Thoughts from the Frontline: A Bubble In Complacency

- Patrick Cox

- |

- May 25, 2014

- |

- Comments

I and many others are still trying to digest the massive amount of useful and original information that was offered at last week’s Strategic Investment Conference. In this week’s letter I want to recap some of what I learned but do so in a little different manner. I find it quite instructive to listen to and read what other people have to say about their takeaways from the conference. I have come across several very good summaries and reviews that I am going to excerpt rather liberally, along with sharing some of my own thoughts.

Nearly everyone noted that there was somewhat of a divide in the opinions as to whether things in the US and global economies are getting better or getting worse. Upon reflection, I think that John Nicola (my Canadian partner of the eponymous wealth management firm, who sent me his comments, which I will use freely below) had it right. If we all examine a glass that is filled up to the mid-level, some of us will describe it is half-full, and others will describe it as half-empty. And of course there is plenty of data to back up either the optimistic or the pessimistic position.

The simple fact is that we are in what I call a Muddle Through Economy. Things aren’t terrible, but they are not great, either. We’ve come through a devastating Great Recession caused by a crisis in the financial sector. It is quite typical for the effects of such a crisis to linger for a decade or more. So compared to where we were at the bottom of the Great Recession, the glass is half-full. But compared to the expectations we have for economic recovery and the resumption of vibrant growth, half-full seems like an exaggeration. And for many people, the glass is simply empty, while for others it is spilling over.

Steve Moore sent me a graph demonstrating that net new jobs since the onset of the Great Recession have come, in large measure, from the energy sector. Those are generally high-paying jobs, but the rest of the country and many industries have not done so well. According to a new report from the National Employment Law Project, the quality of the jobs that have been created since the end of the last recession does not match the quality of the jobs that were lost during that recession:

- Lower-wage industries constituted 22 percent of recession losses, but 44 percent of recovery growth.

- Mid-wage industries constituted 37 percent of recession losses, but only 26 percent of recovery growth.

- Higher-wage industries constituted 41 percent of recession losses, and 30 percent of recovery growth.

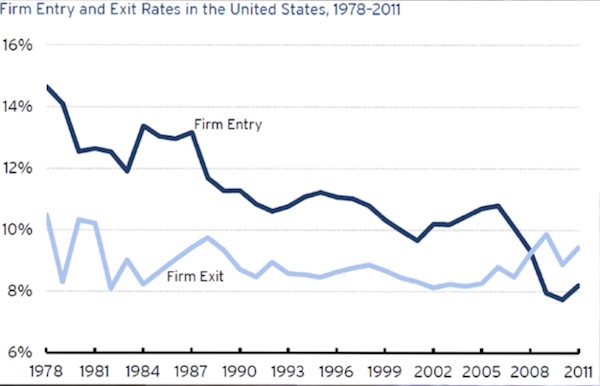

Yes, unemployment is down, but so is labor participation, and the simple fact is that outside of the petroleum sector new jobs are not being created to anyone’s satisfaction. In my presentation at the conference I showed a chart that illustrates the fact that we are losing businesses faster than we are creating new ones – an unprecedented statistic. This is a glass not only half-empty but leaking:

Richard Lehmann and Marty Fridson attended the conference and wrote an exceptionally well-done review in Forbes. (I was honored that they attended.) They started with the optimistic note that my good friend David Rosenberg offered as the very first speaker at the conference:

David Rosenberg, chief economist and strategist at Gluskin Sheff, sees reduced unemployment as a positive sign for the economy, despite objections that the decline in the unemployment rate reflects an unusually low participation rate. For one thing, says Rosenberg, the number of discouraged workers is down by 40% from the peak. At the margin, he adds, people are choosing to stay out of the work force in response to government incentives to remain idle.

The number of people collecting disability benefits, using food stamps, or collecting welfare payments is at a record high. Three-quarters of the reduction in the participation rate, says Rosenberg, is attributable to demographics, as the number of Baby Boomers reaching age 65 is rising dramatically.

Rosenberg further notes that unfilled job openings are at a five-year high. The U.S. government is granting fewer visas, college students are graduating without marketable skills, and the skills of many workers who have been laid off for long periods have become outdated. If all of the current openings could be filled, unemployment would drop to 4%.

The bottom line for Rosenberg is that the current recovery/expansion is in the fourth inning. Business cycles never die from old age, he maintains. He puts the probability of recession in 2015 at close to zero….

