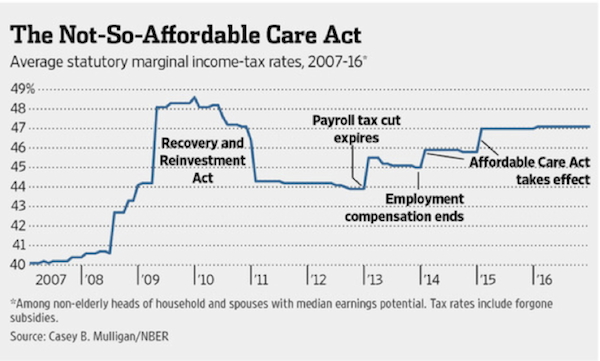

First let's look at what the report actually said. The CBO stated that the implementation of the Affordable Care Act will result in a "substantially larger" and "considerably higher" reduction in the labor force than the "mere" 800,000 the budget office estimated in 2010. The overall level of labor will fall by 1.5% to 2% over the decade, the CBO figures. The revision was evidently driven by economic work done by a professor at the University of Chicago by the name of Casey Mulligan. (When you do a little research on Professor Mulligan and look past the multitude of honors and awards, you find people calling him the antithesis of Paul Krugman. I must therefore state for the record that I already like him.) For you economics wonks, there is a very interesting interview with Professor Mulligan in the weekend Wall Street Journal. For those who don't go there, I will summarize and quote a few salient points.

Let's be clear. This report and Mulligan's research do not say Obamacare destroys jobs. What they suggest is that Obamacare raises the marginal tax rates on income, and to such an extent that it reduces the rewards for working more hours for marginally higher pay at certain income levels. The chart below does not pertain to upper-income individuals but rather to those at the median income level.

What Mulligan's work does demonstrate is that the loss of government benefits has the same effect on an individual as a tax increase. If you lose a government subsidy because you work more hours, then for all intents and purposes it is the same as if you were taxed at a higher rate. Quoting now from the WSJ piece:

Instead, liberals have turned to claiming that ObamaCare's missing workers will be a gift to society. Since employers aren't cutting jobs per se through layoffs or hourly take-backs, people are merely choosing rationally to supply less labor. Thanks to ObamaCare, we're told, Americans can finally quit the salt mines and blacking factories and retire early, or spend more time with the children, or become artists.

Mr. Mulligan reserves particular scorn for the economists making this "eliminated from the drudgery of labor market" argument, which he views as a form of trahison des clercs [loosely translated, "the betrayal of academic economists" – JM]. "I don't know what their intentions are," he says, choosing his words carefully, "but it looks like they're trying to leverage the lack of economic education in their audience by making these sorts of points."

A job, Mr. Mulligan explains, "is a transaction between buyers and sellers. When a transaction doesn't happen, it doesn't happen. We know that it doesn't matter on which side of the market you put the disincentives, the results are the same.... In this case you're putting an implicit tax on work for households, and employers aren't willing to compensate the households enough so they'll still work." Jobs can be destroyed by sellers (workers) as much as buyers (businesses).

He adds: "I can understand something like cigarettes and people believe that there's too much smoking, so we put a tax on cigarettes, so people smoke less, and we say that's a good thing. OK. But are we saying we were working too much before? Is that the new argument? I mean make up your mind. We've been complaining for six years now that there's not enough work being done.... Even before the recession there was too little work in the economy. Now all of a sudden we wake up and say we're glad that people are working less? We're pursuing our dreams?" The larger betrayal, Mr. Mulligan argues, is that the same economists now praising the great shrinking workforce used to claim that ObamaCare would expand the labor market.

Paul Krugman interprets the CBO estimates to mean a loss of the number of hours that would be equivalent to the loss of 2 million jobs. The Wall Street Journal sees that same number as equivalent to 2.5 million jobs. Professor Mulligan's research suggests that they are still off by a factor of two and that it could be closer to 5 million job equivalents.

That means a drop in potential GDP growth of somewhere between 0.5% and 1% per year. A small price to pay for universal healthcare, suggests Krugman. I would personally see it as a large price to pay for structuring healthcare reform the wrong way. That we need healthcare reform and that we as a country want it to be universal is clear. But the CBO report makes it evident that there is a hidden economic cost to the country in the way healthcare reform is currently structured. Dismissing potential GDP growth loss of 0.5% per year as "not all that much" is simply not intellectually sufficient.