Richard Yamarone, senior economist at Bloomberg Economics, takes a less sanguine view on unemployment than David Rosenberg. He argues that the type of jobs being created makes a difference. Currently, job creation is skewed toward low-skill, low-income categories. To circumvent the Affordable Care Act’s requirement to provide health care to full-time employees, retailing, health care and food service employers are cutting workers’ hours. Consequently, new jobs are being created for people who now have to hold multiple part-time jobs, but that does not constitute a genuine increase in employment or GNP.

Yamarone’s view of the labor market leads to a comparatively bearish outlook on the economy. Since GDP began to be reported in 1947, he points out, the U.S. economy has slid into recession every time GDP growth has fallen to 2%, a level below which it currently stands.

Yamarone also reports unfavorable readings in four of five special data series that he has found to be accurate indicators of the economy—dining out, casino gambling, jewelry and watches, cosmetics and perfumes, and women’s dresses….

Lacy Hunt, executive vice president of Hoisington Investment Management, contends that the Fed’s strategy for boosting the economy is not working. Little wealth effect (the tendency of people to step up their spending when their wealth increases) has been observed. Hunt explains that the monetary policy cannot influence the economy unless the market rate of interest (represented by the Baa corporate bond yield) is below the natural rate of interest (the nominal rate of GDP growth). That has not been the case at any point during the recovery. Until it is, Hunt contends, consumers will have no incentive to take on debt to finance spending and economic growth will consequently remain sluggish.

Lacy believes all major developed countries are going to have deal with their “Minsky moments,” because not enough of their overall debt is productive. When all debt (government, corporate, and personal) is added up, it equals 350% of GDP in the US and 440% in developed countries on average. Lacy kept emphasizing his conviction that any number over 275% results in limited growth and eventual deflation.

David Zervos expects the Fed to keep interest rates low until it gets either inflation or solid economic growth. In fact, the private sector has been growing at more than 3% annually since 2010. His view is that savers will continue to be punished, because the interest rates they receive will remain artificially low. Gary Shilling was decidedly more upbeat and felt solid economic growth is at hand. (Nicola)

I noted an interesting theme in several speeches. Millennials, Jeff Gundlach noted, are different. They are less acquisitive. Neil Howe also talked about this and noted that we are in the middle of a “Fourth Turning,” which is a typically an isolationist period. He also notes that Millennials (1981-1994) like to rent (not just homes but cars, recreational property, clothing etc.) They have less stress, often live at home with their parents, and are looking for meaningful work where they can be mentored. Ian Bremmer echoed Neil’s theme and stated that one of the important geopolitical trends at play is that the US is becoming more isolationist.

And Ian, who is a geopolitical analyst with the Eurasia Group and an NYU professor, also noted that the huge increase in US oil and gas production means much less dependence on Mideast oil and suggests that the US will eventually become a net energy exporter. As a result the US will not want to get entangled in the Middle East, and this reluctance will increase the risks in that region. Regarding the Ukraine situation, Ian feels the US made a mistake in trying to put sanctions on Russia that it couldn’t back up (a sentiment echoed by several speakers). He also expects Israel and the US to make a deal with Iran in the next twelve months – and if they do, Iran will bring 1.5 million additional barrels of oil to world markets. The big winner of the Ukraine crisis? Ian argued very cogently that it’s China. Ian continues to impress me every time I hear him or talk with him.

Jeffrey Gundlach was quite negative on US housing but positive on multifamily rental real estate, because rentals increase as home ownership drops. Home ownership has dropped from 69% of households to 65%. One well-known US investor, Sam Zell, expects it to drop to 55%. A 1% drop means 1.2 million additional households are looking for rental accommodations. Another speaker had mentioned that over 1 million millennials are living with their parents, which is a major factor in the reduction of household formation. Jeffrey does not like the risks associated with high-yield bonds but does like emerging-market debt and mortgages on a risk-adjusted basis. He expects the US to see deflation before inflation makes a comeback. (Nicola, et al.)

Grant Williams made a comment during a discussion about global markets that I thought was excellent. There is a bubble, he asserted, in complacency. He is very concerned with shadow banking in China (currently 60% of GDP) and with unaffordable housing. Many investors in wealth management products (WMPs) will lose a lot of money unless government bails them out. Overall there is a credit bubble in China. Japan is even worse at almost 250% of GDP for government debt alone. Grant feels Abenonmics is not working and that little structural reform is occurring. Notwithstanding that, Japanese 10-year bond rates dropped from almost 1% to 0.6% in the last year. Kyle Bass stated that he thinks Japanese 10-year rates will rise to 2.5%.

There was a very consistent theme in a number of presentations: no one is sanguine about China. The comments ranged from quite concerned to worried to very alarmed. (Next week this letter will focus on China.) There was not much that was positive to be said about Europe and Japan. Thoughts on the emerging markets varied a great deal and at the end of the day were very specific to particular markets.

John Nicola offered this summary to his clients:

As you can see, there are definitely two camps but also some common themes. Let me wrap up with our own thoughts on what we learned and how it might change our investment strategies.

There are still many headwinds to getting inflation to rise. One of the main issues is considerable slack in global labor markets. With emerging markets looking to improve their own standards of living, this spare capacity will likely be with us for many years. Overall it should continue to provide deflationary pressure on wages.

For a large part of the twentieth century the developed world experienced real growth of 3%+ per year. Many countries now have flat or declining populations, and all of them are aging. Looking forward, the developed world would be doing well if it were to realize real growth of 2% annually. Global growth will be driven by developing nations.

The impact of shale oil and gas is a game changer for the US both politically and economically. When this is combined with the US having the best demographic profile of any developed nation, it becomes an important part of any portfolio.

Long-term interest rates have been in a relatively narrow range for the last couple of years, and this may continue for some time even as QE is reduced or eliminated. Even when rates rise they may not get to the “real” return levels of the past when long-term government bonds earned between 2-3% after inflation. At some point rates will rise, and we need to design portfolios to prepare for that. But the increases may take longer than many forecasters expect and be more muted as well.

Now let’s turn to a blog by Chris Bailey, who gave his readers ten take-away thoughts from the second day of the conference. I thought his wrap-up was well-done and somewhat different from the views mentioned above.

1. Trust within the economic system was a sub-theme with Dylan Grice noting on the regressive/divisive nature of QE that Central Banks “can only cheat ... because people trust” and that a yield statistic should be considered a trust indicator ... but that the risk with QE was that “if you weaken the currency, you weaken society, you weaken trust.”

2. Talking about yields... Lacy Hunt noted that we have not seen the spread between corporate bonds and nominal GDP be negative for over 30 years ... but there was a real risk that it would happen this year. He noted this was reflective of a world with declining money velocity and a nominal GDP number “not enough or top-line growth.”

3. Geo-political troubles and challenges in the world were well captured by Newt Gingrich who noted from a US perspective that the world is “much harder, denser than thought... we are more limited than we think we are ... our opponents get to play too.” Neil Howe noted that “the fourth turning” (which runs until c. the mid 2020s) generally sees a rise in isolationism. Dylan Grice showed some upturns in capital controls/protectionism (from a very low level) were occurring.

4. Debt levels around the world were a constant theme. Lacy Hunt noted that above a (combined) 275% public/private debt level “bad things happen” (guess where almost all large economies are...). Paul McCulley said that a sovereign country like the United States could not have a public debt crisis because it retained the capability to print... although clearly this could lead to other issues.

5. The role of government was much debated. John Mauldin said that one of his biggest questions was “can governments destroy ... quicker than humans can create.” Newt Gingrich divided everyone in both government and corporate life between pioneers, prison guards, champions and prisoners. Dylan Grice noted he is preferring companies in sectors with less government intervention capability.

6. Neil Howe noted many attitude links between the 1930s and this decade covering pessimism, worries about inequality, distrust in the elites, retreat from globalism, a new desire for community and declining personal risk-taking.

7. Still there is hope. George Gilder said that “creativity always comes as a surprise” whilst John Mauldin talked about the need to evolve yourself into a future-looking homo rationalis with the scope for positive trends across mobile internet, automation, internet of things, robotics, renewals and advanced materials (amongst others) building an exponentially more attractive future.

8. Attractive future themes and traits across all sectors were are those that speak digitally, virtually, from a mobile perspective or personally as per Newt Gingrich. Stephen Moore talked about the importance of “more oil and gas in North Dakota than in Saudi Arabia” and noted ex-oil/gas employment growth had been negative.

9. Whether there a rising capital shortage was a question posed by Dylan Grice, and in such a world “gold is capital” and a focus on high-ROCE companies makes sense.

10. “Millennial[s] come of age in the crisis” – and as new consumers. Neil Howe noted less risk-taking and independence plus a greater friends/social orientation has implications for most sectors from autos (fewer drivers) to housing (more multi-generational houses, less need for large personal space) to advertising strategies (“quantified self,” “blanding of culture”).