(And that is taking Krugman's estimate of 0.5% to be the actual negative effect. There are other economists who can produce credible estimates that are much higher, but for the purposes of this letter Krugman's lower estimate will do.)

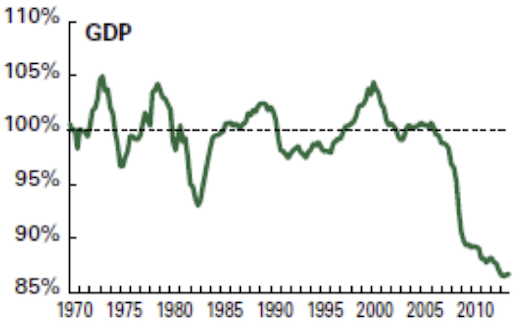

Doug Henwood over at The Liscio Report produced some fascinating research this week on what it has meant for our economy to be growing at a lower rate since 2007. In another report, the CBO offered its own estimate of future growth, which the normally sanguine Henwood thinks has the potential to make us complacent. Let's jump right to his impact paragraphs (emphasis mine):

Another way to measure where GDP is relative to where it "should" be is by comparing the actual level to its long-term trend. [That's what's graphed below.] This technique shows the economy in a much deeper hole than the CBO does.

By this method, actual GDP at the end of 2013 was 86.7% of its trend value. That's actually 3 points below where it was when the recession ended. Consumption was 87.4% of its trend value; investment, 75.1%; and government, 84.5%. (Note that government, despite perceptions to the contrary, has been falling, not rising, relative to its trend.)

These are huge gaps. In nominal dollar terms, per capita GDP is $8,278 below its 1970–2007 trend. Using the CBO's less dramatic gap estimate works out to an actual per capita GDP $2,141 below its potential. Either way, that's a lot of money. One way of reconciling the $6,137 disparity between the figures derived from CBO's method and the trend method is by pointing to the long-term economic damage done by the financial crisis and recession.

The hit to investment, productivity, and labor force participation is enormous and long-lived. To put that $6,137 number in perspective, it's very close to the per capita GDP of China. That is not small, and if the CBO is even half right, it's not going away any time soon.

By the way, Casey Mulligan argues in his 2012 book, The Redistribution Recession, that the expansion of the welfare state through the surge in food stamps, unemployment benefits, disability, Medicaid, and other safety-net programs was responsible for about half the drop in work hours since 2007, and possibly more.

The CBO is de facto admitting that the increase in the entitlement spending due to Obamacare is going to reduce GDP. If Mulligan's larger projection is right, we could lose roughly 10% of GDP potential over the next decade. That means the pie in the future will be smaller by 10%. That is a huge difference, not an inconsequential one. It means tax revenues needed to pay for government benefits will be 10% smaller. I am not arguing for or against whether such benefits are a proper expenditure of money; I'm simply saying that we cannot ignore the economic consequences simply because they may be politically inconvenient.

Think about this for a moment. We have lost the equivalent of Chinese per-person GDP in the space of seven years as a result of policy choices made by both Republican and Democratic administrations and due to the financial repression visited upon us by the Federal Reserve – which, by the way, has created multiple bubbles. The way we structure our policy decisions has consequences beyond the obvious.

Rather than immediately jumping to some kind of conclusion on employment that simply offers a number and doesn't offer insight, I want us to look at the larger picture of work and what we get paid for it. We are rightly concerned in the developed world about the concentration of income and wealth in the top fraction of the population. When 85 people own 46% of the world's wealth, as we've repeatedly heard the past few weeks, what does this portend for the future?

To continue reading this article from Thoughts from the Frontline – a free weekly publication by John Mauldin, renowned financial expert, best-selling author, and Chairman of Mauldin Economics – please click here.

© 2013 Mauldin Economics. All Rights Reserved.

Thoughts from the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.MauldinEconomics.com.

Please write to subscribers@mauldineconomics.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.MauldinEconomics.com.

To subscribe to John Mauldin's e-letter, please click here: www.mauldineconomics.com/subscribe

To change your email address, please click here: http://www.mauldineconomics.com/change-address

Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.