And Martin Fridson and Richard Lehmann concluded with the following:

To make sure we did not go away too happy, the conference wrapped up with Ian Bremmer, Anatole Kaletsky and Niall Ferguson giving a world geopolitical outlook that focused on the risks and uncertainties we still face. This nuanced much of the positive outlook given earlier in the conference by John Mauldin, Pat Cox, George Gilder and Newt Gingrich.

No, the conference was not the World Economic Forum, but at times, it felt like that was where we were. And then, for those who don’t ski, San Diego in May is way nicer than Davos in January.

This does not even take into account the fabulous and powerful presentation by Pat Cox, which took us back into the history of alchemy and showed that almost every major breakthrough in medicine and healthcare was initially opposed by the establishment and ignored by other doctors. Newt Gingrich’s argument about how the “prison guards of the past” are slowing the advances of healthcare and new life-saving medicines re-emphasized that point. George Gilder presented his ideas on a new model for economic theory (which I am enamored with). We extended the conference by one-half day to allow for a few more speakers, and I worked hard to pull together a wider set of topics and views.

Each year we ask ourselves how we can make the conference any better, and each year we seem to do so. But this year set a very high bar for next year’s event, which by the way will be a little earlier in the year and once again in San Diego, April 28 – May 1. Set your calendar. You can buy a set of the 2014 audio CDs and/or MP3 files and listen to the speeches at your leisure by going to this link.

Trequanda, Rome, Nantucket, New York, and Maine

I leave this Thursday evening for Italy. We will spend the first night in Rome, where, randomly, my very good friend Steve Cucchiara (of Windhaven Fund fame) will also find himself, and we will take our kids to dinner that evening. Then we’re off the next day for two weeks at the little hilltop village of Trequanda, where some friends will drop by for a few days and use the villa as a base to explore or work from. I will be starting to work on my next book. Seriously.

Then I will again be in Rome June 14-17, where I will be joined by Christian Menegatti from Roubini Global Economics. We plan to spend time with various businessmen, investors, central bankers, and politicians to get a better understanding of what is really unfolding in Italy. We are actively looking for people to visit and especially for business associations with whom we can meet. Drop me a note if you’re interested.

Drugs, Prostitution, and Smuggling

I was recently sent this note by Cliff Draughn, who will be joining me for a few days in Trequanda. File this under “you can’t make this up.” This shows the extremes to which politicians in Europe will go to “adjust” their accounting to meet treaty requirements. Greece used Goldman Sachs, but now Italy will look to hookers and drugs. This is just too juicy, and I will have fun discussing it in Italy.

Drugs, prostitution and smuggling (ie Hookers & Blow) will be part of Italy’s GDP as of 2014, and prior-year figures will be adjusted to reflect the change in methodology, the Istat national statistics office said today. The revision was made to comply with European Union rules, it said.

Prime Minister Matteo Renzi, 39, is committed to narrowing Italy’s deficit to 2.6 percent of GDP this year, a task that’s easier if output is boosted by portions of the underground economy that previously went uncounted. Four recessions in the last 13 years left Italy’s GDP at 1.56 trillion euros ($2.13 trillion) last year, 2 percent lower than in 2001 after adjusting for inflation.

The punch line: “Even if the impact is hard to quantify, it’s obvious it will have a positive impact on GDP,” said Giuseppe Di Taranto, economist and professor of financial history at Rome’s Luiss University. “Therefore Renzi will have a greater margin this year to spend” without breaching the deficit limit, he said.

It will be interesting to see how much they think drugs and sex will add to the economy, and whether they publish the basis for their accounting. I suppose that next they will try to account for the rest of the massive underground economy in Italy. They are also quantifying other elements such as research and development costs and arms sales in the effort to increase nominal GDP. I wonder whether France will consider including the value added by the mistresses of politicians? Just asking…

Have a great Memorial Day weekend. I hope that a few of my kids show up. And then it’s off to Italy. Ivo the Gardener will be cooking at least twice. Last time he came and made pasta and everything to go with it. I swear that his is the best lasagna ever. And we’ll enjoy other cooks and some fabulous restaurants. Of all the food in the world, countryside Italian is my favorite cuisine. Hard to find it anywhere else as good as it is in Tuscany. Ciao until next week…

Your ready for my daily caprese fix analyst,

John Mauldin, Editor

subscribers@mauldineconomics.com